|

市场调查报告书

商品编码

1940730

美国印刷标籤:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)United States Print Label - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

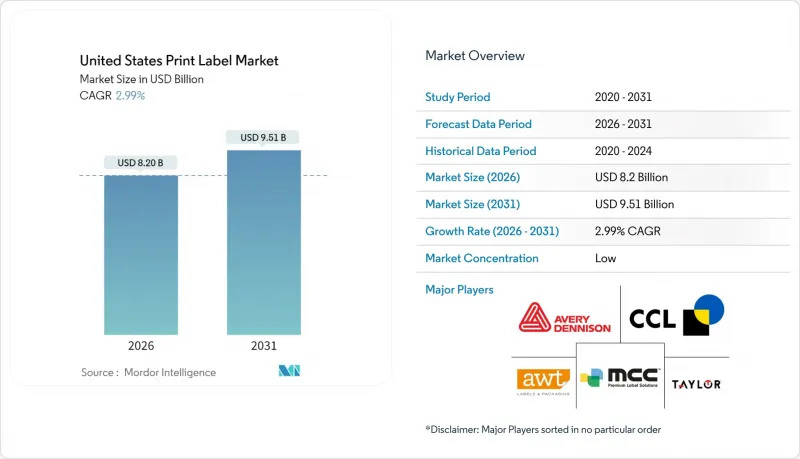

美国印刷标籤市场预计将从 2025 年的 79.6 亿美元成长到 2026 年的 82 亿美元,到 2031 年达到 95.1 亿美元,2026 年至 2031 年的复合年增长率为 2.99%。

食品、医疗保健和电子商务行业的强劲需求支撑着行业成长,而数位印刷和永续性正在重塑技术选择、材料和经营模式。柔版印刷仍拥有庞大的用户群,但随着可变数据功能、小批量生产的经济效益以及序列化法规的推动,数位化工作流程正日益普及,敏捷印刷机也因此受益。加州等地的延伸生产者责任制 (EPR) 立法正在加速无底纸、可回收和生物基结构的推广。技术纯熟劳工短缺推动了自动化投资,而原材料成本的波动则促使整个价值链上的库存管理和采购发生变化。随着大型加工商利用规模经济来确保供应、资金筹措研发并部署混合印刷平台以满足物流通路对智慧标籤日益增长的需求,产业整合仍在继续。

美国印刷标籤市场趋势与洞察

数位印刷技术的普及

对可变数据日益增长的需求正推动印刷企业向数位印刷机转型,这些印刷机能够显着缩短设定时间并支援ERP直接PDF工作流程。东芝BX410T系列于2025年1月发布,整合了双核心处理器和Linux作业系统,可实现无人驾驶操作和云端设备管理,从而缓解技术纯熟劳工短缺问题。製药品牌正在利用这些系统进行个体级序列化,而化妆品品牌则利用按需色彩柔软性来生产季节性产品。远端韧体更新和预测性维护提高了运转率,促使企业将资本投资决策转向数位平台。随着早期采用者透过减少废弃物和缩短宣传活动週期获得投资回报,美国印刷标籤市场越来越青睐具备混合或全数位化能力的印刷企业。

医疗和化妆品标籤的采用趋势

2024年1月,FDA最终确定了《病患药品资讯规则》,强制要求采用单页格式和标准化字体,导致学名药需要定期更换标籤。同时,化妆品品牌正在加速采用防篡改功能和高端表面处理,以在零售货架上脱颖而出。为此,Brady公司在2024年将5.1%的营收投入研发,重点在于拓展其水溶性实验室标籤和RFID溯源解决方案。医疗和美容行业的客户重视加工商在合规基材、微字体清晰度和特殊黏合剂方面的专业知识,这使得美国印刷标籤市场的平均利润率高于一般食品标籤。

纸张和树脂原料成本波动

纸浆价格波动和石化产品供应中断对加工商的利润率带来压力,尤其是那些在价格飙升前签订的长期合约。虽然垂直整合型公司可以透过购买期货或利用自有薄膜挤出设备来对冲风险,但小规模的独立公司往往被迫在合约期间调整库存或重新谈判条款。此外,美国标籤与包装协会 (Associated Labels & Packaging) 2024 年西海岸试验研究发现,对纸衬回收的限制增加了偏远地区造纸厂的运输成本。成本的不确定性促使企业试验使用更轻的基材和无衬纸解决方案,但材料替代可能会影响性能,迫使品质保证团队在紧迫的时间内检验任何变更。

细分市场分析

到2025年,柔版印刷将占美国印刷标籤市场37.02%的份额,主要得益于高速生产线和经济高效的聚合物印版,尤其适用于食品和饮料长幅印刷。凹版印刷虽然规模较小,但预计到2031年将维持3.76%的复合年增长率,这主要得益于高端葡萄酒、化妆品和特种化学品品牌对照片级和金属光泽效果的需求。美国数位静电照相和UV喷墨标籤市场目前小规模,但随着製药和精酿饮料买家对批次序列化和SKU特定图案的需求,预计2024年其装机量将实现两位数增长。提供混合印刷机的加工商可以在类比和数位工位之间无缝切换,从而减少废弃物并缩短交货时间。

拥抱电子商务的品牌所有者正在进行小规模的宣传活动,这些活动不会占用大量的柔版印刷滚筒。这使得数位印刷能够在不影响现有柔版印刷量的情况下增加收入,从而保护印版投资,同时还能利用动态QR码和个人化功能。网版印刷在一些细分领域仍然发挥作用,例如厚光油层和触感效果,而胶印则专注于高端酒类饮品的精准色彩匹配。凸版印刷现在主要应用于生产高利润礼品和文具产品的手工工作室。工艺的多样性赋予了加工商在资本投资谈判中更大的优势,并支持他们为美国印刷标籤市场的跨国客户提供全方位提案。

截至2025年,由于其多功能性和与自动化贴标机的兼容性,压贴式捲标将占据美国印刷标籤市场52.05%的份额。然而,受生产者延伸责任制(EPR)的减废弃物目标和可衡量的生产效率提升(甚至每托盘标籤容量提升40%)的推动,无底纸捲标预计将以4.26%的复合年增长率增长。对于使用传统生产线的主流啤酒瓶装商而言,湿贴式标籤仍然是一种经济高效的选择。同时,精酿啤酒厂正在采用收缩套标和压敏胶标籤,以适应特殊瓶型和小批量生产。多组件标籤在医疗诊断和航太零件追踪等监管链场景中尤其有用。

套模技术应用于耐用消费品和工业桶,这些产品需要具备耐刮擦性,使用寿命超过五年。收缩和拉伸套可为饮料、营养补充品和家用清洁剂产品提供商店促销「特色图案」和「防篡改」标记。随着零售商收紧回收标准,加工商正在提供将浮动套标薄膜与可水洗油墨相结合的解决方案,这种油墨在PET回收过程中能够分离。因此,研发团队的材料工程师与印刷商合作,致力于实现美国印刷标籤市场所需的附着力、不透明度和永续性目标。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 数位印刷技术的普及

- 医疗和化妆品标籤的采用趋势

- 对电子商务和物流标籤的需求

- 基于生产者延伸责任制(EPR)的无底纸/可回收标籤过渡

- 用于供应链追溯的智慧/物联网标籤

- 近岸外包将推动近期VDP需求。

- 市场限制

- 恶劣环境下的耐久性极限

- 纸张和树脂原料成本波动

- 熟练窄幅印刷工人短缺

- 回收流碎片化

- 产业价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 宏观经济因素如何影响市场

第五章 市场规模与成长预测

- 透过印刷工艺

- 胶印

- 凹版印刷

- 柔版印刷

- 萤幕

- 凸版印刷

- 静电照相术

- 喷墨

- 按标籤格式

- 湿胶标籤

- 感压标籤

- 无底纸标籤

- 多页追踪标籤

- 套模标籤

- 缩水/拉伸套

- 按最终用户行业划分

- 食物

- 饮料

- 卫生保健

- 化妆品

- 家用

- 工业(汽车、化工、耐久性消费品)

- 后勤

- 其他终端用户产业

- 依材料类型

- 纸

- 塑胶薄膜(PP、PET、PE)

- 特种和永续表面

- 其他材料类型

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Avery Dennison Corporation

- Multi-Color Corporation

- Fort Dearborn Company LLC

- AWT Labels & Packaging

- Brady Corporation

- RR Donnelley & Sons Company

- Taylor Corporation

- Weber Packaging Solutions

- Grand Rapids Label

- DRG Technologies Inc.

- CCL Industries Inc.

- Constantia Flexibles Group GmbH

- Label Masters LLC

- 3M Company

- Resource Label Group LLC

- Fortis Solutions Group LLC

- Brook & Whittle Holdings Corp.

- Inland Label & Marketing Services LLC

第七章 市场机会与未来展望

The United States print label market is expected to grow from USD 7.96 billion in 2025 to USD 8.2 billion in 2026 and is forecast to reach USD 9.51 billion by 2031 at 2.99% CAGR over 2026-2031.

Robust demand from food, healthcare, and e-commerce applications anchors growth, while digital printing and sustainability mandates reshape technology choices, materials, and business models. Flexography retains a sizeable installed base, yet digital workflows gain ground as variable-data, short-run economics, and serialization rules favor agile presses. Linerless, recyclable, and bio-based constructions accelerate through Extended Producer Responsibility (EPR) legislation in states such as California. Automation spending offsets skilled-labor shortages, and raw-material cost volatility triggers inventory and sourcing shifts across the value chain. Consolidation continues as scale helps leading converters secure supply, fund R&D, and deploy hybrid press platforms that address emerging smart-label needs across fulfillment corridors.

United States Print Label Market Trends and Insights

Digital Print Technology Penetration

Demand for variable data pushes converters toward digital presses that slash makeready times and support ERP-direct PDF workflows. Toshiba's BX410T series, launched in January 2025, integrates a dual-core processor and Linux operating system, enabling driver-free operation and cloud fleet management that mitigates skilled-labor gaps. Pharmaceutical brands leverage these systems for unit-level serialization, while cosmetics lines exploit on-demand color flexibility to run seasonal variants. Remote firmware updates and predictive maintenance improve uptime, tipping capex decisions toward digital platforms. As early adopters demonstrate ROI through reduced waste and quicker campaign cycles, the United States print label market increasingly favors converters with hybrid or fully digital capacity.

Healthcare and Cosmetics Label Uptake

In January 2024, the FDA finalized Patient Medication Information rules that enforce single-page formats and standardized typography, creating recurrent relabeling cycles for generic drugs. Cosmetics brands simultaneously escalate tamper-evident and premium finishes to stand out on retail shelves. Brady Corporation responded by expanding water-dissolvable laboratory labels and RFID-enabled traceability solutions, underpinned by a 5.1% R&D-sales ratio in 2024. Healthcare and beauty accounts thus reward converters skilled in compliant substrates, micro-font legibility, and specialty adhesives, lifting average margins compared with commodity food labels across the United States print label market.

Volatile Paper and Resin Input Costs

Pulp price swings and petrochemical disruptions squeeze converter margins, especially on long-term contracts signed before spike events. Vertically integrated players hedge exposure by forward-buying or leveraging in-house film extrusion, whereas small independents often ration inventory or renegotiate terms mid-cycle. Paper-liner recycling constraints add hauling fees when mills are distant, as documented in Associated Labels & Packaging's 2024 West Coast pilot study. Cost uncertainty encourages substrate light-weighting and linerless trials, but material substitutions can compromise performance, pressing QA teams to validate every change under tight timelines.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce and Logistics Label Volumes

- Smart/IoT Labels for Supply-Chain Traceability

- Skilled Narrow-Web Labor Shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flexography commanded 37.02% of the United States print label market share in 2025, supported by fast line speeds and cost-effective polymer plates for long food and beverage runs. Gravure, though smaller, is on track for a 3.76% CAGR through 2031 as luxury wine, cosmetic, and specialty-chemical brands demand photographic quality and metallic finishes. The United States print label market for digital electrophotography and UV inkjet remains modest currently, yet installs grew double-digit in 2024 because pharmaceutical and craft-beverage buyers need serialization or SKU-specific artwork on every lot. Converters offering hybrid presses switch seamlessly between analog and digital stations, cutting waste and turnaround times.

Brand owners embracing e-commerce launch micro-campaigns that rarely fill a flexo cylinder. Digital thus captures incremental revenue without cannibalizing base flexo volumes, preserving plate investments while unlocking dynamic QR code and personalization features. Screen printing retains niche roles for heavy varnish layers and tactile effects, whereas offset lithography serves precise color-match jobs in premium spirits. Letterpress now survives mainly in artisanal studios catering to high-margin gift and stationery products. Process diversity gives converters bargaining power on capex buys and supports full-line service pitches to multinational clients across the United States print label market.

Pressure-sensitive rolls occupied 52.05% of the United States print label market in 2025 due to universal applicability and automated applicator compatibility. However, linerless reels are forecast to log a 4.26% CAGR, spurred by EPR-driven waste targets and measurable throughput gains, sometimes fitting 40% more labels per pallet. Wet-glue remains cost-effective for mainstream beer bottlers using legacy lines, but craft brewers adopt shrink sleeves and PS because they accommodate unique bottle shapes and small batches. Multi-part sets flourish in chain-of-custody scenarios, particularly medical diagnostics and aerospace part tracking.

In-mold options appeal to durable goods and industrial pails that require scuff resistance for product life spans exceeding five years. Shrink and stretch sleeves provide billboard graphics and tamper indication for beverage, nutraceutical, and household cleaners, where shelf appeal directly drives sell-through. As retailers enforce recyclability standards, converters pair floatable sleeve films with washable inks that separate during PET reclamation. Material engineers, therefore, sit alongside press operators in R&D teams to ensure adhesion, opacity, and sustainability targets converge within the United States print label market.

The United States Print Label Market Report is Segmented by Print Process (Offset Lithography, Gravure, Flexography, Screen, and More), Label Format (Wet-Glue Labels, Pressure-Sensitive Labels, Linerless Labels, and More), End-User Industry (Food, Beverage, Healthcare, Cosmetics, Household, and More), Material Type (Paper, Plastic Films, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Avery Dennison Corporation

- Multi-Color Corporation

- Fort Dearborn Company LLC

- AWT Labels & Packaging

- Brady Corporation

- RR Donnelley & Sons Company

- Taylor Corporation

- Weber Packaging Solutions

- Grand Rapids Label

- DRG Technologies Inc.

- CCL Industries Inc.

- Constantia Flexibles Group GmbH

- Label Masters LLC

- 3M Company

- Resource Label Group LLC

- Fortis Solutions Group LLC

- Brook & Whittle Holdings Corp.

- Inland Label & Marketing Services LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Digital Print Technology Penetration

- 4.2.2 Healthcare and Cosmetics Label Uptake

- 4.2.3 E-Commerce and Logistics Label Volumes

- 4.2.4 EPR-Driven Shift to Linerless/Recyclable Labels

- 4.2.5 Smart/IoT Labels for Supply-Chain Traceability

- 4.2.6 Near-Shoring Driving Short-Run VDP Demand

- 4.3 Market Restraints

- 4.3.1 Durability Limits in Harsh Conditions

- 4.3.2 Volatile Paper and Resin Input Costs

- 4.3.3 Skilled Narrow-Web Labor Shortages

- 4.3.4 Recycling-Stream Fragmentation

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Print Process

- 5.1.1 Offset Lithography

- 5.1.2 Gravure

- 5.1.3 Flexography

- 5.1.4 Screen

- 5.1.5 Letterpress

- 5.1.6 Electrophotography

- 5.1.7 Inkjet

- 5.2 By Label Format

- 5.2.1 Wet-Glue Labels

- 5.2.2 Pressure-Sensitive Labels

- 5.2.3 Linerless Labels

- 5.2.4 Multi-part Tracking Labels

- 5.2.5 In-Mold Labels

- 5.2.6 Shrink and Stretch Sleeves

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Healthcare

- 5.3.4 Cosmetics

- 5.3.5 Household

- 5.3.6 Industrial (Automotive, Chemicals, Durables)

- 5.3.7 Logistics

- 5.3.8 Other End-User Industries

- 5.4 By Material Type

- 5.4.1 Paper

- 5.4.2 Plastic Films (PP, PET, PE)

- 5.4.3 Specialty and Sustainable Facestocks

- 5.4.4 Other Material Types

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Avery Dennison Corporation

- 6.4.2 Multi-Color Corporation

- 6.4.3 Fort Dearborn Company LLC

- 6.4.4 AWT Labels & Packaging

- 6.4.5 Brady Corporation

- 6.4.6 RR Donnelley & Sons Company

- 6.4.7 Taylor Corporation

- 6.4.8 Weber Packaging Solutions

- 6.4.9 Grand Rapids Label

- 6.4.10 DRG Technologies Inc.

- 6.4.11 CCL Industries Inc.

- 6.4.12 Constantia Flexibles Group GmbH

- 6.4.13 Label Masters LLC

- 6.4.14 3M Company

- 6.4.15 Resource Label Group LLC

- 6.4.16 Fortis Solutions Group LLC

- 6.4.17 Brook & Whittle Holdings Corp.

- 6.4.18 Inland Label & Marketing Services LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

印刷标籤:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

印刷标籤:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 印刷标籤市场报告:按原料、印刷工艺、标籤格式、最终用途行业和地区划分(2026-2034年)

印刷标籤市场报告:按原料、印刷工艺、标籤格式、最终用途行业和地区划分(2026-2034年) 2026年全球印刷标籤市场报告北美印刷标籤市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

2026年全球印刷标籤市场报告北美印刷标籤市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 印刷组件和标籤(热转印、数位印刷、网版印刷):全球市场份额和排名、总收入和需求预测(2025-2031 年)日本印刷标籤市场规模、份额、趋势及预测(按原材料、印刷工艺、标籤格式、最终用途行业和地区),2025 年至 2033 年

印刷组件和标籤(热转印、数位印刷、网版印刷):全球市场份额和排名、总收入和需求预测(2025-2031 年)日本印刷标籤市场规模、份额、趋势及预测(按原材料、印刷工艺、标籤格式、最终用途行业和地区),2025 年至 2033 年 印刷标籤市场规模、份额及成长分析(依印刷製程、标籤格式、原料、最终用途产业、地区及细分市场预测),2025 年至 2032 年

印刷标籤市场规模、份额及成长分析(依印刷製程、标籤格式、原料、最终用途产业、地区及细分市场预测),2025 年至 2032 年 2025-2029年全球印刷标籤市场

2025-2029年全球印刷标籤市场 印刷标籤市场:按标籤格式、印刷工艺、最终用户产业和地区划分标籤印刷和贴标设备:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

印刷标籤市场:按标籤格式、印刷工艺、最终用户产业和地区划分标籤印刷和贴标设备:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)