|

市场调查报告书

商品编码

1939069

越南塑胶市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Vietnam Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

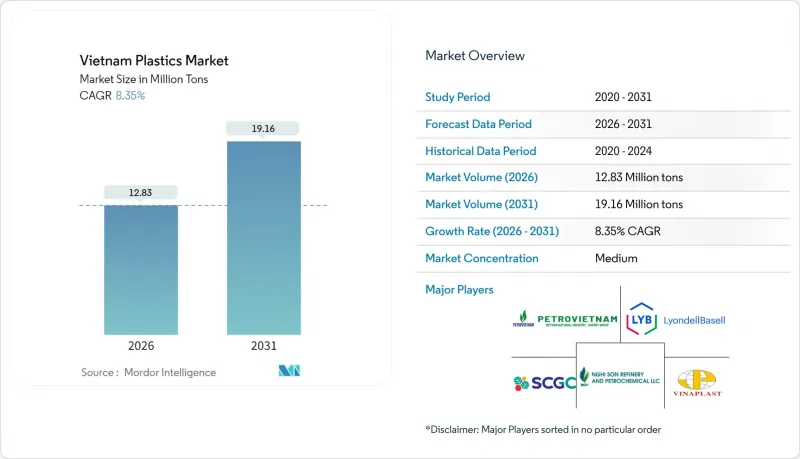

预计到 2026 年,越南塑胶市场规模将达到 1,283 万吨,高于 2025 年的 1,184 万吨。

预计到 2031 年将达到 1,916 万吨,2026 年至 2031 年的复合年增长率为 8.35%。

强劲的外商直接投资、积极的基础设施建设投入以及坚定的监管现代化,使越南成为东南亚成长最快的塑胶中心。製造业从中国转移至越南,持续扩大下游消费,而建筑投资(2025年上半年年增40%)也为管道、型材和隔热材料创造了稳定的需求。本地加工商优先考虑产量而非试验,并扩大挤出生产线以满足激增的订单。同时,永续性的迫切需求正在加速生质塑胶的普及,促使树脂供应商实现原料多元化并采用再生材料。然而,进口石脑油和丙烯仍然是成本敏感的原料。

越南塑胶市场趋势与展望

国内建筑计划稳定成长

2025年上半年,基础建设支出较去年同期成长40%,主要得益于资本执行週期从数週缩短至1-3天。 PVC管材、保温板和阻燃电缆配线架的需求激增,反映出越南作为建筑中心具有成本优势,其成本比新加坡低60-65%。资料中心计划数量超过工厂建设,推动了对无卤化合物和耐热工程树脂的需求。 10/2024/TT-BXD号通知强制要求对进口建筑材料进行品质检验,这有利于能够证明符合规定的本地加工商。这些趋势共同推动了越南塑胶市场在销售和价值方面的成长。

食品级包装和电商包装的需求快速成长

预计2024年,越南食品加工产值将达到793亿美元(年增7.4%),电子商务在都市区蓬勃发展。因此,加工商必须同时满足两方面的需求:一方面需要阻隔薄膜来延长保质期,另一方面需要轻巧的邮寄袋来降低运输成本。电子产品保护缓衝材料(截至2025年3月,零件进口量增加了29.3%)的需求进一步推动了对缓衝泡棉和模压嵌件的需求。政府鼓励使用国产包装材料的优惠政策,促使企业向国内供应商采购,刺激了对印刷、复合和多层挤出生产线的资本投资。

对进口石脑油和丙烯的高度依赖

2025年1月至7月,越南进口了超过550万吨塑胶原料,其中大部分来自中国、韩国和台湾地区。 SCG的龙山塑胶综合体于2025年8月运作,年产能为140万吨,但目前仍只能满足部分国内需求。原料成本占生产成本的60%至70%,且极易受原油价格波动的影响,这意味着原油价格飙涨时,越南的价格竞争力会受到削弱。一项计划投资7亿美元的乙烷升级项目预计将缩小这一差距,但越南与以天然气为主的海湾产油国相比,在成本上仍然具有竞争力。

细分市场分析

截至2025年,传统塑胶将维持越南塑胶市场51.10%的份额。聚乙烯和聚丙烯是市场的核心,广泛应用于日常包装、管道和模塑件等领域。凭藉成熟的供应链和较低的单位成本,这些产品继续保持销售优势。工程塑料,包括聚碳酸酯和聚酰胺,在用于输送高亮度有机发光二极体(有机发光二极体)显示器和光学模组的电子产品线中需求不断增长。受建筑业蓬勃发展的推动,聚氨酯则被用于夹芯板和家具缓衝材料。

生质塑胶目前仍属于小众市场,但预计到2031年将以12.55%的复合年增长率成长,这主要得益于品牌所有者追求永续性目标以及新法规推动了市场需求。农业残余物可作为潜在的淀粉原料,但由于认证障碍和高昂的价格,扩大生产规模仍然困难重重。然而,一项主导的试验计画表明,越南具有成为未来生物聚合物生产中心的潜力,并预示着2027年及以后将迎来转折点。

越南塑胶市场报告按类型(传统塑胶、工程塑胶、生质塑胶)、技术(吹塑成型、挤出成型、射出成型及其他技术)和应用(包装、电气和电子设备、建筑施工、汽车和运输设备、家居用品、家具和床上用品及其他应用)进行细分。市场预测以吨为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 国内建筑计划稳定成长

- 食品和电商包装需求快速成长

- 增加下游树脂加工产业的外国直接投资

- 汽车和电子产业向越南的转移速度迅速加快

- 政府对再生树脂的奖励措施

- 市场限制

- 对进口石脑油和丙烯的高度依赖

- 反对一次性塑胶製品的环保行动活性化

- 快速消费品产业中来自生物基替代品的竞争日益加剧

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争程度

- 原料分析

第五章 市场规模与成长预测

- 按类型

- 传统塑料

- 聚乙烯

- 聚丙烯

- 聚苯乙烯

- 聚氯乙烯

- 工程塑料

- 聚氨酯

- 氟树脂

- 聚酰胺

- 聚碳酸酯

- 苯乙烯共聚物(ABS 和 SAN)

- 热塑性聚酯

- 其他工程塑料

- 生质塑胶

- 传统塑料

- 透过技术

- 吹塑成型

- 挤出成型

- 射出成型

- 其他技术

- 透过使用

- 包装

- 电气和电子

- 建筑/施工

- 汽车和运输设备

- 家居用品

- 家具和床上用品

- 其他用途

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- AGC Inc.

- Billion Industrial Holding Limited

- Far Eastern New Century Corporation

- Hyosung Chemical

- LyondellBasell Industries Holdings BV

- NAN YA PLASTICS CORPORATION

- NSRP LLC

- SCG Chemicals Public Company Limited

- SKC

- Toray Industries Inc.

- 越南石油天然气集团

- Vietnam Polystyrene Co. Ltd

- Vinaplast

第七章 市场机会与未来展望

Vietnam Plastics Market size in 2026 is estimated at 12.83 million tons, growing from 2025 value of 11.84 million tons with 2031 projections showing 19.16 million tons, growing at 8.35% CAGR over 2026-2031.

Robust foreign direct investment, aggressive infrastructure outlays, and decisive regulatory modernization converge to position Vietnam as Southeast Asia's fastest-growing plastics hub. Manufacturing relocation from China continues to swell downstream consumption, while construction investments-up 40% year over year in H1 2025-channel steady demand for pipes, profiles, and insulation materials. Local converters prioritize throughput over experimentation, scaling extrusion lines to meet surging orders. Simultaneously, sustainability mandates accelerate bioplastics adoption, nudging resin suppliers to diversify feedstocks and recycle content even as imported naphtha and propylene remain cost-sensitive inputs.

Vietnam Plastics Market Trends and Insights

Robust Growth in Domestic Construction Projects

Infrastructure spending climbed 40% year over year in H1 2025 after disbursement timelines were cut from weeks to 1-3 days. Demand for PVC pipes, insulation boards, and flame-retardant cable trays has soared, reflecting Vietnam's status as a cost-competitive construction center with costs still 60%-65% below Singapore levels. Data center projects outpace factory builds, elevating requirements for halogen-free compounds and heat-resistant engineered resins. Circular 10/2024/TT-BXD mandates quality checks on imported building materials, a policy that favors local converters able to document compliance. Together, these trends funnel volume and value growth into the Vietnam plastics market.

Booming Food-grade & E-commerce Packaging Demand

Vietnam's food processing output reached USD 79.3 billion in 2024, up 7.4%, just as e-commerce adoption leapt across urban centers. As a result, converters face parallel requirements for barrier films that prolong shelf life and lightweight mailers that cut shipping costs. Protective cushioning for electronics-imports of components rose 29.3% through March 2025-adds further pull for cushioning foams and molded inserts. Government preference programs that spotlight locally made packaging tilt procurement toward domestic suppliers, encouraging capital upgrades in printing, lamination, and multilayer extrusion lines.

Heavy Dependence on Imported Naphtha and Propylene

Vietnam imported more than 5.5 million tons of plastic feedstock in the first 7 months of 2025, largely from China, South Korea, and Taiwan. SCG's Long Son complex came online in August 2025 with a 1.4 million tons capacity, yet it still covers only a slice of domestic demand. Feedstock expenses, 60%-70% of output cost, remain tethered to global oil swings, eroding price competitiveness when crude spikes. Planned ethane upgrades worth USD 700 million will narrow the gap, but cost parity with gas-advantaged Gulf producers remains elusive.

Other drivers and restraints analyzed in the detailed report include:

- Rising Foreign Direct Investment in Downstream Resin Conversion

- Surge in Automotive & Electronics Relocation to Vietnam

- Escalating Environmental Activism Against Single-use Plastics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Traditional plastics retained 51.10% of the Vietnam Plastics market share in 2025, anchored by polyethylene and polypropylene grades used in everyday packaging, pipes, and molded parts. These products benefit from mature supply chains and low unit costs, ensuring continued volume leadership. Engineering plastics, including polycarbonate and polyamide, are gaining traction in electronics lines that ship high-brightness OLED(Organic Light Emitting Diode) displays and optical modules. Polyurethanes ride the construction boom, serving sandwich panels and furniture cushioning.

Bioplastics, though still a niche, are set to grow at a 12.55% CAGR through 2031 as brand owners chase sustainability targets and new regulations unlock demand. Agricultural residues supply potential starch inputs, yet scaling remains hindered by certification hurdles and premium pricing. Still, pilot programs led by international apparel groups showcase Vietnam as a future biopolymer production site, signaling a possible inflection after 2027.

The Vietnam Plastics Market Report is Segmented by Type (Traditional Plastics, Engineering Plastics, and Bioplastics), Technology (Blow Molding, Extrusion, Injection Molding, and Other Technologies), Application (Packaging, Electrical and Electronics, Building and Construction, Automotive and Transportation, Housewares, Furniture and Bedding, and Other Applications). The Market Forecasts are Provided in Terms of Volume (Tons).

List of Companies Covered in this Report:

- AGC Inc.

- Billion Industrial Holding Limited

- Far Eastern New Century Corporation

- Hyosung Chemical

- LyondellBasell Industries Holdings B.V.

- NAN YA PLASTICS CORPORATION

- NSRP LLC

- SCG Chemicals Public Company Limited

- SKC

- Toray Industries Inc.

- Vietnam Oil and Gas Group

- Vietnam Polystyrene Co. Ltd

- Vinaplast

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Robust Growth in Domestic Construction Projects

- 4.2.2 Booming Food-grade & E-commerce Packaging Demand

- 4.2.3 Rising Foreign Direct Investment in Downstream Resin Conversion

- 4.2.4 Surge in Automotive & Electronics Relocation to Vietnam

- 4.2.5 Government Incentives for Recycled-content Resins

- 4.3 Market Restraints

- 4.3.1 Heavy Dependence on Imported Naphtha and Propylene

- 4.3.2 Escalating Environmental Activism Against Single-use Plastics

- 4.3.3 Rising Competition from Bio-based Substitutes in FMCG

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products & Services

- 4.5.5 Degree of Competition

- 4.6 Raw Material Analysis

5 Market Size & Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Traditional Plastics

- 5.1.1.1 Polyethylene

- 5.1.1.2 Polypropylene

- 5.1.1.3 Polystyrene

- 5.1.1.4 Poly Vinyl Chloride

- 5.1.2 Engineering Plastics

- 5.1.2.1 Polyurethanes

- 5.1.2.2 Fluoropolymers

- 5.1.2.3 Polyamides

- 5.1.2.4 Polycarbonates

- 5.1.2.5 Styrene Copolymers (ABS and SAN)

- 5.1.2.6 Thermoplastic Polyesters

- 5.1.2.7 Other Engineering Plastics

- 5.1.3 Bioplastics

- 5.1.1 Traditional Plastics

- 5.2 By Technology

- 5.2.1 Blow Molding

- 5.2.2 Extrusion

- 5.2.3 Injection Molding

- 5.2.4 Other Technologies

- 5.3 By Application

- 5.3.1 Packaging

- 5.3.2 Electrical and Electronics

- 5.3.3 Building and Construction

- 5.3.4 Automotive and Transportation

- 5.3.5 Housewares

- 5.3.6 Furniture and Bedding

- 5.3.7 Other Applications

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)**/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 AGC Inc.

- 6.4.2 Billion Industrial Holding Limited

- 6.4.3 Far Eastern New Century Corporation

- 6.4.4 Hyosung Chemical

- 6.4.5 LyondellBasell Industries Holdings B.V.

- 6.4.6 NAN YA PLASTICS CORPORATION

- 6.4.7 NSRP LLC

- 6.4.8 SCG Chemicals Public Company Limited

- 6.4.9 SKC

- 6.4.10 Toray Industries Inc.

- 6.4.11 Vietnam Oil and Gas Group

- 6.4.12 Vietnam Polystyrene Co. Ltd

- 6.4.13 Vinaplast

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

2026-2030年全球塑胶市场

2026-2030年全球塑胶市场 塑胶市场:依形状、等级、製造流程、类型、应用和分销管道划分-2026-2032年全球市场预测

塑胶市场:依形状、等级、製造流程、类型、应用和分销管道划分-2026-2032年全球市场预测 塑胶市场分析及预测(至2035年):类型、产品、应用、材料类型、技术、最终用户、製程、组件、安装类型

塑胶市场分析及预测(至2035年):类型、产品、应用、材料类型、技术、最终用户、製程、组件、安装类型 东南亚塑胶市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国塑胶:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

东南亚塑胶市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国塑胶:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 2026-2034年全球塑胶降解细菌市场规模、份额、趋势和成长分析报告2026-2034年全球电气设备塑胶市场规模、份额、趋势和成长分析报告

2026-2034年全球塑胶降解细菌市场规模、份额、趋势和成长分析报告2026-2034年全球电气设备塑胶市场规模、份额、趋势和成长分析报告 2026年全球塑胶和橡胶製品市场报告2026年全球塑胶製品市场报告2026年全球热塑性半成品市场报告

2026年全球塑胶和橡胶製品市场报告2026年全球塑胶製品市场报告2026年全球热塑性半成品市场报告