|

市场调查报告书

商品编码

1939578

泰国塑胶:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Thailand Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

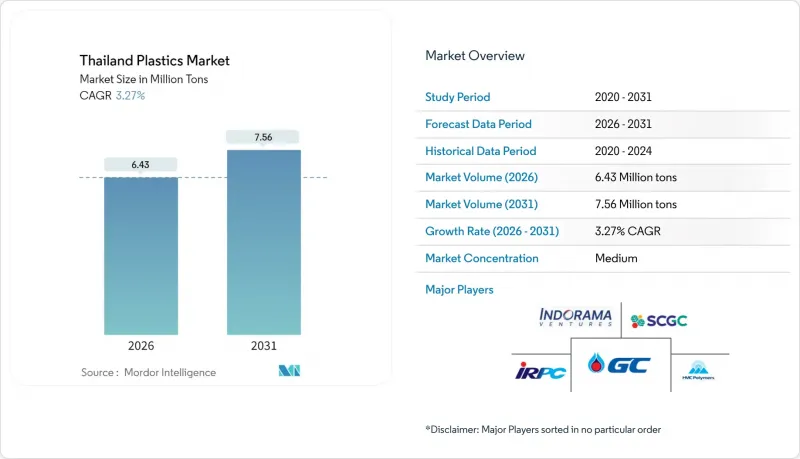

预计到 2026 年,泰国塑胶市场规模将达到 643 万吨,高于 2025 年的 623 万吨。

预计到 2031 年将达到 756 万吨,2026 年至 2031 年的复合年增长率为 3.27%。

这种温和的成长率掩盖了关键的转变,包括向低碳原料、循环经济实践和特种应用领域的转型,即使大宗商品价差收窄,也能提升利润率。虽然树脂传统上占据产量主导地位,但生物聚合物正在迅速崛起,这要归功于生物乙烯和聚乳酸(PLA)的大规模合资产能扩张。食品、饮料和电商包装行业的需求势头最为强劲,而电动车供应链的兴起和大型基础设施计划的推进也为工程树脂和高性能化合物创造了新的需求。鑑于中国日益严重的供应过剩、石脑油价格波动以及更严格的废弃物管理法规都对利润率构成压力,那些实现原料多元化并投资于回收基础设施的公司,更有能力在泰国塑胶市场保护利润。

泰国塑胶市场趋势及分析

食品和饮料包装行业的需求不断增长

国内饮料消费持续成长,为包装需求提供了稳定的支撑。将于2025年3月生效的新食品接触标准正鼓励加工商转向使用可回收、耐热和高附加价值的产品。饮料出口到邻国柬埔寨和越南是推动需求的主要因素,自疫情爆发以来成长超过一倍的食品配送业务,每份订单都会使用多种塑胶製品。气温上升、快速都市化以及旅游业的復苏预计将继续推动泰国塑胶市场强劲的包装需求。随着个人护理行业的蓬勃发展,硬质容器的需求也在同步增长,化妆品和保健品的销售额呈现温和的个位数增长,推动了专用包装材料的应用。

建筑和施工行业塑胶使用量的增加

政府在150多个基础设施计划上的支出,支撑了对PVC管道、隔热材料和屋顶板的长期需求。 「塑胶公路」计画每公里使用多达5吨的再生材料,标誌着政策向循环建筑模式转变,并扩大了再生树脂的潜在市场。目前,已有800多家中大型製造商正在实施数位化订购工具和低碳生产流程,以满足绿色建筑标准。预计大型企划将创造100万个新的就业岗位,从而促进住宅和商业建筑的发展。即使能源价格上涨和中国廉价进口产品挤压了利润空间,这些因素仍将支撑对塑胶建筑材料的强劲需求。

加强对一次性塑胶的监管和课税

泰国塑胶废弃物蓝图将于2025年1月起分阶段实施,其中包括进口禁令以及对食品接触产品更严格的品质标准。曼谷等都市区每天产生1800吨一次性塑胶废弃物,当局正迅速推动课税和标籤要求,这将增加加工商的合规成本。 《工业废弃物管理法案》新增了一项专门用于环境影响修復的基金,并对危险废弃物製定了更严格的处置规则。泰国塑胶市场的生产商必须投资于经认证的可再生或可堆肥替代品,并加强可追溯性体系,违规者将受到处罚。虽然这些法规初期会限制一次性塑胶产品,但最终将推动对高价值、永续树脂的需求。

细分市场分析

截至2025年,传统树脂在泰国塑胶市场占据70.55%的份额,这主要得益于完善的基础设施、规模经济以及多样化的终端应用。聚乙烯和聚丙烯等树脂支撑了包装、汽车和建筑业的需求,而PET的应用范围也从瓶子扩展到工业纱线和轮胎织物等领域。 HMC Polymers预计2023年的销售额将超过250亿泰铢,这表明大宗商品级树脂仍具有持续的商业性价值。工程树脂,例如聚酰胺和聚碳酸酯,在电子组装和电动车动力传动系统应用的推动下,实现了中等个位数的成长。

生物聚合物是成长最快的品类,复合年增长率达5.53%,主要得益于20万吨生物乙烯业务和7.5万吨PLA产能的快速提升。领先的製造商目前正在试验化学回收路线和循环石脑油流,以确保其资产基础的未来发展,并在新的食品接触法规下保持竞争力。传统供应商透过获得生物基製程的许可来拓展业务,而新参与企业则透过碳足迹声明和可堆肥认证来凸显自身优势,从而缩小竞争差距。

泰国塑胶市场报告按类型(传统塑胶、工程塑胶、生质塑胶)和应用(包装、电气和电子设备、建筑施工、汽车和运输设备、家具和床上用品以及其他应用)进行细分。市场预测以吨为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 食品和饮料包装行业的需求不断增长

- 建筑和施工行业塑胶使用量的增加

- 对轻量化汽车和电动车零件的需求

- 电子商务的快速成长推动了防护包装的发展

- 生物基聚合物合资企业(例如,SCGC、Braskem)

- 市场限制

- 禁止和课税一次性塑胶製品

- 原油和石脑油价格波动

- 聚丙烯(PP)和聚乙烯(PE)供应过剩,以及来自中国的低成本进口

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 按类型

- 传统塑料

- 聚乙烯(PE)

- 聚丙烯(PP)

- 聚氯乙烯(PVC)

- 聚苯乙烯(PS)

- 工程塑料

- 聚对苯二甲酸乙二醇酯(PET)

- 聚酰胺(PA)

- 聚碳酸酯(PC)

- 苯乙烯共聚物(ABS 和 SAN)

- 聚丁烯对苯二甲酸酯(PBT)

- 聚甲基丙烯酸甲酯(PMMA)

- 其他工程塑料

- 生质塑胶

- 传统塑料

- 透过使用

- 包装

- 电气和电子设备

- 建筑/施工

- 汽车与运输

- 家具和床上用品

- 其他用途

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Covestro AG

- HMC Polymers Thailand

- Indorama Ventures Public Company Limited

- INEOS Styrolution Group GmbH

- IRPC Public Company Limited

- PTT Global Chemical Public Company Limited

- SCG Chemicals Co. Ltd

- Thai Plastic Industries Co. Ltd

第七章 市场机会与未来展望

Thailand Plastics Market size in 2026 is estimated at 6.43 million tons, growing from 2025 value of 6.23 million tons with 2031 projections showing 7.56 million tons, growing at 3.27% CAGR over 2026-2031.

This moderate headline growth conceals a decisive shift toward low-carbon feedstocks, circular economy practices, and specialty applications that lift margins even as commodity spreads tighten. Traditional resins dominate volumes, yet a rapid pivot to biopolymers is underway because joint ventures are unlocking bio-ethylene and PLA capacity at scale. Demand momentum remains strongest in food, beverage, and e-commerce packaging, but the emergence of an electric-vehicle supply chain and large-scale infrastructure projects creates fresh pull for engineering resins and high-performance compounds. Intensifying Chinese oversupply, volatile naphtha costs, and stricter waste regulations pressure margins; firms that diversify feedstocks and invest in recycling infrastructure are best placed to protect returns in the Thailand plastics market.

Thailand Plastics Market Trends and Insights

Rising Demand from Food and Beverage Packaging

Domestic beverage consumption continues to expand, locking in steady packaging tonnage. New food-contact standards effective March 2025 encourage converters to adopt recyclable and heat-resistant formulations that command premium pricing. Beverage exports to neighboring Cambodia and Vietnam add incremental volumes, and food-delivery growth has more than doubled since the pandemic, generating multiple plastic items per order. Rising temperatures, rapid urbanization, and a tourism rebound sustain packaging intensity in the Thailand plastics market. Demand for rigid containers grows in parallel with the personal-care segment, where mid-single-digit sales growth of cosmetics and health products boosts specialized packaging uptake.

Increasing Plastics Use in Building and Construction

Government spending across over 150 infrastructure projects underwrites long-run demand for PVC pipes, insulation, and roofing sheets. The Plastic Roads initiative, which incorporates up to five tons of recycled material per kilometer, signals a policy pivot toward circular construction practices that enlarge the addressable market for recycled resin. More than 800 mid- and large-size manufacturers now integrate digital ordering tools and low-carbon processes to satisfy green-building specifications. An expected 1 million new jobs linked to megaprojects will spur residential and commercial builds, reinforcing demand for plastic building products even as energy inflation and cheap Chinese imports squeeze margins.

Stricter Single-Use-Plastic Bans and Taxes

Thailand's plastic-waste roadmap phases out imports from January 2025 and tightens quality rules for food-contact articles. Urban centers such as Bangkok generate 1,800 metric tons of single-use waste daily, prompting authorities to fast-track levies and labeling mandates that raise compliance costs for converters. Additional legislation under the Draft Industrial Waste Management Act introduces a dedicated fund to remediate environmental impacts and imposes stricter disposal rules on hazardous scrap. Producers in the Thailand plastics market must invest in certified recyclable or compostable alternatives and enhance traceability systems or face penalties. These rules initially restrict disposable items but ultimately catalyze demand for higher-value sustainable resins.

Other drivers and restraints analyzed in the detailed report include:

- Lightweighting Needs in Automotive and EV Components

- Bio-Based Polymer Joint Ventures

- Polypropylene and Polyethylene Oversupply and Low-Cost Imports from China

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Traditional resins retained 70.55% of Thailand's plastics market share in 2025 thanks to entrenched infrastructure, scale economics, and diversified end-use exposure. Among them, polyethylene and polypropylene anchor packaging, automotive, and construction demand, while PET has grown beyond bottles into technical yarns and tire fabrics. HMC Polymers surpassed THB 25 billion in sales in 2023, illustrating the continuing commercial relevance of commodity grades. Engineering resins such as polyamides and polycarbonates post mid-single-digit demand gains tied to electronics assembly and EV power-train applications.

Biopolymers are the fastest-expanding category, progressing at a 5.53% CAGR and lifted by the 200,000-ton bio-ethylene venture and the 75,000-ton PLA expansion. Mainstream producers now trial chemical-recycling routes and circular naphtha streams to future-proof their asset bases and preserve relevance under new food-contact rules. The competitive gap narrows as conventional suppliers license bio-based processes, while newcomers differentiate through carbon-footprint declarations and compostability certifications.

The Thailand Plastics Report is Segmented by Type (Traditional Plastics, Engineering Plastics, and Bioplastics), Application (Packaging, Electrical and Electronics, Building and Construction, Automotive and Transportation, Furniture and Bedding, and Other Applications). The Market Forecasts are Provided in Terms of Volume (Tons).

List of Companies Covered in this Report:

- Covestro AG

- HMC Polymers Thailand

- Indorama Ventures Public Company Limited

- INEOS Styrolution Group GmbH

- IRPC Public Company Limited

- PTT Global Chemical Public Company Limited

- SCG Chemicals Co. Ltd

- Thai Plastic Industries Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand from Food and Beverage Packaging

- 4.2.2 Increasing Plastics Use in Building and Construction

- 4.2.3 Lightweighting Needs in Automotive and EV Components

- 4.2.4 Rapid E-Commerce Growth Boosting Protective Packaging

- 4.2.5 Bio-Based Polymer Joint Ventures (E.G., SCGC, Braskem)

- 4.3 Market Restraints

- 4.3.1 Stricter Single-Use-Plastic Bans and Taxes

- 4.3.2 Crude-Oil/Naphtha Price Volatility

- 4.3.3 PP and PE Oversupply and Low-Cost Imports from China

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Traditional Plastics

- 5.1.1.1 Polyethylene (PE)

- 5.1.1.2 Polypropylene (PP)

- 5.1.1.3 Polyvinyl Chloride (PVC)

- 5.1.1.4 Polystyrene (PS)

- 5.1.2 Engineering Plastics

- 5.1.2.1 Polyethylene Terephthalate (PET)

- 5.1.2.2 Polyamides (PA)

- 5.1.2.3 Polycarbonates (PC)

- 5.1.2.4 Styrene Copolymers (ABS and SAN)

- 5.1.2.5 Polybutylene Terephthalate (PBT)

- 5.1.2.6 Polymethyl Methacrylate (PMMA)

- 5.1.2.7 Other Engineering Plastics

- 5.1.3 Bioplastics

- 5.1.1 Traditional Plastics

- 5.2 By Application

- 5.2.1 Packaging

- 5.2.2 Electrical and Electronics

- 5.2.3 Building and Construction

- 5.2.4 Automotive and Transportation

- 5.2.5 Furniture and Bedding

- 5.2.6 Other Applications

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Covestro AG

- 6.4.2 HMC Polymers Thailand

- 6.4.3 Indorama Ventures Public Company Limited

- 6.4.4 INEOS Styrolution Group GmbH

- 6.4.5 IRPC Public Company Limited

- 6.4.6 PTT Global Chemical Public Company Limited

- 6.4.7 SCG Chemicals Co. Ltd

- 6.4.8 Thai Plastic Industries Co. Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

2026-2030年全球塑胶市场

2026-2030年全球塑胶市场 塑胶市场:依形状、等级、製造流程、类型、应用和分销管道划分-2026-2032年全球市场预测

塑胶市场:依形状、等级、製造流程、类型、应用和分销管道划分-2026-2032年全球市场预测 塑胶市场分析及预测(至2035年):类型、产品、应用、材料类型、技术、最终用户、製程、组件、安装类型

塑胶市场分析及预测(至2035年):类型、产品、应用、材料类型、技术、最终用户、製程、组件、安装类型 东南亚塑胶市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)越南塑胶市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

东南亚塑胶市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)越南塑胶市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 2026-2034年全球塑胶降解细菌市场规模、份额、趋势和成长分析报告2026-2034年全球电气设备塑胶市场规模、份额、趋势和成长分析报告

2026-2034年全球塑胶降解细菌市场规模、份额、趋势和成长分析报告2026-2034年全球电气设备塑胶市场规模、份额、趋势和成长分析报告 2026年全球塑胶和橡胶製品市场报告2026年全球塑胶製品市场报告2026年全球热塑性半成品市场报告

2026年全球塑胶和橡胶製品市场报告2026年全球塑胶製品市场报告2026年全球热塑性半成品市场报告