|

市场调查报告书

商品编码

1939704

自行车:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Bicycle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

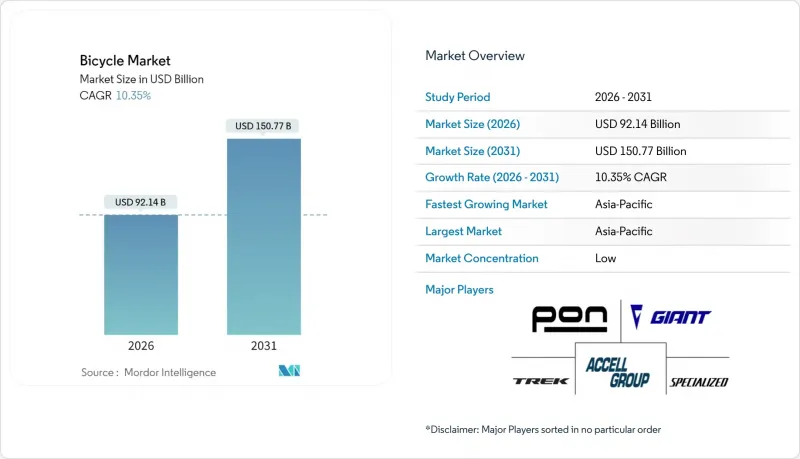

预计自行车市场将从 2025 年的 835 亿美元成长到 2026 年的 921.4 亿美元,到 2031 年将达到 1507.7 亿美元,2026 年至 2031 年的复合年增长率为 10.35%。

随着都市区越来越多地实施拥堵收费,以及企业将骑行激励措施纳入员工健康计划,自行车需求持续增长。政府基础设施投资远超预期,以及旨在减少碳排放的严格气候政策,进一步推动了这项需求。此外,电池安全技术的不断进步正在解决安全隐患,并扩大潜在消费群。直销品牌的兴起和软体驱动的车队服务的整合正在重塑零售环境,优化营运效率,并改善客户体验。不断上涨的燃油价格进一步凸显了自行车相对于汽车的成本优势,使其成为自行车市场中更具经济可行性的选择。总而言之,在有利的法规结构、技术进步以及城市生活方式向永续和积极出行方式转变的推动下,自行车市场持续成长。

全球自行车市场趋势与洞察

政府支持促进绿色交通途径

世界各国政府日益认识到,骑行不仅仅是一项休閒活动,更是应对气候变迁基础设施的重要组成部分。欧盟于2024年4月通过的《欧洲自行车宣言》便是这项转变的有力佐证。该宣言概述了成员国为加强自行车基础设施建设并促进其融入永续交通系统而作出的36项具有约束力的承诺。同样,在美国,「积极交通基础设施投资计画」每年将提供4,450万美元,用于支持互联自行车网路的建设,从而提升骑乘者的便利性和安全性。在州一级,加州承诺在四年内投入9.3亿美元,用于建造265英里(约420公里)的新自行车道,进一步强调了自行车在城市规划中的重要性。这些全面的政策措施正在推动对自行车相关产品和服务的持续需求,促使製造商扩大产能,零售商增加库存,以满足自行车市场日益增长的需求。

都市区拥挤促使人们骑自行车上班。

随着城市密度压力的增加,特大城市,尤其是在亚太地区,面临交通拥堵带来的经济和社会成本,因此,自行车出行解决方案至关重要。拥挤收费和低排放区鼓励人们骑自行车出行,而非驾驶私家车。混合办公模式也正在改变通勤方式,让骑自行车成为短程、弹性出行的理想选择。荷兰就是一个很好的例子,它成功地将自行车与连接铁路网络的专用自行车高速公路相结合,透过创建多模态系统,同时应对了环境和出行方面的挑战。企业采用自行车出行也受到员工健康计画和永续发展报告要求的推动。自行车基础设施的投资有助于吸引人才、实现碳减排目标,并提高自行车市场与环境、社会和管治(ESG) 目标的契合度。

自行车和其他快速交通途径的普及是阻碍人们骑自行车的因素。

随着电动Scooter、共享旅游服务和自动驾驶汽车测试在短途出行领域占据主导地位,交通途径之间的竞争日益激烈。在都市区,拥有电动自行车的成本如今已与普通电动Scooter或共享出行订阅服务的成本相当,价格竞争愈演愈烈。微出行平台的整合催生了众多综合交通应用程序,使得骑乘成为众多出行选择之一。在拥有发达地铁网路的亚太城市,公共运输的进步降低了骑乘作为长途通勤方式的吸引力。儘管对替代交通途径的监管进展迅速,但自行车基础设施的建设却相对落后。例如,电动Scooter共享专案审核速度很快,而自行车相关计划则需要更长时间。然而,骑行带来的健康和环境效益限制了替代品的威胁,并确保了其市场地位。

细分市场分析

预计到2025年,电动自行车将占自行车市场50.74%的份额,并在2031年之前以12.52%的复合年增长率成长。在UL 2849等安全认证提升消费者信心的推动下,电动自行车市场规模预计在未来十年内将增加一倍以上。如今,电池可拆卸且符合航空标准,从而拓展了电动自行车的应用场景。同时,传统公路车和城市自行车的销售量保持稳定,为零部件供应商带来了规模经济效益。

技术融合正在重塑竞争优势:整合导航、防盗追踪和预测性维护等技术正在提升骑乘体验,并推高高端价格。亚太地区的生产商受益于成本效益高的生产能力,而欧洲组装则利用其地理优势抢占高端市场。中国强制性的电池回收制度为其他地区树立了榜样,并可能为合规品牌带来业务收益。对于那些将自行车与车队分析结合的软体公司而言,市场机会依然存在,它们能够以轻资产的方式为出行预算提供支援。

到2025年,传统车架仍将占据自行车市场85.12%的主导地位。这一主导地位反映了消费者对其的认可,这得益于其极具吸引力的量产几何结构、经济实惠的价格以及与现有基础设施的无缝兼容性。同时,折迭式自行车预计将迎来强劲成长,到2031年将实现11.22%的年复合成长率。这一成长率是整体自行车市场成长率的两倍,主要驱动力是消费者对紧凑、节省空间解决方案的需求不断增长,尤其是在应对都市区住宅空间有限以及需要高效连接铁路网络等挑战方面。

材料技术的进步,例如镁合金铰链和快拆夹具,降低了折迭自行车的重量,并使其保固期与普通自行车相同,从而解决了人们的担忧。自行车产业也看到,越来越多的员工开始选择折迭式自行车作为通勤工具,因为它们可以安全地存放在办公桌下或小型储物柜中。欧洲,特别是德国和荷兰,推行支持铁路和自行车联合通勤的政策,也为折迭式自行车提供了监管支持。然而,在折迭式自行车的零售价格接近普通自行车之前,预计普通自行车仍将占据年度销售的大部分。

区域分析

预计到2025年,亚太地区将占全球市场的47.68%,巩固其作为主要收入来源的地位。受多种因素影响,该地区预计到2031年将达到13.08%的高复合年增长率。中国自行车市场正经历显着成长,这得益于电动自行车的普及、强制性电池回收政策的实施以及积极推广摩托车作为永续交通途径的城市交通政策。同时,日本正策略性地使其认证体系与欧洲标准接轨,简化出口程序,并提升国内品牌的国际竞争力。

在北美和欧洲,大规模的基础设施投资项目正在创造稳定且永续的自行车需求。从市场地域分布来看,製造业活动集中在亚洲,而已开发市场则在利好政策的推动下实现了成长。这种趋势不仅促进了贸易流动,巩固了亚洲老牌製造商的优势,也为高级产品。

中东和非洲的自行车市场正经历强劲成长,电动自行车的普及率以两位数的速度加速成长,传统自行车的需求也保持稳定。杜拜、开普敦、内罗毕和特拉维夫等主要城市的消费者越来越将自行车,尤其是电动式自行车,视为汽车和摩托车等传统交通工具的现代化环保替代品。然而,缺乏标准化的安全法规、保险体系和道路使用权仍然是限制非洲国家自行车市场快速发展的一大挑战。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 都市区拥挤促使人们选择骑自行车进行日常通勤。

- 健身趋势推动自行车运动

- 政府支持促进绿色交通途径

- 日益增强的环保意识和永续性正在推动消费者循环消费。

- 职场健康计画鼓励员工骑自行车

- 燃油价格上涨使骑自行车成为一种经济实惠的出行方式。

- 市场限制

- 替代交通方式(例如摩托车)和其他更快捷的交通途径的普及

- 仿冒自行车阻碍市场成长

- 电动自行车高成本

- 遍远地区道路状况差

- 监管环境

- 技术进步

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依产品类型

- 路城

- 山地/全地形

- 杂交种

- 电动自行车

- 其他类型

- 有意为之

- 通常

- 折迭式的

- 最终用户

- 男性

- 女士

- 孩子

- 透过分销管道

- 线下零售店

- 线上零售商

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 北美其他地区

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 西班牙

- 荷兰

- 波兰

- 比利时

- 瑞典

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 印尼

- 韩国

- 泰国

- 新加坡

- 亚太其他地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 智利

- 秘鲁

- 南美洲其他地区

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 奈及利亚

- 埃及

- 摩洛哥

- 土耳其

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Accell Group NV

- Trek Bicycle Corporation

- Pon Holdings BV

- Giant Manufacturing Co. Ltd

- Specialized Bicycle Components Inc.

- Shimano Inc.

- Scott Sports SA

- Merida Industry Co. Ltd

- Stryder Cycle Private Limited

- Cycles Devinci inc.

- Pending System GmbH & Co. KG

- Brompton Bicycle Ltd

- Decathlon SA

- Rad Power Bikes Inc.

- Riese and Muller GmbH

- Bulls Bikes GmbH

- Yadea Group Holdings Ltd

- Canyon Bicycles GmbH

- Hero Cycles Limited

- Ribble Cycles

第七章 市场机会与未来展望

The Bicycle market is expected to grow from USD 83.5 billion in 2025 to USD 92.14 billion in 2026 and is forecast to reach USD 150.77 billion by 2031 at 10.35% CAGR over 2026-2031.

Urban centers are increasingly implementing congestion charges, while employers are incorporating bicycle incentives into wellness programs, driving sustained demand for bicycles. This demand is further reinforced by significant government investments in infrastructure, which have already exceeded projections, alongside stricter climate policies aimed at reducing carbon emissions. Additionally, ongoing advancements in battery safety technology are expanding the potential consumer base by addressing safety concerns. The emergence of direct-to-consumer brands and the integration of software-enabled fleet services are redefining the retail landscape, optimizing operational efficiencies, and enhancing customer accessibility. Rising fuel prices are further amplifying the cost advantage of bicycles over motorized vehicles, making them a more economically viable option in the bicycle market. Overall, the bicycle market continues to experience growth, supported by favorable regulatory frameworks, technological progress, and a shift in urban lifestyles toward sustainable and active mobility solutions.

Global Bicycle Market Trends and Insights

Government support encourages eco-friendly transportation methods

Governments worldwide are increasingly recognizing cycling as a critical element of climate infrastructure rather than merely a recreational activity. This shift is evident in the European Union's adoption of the European Declaration on Cycling in April 2024, which outlines 36 binding commitments for member states to enhance cycling infrastructure and promote its integration into sustainable transport systems . Similarly, in the United States, the Active Transportation Infrastructure Investment Program provides USD 44.5 million annually to develop connected cycling networks, fostering greater accessibility and safety for cyclists. On a state level, California has committed USD 930 million over four years to build 265 miles of new bike paths, further emphasizing the importance of cycling in urban planning . These comprehensive policy measures are driving sustained demand for cycling-related products and services, encouraging manufacturers to scale up production capacities and motivating retailers to increase their inventory levels to meet the growing market needs in the bicycle market.

Urban congestion boosts bicycle usage for daily commute

As urban density pressures rise, especially in Asia-Pacific megacities facing traffic congestion's economic and social costs, the need for cycling solutions is critical. Congestion pricing and low-emission zones further promote cycling over private vehicles. Hybrid work models have also reshaped commuting, making cycling ideal for shorter, flexible trips. The Netherlands exemplifies successful cycling integration with cycling highways linked to rail networks, creating a multimodal transport system that rivals car ownership while addressing environmental and mobility challenges. Corporations are increasingly adopting cycling, driven by employee wellness initiatives and sustainability reporting mandates. Investments in cycling infrastructure help attract talent and meet carbon reduction goals, aligning with environmental and social governance (ESG) objectives in the bicycle market.

Availability of substitute like bikes, and other faster transport modes discourages the use of bicycle

Competition among transport modes is intensifying as electric scooters, ride-sharing services, and autonomous vehicle pilots address short-distance mobility. In urban areas, e-bike ownership costs now rival those of electric scooters and ride-sharing subscriptions, heightening pricing competition. Integrated transport apps, driven by micromobility platform consolidation, have made bicycles one of many transport options. In Asia-Pacific cities with extensive metro systems, public transportation advancements have reduced cycling's appeal for longer commutes. While regulations for alternative transport modes advance quickly, cycling infrastructure faces delays. For instance, electric scooter-sharing programs receive rapid approvals, whereas cycling projects take longer. However, cycling's health and environmental benefits limit substitution threats, ensuring its market presence.

Other drivers and restraints analyzed in the detailed report include:

- Fitness trends increase popularity of cycling activities

- Environmental awareness and sustainability drives bicycle usage among consumers

- High e-bike cost restricts wider adoption globally

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

E-bicycles held 50.74% of the bicycle market in 2025, and the segment is forecast to post a 12.52% CAGR to 2031. The bicycle market size for e-bicycles is therefore on track to more than double within the decade, propelled by safety certifications such as UL 2849 that boost consumer trust. Batteries are now removable and airline-compliant, widening use cases. Meanwhile, conventional road and city bikes preserve large sales volumes, sustaining economies of scale for component suppliers.

Technology convergence defines competitive edges: integrated navigation, theft-tracking, and predictive maintenance enrich the rider experience and push premium price points. Asia-Pacific producers benefit from cost-efficient capacity, while European assemblers leverage proximity to capture premium niches. Battery recycling mandates in China set a template other regions may follow, adding after-sales service revenue for compliant brands. Market entry remains open for software-native firms bundling bikes with fleet analytics, providing asset-light access to mobility budgets.

In 2025, regular frames continue to dominate the bicycle market, accounting for a substantial 85.12% market share. This dominance highlights the strong appeal of mass-produced geometries, cost-effective pricing, and seamless compatibility with existing infrastructure, which collectively make regular frames a preferred choice among consumers. On the other hand, folding designs are projected to experience a robust growth trajectory, registering an impressive 11.22% CAGR through 2031. This growth rate, which is double that of the overall bicycle market, is primarily driven by the rising demand for compact and space-efficient solutions, particularly in response to challenges such as limited urban housing space and the growing need for efficient last-mile connectivity with rail networks.

Material advances in magnesium hinges and quick-release clamps now limit weight premiums, and warranty parity with regular bikes removes past hesitations. In the bicycle industry, corporations also favor foldables for employee fleets because units store safely under desks and in small lockers. European policy supporting combined rail-bike commutes, notably in Germany and the Netherlands, gives folding models regulatory tailwinds. Yet the bulk of annual volume will still come from regular bikes until folding retail prices close the gap.

The Bicycle Market Report is Segmented by Product Type (Road/City, Mountain/All-Terrain, Hybrid, E-Bicycle, and Others), Design (Regular and Folding), End-User (Men, Women, and Children), Distribution Channel (Offline Retail Stores and Online Retail Stores), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, the Asia-Pacific region solidified its position as a key revenue contributor, accounting for 47.68% of the global market. The region is forecasted to achieve a strong compound annual growth rate (CAGR) of 13.08% through 2031, driven by several factors. In China, the bicycle market is experiencing significant growth due to the widespread adoption of e-bikes, the enforcement of mandatory battery-recycling initiatives, and urban traffic policies that actively encourage the use of two-wheelers as a sustainable mode of transportation. Japan, on the other hand, is strategically aligning its certification frameworks with European standards, thereby simplifying export procedures and enhancing the global competitiveness of its domestic brands.

In North America and Europe, large-scale infrastructure investment programs are creating a stable and sustained demand for bicycles. The market's geographic distribution underscores a concentration of manufacturing activities in Asia, while developed markets are witnessing growth driven by favorable policy measures. This dynamic fosters trade flows that not only reinforce the dominance of established Asian manufacturers but also create opportunities for premium product positioning in Western markets, catering to a consumer base that values high-quality and innovative offerings.

The bicycle market in the Middle East and Africa is experiencing robust growth, with e-bike adoption accelerating at double-digit rates and traditional bicycles maintaining steady demand. Urban consumers in key cities such as Dubai, Cape Town, Nairobi, and Tel Aviv are increasingly perceiving bicycles, particularly e-bikes, as modern, eco-conscious alternatives to conventional vehicles like cars and motorbikes. However, the lack of standardized safety regulations, insurance frameworks, and traffic rights continues to pose challenges, hindering the rapid formalization of the bicycle market in several African nations.

- Accell Group NV

- Trek Bicycle Corporation

- Pon Holdings BV

- Giant Manufacturing Co. Ltd

- Specialized Bicycle Components Inc.

- Shimano Inc.

- Scott Sports SA

- Merida Industry Co. Ltd

- Stryder Cycle Private Limited

- Cycles Devinci inc.

- Pending System GmbH & Co. KG

- Brompton Bicycle Ltd

- Decathlon SA

- Rad Power Bikes Inc.

- Riese and Muller GmbH

- Bulls Bikes GmbH

- Yadea Group Holdings Ltd

- Canyon Bicycles GmbH

- Hero Cycles Limited

- Ribble Cycles

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Urban congestion boosts bicycle usage for daily commute

- 4.2.2 Fitness trends increase popularity of cycling activities

- 4.2.3 Government support encourages eco-friendly transportation methods

- 4.2.4 Environmental awareness and sustainability drives bicycle usage among consumers

- 4.2.5 Workplace wellness programs encourage employee bicycle usage

- 4.2.6 Rising fuel prices make bicycles cost-effective alternatives

- 4.3 Market Restraints

- 4.3.1 Availability of substitute like bikes, and other faster transport modes discourages the use of bicycle

- 4.3.2 Presence of counterfeit bicycles hinders market growth

- 4.3.3 High e-bike cost restricts wider adoption globally

- 4.3.4 Poor road conditions in rural areas hinder smooth bicycle experience

- 4.4 Regulatory Landscape

- 4.5 Technological Advancements

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Road/City

- 5.1.2 Mountain/All-Terrain

- 5.1.3 Hybrid

- 5.1.4 E-Bicycle

- 5.1.5 Other Types

- 5.2 By Design

- 5.2.1 Regular

- 5.2.2 Folding

- 5.3 By End-User

- 5.3.1 Men

- 5.3.2 Women

- 5.3.3 Children

- 5.4 By Distribution Channel

- 5.4.1 Offline Retail Stores

- 5.4.2 Online Retail Stores

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Indonesia

- 5.5.3.6 South Korea

- 5.5.3.7 Thailand

- 5.5.3.8 Singapore

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Peru

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Accell Group NV

- 6.4.2 Trek Bicycle Corporation

- 6.4.3 Pon Holdings BV

- 6.4.4 Giant Manufacturing Co. Ltd

- 6.4.5 Specialized Bicycle Components Inc.

- 6.4.6 Shimano Inc.

- 6.4.7 Scott Sports SA

- 6.4.8 Merida Industry Co. Ltd

- 6.4.9 Stryder Cycle Private Limited

- 6.4.10 Cycles Devinci inc.

- 6.4.11 Pending System GmbH & Co. KG

- 6.4.12 Brompton Bicycle Ltd

- 6.4.13 Decathlon SA

- 6.4.14 Rad Power Bikes Inc.

- 6.4.15 Riese and Muller GmbH

- 6.4.16 Bulls Bikes GmbH

- 6.4.17 Yadea Group Holdings Ltd

- 6.4.18 Canyon Bicycles GmbH

- 6.4.19 Hero Cycles Limited

- 6.4.20 Ribble Cycles

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

自行车市场分析及预测(至2035年):依类型、产品类型、服务、技术、零件、应用、材质、最终使用者、模式、安装类型划分

自行车市场分析及预测(至2035年):依类型、产品类型、服务、技术、零件、应用、材质、最终使用者、模式、安装类型划分 全球自行车市场规模、份额、趋势和成长分析报告(2026-2034)自行车市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年

全球自行车市场规模、份额、趋势和成长分析报告(2026-2034)自行车市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年 双人自行车市场-全球产业规模、份额、趋势、机会与预测:动力类型、应用、销售管道、地区与竞争格局(2021-2031年)

双人自行车市场-全球产业规模、份额、趋势、机会与预测:动力类型、应用、销售管道、地区与竞争格局(2021-2031年) 北美自行车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

北美自行车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 日本自行车市场报告:按类型、技术、价格范围、通路、最终用户和地区划分(2026-2034年)

日本自行车市场报告:按类型、技术、价格范围、通路、最终用户和地区划分(2026-2034年) 自行车市场:依产品类型、技术、最终用户、价格、地区划分

自行车市场:依产品类型、技术、最终用户、价格、地区划分 自行车市场规模、份额和成长分析(按技术、最终用户、类型、设计、分销管道和地区划分)-2026-2033年产业预测

自行车市场规模、份额和成长分析(按技术、最终用户、类型、设计、分销管道和地区划分)-2026-2033年产业预测 二手摩托车市场规模、份额和成长分析(按分销、来源、引擎排气量、类型、动力和地区划分)—产业预测(2026-2033 年)

二手摩托车市场规模、份额和成长分析(按分销、来源、引擎排气量、类型、动力和地区划分)—产业预测(2026-2033 年) 自行车市场规模、份额和趋势分析报告:按产品、技术、最终用途、分销管道、地区和细分市场预测(2026-2033 年)

自行车市场规模、份额和趋势分析报告:按产品、技术、最终用途、分销管道、地区和细分市场预测(2026-2033 年)