|

市场调查报告书

商品编码

1939719

美国逆向物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)United States Reverse Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

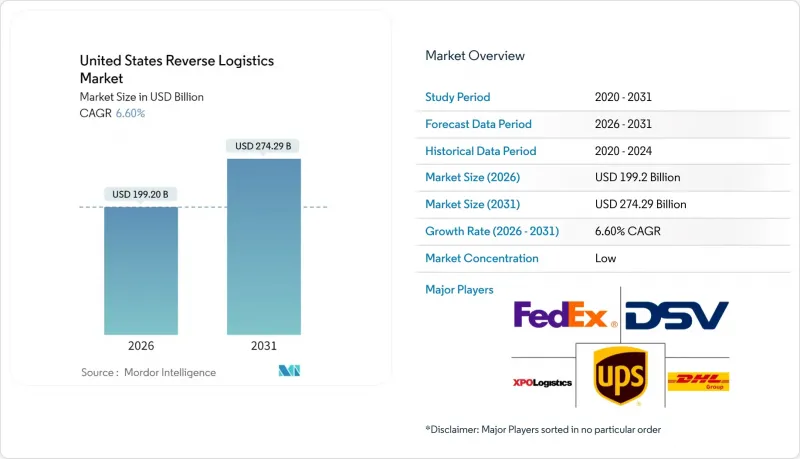

美国逆向物流市场预计到 2026 年将达到 1,992 亿美元,高于 2025 年的 1,868.7 亿美元,预计到 2031 年将达到 2,742.9 亿美元。

预计2026年至2031年年复合成长率(CAGR)为6.6%。

推动这一成长的关键因素包括强劲的电子商务成长、对电子废弃物监管力度的加大,以及旨在建立客户忠诚度的便利退货品牌策略。运输成本仍然是支出中的主导因素,因为退货商品来自数百万个分散的地址,需要快速重新部署到中央处理中心。同时,对机器人、电脑视觉和人工智慧驱动的处置引擎等技术的投资正在降低单位成本,并迅速将退货产品转化为可变现的资产,从而提高回收率。随着领先物流供应商之间的整合加剧(如2025年的一些重要收购案所示),显然,只有那些拥有专用逆向物流网络、低温运输资产和合规专业知识的公司才能充分利用这一机会。

美国逆向物流市场趋势与洞察

电子商务的快速成长导致报酬率上升

线上消费的成长几乎直接转化为退货率的上升。零售商经常遇到「分批退货」的情况,即消费者订购多种款式,并预期退回其中大部分,因此快速的退货流程成为消费者购买前的一大卖点。大型宅配业者现在已将退货取件纳入最后一公里配送路线规划,以最大限度地减少车辆空驶里程。这项调整缩短了车辆停留时间,并缓解了收货码头的拥挤。配备高容量输送机的退货中心也在扩大规模,以应对节后退货量的激增,并透过在48小时内补货来防止断货。高效运作此流程的全国性零售商能够回收更多营运资金,同时提升顾客终身价值。

宽鬆的退货政策是一种竞争优势

曾经只是一项服务,如今宽鬆的退货期限已成为提升转换率的关键。开创「先试后买」模式的D2C品牌都在寻找能够在数小时内(而非数天)处理和退款的合作伙伴,以确保客户满意度。因此,逆向物流网路在地理覆盖范围和技术基础设施方面与正向物流网路类似,将宅配柜、商店柜檯和邮寄退货管道连接到同一个库存云平台。人工智慧驱动的诈欺分析能够识别退货率异常高的客户,使零售商能够在不增加损失率的情况下维持宽鬆的退货政策。能够掌握这种平衡的供应商正在赢得与服装和电子产品零售商的长期合约。

高昂的运输和处理成本

逆向物流路线本身就存在不平衡问题,卡车回程时往往只装载了部分货物,导致单位成本上升。燃油价格波动加剧了这项挑战,车队营运商也被迫遵守新的第三阶段温室气体排放标准,这需要昂贵的设备升级。为了保障利润率,物流供应商会在区域转运中心整合小包裹,并协商动态回程传输协议以提高装载率。然而,对于低价值商品而言,仅运输成本就可能抵消转售利润,导致销量较大的产品最终被清仓甩卖,而不是进行再製造。

细分市场分析

到2025年,运输将占美国逆向物流市场规模的64.40%,显示回收和再利用是价值回收的首要任务。包裹和零担货运公司正在部署与运输路线相衔接的专用退货通道,以最大限度地提高网路密度。空运继续处理高价值和对温度敏感的退货,尤其是来自医疗设备业的退货。仓储仍然是次要的成本中心,靠近主要港口和州际公路的多客户仓储设施有助于缩短越库作业货物的週期时间。随着品牌追求循环模式,其他附加价值服务(维修、翻新、分级、认证处置)的需求不断增长,推动该细分市场到2031年的复合年增长率达到4.65%。将这些服务与运输相结合的供应商透过管理整个处置链来获得高额收入。

第二代设施整合了机器人分类、资料脱敏测试实验室和电商拍照亭,使收集到的商品能够在抵达当天上架到二手商品交易平台。这项转型提高了美国逆向物流市场的收入,并减少了外包给清算批发商的业务。长途货运公司也增加了码头分拣作业,减少了不必要的运输里程,这表明整合在盈利能力和永续性都带来了回报。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 电子商务的快速成长正在推动退货率上升。

- 宽鬆的退货政策是竞争优势之一。

- 永续性与电子废弃物法规

- 退货中心的自动化和机器人技术

- 人工智慧驱动的预测性效益预防分析

- 二手商品交易市场的获利模式

- 市场限制

- 高昂的运输和处理成本

- 全通路退货的复杂性

- 退货诈骗增多

- 大型物品再製造及回收能力方面的瓶颈

- 价值/供应链分析

- 技术展望

- 监管环境

- 波特五力模型

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 专题报导—美国电子商务产业

- 研究消费行为和偏好的变化

- 退货成本如何影响零售商—分析师观点

第五章 市场规模与成长预测

- 按功能

- 运输

- 路

- 航空

- 其他交通方式

- 仓储营运(储存、配送、收货)

- 其他附加价值服务(退货处理、重新入库、翻新、处置)

- 运输

- 最终用户

- 消费品及零售

- 家居与室内设计

- 医疗和药品

- 快速消费品(日常消费品)

- 其他最终用户

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- United Parcel Service(UPS)

- FedEx Corp.

- XPO Logistics

- DSV

- DHL Supply Chain

- CH Robinson Worldwide

- Geodis

- Yusen Logistics

- CEVA Logistics

- Kuehne+Nagel

- ShipBob

- United States Postal Service(USPS)

- Excelsior Integrated LLC

- Ryder

- Kenco Logistics

- Yellow Corporation

- RXO Inc.

- ArcBest

- AP Express

- Bluebird Express

第七章 市场机会与未来展望

United States Reverse Logistics market size in 2026 is estimated at USD 199.2 billion, growing from 2025 value of USD 186.87 billion with 2031 projections showing USD 274.29 billion, growing at 6.6% CAGR over 2026-2031.

Robust e-commerce growth, heightened regulatory scrutiny of electronic waste, and brand strategies that use friction-free returns to win customer loyalty are the chief forces behind this trajectory. Transportation continues to absorb the bulk of spending because returned items originate from millions of dispersed addresses and require rapid repositioning into central processing hubs. At the same time, technology investments in robotics, computer vision, and AI-enabled disposition engines are lowering unit costs, turning returned products into quickly monetized assets, and improving recovery rates. Consolidation among major logistics providers-underscored by headline acquisitions in 2025-signals that only operators with dedicated reverse networks, cold-chain assets, and compliance expertise can fully monetize the opportunity.

United States Reverse Logistics Market Trends and Insights

E-commerce Boom Lifting Return Volumes

Online spending growth translates almost directly into higher returns. Retailers frequently encounter "bracketing," where shoppers order multiple variants with the expectation of sending most of them back, turning reverse flow speed into a pre-purchase selling point. Major parcel carriers now embed returns pick-ups in last-mile route plans to minimize empty-truck miles, an adjustment that cuts dwell time and limits congestion at inbound docks. Returns centers equipped with high-throughput conveyors are also scaling to meet the post-holiday influx, preventing stockouts by redeploying inventory within 48 hours. National retailers that excel at this cycle improve customer lifetime value while recovering more working capital.

Liberal Returns Policies as Competitive Differentiator

Generous return windows, once a courtesy, are now pivotal to conversion. Direct-to-consumer brands that originated the "try-before-you-buy" model require partners that can process and refund within hours, not days, to maintain customer satisfaction scores. Reverse networks, therefore, mirror forward networks in geographic reach and technology stack, linking parcel lockers, in-store counters, and mail-back channels to the same inventory cloud. AI-driven fraud analytics flag unusually high-return personas, allowing retailers to sustain lenient policies without escalating shrinkage. Providers that master this balance earn sticky multi-year contracts from apparel and electronics merchants.

High Transportation & Handling Costs

Reverse lanes are inherently imbalanced, with trucks often returning partially filled, which elevates cost per unit. Fuel price volatility amplifies the challenge; fleet operators must align with emerging Phase 3 greenhouse-gas standards that require expensive equipment upgrades. To protect margins, providers consolidate parcels into regional cross-docks and negotiate dynamic backhaul agreements to boost load factors. Yet for low-value merchandise, transportation alone can erase resale profit, pushing volume toward liquidation instead of refurbishment.

Other drivers and restraints analyzed in the detailed report include:

- Sustainability & E-waste Regulations

- Automation & Robotics in Returns Centers

- Omnichannel Returns Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation generated 64.40% of the United States Reverse Logistics market size in 2025, underscoring the primacy of collection and repositioning in value recovery. Parcel and less-than-truckload carriers have deployed dedicated returns lanes that sync with outbound routes, maximizing network density. Airfreight continues to handle high-value or temperature-sensitive returns, notably from the medical-device trade. Warehousing follows as the secondary cost center; multi-client campuses near major ports and interstates shorten cycle times for cross-docked items. Other Value-added Services (repair, refurbishment, grading, and certified destruction) capture rising demand as brands pursue circular models, propelling this sub-segment's 4.65% CAGR to 2031. Providers bundling transportation with these services command premium yields because they control the full disposition chain.

Second-generation facilities now combine robotic sortation, data-sanitized test labs, and e-commerce photo booths to list recovered items on recommerce marketplaces the same day they arrive. This shift embeds incremental revenue inside the United States Reverse Logistics market rather than outsourcing it to liquidation wholesalers. Long-haul carriers are likewise adding dockside triage to reduce wasted miles, proving that functional integration yields both margin and sustainability wins.

The United States Reverse Logistics Market Report is Segmented by Function (Transportation, Warehousing, and Other Value-Added Services), End User (Consumer & Retail, Home & Decor, Healthcare & Pharmaceuticals, FMCG, and Other End Users). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- United Parcel Service (UPS)

- FedEx Corp.

- XPO Logistics

- DSV

- DHL Supply Chain

- C.H. Robinson Worldwide

- Geodis

- Yusen Logistics

- CEVA Logistics

- Kuehne+Nagel

- ShipBob

- United States Postal Service (USPS)

- Excelsior Integrated LLC

- Ryder

- Kenco Logistics

- Yellow Corporation

- RXO Inc.

- ArcBest

- AP Express

- Bluebird Express

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce boom lifting return volumes

- 4.2.2 Liberal returns policies as a competitive differentiator

- 4.2.3 Sustainability & e-waste regulations

- 4.2.4 Automation & robotics in returns centers

- 4.2.5 AI-driven predictive return-prevention analytics

- 4.2.6 Monetization of recommerce marketplaces

- 4.3 Market Restraints

- 4.3.1 High transportation & handling costs

- 4.3.2 Omnichannel returns complexity

- 4.3.3 Rising returns fraud

- 4.3.4 Refurbish/recycle capacity bottlenecks for bulky goods

- 4.4 Value / Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Spotlight - US E-commerce Industry

- 4.9 Study on Changing Consumer Behavior & Preferences

- 4.10 Impact of Cost of Returns on Retailers - Analyst View

5 Market Size & Growth Forecasts

- 5.1 By Function

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Air

- 5.1.1.3 Other Modes

- 5.1.2 Warehousing (Storage, Distribution, Consolidation)

- 5.1.3 Other Value-added Services (Return Processing, Restocking, Refurbishment, Disposition)

- 5.1.1 Transportation

- 5.2 By End User

- 5.2.1 Consumer & Retail

- 5.2.2 Home & Decor

- 5.2.3 Healthcare & Pharmaceuticals

- 5.2.4 FMCG

- 5.2.5 Other End Users

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)}

- 6.4.1 United Parcel Service (UPS)

- 6.4.2 FedEx Corp.

- 6.4.3 XPO Logistics

- 6.4.4 DSV

- 6.4.5 DHL Supply Chain

- 6.4.6 C.H. Robinson Worldwide

- 6.4.7 Geodis

- 6.4.8 Yusen Logistics

- 6.4.9 CEVA Logistics

- 6.4.10 Kuehne+Nagel

- 6.4.11 ShipBob

- 6.4.12 United States Postal Service (USPS)

- 6.4.13 Excelsior Integrated LLC

- 6.4.14 Ryder

- 6.4.15 Kenco Logistics

- 6.4.16 Yellow Corporation

- 6.4.17 RXO Inc.

- 6.4.18 ArcBest

- 6.4.19 AP Express

- 6.4.20 Bluebird Express

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

逆向物流市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并提供 2026-2034 年的洞察和预测

逆向物流市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并提供 2026-2034 年的洞察和预测 逆向物流市场报告:按退货类型、服务、最终用户和地区划分(2026-2034 年)

逆向物流市场报告:按退货类型、服务、最终用户和地区划分(2026-2034 年) 2026-2030年全球逆向物流自动化软体市场

2026-2030年全球逆向物流自动化软体市场 逆向供应链解决方案市场按服务类型、技术、流程步骤、通路类型、材料类型、最终用户和应用划分-2026-2032年全球预测日本逆向物流市场报告(依退货类型、服务、最终用户和地区划分,2026-2034年)

逆向供应链解决方案市场按服务类型、技术、流程步骤、通路类型、材料类型、最终用户和应用划分-2026-2032年全球预测日本逆向物流市场报告(依退货类型、服务、最终用户和地区划分,2026-2034年) 逆向物流市场机会、成长要素、产业趋势分析及预测(2026年至2035年)

逆向物流市场机会、成长要素、产业趋势分析及预测(2026年至2035年) 逆向物流市场规模、份额和成长分析(按退货类型、服务、最终用户产业和地区划分)-2026-2033年产业预测

逆向物流市场规模、份额和成长分析(按退货类型、服务、最终用户产业和地区划分)-2026-2033年产业预测 2032年农业价值链逆向物流市场预测:按产品类型、逆向物流类型、最终用户和地区分類的全球分析可回收包装市场预测至2032年:逆向物流-按材料、包装类型、应用、最终用户和地区分類的全球分析

2032年农业价值链逆向物流市场预测:按产品类型、逆向物流类型、最终用户和地区分類的全球分析可回收包装市场预测至2032年:逆向物流-按材料、包装类型、应用、最终用户和地区分類的全球分析 全球逆向物流市场

全球逆向物流市场