|

市场调查报告书

商品编码

1939739

机上盒(STB):市场份额分析、行业趋势和统计数据、成长预测(2026-2031)Set-Top Box - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

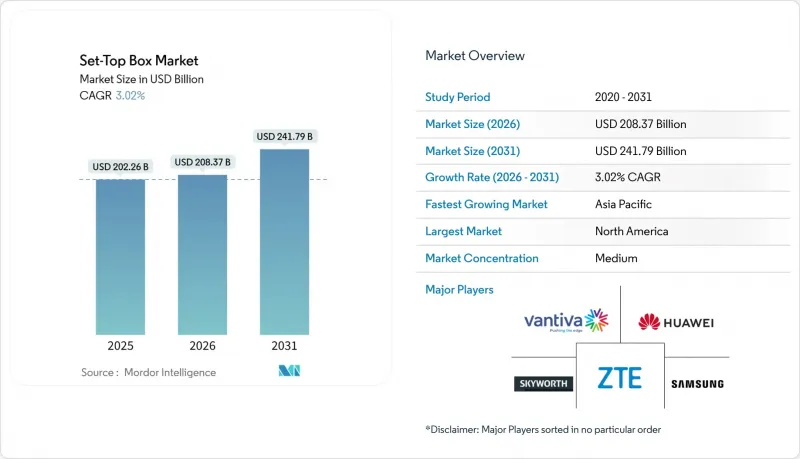

预计到 2026 年,机上盒 (STB) 市值将达到 2,022.7 亿美元,高于 2025 年的 2,047.2 亿美元。

预计到 2031 年,该产业规模将达到 1,904.4 亿美元,2026 年至 2031 年的复合年增长率为 -1.20%。

儘管预计成长为负,营运商仍在将传统接收设备转型为支援 IP 的枢纽,整合广播和串流媒体服务,降低软体授权费用,并减少能源消耗。光纤网路的部署、RDK 和 Android TV 等开放原始码平台以及混合 IP 闸道持续刺激着装置更新换代的需求。全球赛事前的超高清体育频道、新兴市场的 DTH OTT 整合服务以及 ESG主导的更新周期都在推动硬体创新。随着科技巨头纷纷推出集娱乐、智慧家居、电子商务和广告功能于一体的消费级设备,绕过营运商的发行网络,竞争日益激烈。

全球机上盒(STB)市场趋势与洞察

透过光纤基础设施向IP/混合机上盒迁移

欧洲有线电视业者在向光纤过渡的同时,也需要能够同时支援DOCSIS和全IP传输的机上盒,以在中期内继续使用HFC网路。 CommScope的DOCSIS 4.0试验表明,整合晶片组能够充分利用更高的上行频宽,这促使营运商采购混合型硬体。瑞典BoxerTV退出地面电波广播业务,凸显了向纯串流媒体传输模式的更广泛转变,加速了升级需求。

开放原始码RDK和Android TV降低了营运成本

Vantiva 已出货超过 1.25 亿台 RDK 设备和 2,200 万台 Android TV 设备,显示标准化技术堆迭能够降低授权成本并简化认证流程。印尼 Telkomsel 部署 200 万台 Android TV 设备,凸显了开放原始码在价格敏感市场中的强劲发展势头。营运商目前正在将 RDK 安全功能与 Android 应用目录整合到混合型机上盒中,以缩短产品上市时间,同时保持对使用者介面的控制。

北美和西欧有线电视取消用户数上升

光是2024年第四季,DISH和Sling就流失了25.3万付费电视用户,导致其提供的机上盒需求下降。英国广播公司(BBC)计划在2030年代转向纯网路广播,这表明即使是公共广播公司也认为传统分发方式的前景有限。

细分市场分析

到2025年,卫星广播将保持37.42%的市场份额,即使用户持续停掉有线电视服务有线电视,它仍将为机上盒(STB)市场奠定基础。在光纤网路发展的推动下,随着营运商将宽频、音讯和影像捆绑销售,IPTV预计将以0.83%的复合年增长率成长。有线电视正在经历从QAM到全IP的转换,而像巴西电视3.0这样的混合地面电波-OTT模式则将广播网路覆盖与互动串流媒体结合。虽然卫星机上盒(STB)市场依然庞大,但长期趋势正转向IP闸道。

营运商希望机上盒能够解码目前的DVB-S2讯号,并在未来支援HLS和DASH协议,这迫使供应商采用多重通讯协定晶片组。 Astundo在美国从QAM迁移到IPTV就是一个清晰的例子,它展示瞭如何将现有的有线电视基础设施改造用于管理型IP服务。预计到2025年,巴西的免费卫星电视用户数将达到900万,印证了付费和免费平台的市场需求。

由于生产线日趋成熟且频宽需求降低,高清(HD)将在2025年占据出货量的一半。超高清(UHD)/4K将以1.03%的复合年增长率推动成长,人工智慧辅助的图像升频技术使营运商无需拥有完整的原生内容库即可提供优质体验。中兴通讯的4K AI-SR机上盒功耗降低50%,速度提升29%,在提高解析度的同时实现了更高的效率。目前,支援超高清的机上盒市场份额虽然不大,但随着体育赛事拥有者强制要求4K分发,其市场份额正在稳步增长。

SEI Robotics 的 AI超高解析度装置弥合了原生 4K 串流播放能力有限与消费者对高清影像需求之间的差距,在降低营运商频宽的同时保持了画质。儘管原生 4K 体育赛事直播仍受制于製作成本,但混合式超解析度解决方案将保持成长动能。

区域分析

北美地区预计到2025年将贡献29.65%的收入,这主要得益于较高的每位用户平均收入(ARPU)和广泛的宽频普及。自2012年以来,能源效率法规已使设备的平均功耗降低了68%,迫使供应商采用更先进的晶片製程。持续的「停掉有线电视服务有线电视服务)趋势正迫使营运商转向全屋覆盖解决方案,将纯IP网关与Wi-Fi Mesh网路结合。

亚太地区正经历最快成长,复合年增长率达0.58%,这主要得益于印度、中国和印尼的光纤网路部署。中兴通讯和Telkomsel部署的200万台安卓电视表明,在价格敏感的市场中,通讯业者正在将宽频与OTT聚合服务捆绑销售。日本和韩国正在大力推广4K/HDR,为高阶机上盒打造了一个高端市场。

欧洲正经历分化趋势。由于串流媒体的兴起,西方市场正在萎缩,而东欧市场则继续推动地面电波和有线电视网络的数位化。欧盟的电子废弃物指令提高了回收成本,但也催生了对模组化、可维修硬体的需求。中东正结合国家发展规划,投资建置超高清卫星平台。预计到2029年,非洲将新增1,200万付费电视家庭,政府资金筹措包括低成本DVB-T2和卫星接收设备在内的费用。南美洲正着力推进巴西的TV 3.0计划,随着ATSC 3.0的推出,混合型机上盒在厂商的产品蓝图中继续占据重要位置。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 透过光纤基础设施向IP/混合机上盒迁移

- 利用开放原始码RDK和Android TV降低营运成本

- 大型赛事前夕,4K/HDR体育频道将播出。

- 新兴市场DTH捆绑式OTT聚合服务

- 促进非洲和东南亚的数位化

- 以ESG主导的低功耗CPE更新週期

- 市场限制

- 北美和西欧的停掉有线电视服务

- 灰色市场IPTV盗版设备

- 半导体成本上涨

- 严格的电子废弃物收集要求

- 产业价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 产业相关人员分析

- 宏观经济趋势评估

- 投资和资金筹措环境

第五章 市场规模与成长预测

- 透过技术

- 卫星广播/直播卫星(DTH)

- 电缆

- IPTV

- 数位地面广播/混合广播

- 通过决议

- SD

- HD

- 超高清/4K 以上分辨率

- 最终用户

- 住宅

- 商业/饭店

- 政府及教育机构

- 运输(航空、海运)

- 按作业系统

- Android-TV

- RDK

- Proprietary Linux

- 其他开放原始码

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 其他亚洲地区

- 中东

- 以色列

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Vantiva SA

- Samsung Electronics Co., Ltd.

- Huawei Technologies Co., Ltd.

- Skyworth Digital Technology Co., Ltd.

- Humax Holdings Co., Ltd.

- ZTE Corporation

- Sagemcom SAS

- Kaonmedia Co., Ltd.

- CommScope Holding Company, Inc.

- Shenzhen SDMC Technology Co., Ltd.

- Shenzhen Coship Electronics Co., Ltd.

- Evolution Digital LLC

- Technicolor Connected Home USA LLC

- Dish TV India Ltd.

- Tata Play Ltd.

- ARRIS International plc(re-branded)

- Apple Inc.(Apple TV 4K)

- Roku Inc.

- Amazon .com, Inc.(Fire TV Cube)

- DISH Network LLC(Hopper)

第七章 市场机会与未来展望

The set-top box market size in 2026 is estimated at USD 202.27 billion, growing from 2025 value of USD 204.72 billion with 2031 projections showing USD 190.44 billion, growing at -1.20% CAGR over 2026-2031.

Even with negative growth, operators are transforming traditional reception devices into IP-enabled hubs that unify broadcast and streaming services, cut software licensing fees, and lower energy use. Fiber network rollouts, open-source platforms such as RDK and Android TV, and hybrid IP gateways continue to stimulate replacement demand. UHD sports channels ahead of global tournaments, bundled OTT aggregation in emerging-market DTH, and ESG-driven refresh cycles sustain hardware innovation. Competitive intensity is rising as technology giants bypass operator distribution with direct-to-consumer devices that blend entertainment, smart-home, e-commerce, and advertising functions.

Global Set-Top Box Market Trends and Insights

Fiber-backed migration to IP/hybrid STBs

European cable groups shifting to fibre while retaining HFC for the medium-term need boxes that handle both DOCSIS and full-IP delivery. CommScope's DOCSIS 4.0 trials show unified chipsets that exploit higher upstream bandwidth, spurring operator purchase of hybrid hardware. Sweden's BoxerTV exit from terrestrial broadcast underscores a broader move toward streaming-only distribution that accelerates replacement demand.

Open-source RDK and Android-TV lowering opex

Vantiva has shipped more than 125 million RDK units and 22 million Android TV units, proving that standardized stacks trim licensing costs and simplify certification. Indonesia's Telkomsel deployed 2 million Android TV units, highlighting open-source momentum in price-sensitive markets. Operators now merge RDK security with Android's app catalogue inside hybrid boxes, accelerating time-to-market while keeping UI control.

Cord-cutting in North America and Western Europe

DISH and Sling lost 253,000 pay-TV subscribers in Q4 2024 alone, eroding demand for operator-supplied boxes. The BBC plans an internet-only switchover in the 2030s, signalling that even public broadcasters see a limited future for legacy distribution.

Other drivers and restraints analyzed in the detailed report include:

- 4K/HDR sports channels before mega-events

- Digitisation stimulus in Africa and SE-Asia

- Grey-market IPTV piracy devices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Satellite held a 37.42% share in 2025, anchoring the set-top box market despite cord-cutting. IPTV, supported by fiber rollouts, will grow at a 0.83% CAGR as operators bundle broadband, voice, and video. Cable's move to all-IP QAM replacement is underway, while hybrid DTT-OTT models such as Brazil's TV 3.0 combine broadcast reach with interactive streaming. The set-top box market size for satellite remains large, yet the long-term trajectory tilts toward IP gateways.

Operators want boxes that decode DVB-S2 today and HLS or DASH tomorrow, pressuring vendors to add multi-protocol chipsets. Astound's conversion from QAM to IPTV in the United States shows how legacy cable infrastructure is being repurposed for managed IP. Free-to-air satellite households in Brazil are projected to reach 9 million by 2025, underscoring dual demand for both pay and free platforms.

HD represents half of 2025 shipments due to mature production chains and lower bandwidth needs. UHD/4K will lead growth at 1.03% CAGR as AI-assisted upscaling enables operators to market premium experiences without full native content libraries. ZTE's 4K AI-SR box lowers power use by 50% and boosts speed by 29%, proving efficiency gains alongside resolution upgrades. The set-top box market share for UHD remains modest today but rises steadily as sports rights holders mandate 4K distribution.

AI super-resolution devices from SEI Robotics bridge the gap between scarce native 4K feeds and consumer appetite for sharper imagery, reducing operator bandwidth while sustaining quality. Native 4K live sports streaming is still limited by production costs, but hybrid upscaling solutions keep momentum intact.

The Set-Top Box Market Report is Segmented by Technology (Satellite/DTH, Cable, IPTV, DTT/Hybrid), Resolution (SD, HD, UHD/4K and Higher), End-User (Residential, Commercial/Hospitality, Government and Education, Transportation), Operating System (Android-TV, RDK, Proprietary Linux, Other Open-Source), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 29.65% revenue in 2025, anchored by high ARPU and widespread broadband. Energy-efficiency rules have cut average box power by 68% since 2012, prompting vendors to adopt advanced silicon nodes. Continuous cord-cutting forces operators to shift toward IP-only gateways paired with Wi-Fi mesh for whole-home coverage.

Asia-Pacific is the fastest-growing region at 0.58% CAGR, propelled by fiber buildouts in India, China, and Indonesia. ZTE and Telkomsel's 2 million-unit Android TV deployment showcases how telcos bundle broadband with OTT aggregators in price-sensitive markets. Japan and South Korea champion 4K/HDR, creating premium niches for high-spec boxes.

Europe shows a bifurcated trend: Western markets decline with streaming adoption, while Eastern markets still digitize terrestrial and cable networks. EU e-waste directives raise recycling costs yet also open demand for modular, repairable hardware. The Middle East invests in UHD satellite platforms linked to national Vision programs. Africa expects 12 million additional pay-TV homes by 2029, often financed through state vouchers that include low-cost DVB-T2 or satellite kits. South America's focus on Brazil's TV 3.0 keeps hybrid boxes on vendor roadmaps as ATSC 3.0 launches.

- Vantiva SA

- Samsung Electronics Co., Ltd.

- Huawei Technologies Co., Ltd.

- Skyworth Digital Technology Co., Ltd.

- Humax Holdings Co., Ltd.

- ZTE Corporation

- Sagemcom SAS

- Kaonmedia Co., Ltd.

- CommScope Holding Company, Inc.

- Shenzhen SDMC Technology Co., Ltd.

- Shenzhen Coship Electronics Co., Ltd.

- Evolution Digital LLC

- Technicolor Connected Home USA LLC

- Dish TV India Ltd.

- Tata Play Ltd.

- ARRIS International plc (re-branded)

- Apple Inc. (Apple TV 4K)

- Roku Inc.

- Amazon .com, Inc. (Fire TV Cube)

- DISH Network L.L.C. (Hopper)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Fibre-backed migration to IP/hybrid STBs

- 4.2.2 Open-source RDK and Android-TV lowering opex

- 4.2.3 4K / HDR sports channels before mega-events

- 4.2.4 Bundled OTT aggregation in emerging-market DTH

- 4.2.5 Digitisation stimulus in Africa and SE-Asia

- 4.2.6 ESG-driven low-power CPE refresh cycles

- 4.3 Market Restraints

- 4.3.1 Cord-cutting in N. America and W. Europe

- 4.3.2 Grey-market IPTV piracy devices

- 4.3.3 Semiconductor cost inflation

- 4.3.4 Strict e-waste take-back mandates

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Industry Stakeholder Analysis

- 4.9 Assessment of Macroeconomic Trends

- 4.10 Investment and Funding Landscape

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Satellite / DTH

- 5.1.2 Cable

- 5.1.3 IPTV

- 5.1.4 DTT / Hybrid

- 5.2 By Resolution

- 5.2.1 SD

- 5.2.2 HD

- 5.2.3 UHD / 4K and Higher

- 5.3 By End-User

- 5.3.1 Residential

- 5.3.2 Commercial / Hospitality

- 5.3.3 Government and Education

- 5.3.4 Transportation (Airline, Maritime)

- 5.4 By Operating System

- 5.4.1 Android-TV

- 5.4.2 RDK

- 5.4.3 Proprietary Linux

- 5.4.4 Other Open-Source

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Vantiva SA

- 6.4.2 Samsung Electronics Co., Ltd.

- 6.4.3 Huawei Technologies Co., Ltd.

- 6.4.4 Skyworth Digital Technology Co., Ltd.

- 6.4.5 Humax Holdings Co., Ltd.

- 6.4.6 ZTE Corporation

- 6.4.7 Sagemcom SAS

- 6.4.8 Kaonmedia Co., Ltd.

- 6.4.9 CommScope Holding Company, Inc.

- 6.4.10 Shenzhen SDMC Technology Co., Ltd.

- 6.4.11 Shenzhen Coship Electronics Co., Ltd.

- 6.4.12 Evolution Digital LLC

- 6.4.13 Technicolor Connected Home USA LLC

- 6.4.14 Dish TV India Ltd.

- 6.4.15 Tata Play Ltd.

- 6.4.16 ARRIS International plc (re-branded)

- 6.4.17 Apple Inc. (Apple TV 4K)

- 6.4.18 Roku Inc.

- 6.4.19 Amazon .com, Inc. (Fire TV Cube)

- 6.4.20 DISH Network L.L.C. (Hopper)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

机上盒市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、功能、安装类型、设备划分

机上盒市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、功能、安装类型、设备划分 全球机上盒(STB)市场规模、份额、趋势和成长分析报告(2026-2034)

全球机上盒(STB)市场规模、份额、趋势和成长分析报告(2026-2034) 2026年全球机上盒市场报告全球安卓机上盒(STB)和电视市场报告(2026 年)

2026年全球机上盒市场报告全球安卓机上盒(STB)和电视市场报告(2026 年) 高清机上盒市场按类型、设备、最终用户和分销管道划分 - 全球预测 2026-2032

高清机上盒市场按类型、设备、最终用户和分销管道划分 - 全球预测 2026-2032 安卓机上盒和电视市场规模、份额及成长分析(按类型、分销管道、应用和地区划分)-2026-2033年产业预测

安卓机上盒和电视市场规模、份额及成长分析(按类型、分销管道、应用和地区划分)-2026-2033年产业预测 机上盒市场规模、份额和成长分析(按技术、解析度、通路、应用、作业系统、录製功能和地区划分)-2026-2033年产业预测

机上盒市场规模、份额和成长分析(按技术、解析度、通路、应用、作业系统、录製功能和地区划分)-2026-2033年产业预测 4K机上盒市场规模、份额和成长分析(按产品类型、价格分布、应用和地区划分)-产业预测(2026-2033年)

4K机上盒市场规模、份额和成长分析(按产品类型、价格分布、应用和地区划分)-产业预测(2026-2033年) 机上盒市场-全球产业规模、份额、趋势、机会和预测,依产品类型、内容品质、服务、最终用户、地区和竞争格局划分,2020-2030年预测

机上盒市场-全球产业规模、份额、趋势、机会和预测,依产品类型、内容品质、服务、最终用户、地区和竞争格局划分,2020-2030年预测 机上盒市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

机上盒市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测