|

市场调查报告书

商品编码

1939748

数位双胞胎(DT):市场占有率分析、产业趋势与统计、成长预测(2026-2031)Digital Twin (DT) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

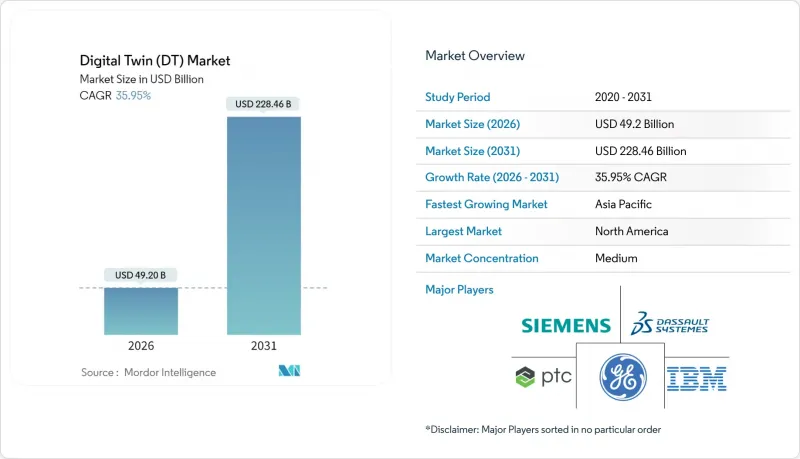

2025 年数位双胞胎市场价值 361.9 亿美元,预计到 2031 年将达到 2,284.6 亿美元,高于 2026 年的 492 亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 35.95%。

利好因素包括工业IoT平台的成熟、边缘人工智慧的广泛应用以及安全关键型基础设施的监管要求。儘管製造业凭藉已建立的智慧工厂投资仍是最大的应用领域,但石油和天然气产业正经历最强劲的成长,这主要得益于生产商对在恶劣运作环境下提升资产健康状况的需求。北美保持领先地位,但随着中国、印度和日本的公共计画资助大规模数位化,亚太地区正在缩小差距。虽然解决方案目前占据了大部分支出,但随着企业寻求整合方面的专业知识,服务也在快速成长。云端采用速度超过了本地部署,这表明人们对安全远端资料管理和可扩展架构的信心日益增强。网路安全漏洞和基于实体建模的人才短缺限制了成长前景,但尚未改变主要的采用方向。

全球数位双胞胎(DT)市场趋势与洞察

工业IoT平台快速发展

工业物联网 (IIoT) 的广泛应用可提供即时数据,使数位模型与工厂车间保持同步。西门子报告称,其数位化业务收入在 2024 年将达到 90 亿欧元(97.2 亿美元),较上年增长 22%,这主要得益于其 Xcelerator 生态系统的强大实力。Honeywell的 Forge 平台每天处理超过 30 亿个资料点,可将客户工厂的非计划停机时间减少 35%。 OPC UA 和 MQTT 等标准化通讯协定降低了整合摩擦,使工厂能够在数週内而非数月内部署数位双胞胎模型。最终成果包括:持续的成本节约、更快的根本原因分析以及更具预测性的产能规划。

在设备层面扩展边缘/AI推理

将分析处理从云端迁移到边缘可以降低延迟并保障资料主权。微软和西门子共同开发的工业基础设施模型可在资产层级执行推理,从而实现毫秒级异常检测响应。奥迪目前透过部署在边缘的孪生体运行虚拟PLC,优化其实际生产线的週期时间。本地模拟还能降低频宽消耗,因为只有异常资料才会向上游发送。专用晶片和容器化运行时进一步降低了二级供应商的部署成本,加速了人工智慧孪生体在整个价值链中的应用。

IT/OT堆迭中的网实整合安全漏洞

西班牙国家网路安全研究所指出,连接IT和OT的孪生系统扩大了攻击面,并将製程控制器暴露于资料完整性威胁之下。最近一次勒索软体攻击迫使一家製造商停产数日,以便清理其孪生资料湖。零信任架构的整合和员工培训导致平均实施延迟18个月。多租户孪生系统增加了复杂性,需要在不影响协作的情况下对合作伙伴的存取权限进行划分。

细分市场分析

到2025年,製造业将占据数位双胞胎市场35.10%的份额,这主要得益于嵌入式工业物联网感测器、预测性维护程序以及持续改进的文化。汽车和电子工厂正在实施生产线级数数位双胞胎,以分析节拍时间的变化以及品质和产量比率模式,从而实现两位数的废品率下降。能源效率的提升,尤其是在资源密集的冶金和水泥产业,将带来进一步的投资回报。预计即使其他行业迎头赶上,该领域仍将稳步成长并保持其市场领先地位。

目前规模较小的油气产业预计到2031年将以28.1%的复合年增长率成长,这主要得益于海上业者对远端侦测和故障隔离能力的需求。上游公司正在部署储存联技术,该技术整合了地震资料和生产记录,使工程师能够在部署钻井平台之前模拟油井维修场景。中游公司正在利用管道双联技术进行洩漏检测,而下游炼油厂(例如壳牌公司)已证明,透过检验DNV标准的双联技术,计划外停机时间减少了20%。政府的脱碳目标也在推动双联技术的应用,该技术有助于最大限度地减少火炬燃烧并优化热整合策略。在上述两个领域,人工智慧辅助的情境测试正在推动双联技术从监测系统转向决策支援系统转变,从而提高其整体应用率。

到2025年,解决方案类别(软体平台、实体引擎、连接硬体)的支出占总支出的62.85%,因为企业正在获取核心能力。供应商将建模库与视觉化引擎捆绑在一起,使流程工程师无需从头开始编写程式码即可建立模型。授权模式正转向基于使用量的分级模式,从而扩大了二级供应商的存取权限。

同时,服务领域正以30%的复合年增长率快速扩张。实施咨询服务包括资料管道调优、语意模型建构和模拟精度检验。託管服务合约监控孪生健康指标、应用修补程式并调整漂移预防演算法,从而为资产所有者带来可预测的营运成本。随着基于结果的合约日益普及(例如,劳斯莱斯的TotalCare基于孪生分析保证引擎运转率),服务合作伙伴承担了更多风险,并采用与效率提升挂钩而非按工时计费的收费系统。这种模式增强了客户忠诚度,并鼓励平台持续改进。

数位双胞胎市场报告按应用(製造业、能源电力、航太与国防、石油天然气、汽车等)、组件(解决方案/平台、服务)、部署类型(本地部署、云端部署)、公司规模(大型企业、中小企业)和地区进行细分。

区域分析

到2025年,北美将占据数位双胞胎市场37.95%的收入份额,这主要得益于工业4.0的早期应用、大规模航太项目以及工业SaaS领域强劲的创业融资。美国航空监管机构核准基于模拟的认证,正推动飞机原始设备製造商(OEM)和一级供应商在数位孪生技术方面进行广泛的投资。加拿大和美国的能源巨头正在实施管道和LNG接收站的数位孪生技术,以降低甲烷外洩率,符合日益严格的环境政策。成熟的网路保险框架和标准化的资料保护要求尤其推动了云端运算的普及。

亚太地区以26.0%的复合年增长率领跑,主要得益于政府主导的大型企划。中国的「数位中国建设计画」要求为新建基础设施创建城市数位双胞胎,为国内外供应商创造了大量的采购机会。印度的「桑格姆数位双胞胎计画」将网路孪生能力融入其全国性的6G电信升级计画。日本NTT数位双胞胎计算倡议支援城市规模的数位孪生复製,以优化交通和灾害应变演算法。韩国和新加坡正在推进智慧工厂和港口试点项目,重点关注即时碳足迹追踪。该地区在供应链中的中心地位使其能够迅速将相关洞察传递给全球原始设备製造商(OEM)。

在欧洲,监管要求正日益受到重视并稳步推进。数位产品护照要求製造商在产品生命週期内实现可追溯性,这实际上强制要求大规模生产的产品采用轻量化的「孪生」模式。德国的「工业4.0平台」提供标准化的管理框架指南,减轻了中小企业的整合负担。法国正在投资虚拟造船厂的「孪生」模式,以维持其在海军建设领域的竞争优势;北欧国家则利用建筑「孪生」模式来实现净零排放标准。中东和非洲地区虽然尚不成熟,但前景广阔:阿联酋和沙乌地阿拉伯正在试点油田「孪生」和计划城市「孪生」模式,以在大规模扩张之前探索其在效率和永续性方面的益处。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 工业IoT平台快速发展

- 在设备层面扩展边缘/AI推理

- 资产密集产业安全关键基础设施数位化监管进步

- 现有设施计划对虚拟试运行的需求日益增长,以降低资本支出 (CAPEX)。

- 基于结果的服务合约的兴起需要即时资产副本数据

- 欧盟和美国数位产品护照的兴起

- 市场限制

- IT/OT堆迭中的网实整合安全漏洞

- 某些领域缺乏基于物理的建模方面的专业知识

- 联邦孪生体产生的资料的智慧财产权所有权不透明

- 仿真标准的碎片化限制了互通性。

- 重要法规结构评估

- 价值链分析

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 关键相关人员影响评估

- 主要用例和案例研究

- 宏观经济因素对市场的影响

- 投资分析

第五章 市场区隔

- 透过使用

- 製造业

- 能源与电力

- 航太/国防

- 石油和天然气

- 车

- 其他的

- 按组件

- 解决方案/平台

- 服务

- 透过部署模式

- 本地部署

- 云

- 按公司规模

- 大公司

- 中小企业

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 其他欧洲地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 埃及

- 奈及利亚

- 其他非洲地区

- 中东

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ASEAN

- 澳洲

- 纽西兰

- 亚太其他地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- ANSYS, Inc.

- AVEVA Group plc

- Bentley Systems, Incorporated

- Cal-Tek SRL

- Cityzenith, Inc.

- Dassault Systemes SE

- General Electric Company

- Hexagon AB

- International Business Machines Corporation

- Lanner Group Limited(Royal HaskoningDHV)

- Mevea Ltd.

- Microsoft Corporation

- Oracle Corporation

- PTC Inc.

- Rescale, Inc.

- Robert Bosch GmbH(Bosch.IO)

- SAP SE

- Schneider Electric SE

- Siemens AG

- Amazon Web Services, Inc.

第七章 市场机会与未来展望

The digital twin market was valued at USD 36.19 billion in 2025 and estimated to grow from USD 49.2 billion in 2026 to reach USD 228.46 billion by 2031, at a CAGR of 35.95% during the forecast period (2026-2031).

Tailwinds include the maturation of industrial IoT platforms, wider edge-AI deployment, and regulatory requirements for safety-critical infrastructure. Manufacturing remains the largest application thanks to established smart-factory investments, while Oil and Gas shows the strongest growth as producers seek asset-integrity gains in harsh operating conditions. Regionally, North America retains the lead, but Asia-Pacific is closing the gap as public programs in China, India, and Japan channel funding toward large-scale digitalization. Solutions account for most spending today, yet services are scaling quickly as firms seek integration expertise. Cloud deployment is growing faster than on-premises, signaling rising confidence in remote data-management safeguards and scalable architectures. Cyber-security gaps and scarce physics-based modeling talent temper the growth outlook, though they have not altered the primary trajectory of adoption.

Global Digital Twin (DT) Market Trends and Insights

Rapid growth of industrial IoT platforms

Widespread IIoT deployment supplies real-time data that keeps digital models synchronized with factory floors. Siemens reported EUR 9 billion (USD 9.72 billion) digital business revenue in 2024, up 22% on the strength of its Xcelerator ecosystem. Honeywell's Forge platform processes 3 billion+ datapoints daily, cutting unplanned downtime by 35% in client plants. Standardized protocols such as OPC UA and MQTT reduce integration friction, enabling plants to deploy twins in weeks rather than months. The result is steady cost avoidance, quicker root-cause analysis, and more predictable capacity planning.

Expansion of edge/AI inference at the device level

Moving analytics from cloud to edge trims latency and preserves data sovereignty. Microsoft and Siemens co-developed Industrial Foundation Models that run inference at the asset, allowing millisecond-level responses for anomaly detection. Audi now operates virtual PLCs through edge-deployed twins that optimize cycle times in real manufacturing lines. Local simulation also limits bandwidth consumption because only exception of data moves upstream. Specialized chips and containerized runtimes further cut deployment costs for tier-two suppliers, accelerating the spread of AI-ready twins throughout value chains.

Cyber-physical security vulnerabilities across IT/OT stacks

The Spanish National Cybersecurity Institute notes that twins bridging IT and OT widen attack surfaces, exposing process controllers to data-integrity threats. Recent ransomware events forced manufacturers to halt production for days while cleansing twin data lakes. Average deployment delays of 18 months arise as firms integrate zero-trust architectures and train staff. Multi-tenant twins add complexity because partner access must be segmented without slowing collaboration.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory push for asset-intensive industries to digitise safety-critical infrastructure

- Demand for virtual commissioning to cut CAPEX

- Shortage of domain-specific physics-based modelling expertise

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing contributed 35.10% of the digital twin market in 2025 thanks to embedded IIoT sensors, predictive maintenance programs, and continuous-improvement cultures. Automotive and electronics plants deploy line-level twins to analyze takt-time fluctuations and quality-yield patterns, trimming scrap rates by double digits. Energy-efficiency gains add another payback layer, particularly in resource-intensive metallurgy and cement operations. The segment is forecast to expand steadily, preserving its quantitative edge even as other verticals catch up.

Oil and Gas, though smaller today, is projected to grow at a 28.1% CAGR to 2031 as offshore operators require remote inspection and fault-isolation capabilities. The upstream segment deploys reservoir twins that integrate seismic data and production logs, allowing engineers to simulate well-workover scenarios before mobilizing rigs. Midstream companies apply pipeline twins for leak detection, while downstream refineries like Shell have documented 20% unplanned downtime reductions using twins verified by DNV standards. Government decarbonization targets further propel adoption as twins optimize flare minimization and heat-integration strategies. Across both segments, AI-assisted scenario testing elevates twins from monitoring to decision-support systems, reinforcing their share of total deployments.

The solutions category-software platforms, physics engines, and connected hardware-accounted for 62.85% of spending in 2025 as companies acquired core capabilities. Vendors bundle modeling libraries with visualization engines so process engineers can assemble replicas without coding from scratch. Licensing models are shifting to consumption-based tiers, broadening access among tier-two suppliers.

Services, however, are scaling faster at a 30% CAGR. Implementation consultancies align data pipelines, create semantic models, and validate simulation fidelity. Managed-service contracts monitor twin health metrics, apply patches, and tune algorithms for drift, yielding predictable OPEX for asset owners. As outcome-based agreements proliferate-Rolls-Royce TotalCare guarantees engine uptime backed by twin analytics-service partners assume more risk, tying fees to efficiency gains rather than billable hours. This model strengthens customer loyalty and encourages continuous platform enhancements.

The Digital Twin Market Report is Segmented by Application (Manufacturing, Energy and Power, Aerospace and Defense, Oil and Gas, Automotive, and Others), Component (Solutions/Platforms, and Services), Deployment Mode (On-Premises, and Cloud), Enterprise Size (Large Enterprises, and Small and Medium Enterprises (SMEs)), and Geography.

Geography Analysis

North America commanded 37.95% of digital twin market revenue in 2025 driven by early Industry 4.0 rollouts, extensive aerospace programs, and robust venture funding for industrial SaaS. U.S. aviation regulators' acceptance of simulation-based certification has spurred widespread twin investment among aircraft OEMs and Tier-1 suppliers. Energy majors in Canada and the United States deploy pipeline and LNG terminal twins to cut methane leak rates, aligning with tightening environmental policy. Cloud adoption is particularly strong due to mature cyber-insurance frameworks and standardized data-protection mandates.

Asia-Pacific posts the highest CAGR at 26.0%, supported by government megaprojects. China's Digital China Construction plan mandates urban digital twins for new infrastructure, creating large procurement pipelines for domestic and foreign vendors. India's Sangam Digital Twin scheme integrates network twin capability into nationwide telecom upgrades as the country moves toward 6G readiness. Japan's NTT Digital Twin Computing Initiative supports city-scale replicas that feed transportation and disaster-response algorithms. South Korea and Singapore push smart-factory and smart-port pilots, emphasizing real-time carbon-footprint tracking. The region's supply-chain centrality means lessons learned here propagate quickly to global OEMs.

Europe advances steadily as regulatory imperatives take center stage. The digital product passport forces manufacturers to embed traceability across product life cycles, effectively making a lightweight twin mandatory for high-volume goods. Germany's Plattform Industrie 4.0 provides standardized administration shell guidelines, reducing integration overhead for SMEs. France invests in virtual shipyard twins to maintain competitive edge in naval construction, while the Nordics use building twins to meet net-zero codes. The Middle East and Africa remain nascent but promising: the UAE and Saudi Arabia are piloting oil-field twins and giga-project city twins, seeking efficiency and sustainability benefits prior to large-scale expansion.

- ANSYS, Inc.

- AVEVA Group plc

- Bentley Systems, Incorporated

- Cal-Tek S.R.L.

- Cityzenith, Inc.

- Dassault Systemes SE

- General Electric Company

- Hexagon AB

- International Business Machines Corporation

- Lanner Group Limited (Royal HaskoningDHV)

- Mevea Ltd.

- Microsoft Corporation

- Oracle Corporation

- PTC Inc.

- Rescale, Inc.

- Robert Bosch GmbH (Bosch.IO)

- SAP SE

- Schneider Electric SE

- Siemens AG

- Amazon Web Services, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid growth of industrial IoT platforms

- 4.2.2 Expansion of edge/AI inference at the device level

- 4.2.3 Regulatory push for asset-intensive industries to digitise safety-critical infrastructure

- 4.2.4 Demand for virtual commissioning to cut CAPEX in brownfield projects

- 4.2.5 Rise of outcome-based service contracts needing real-time asset replica data

- 4.2.6 Proliferation of digital product passports in EU and U.S.

- 4.3 Market Restraints

- 4.3.1 Cyber-physical security vulnerabilities across IT/OT stacks

- 4.3.2 Shortage of domain-specific physics-based modelling expertise

- 4.3.3 Opaque IP ownership of data generated in federated twins

- 4.3.4 Fragmentation of simulation standards limiting interoperability

- 4.4 Evaluation of Critical Regulatory Framework

- 4.5 Value Chain Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact Assessment of Key Stakeholders

- 4.9 Key Use Cases and Case Studies

- 4.10 Impact on Macroeconomic Factors of the Market

- 4.11 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Application

- 5.1.1 Manufacturing

- 5.1.2 Energy and Power

- 5.1.3 Aerospace and Defense

- 5.1.4 Oil and Gas

- 5.1.5 Automotive

- 5.1.6 Others

- 5.2 By Component

- 5.2.1 Solutions/Platforms

- 5.2.2 Services

- 5.3 By Deployment Mode

- 5.3.1 On-premises

- 5.3.2 Cloud

- 5.4 By Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises (SMEs)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Nordics

- 5.5.3.7 Rest of Europe

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Turkey

- 5.5.4.1.4 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Nigeria

- 5.5.4.2.4 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 Asia-Pacific

- 5.5.5.1 China

- 5.5.5.2 India

- 5.5.5.3 Japan

- 5.5.5.4 South Korea

- 5.5.5.5 ASEAN

- 5.5.5.6 Australia

- 5.5.5.7 New Zealand

- 5.5.5.8 Rest of Asia-Pacific

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ANSYS, Inc.

- 6.4.2 AVEVA Group plc

- 6.4.3 Bentley Systems, Incorporated

- 6.4.4 Cal-Tek S.R.L.

- 6.4.5 Cityzenith, Inc.

- 6.4.6 Dassault Systemes SE

- 6.4.7 General Electric Company

- 6.4.8 Hexagon AB

- 6.4.9 International Business Machines Corporation

- 6.4.10 Lanner Group Limited (Royal HaskoningDHV)

- 6.4.11 Mevea Ltd.

- 6.4.12 Microsoft Corporation

- 6.4.13 Oracle Corporation

- 6.4.14 PTC Inc.

- 6.4.15 Rescale, Inc.

- 6.4.16 Robert Bosch GmbH (Bosch.IO)

- 6.4.17 SAP SE

- 6.4.18 Schneider Electric SE

- 6.4.19 Siemens AG

- 6.4.20 Amazon Web Services, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

工业数位化技术展望:2026

工业数位化技术展望:2026 数位双胞胎市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、部署类型、最终用户、功能和解决方案划分

数位双胞胎市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、部署类型、最终用户、功能和解决方案划分 全球数位双胞胎市场规模、份额、趋势和成长分析报告(2026-2034年)

全球数位双胞胎市场规模、份额、趋势和成长分析报告(2026-2034年) V2X数位双胞胎分析市场机会、成长要素、产业趋势分析及2026年至2035年预测

V2X数位双胞胎分析市场机会、成长要素、产业趋势分析及2026年至2035年预测 数位双胞胎市场规模、份额、趋势及预测(按类型、技术、应用和地区划分,2026-2034年)数位双胞胎技术市场-2026-2031年预测

数位双胞胎市场规模、份额、趋势及预测(按类型、技术、应用和地区划分,2026-2034年)数位双胞胎技术市场-2026-2031年预测 3D点云软体市场按元件、部署类型、平台、应用程式和最终用户产业划分-2026-2032年全球预测农业数位双胞胎技术市场:按组件、实施类型、组织规模、应用和最终用户分類的全球预测(2026-2032年)数位双胞胎技术市场:2026-2032年全球预测(依组织规模、产品/服务、技术、应用、最终用户产业和部署类型划分)日本数位孪生市场规模、份额、趋势及预测(按类型、技术、最终用途和地区划分),2026-2034年

3D点云软体市场按元件、部署类型、平台、应用程式和最终用户产业划分-2026-2032年全球预测农业数位双胞胎技术市场:按组件、实施类型、组织规模、应用和最终用户分類的全球预测(2026-2032年)数位双胞胎技术市场:2026-2032年全球预测(依组织规模、产品/服务、技术、应用、最终用户产业和部署类型划分)日本数位孪生市场规模、份额、趋势及预测(按类型、技术、最终用途和地区划分),2026-2034年