|

市场调查报告书

商品编码

1959283

V2X数位双胞胎分析市场机会、成长要素、产业趋势分析及2026年至2035年预测V2X Digital Twin Analytics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

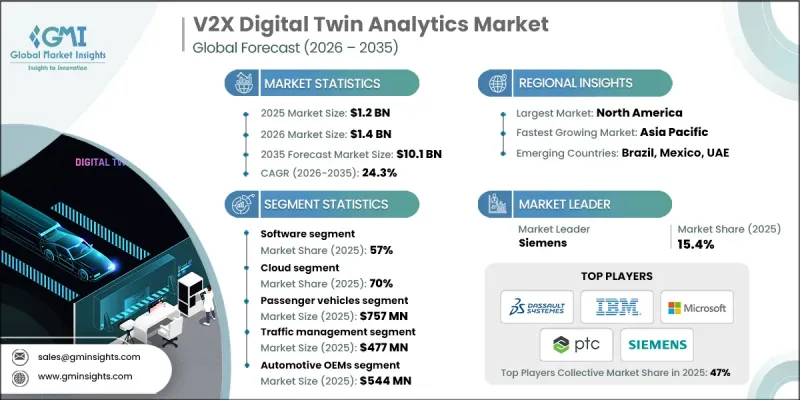

2025 年全球 V2X数位双胞胎分析市场价值 12 亿美元,预计到 2035 年将达到 101 亿美元,复合年增长率为 24.3%。

这一增长是由互联出行生态系统的加速转型和智慧型运输系统的日益融合所驱动的。出行网路中的相关人员越来越依赖资料驱动平台来提升安全性、提高交通效率,并应对排放气体严格的排放和资料管治监管要求。数位双胞胎分析解决方案因其能够实现跨交通网路的即时视觉化、高阶模拟和预测性决策而备受关注。分析引擎、通讯技术和整合资料架构的不断进步正在改变出行营运的规划和管理方式。市场参与企业正稳步转向灵活、云端化且可互通的平台,以支援即时洞察和主动系统最佳化。随着全球数位基础设施的日益成熟,V2X数位双胞胎分析正成为建构智慧、高效且具韧性的出行框架的关键推动因素。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 12亿美元 |

| 预测金额 | 101亿美元 |

| 复合年增长率 | 24.3% |

软体领域占57%的市场份额,预计2026年至2035年将以24.8%的复合年增长率成长。软体解决方案透过提供先进的建模能力、持续模拟和智慧数据处理,为数数位双胞胎分析奠定了基础。这些平台支援高精度、扩充性和运作控制,使其成为管理复杂交通环境的关键。它们提供即时洞察和预测智慧的能力持续推动着整个交通生态系统的应用。

预计到2025年,基于云端的细分市场将占据70%的市场份额,并在2035年之前以24.6%的复合年增长率成长。云端平台因其适应性强、资料集中存取以及支援高级分析(无需大规模基础设施投资)而备受青睐。它们能够实现无缝资料整合、快速扩充性和远端系统管理,从而显着提高地理位置分散的行动网路的营运效率。

预计到2025年,北美V2X数位双胞胎分析市场将占据83%的市场份额,并创造3.547亿美元的收入。强大的数位基础设施、先进的连接框架以及智慧行动技术的早期应用,巩固了该地区的主导地位。美国持续受益于其强大的创新生态系统、大规模的行动旅行计画以及完善的法规结构,这些都促进了高阶分析技术的应用。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 联网汽车和自动驾驶汽车的快速发展

- 与智慧城市和智慧交通系统相关的倡议

- 高级人工智慧/机器学习和边缘到云端分析

- 关于安全和排放的监管压力

- 产业潜在风险与挑战

- 高昂的实施成本

- 资料隐私、安全性和互通性挑战

- 市场机会

- 在亚太和新兴市场拓展业务

- 与自动驾驶车辆和车队管理系统集成

- 监管合规和安全解决方案

- 车队和物流优化

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 美国:国家公路交通安全管理局 (NHTSA) 和联邦通讯委员会 (FCC) 指南

- 加拿大:运输部与创新、科学及经济发展部指南

- 欧洲

- 德国:联邦交通和数位基础设施部

- 法国:生态系转型部

- 英国:运输部

- 义大利:基础设施和运输部

- 亚太地区

- 中国:工业和资讯化部

- 日本国土交通省

- 韩国国土交通部

- 印度:公路运输与公路部

- 拉丁美洲

- 巴西:国家交通运输署

- 墨西哥:通讯与运输部部 (SCT)

- 中东和非洲

- 阿拉伯联合大公国:工业与先进技术部

- 沙乌地阿拉伯:沙乌地阿拉伯标准、计量和品质研究院

- 北美洲

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 成本細項分析

- 专利分析

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 具有环保意识的倡议

- 碳足迹考量

- 使用案例场景

- 资料架构和互通性框架

- 对网路安全、资料管治和功能安全的影响

- 实施和商业化模式

第四章 竞争情势

- 介绍

- 企业市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划及资金筹措

第五章 市场估计与预测:依组件划分,2022-2035年

- 软体

- 数位双胞胎平台

- 模拟和建模引擎

- 分析和人工智慧软体

- 硬体

- 边缘运算设备

- 感测器和路侧单元

- 汽车计算单元

- 服务

- 整合与实施

- 託管分析服务

- 咨询和定制

第六章 市场估价与预测:依车辆类型划分,2022-2035年

- 搭乘用车

- 掀背车车

- 轿车

- SUV

- 商用车辆

- 轻型商用车(LCV)

- 中型商用车(MCV)

- 重型商用车(HCV)

第七章 市场估计与预测:依应用领域划分,2022-2035年

- 交通管理

- 预测性保护

- 车队管理

- 安全保障

- 自动驾驶

第八章 市场估算与预测:依部署类型划分,2022-2035年

- 云

- 现场

第九章 市场估计与预测:依最终用途划分,2022-2035年

- 汽车製造商

- 政府和交通运输部门

- 车队营运商

- 其他的

第十章 市场估价与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 比利时

- 荷兰

- 瑞典

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 新加坡

- 韩国

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 阿拉伯聯合大公国

- 南非

- 沙乌地阿拉伯

第十一章:公司简介

- Global Player

- ANSYS

- Dassault Systemes

- EZ Crusher

- Hexagon

- IBM

- Keestrack

- Microsoft

- OverBuilt

- PTC

- Siemens

- Regional Player

- Al-Jon Manufacturing

- Eagle Crusher Company

- Fayat

- Hammel Recyclingtechnik

- Liebherr

- McCloskey International

- Metso Outotec

- Sandvik

- Sierra International Machinery

- Terex

- 新兴企业

- BHS-Sonthofen

- Komplet America

- Mobile Crushers International

- Rockster Recycler

- Rubble Master

The Global V2X Digital Twin Analytics Market was valued at USD 1.2 billion in 2025 and is estimated to grow at a CAGR of 24.3% to reach USD 10.1 billion by 2035.

Growth is fueled by the accelerating shift toward connected mobility ecosystems and the rising integration of intelligent transportation systems. Stakeholders across mobility networks increasingly rely on data-driven platforms to enhance safety outcomes, improve traffic efficiency, and meet tightening regulatory expectations related to emissions and data governance. Digital twin analytics solutions are gaining traction as they enable real-time visibility, advanced simulation, and predictive decision-making across transportation networks. Continuous progress in analytics engines, communication technologies, and integrated data architectures is reshaping how mobility operations are planned and managed. Market participants are steadily moving toward flexible, cloud-enabled, and interoperable platforms that support real-time insights and proactive system optimization. As digital infrastructure matures globally, V2X digital twin analytics is becoming a critical enabler of intelligent, efficient, and resilient mobility frameworks.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.2 Billion |

| Forecast Value | $10.1 Billion |

| CAGR | 24.3% |

The software segment held 57% share and is forecast to grow at a CAGR of 24.8% from 2026 to 2035. Software solutions form the foundation of digital twin analytics by delivering advanced modeling capabilities, continuous simulation, and intelligent data processing. These platforms support high levels of accuracy, scalability, and operational control, making them essential for managing complex mobility environments. Their ability to deliver real-time insights and predictive intelligence continues to drive widespread adoption across transportation ecosystems.

The cloud-based segment held 70% share in 2025 and is anticipated to grow at a CAGR of 24.6% through 2035. Cloud platforms are favored for their adaptability, centralized data access, and support for advanced analytics without heavy infrastructure investment. They enable seamless data integration, rapid scalability, and remote system management, which significantly enhances operational efficiency across geographically distributed mobility networks.

North America V2X Digital Twin Analytics Market held 83% share and generated USD 354.7 million in 2025. Strong digital infrastructure, advanced connectivity frameworks, and early adoption of intelligent mobility technologies have supported regional leadership. The U.S. continues to benefit from robust innovation ecosystems, large-scale mobility programs, and established regulatory frameworks that encourage advanced analytics deployment.

Key companies active in the Global V2X Digital Twin Analytics Market include Siemens, Microsoft, IBM, Dassault Systemes, ANSYS, Hexagon, PTC, OverBuilt, EZ Crusher, and Keestrack. Companies operating in the V2X Digital Twin Analytics Market focus on platform innovation, ecosystem partnerships, and scalable deployment models to strengthen their competitive position. Many invest heavily in advanced analytics capabilities, artificial intelligence integration, and real-time simulation performance to enhance solution value. Strategic alliances with mobility stakeholders help accelerate adoption and expand application scope. Firms also prioritize cloud-native architectures and interoperability to support seamless integration with existing systems. Continuous enhancement of cybersecurity, compliance readiness, and data governance strengthens customer trust.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicle

- 2.2.4 Application

- 2.2.5 Deployment Mode

- 2.2.6 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid growth of connected and autonomous vehicles

- 3.2.1.2 Smart city and intelligent transportation initiatives

- 3.2.1.3 Advanced AI/ML and edge-to-cloud analytics

- 3.2.1.4 Regulatory pressure on safety and emissions

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation costs

- 3.2.2.2 Data privacy, security, and interoperability issues

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in Asia-pacific and emerging markets

- 3.2.3.2 Integration with autonomous vehicle and fleet management system

- 3.2.3.3 Regulatory compliance and safety solutions

- 3.2.3.4 Fleet and logistics optimization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.: NHTSA & FCC Guidelines

- 3.4.1.2 Canada: Transport Canada & ISED Guidelines

- 3.4.2 Europe

- 3.4.2.1 Germany: Federal Ministry of Transport & Digital Infrastructure

- 3.4.2.2 France: Ministry for the Ecological Transition

- 3.4.2.3 UK: Department for Transport

- 3.4.2.4 Italy: Ministry of Infrastructure & Transport

- 3.4.3 Asia Pacific

- 3.4.3.1 China: Ministry of Industry and Information Technology

- 3.4.3.2 Japan: Ministry of Land, Infrastructure, Transport and Tourism

- 3.4.3.3 South Korea: Ministry of Land, Infrastructure and Transport

- 3.4.3.4 India: Ministry of Road Transport & Highways

- 3.4.4 Latin America

- 3.4.4.1 Brazil: National Transport Agency

- 3.4.4.2 Mexico: Secretariat of Communications and Transportation (SCT)

- 3.4.5 Middle East and Africa

- 3.4.5.1 UAE: Ministry of Industry and Advanced Technology

- 3.4.5.2 Saudi Arabia: Saudi Standards, Metrology and Quality Organization

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and Environmental Aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Use case scenarios

- 3.13 Data Architecture & Interoperability Frameworks

- 3.14 Cybersecurity, Data Governance & Functional Safety Implications

- 3.15 Deployment & Commercialization Models

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($ Bn)

- 5.1 Key trends

- 5.2 Software

- 5.2.1 Digital twin platforms

- 5.2.2 Simulation & modeling engines

- 5.2.3 Analytics & AI software

- 5.3 Hardware

- 5.3.1 Edge computing devices

- 5.3.2 Sensors & RSUs

- 5.3.3 On-board vehicle computing units

- 5.4 Services

- 5.4.1 Integration & deployment

- 5.4.2 Managed analytics services

- 5.4.3 Consulting & customization

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($ Bn)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchbacks

- 6.2.2 Sedans

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles (LCV)

- 6.3.2 Medium commercial vehicles (MCV)

- 6.3.3 Heavy commercial vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($ Bn)

- 7.1 Key trends

- 7.2 Traffic Management

- 7.3 Predictive Maintenance

- 7.4 Fleet Management

- 7.5 Safety & Security

- 7.6 Autonomous Driving

Chapter 8 Market Estimates & Forecast, By Deployment Mode, 2022 - 2035 ($ Bn)

- 8.1 Key trends

- 8.2 Cloud

- 8.3 On-Premises

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($ Bn)

- 9.1 Key trends

- 9.2 Automotive OEMs

- 9.3 Government & transportation authorities

- 9.4 Fleet Operators

- 9.5 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($ Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Belgium

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 Singapore

- 10.4.6 South Korea

- 10.4.7 Vietnam

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Global Player

- 11.1.1 ANSYS

- 11.1.2 Dassault Systemes

- 11.1.3 EZ Crusher

- 11.1.4 Hexagon

- 11.1.5 IBM

- 11.1.6 Keestrack

- 11.1.7 Microsoft

- 11.1.8 OverBuilt

- 11.1.9 PTC

- 11.1.10 Siemens

- 11.2 Regional Player

- 11.2.1 Al-Jon Manufacturing

- 11.2.2 Eagle Crusher Company

- 11.2.3 Fayat

- 11.2.4 Hammel Recyclingtechnik

- 11.2.5 Liebherr

- 11.2.6 McCloskey International

- 11.2.7 Metso Outotec

- 11.2.8 Sandvik

- 11.2.9 Sierra International Machinery

- 11.2.10 Terex

- 11.3 Emerging Players

- 11.3.1 BHS-Sonthofen

- 11.3.2 Komplet America

- 11.3.3 Mobile Crushers International

- 11.3.4 Rockster Recycler

- 11.3.5 Rubble Master

2026年全球数位双胞胎孪生即服务市场报告2026年全球数位双胞胎技术市场报告2026年全球物流数位双胞胎市场报告2026年全球人工智慧(AI)增强数位双胞胎品质指数市场报告2026年全球数位双胞胎市场报告

2026年全球数位双胞胎孪生即服务市场报告2026年全球数位双胞胎技术市场报告2026年全球物流数位双胞胎市场报告2026年全球人工智慧(AI)增强数位双胞胎品质指数市场报告2026年全球数位双胞胎市场报告 全机械化采矿作业的数位双胞胎系统市场:按组件、部署类型、应用和最终用户划分——2026-2032年全球预测

全机械化采矿作业的数位双胞胎系统市场:按组件、部署类型、应用和最终用户划分——2026-2032年全球预测 商用车及车队数位双胞胎市场:成长机会、成长要素、产业趋势分析及2026-2035年预测

商用车及车队数位双胞胎市场:成长机会、成长要素、产业趋势分析及2026-2035年预测 工业数位化技术展望:2026

工业数位化技术展望:2026 数位双胞胎市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、部署类型、最终用户、功能和解决方案划分

数位双胞胎市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、部署类型、最终用户、功能和解决方案划分 数位双胞胎(DT):市场占有率分析、产业趋势与统计、成长预测(2026-2031)

数位双胞胎(DT):市场占有率分析、产业趋势与统计、成长预测(2026-2031)