|

市场调查报告书

商品编码

1940606

壁纸:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Wallpaper - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

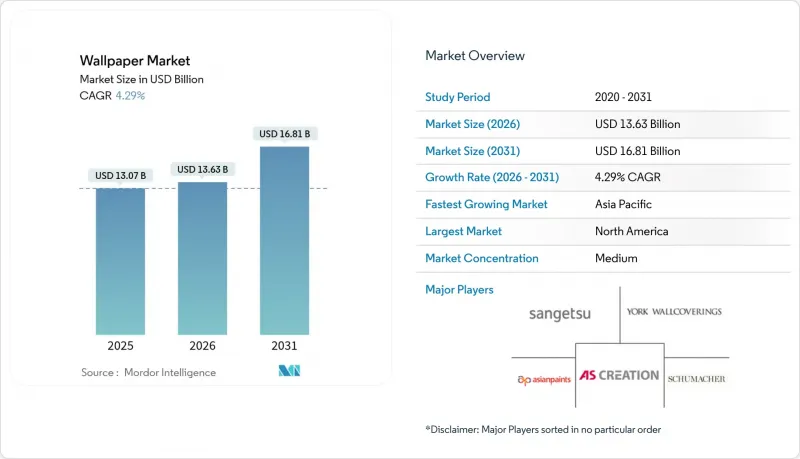

预计到 2026 年,壁纸市场价值将达到 136.3 亿美元,高于 2025 年的 130.7 亿美元。

预计到 2031 年将达到 168.1 亿美元,2026 年至 2031 年的复合年增长率为 4.29%。

需求成长主要受以下因素驱动:数位印刷技术、抗菌涂层和自黏基材的日益普及,以及住宅维修热潮、饭店翻新週期加快和中等收入消费者美学意识的提升。目前,商业应用占据主导地位,海湾合作委员会 (GCC) 地区和东盟 (ASEAN) 的饭店建筑计划持续指定使用能够承受高强度维护的高品质耐用壁材。随着东南亚国家津贴经济适用住宅项目,以及北美住宅倾向于选择独特的装饰而非定期重新粉刷,住宅应用正在加速成长。儘管PVC价格波动和关税上涨影响着供应链,但製造商正透过垂直整合、长期树脂合约以及非PVC基材的创新来保护利润率。如今,竞争优势主要体现在全通路分销、永续性以及客製印刷将设计概念快速转化为成品捲材的能力上。

全球壁纸市场趋势与洞察

北美和欧洲对采用数位印刷技术进行个人化装饰的需求激增。

按需数位印刷使设计师摆脱了製版和最低订购量的限制,能够实现连续图案、厚度达2毫米的3D纹理以及快速原型製作,从而缩短了从设计到施工的周期。 Roland DG和Panasonic房屋解决方案公司联合推出了DIMENSE技术,无需额外的压纹製作流程即可製作三维表面,拓展了创意空间并提高了成本效益。高端涂料製造商Benjamin Moore与Alpha 研讨会合作开发了一款手绘壁纸,售价为每码125美元,这表明客製化产品能够带来40%至60%的溢价。欧洲知名设计公司Sanderson Design Group也推出了融合传统与数位元素的新产品(每卷售价13,900日圆至35,100日圆),印证了富裕消费者愿意为独特的品牌故事买单。电子商务加速了数位转型:Graham & Brown 的 B2B 入口网站在短短 12 週内就实现了 90% 的客户采用率,有效降低了订购流程的繁琐和库存风险。这些成果提高了製造商的利润率,并使数位化工作流程成为住宅客製化和小规模商业计划的标准方法。

东南亚中等收入城市住宅快速成长

印尼2024年第一季的建设活动相当于GDP的10.23%,而越南在2025年上半年动工兴建了超过60万套社会住宅。这为兼具美观性和经济性的中价位壁材创造了长期需求曲线。印尼的「百万住宅计画」等政府计画以及卡达支持的融资管道正在提升首次住宅者的购买力,鼓励他们选择品牌化且成本绩效合理的装饰材料。亚洲开发银行预测,2025年区域GDP成长率将达到4.5%,这将支持有选择的装修支出。国际生产商正在区域内设立工厂以规避关税并缩短前置作业时间,而本土品牌则在利用进口替代激励措施。千禧世代的线上购物习惯正在推动数位化客製化平台的发展,进一步刺激了对数位印刷产品的需求。

市面上有许多替代品可供选择

儘管涂料、装饰面板和数位显示器的价值提案不断提升,但在易于维护和互动内容至关重要的领域,壁纸份额却逐渐萎缩。剪切机司的PaintShield涂料直接将抗菌性能融入其中,可在两小时内杀死99.9%的细菌,从而占据了以往用于特殊墙壁材料的预算。纹理涂料、墙贴和植物墙满足了亲生物设计的要求,而模组化面板系统则使得办公空间能够在一夜之间重新配置。这些多样化的选择迫使壁纸製造商更加重视触感深度、材料循环利用和安装效率。

细分市场分析

预计到2026年,不织布产品将以5.88%的复合年增长率推动市场成长,其成长速度将超过壁纸市场整体成长,这主要得益于其透气性和尺寸稳定性,简化了施工和移除流程。高阶安装商青睐此类产品,因为其干式释放特性可减少高达30%的人力成本。乙烯基壁纸预计到2025年将保持32.03%的市场份额,这得益于其医用级的耐用性和成本竞争力。然而,日益严格的环保法规正在推动对生物基PVC、再生PET和无溶剂油墨的需求。纸基产品线正在萎缩,主要保留在註重真实性而非易于维护性的传统住宅中。织物表面触感温暖,并具有内建吸音功能,常用于高端小众空间。博拉斯特佩塔(Borastapeta)位于维亚莱德(Vialed)的工厂展现了其技术上的多样性,将表面印刷、凹版印刷、丝网印刷和数位印刷机整合于同一屋檐下,从而能够根据每种材料的印刷特性进行客製化生产。

不织布产业的蓬勃发展与永续性法规相辅相成,推动市场转向FSC认证纤维和水性黏合剂。该行业的敏捷性使得抗菌化学处理和剥离式黏合剂得以迅速应用,其应用范围也从出租公寓扩展到小儿科诊所。乙烯基创新者正透过不含邻苯二甲酸酯的配方和节能压花技术来捍卫其市场份额。金属箔和玻璃纤维增强片材等新兴复合复合材料则瞄准了需要阻燃和电磁屏蔽等性能的细分市场。

到2025年,数位科技将占壁纸产量的58.12%,并以每年7.15%的速度持续成长,将壁纸市场转变为订单客製化的模式。喷墨印表机头与UV固化化学技术的结合,可在各种基材上达到即时固化和鲜艳色彩,而乳胶系统则符合低VOC排放标准。Canon指出,数位技术无需製版,即可实现从单卷定製到中型酒店订单的生产,且无需增加设置成本。网版印刷在油墨沉积丰富和特殊效果方面仍保持领先地位,尤其是在传统锦缎图案方面。柔版印刷在大尺寸商业印刷领域也占有一席之地,其精确的重复性使得滚筒投资物有所值。混合生产线正在兴起,在传统工艺之前整合单一途径数位单元,从而可以在批量印刷的底布上迭加定製图案。

快速打样流程和人工智慧色彩匹配软体将从概念到上市的时间从数月缩短至数天,使设计师能够即时响应潮流趋势。成本优势不仅限于库存管理,数位化小批量生产能力还能降低营运资金,减少报废库存的损失;同时,高效率的UV- LED灯降低了能源成本,帮助印刷企业实现碳中和目标。 Octink 50年的发展历程表明,传统印刷厂可以在不损害其传统印刷工艺的前提下,成功转型数位化。

区域分析

北美地区在2024年引领了出货量成长,这得益于其成熟的维修文化和对数位印刷工作流程的早期应用。美国自黏墙纸市场的蓬勃发展,得益于灵活的零售模式,即使原料成本波动,也支撑了预期需求。加拿大建材市场预计2026年将成长4.5%至5.5%,公共工程计划也成为其目标市场之一。墨西哥正在崛起为近岸外包中心,为寻求降低亚洲运输成本波动的美国高端品牌提供成本效益高的生产方案。约克墙纸公司收购了一家独立的表面印刷企业,巩固了其区域领先地位并强化了其本地供应链。

欧洲的设计传统和严格的环保法规维持其产品的高溢价。德国和义大利正在强制推行无溶剂印刷,加速水性油墨的普及。英国室内装潢产业正经历一场手工技艺的復兴,桑德森(Sanderson)以羊毛为灵感的「奥威尔编织」(Orwell Weave)系列和新款「乡村森林」(Country Woodland)系列产品便是例证。西班牙等南欧市场正专注于开发抗紫外线的外墙覆层,以完善旅馆业的露台空间。东欧的需求随汇率波动而波动,但波兰和捷克共和国的维修补贴政策正在缓解销售下滑。循环经济指南正推动製造商试点「从摇篮到摇篮」的基材认证和回收计画。

亚太地区销售成长最快。印尼计划每年供应300万套住宅,越南的社会住宅目标预计将增加数十万套。中国国内需求与出口生产同步成长,维持大规模生产线,从而发挥了规模经济效益。印度主要装饰涂料製造商亚洲涂料公司利用其全通路布局,在服务业推广壁纸套装的交叉销售。高性能产品在日本和韩国等成熟市场更受欢迎。三月公司的再生PET玻璃薄膜符合低碳建筑标准,同时提供紫外线和隔热保护。澳洲在易发山火地区推广使用阻燃墙面织物,正在扩大此一功能性细分市场。该地区计划在2025年第一季启动2074个酒店计划,确保了合约量的持续成长。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 北美和欧洲对个人化数位印刷的需求激增

- 东南亚中等收入家庭城市住宅快速成长

- 酒店业更新周期推动海湾合作委员会和东协地区豪华商业壁纸的发展

- 美国零售视觉商品行销转向自黏乙烯基材料

- 医疗设施维修采用抗菌壁纸

- 市场限制

- 市面上有许多替代品可供选择

- 氯乙烯价格波动导致利润率下降

- 在高温高湿环境下使用寿命缩短

- 供应链分析

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 壁纸类型

- 乙烯基塑料

- 不织布

- 纸本

- 织物(丝绸、亚麻布等)

- 其他壁纸类型

- 透过印刷技术

- 数位(喷墨/EP)

- 萤幕

- 柔版印刷

- 其他印刷技术

- 最终用户

- 住宅

- 商业

- -饭店业

- 企业办公空间

- -美容美髮沙龙和水疗中心

- - 医院

- 其他最终用户

- 透过分销管道

- 直销

- 间接销售

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲和纽西兰

- 亚太其他地区

- 中东和非洲

- 中东

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 埃及

- 其他非洲地区

- 中东

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Sangetsu Corporation

- York Wall Coverings Inc.

- AS Creation Tapeten AG

- Brewster Home Fashion LLC

- Grandeco Wallfashion Group

- Erismann & Cie. GmbH

- Sanderson Design Group PLC

- Tapetenfabrik Gebr. Rasch GmbH & Co. KG

- Marshalls Wallcoverings

- Asian Paints Ltd(Nilaya)

- Eximus Wallpaper

- Gratex Industries Ltd

- Graham & Brown Ltd

- Wallquest Inc.

- Adornis Wallpapers

- Arte International

- 4walls

- Omexco NV

- Life n Colors Private Limited

- Komar Products GmbH

- Houfling GmbH(Hohenberger)

第七章 市场机会与未来展望

Wallpaper market size in 2026 is estimated at USD 13.63 billion, growing from 2025 value of USD 13.07 billion with 2031 projections showing USD 16.81 billion, growing at 4.29% CAGR over 2026-2031.

Demand expands as digital printing, antimicrobial coatings, and peel-and-stick substrates converge with surging residential renovation activity, intensified hospitality refresh cycles, and rising interior-aesthetic expectations among mid-income households. Commercial installations currently lead because hotel construction pipelines in the GCC and ASEAN continue to specify premium, durable wallcoverings that withstand rigorous maintenance schedules. Residential adoption accelerates as Southeast Asian governments subsidize affordable housing programs and North American homeowners opt for personalized decor over routine repainting. Supply chains face vinyl-chloride price swings and tariff hikes, yet manufacturers defend margins through vertical integration, long-term resin contracts, and innovation in non-vinyl substrates. Competitive differentiation now hinges on omnichannel distribution, sustainability credentials, and the speed with which on-demand printing can translate design concepts into finished rolls.

Global Wallpaper Market Trends and Insights

Surge in Demand for Digitally-Printed Personalised Decor in North America and Europe

On-demand digital printing liberates designers from plate-making and minimum-run constraints, enabling serialized patterns, tactile 3D textures up to 2 mm, and fast prototyping that shortens design-to-installation cycles. Roland DG and Panasonic Housing Solutions unveiled DIMENSE technology that produces sculpted surfaces without extra embossing passes, widening creative scope and cost efficiency. Luxury paint maker Benjamin Moore collaborated with The Alpha Workshops to hand-paint wallpapers retailing at USD 125 per yard, proof that customization supports 40-60% price premiums. European stalwarts such as Sanderson Design Group chase this segment with heritage-meets-digital launches that sell for ¥13,900-¥35,100 per roll, validating affluent willingness to pay for unique stories Sanderson. Ecommerce accelerates uptake: Graham & Brown's B2B portal reached 90% client adoption in just 12 weeks, cutting order friction and inventory risk. These gains lift manufacturer margins and position digital workflows as the default mode for bespoke residential and boutique commercial projects.

Rapid Mid-Income Urban Housing Boom in Southeast Asia

Indonesia reported construction representing 10.23% of GDP in Q1 2024 while Vietnam initiated over 600,000 social housing units during H1 2025, setting a long-tail demand curve for mid-priced wallcoverings that balance aesthetics with affordability. Government programs such as Indonesia's One Million House plan and Qatar-backed financing channels lift first-time buyers' purchasing power, steering them toward branded yet cost-effective decor choices. Asian Development Bank forecasts 4.5% regional GDP growth for 2025, underpinning discretionary renovation spending. International producers answer with regional plants that dodge tariffs and shorten lead times, while local brands exploit import substitution incentives. Millennials' online buying habits drive traffic to digital customization platforms, further intensifying the pull on digitally printed offerings.

Easy Availability of Substitutes in the Market

Paints, decorative panels, and digital displays constantly upgrade value propositions, eroding wallpaper's share where maintenance simplicity or interactive content holds sway. Sherwin-Williams Paint Shield introduces microbicidal functions directly into paint, killing 99.9% of bacteria in 2 hours and capturing budgets once reserved for specialty wallcoverings. Textured paints, wall decals, and living-plant walls fulfil biophilic design briefs, while modular panel systems allow offices to reconfigure spaces overnight. The broadening substitute set compels wallpaper producers to stress tactile depth, material circularity, and installation efficiency.

Other drivers and restraints analyzed in the detailed report include:

- Hospitality Refresh Cycles Driving Premium Commercial Wallpaper in GCC and ASEAN

- Retail Visual-Merchandising Shift to Peel-and-Stick Vinyl in the U.S.

- Vinyl-Chloride Price Volatility Compressing Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Non-woven products opened 2026 with a 5.88% CAGR outlook, eclipsing overall wallpaper market growth as breathable, dimensionally stable substrates simplify installation and removal tasks. Premium installers champion the category because dry-strippable properties cut labour by up to 30%. Vinyl retained 32.03% wallpaper market share in 2025 thanks to hospital-grade durability and cost competitiveness, yet environmental scrutiny intensifies calls for bio-PVC, recycled PET, and solvent-free inks. Paper-based lines contract, surviving mostly in heritage residences where authenticity tops maintenance ease. Fabric surface coverings serve niche luxury spaces, offering tactile warmth and built-in acoustic dampening. Borastapeter's Viared facility illustrates technical diversity, running surface, gravure, screen, and digital presses under one roof to match each material's printability.

Non-woven momentum intersects sustainability regulation, prompting marketing pivots toward FSC-certified fibres and water-based adhesives. The segment's agility allows quick adoption of antimicrobial chemistries or peel-and-stick adhesives, widening end-use scope from rental apartments to pediatric clinics. Vinyl innovators respond with phthalate-free formulations and energy-saving emboss cures to defend share. Emerging composites such as metallic foils or glass fibre reinforced sheets target functional niches demanding fire retardancy or electromagnetic shielding.

Digital technologies captured 58.12% of production in 2025 and are adding 7.15% annually, transforming the wallpaper market into a make-to-order paradigm. Inkjet heads paired with UV-curable chemistries deliver immediate curing and vibrant colour saturation on diverse substrates, while latex systems comply with low-VOC codes. Canon's guidance confirms that digital eliminates plates, enabling batch sizes from a single customised roll to mid-volume hospitality orders without setup penalties. Screen printing retains pockets where rich ink laydown and special effects are still unrivalled, particularly for heritage damasks. Flexography holds ground in long-run commercial corridors where precision repeatability justifies cylinder investments. Hybrid lines emerge, integrating single-pass digital units ahead of conventional stations so bespoke motifs overlay mass-printed bases.

Rapid proofing loops and AI colour-matching software compress concept-to-market timelines from months to days, letting designers react to viral trends. Cost advantages extend beyond inventory: digital short-run capabilities reduce working capital and shrink obsolete stock write-offs. Meanwhile, UV-LED lamp efficiencies drop energy bills, helping printers meet carbon-neutral targets. Octink's 50-year trajectory shows legacy shops can retrofit for digital without surrendering printcraft heritage.

The Wallpaper Market Report is Segmented by Wallpaper Type (Vinyl, Non-Woven, Paper-Based, Fabric, Other), Printing Technology (Digital, Screen, Flexographic, Other), End User (Residential, Commercial), Distribution Channel (Direct Sales, Indirect Sales), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led 2024 shipments on the back of established renovation culture and early adoption of digital-print workflows. The U.S. peel-and-stick craze, fuelled by flexible retail concepts, bolsters forecast demand despite raw-material cost swings. Canada's construction-materials market expects 4.5-5.5% growth through 2026, adding institutional projects to the addressable base. Mexico emerges as a near-shoring hub, providing cost-efficient production for premium U.S. brands looking to mitigate Asian freight volatility. York Wallcoverings consolidates regional leadership after acquiring independent surface-print operations, strengthening local supply chains.

Europe preserves a strong pricing premium through design heritage and stringent eco-regulation. Germany and Italy push solvent-free print mandates, prompting accelerated adoption of water-based inks. United Kingdom interiors celebrate artisanal revival, evident in Sanderson's wool-inspired Orwell Weaves and Country Woodland launches. Southern markets such as Spain emphasise UV-stable outdoor wall applications to complement hospitality terraces. Eastern Europe's demand fluctuates with currency swings, though renovation subsidies in Poland and Czechia cushion volume declines. Circular-economy directives drive producers to certify cradle-to-cradle substrates and pilot take-back schemes.

Asia-Pacific records the steepest volume climb; Indonesia plans to deliver three million homes yearly while Vietnam's social housing targets add hundreds of thousands of units. China's domestic appetite strengthens alongside export output, sustaining mega-scale lines that benefit from economies of scope. India's decorative coatings leader Asian Paints leverages omnichannel reach to cross-sell wallpaper bundles under its services arm. Mature markets Japan and South Korea favour high-function products: Sangetsu's recycled-PET glass films meet low-carbon building codes while offering UV heat-shielding. Australia pivots to fire-retardant wall fabrics for bushfire-vulnerable regions, enriching the functional niche. Collectively, the region's 2,074-project hospitality pipeline through Q1 2025 guarantees sustained contract volumes.

- Sangetsu Corporation

- York Wall Coverings Inc.

- A.S. Creation Tapeten AG

- Brewster Home Fashion LLC

- Grandeco Wallfashion Group

- Erismann & Cie. GmbH

- Sanderson Design Group PLC

- Tapetenfabrik Gebr. Rasch GmbH & Co. KG

- Marshalls Wallcoverings

- Asian Paints Ltd (Nilaya)

- Eximus Wallpaper

- Gratex Industries Ltd

- Graham & Brown Ltd

- Wallquest Inc.

- Adornis Wallpapers

- Arte International

- 4walls

- Omexco NV

- Life n Colors Private Limited

- Komar Products GmbH

- Houfling GmbH (Hohenberger)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Demand for Digitally-Printed Personalised Decor in North America and Europe

- 4.2.2 Rapid Mid-Income Urban Housing Boom in Southeast Asia

- 4.2.3 Hospitality Refresh Cycles Driving Premium Commercial Wallpaper in GCC and ASEAN

- 4.2.4 Retail Visual-Merchandising Shift to Peel-and-Stick Vinyl in the U.S.

- 4.2.5 Adoption of Antimicrobial Coated Wallcoverings in Healthcare Renovations

- 4.3 Market Restraints

- 4.3.1 Easy Availability of Substitues in the Market

- 4.3.2 Vinyl-Chloride Price Volatility Compressing Margins

- 4.3.3 Shorter Life-span on Exposure to Heat and Moisture

- 4.4 Supply-Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Wallpaper Type

- 5.1.1 Vinyl

- 5.1.2 Non-woven

- 5.1.3 Paper-based

- 5.1.4 Fabric (Silk, Linen, etc.)

- 5.1.5 Other wallapaper Type

- 5.2 By Printing Technology

- 5.2.1 Digital (Inkjet/EP)

- 5.2.2 Screen

- 5.2.3 Flexographic

- 5.2.4 Other Printing Technology

- 5.3 By End User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 -Hospitality

- 5.3.4 - Corporate Office Space

- 5.3.5 -Salons and Spas

- 5.3.6 - Hospitals

- 5.3.7 -Other End User

- 5.4 By Distribution Channel

- 5.4.1 Direct Sales

- 5.4.2 Indirect Sales

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 United Arab Emirates

- 5.5.4.1.2 Saudi Arabia

- 5.5.4.1.3 Turkey

- 5.5.4.1.4 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Nigeria

- 5.5.4.2.3 Egypt

- 5.5.4.2.4 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Sangetsu Corporation

- 6.4.2 York Wall Coverings Inc.

- 6.4.3 A.S. Creation Tapeten AG

- 6.4.4 Brewster Home Fashion LLC

- 6.4.5 Grandeco Wallfashion Group

- 6.4.6 Erismann & Cie. GmbH

- 6.4.7 Sanderson Design Group PLC

- 6.4.8 Tapetenfabrik Gebr. Rasch GmbH & Co. KG

- 6.4.9 Marshalls Wallcoverings

- 6.4.10 Asian Paints Ltd (Nilaya)

- 6.4.11 Eximus Wallpaper

- 6.4.12 Gratex Industries Ltd

- 6.4.13 Graham & Brown Ltd

- 6.4.14 Wallquest Inc.

- 6.4.15 Adornis Wallpapers

- 6.4.16 Arte International

- 6.4.17 4walls

- 6.4.18 Omexco NV

- 6.4.19 Life n Colors Private Limited

- 6.4.20 Komar Products GmbH

- 6.4.21 Houfling GmbH (Hohenberger)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026-2034年全球壁纸市场规模、份额、趋势和成长分析报告

2026-2034年全球壁纸市场规模、份额、趋势和成长分析报告 日本壁纸市场规模、份额、趋势及预测(按壁纸类型、通路、最终用户和地区划分),2026-2034年

日本壁纸市场规模、份额、趋势及预测(按壁纸类型、通路、最终用户和地区划分),2026-2034年 壁纸市场 - 全球产业规模、份额、趋势、机会及预测(按产品类型、最终用途、分销管道、地区和竞争格局划分,2021-2031年)

壁纸市场 - 全球产业规模、份额、趋势、机会及预测(按产品类型、最终用途、分销管道、地区和竞争格局划分,2021-2031年) 数位印刷壁纸市场规模、份额及成长分析(按基材、印刷技术、最终用户和地区划分)-2026-2033年产业预测

数位印刷壁纸市场规模、份额及成长分析(按基材、印刷技术、最终用户和地区划分)-2026-2033年产业预测 2021-2031年亚太地区壁纸市场报告:范围、细分、动态和竞争分析

2021-2031年亚太地区壁纸市场报告:范围、细分、动态和竞争分析 全球壁纸市场

全球壁纸市场 壁纸市场规模、份额、趋势分析报告:按产品、最终用途、地区、细分市场预测,2025-2030 年

壁纸市场规模、份额、趋势分析报告:按产品、最终用途、地区、细分市场预测,2025-2030 年 壁纸市场报告:趋势、预测和竞争分析(至 2031 年)

壁纸市场报告:趋势、预测和竞争分析(至 2031 年) 印度壁纸:市场占有率分析、产业趋势与统计、成长预测(2025-2030)

印度壁纸:市场占有率分析、产业趋势与统计、成长预测(2025-2030) 壁纸市场按产品类型、应用、分销管道和地区划分

壁纸市场按产品类型、应用、分销管道和地区划分