|

市场调查报告书

商品编码

1940609

棒状包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Stick Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

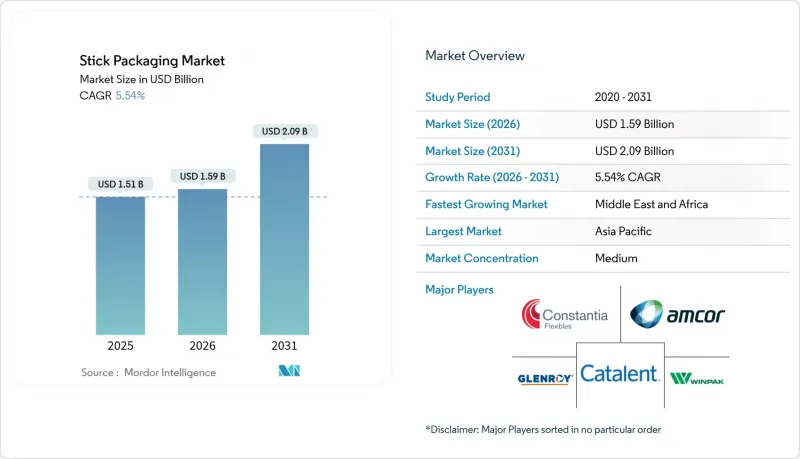

2025年,棒状包装市场价值为15.1亿美元,预计到2031年将达到20.9亿美元,高于2026年的15.9亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 5.54%。

这一前景得益于消费者对便捷单份包装日益增长的需求、减少塑胶废弃物的监管压力不断加大,以及柔软性薄膜阻隔性能的持续提升。製造商正投资数位印刷机以满足小批量个人化订单的需求,品牌所有者也优先考虑份量控制的优势,以顺应健康意识的趋势。树脂价格的波动和铝关税的影响提升了轻质复合材料的相对吸引力。同时,为满足电商物流效率目标,供应商正致力于开发能够优化体积运输成本的窄型紧凑包装。主要加工商之间的整合加剧了其采购能力,加速了可回收单一材料结构的规模化生产。

全球棒状包装市场趋势与洞察

便利性和行动消费的蓬勃发展

城市生活方式的兴起和女性劳动参与率的提高,使得便携性成为重要的购买考量因素,促使消费者选择单份包装。品牌商表示,以可放入口袋或健身包的纤薄小袋包装销售粉状饮料、即溶咖啡和电解质饮料时,家庭用户接受度显着提升。速食连锁店正将此概念延伸至调味品领域,从笨重的包装袋转向细长的条状容器,从而减少高达35%的包装材料。同时,电商食品平台也青睐条状包装的长方形形状,可以最大限度地减少包装空隙,并降低配送成本。便利性和配送效率的良性循环,为条状包装市场带来了长期的良好需求。

对材料和重量减少的需求

原料成本上涨正促使人们更加重视薄壁复合材料的应用。预计到2025年初,瓦楞纸板价格将上涨70美元/吨,而美国对铝箔征收25%的进口关税,进一步拉大了硬质和软质基材之间的成本差距。与枕形袋相比,条状包装通常每克产品可节省30-40%的薄膜用量,有助于品牌商减轻树脂价格波动的影响。供应商正抓住这一机会,推出更薄的密封层(不会影响加工性能)和更高产量比率的聚乙烯基阻隔材料。这些变化共同增强了条状包装市场在通膨环境下的竞争力。

加强对一次性塑胶製品的监管

对某些一次性产品的禁令以及对再生树脂含量低于30%的包装课税,增加了多层复合材料的合规成本。在英国,不合规包装最高可被处以每吨200英镑的罚款,这促使供应商要求提供经认证的再生树脂含量证明。由于条状包装的材料用量低且薄膜宽度窄,再生树脂的整合面临挑战,即使是微小的缺陷也会影响生产线速度。加工商必须加快物料平衡认证树脂的合格,以确保提高产量。

细分市场分析

到2025年,塑胶产品板块将占总收入的63.42%,这主要得益于成本效益高的PE和PET结构,这些结构具有成熟的加工窗口。对薄壁共压製产品和基于EVOH的氧气阻隔材料的需求,帮助该板块即使在监管审查下也保持了市场份额。然而,生质塑胶预计将以10.24%的复合年增长率成长,这是所有材料板块中最高的成长率。弗劳恩霍夫研究所等生产商已经展示了80%生物基PLA共混物,其柔软性与LDPE相当,突破了性能上的重大瓶颈。纸箔混合材料目前仍处于小众市场,但由于其保质期短,调味品领域的需求正在成长。

从价值角度来看,传统基材至少在2028年之前仍将主导棒状包装市场规模,但随着可追溯成分认证的实施,生物基薄膜将成为成长的主要来源,这将释放企业在环境、社会和治理(ESG)方面的采购预算。领先的跨国饮料品牌正在就生物基聚乙烯(bio-PE)的多年采购协议进行谈判,以确保在监管截止日期前获得供应。同时,由于关税政策的影响,金属箔的成本不断上涨,预计其应用范围将仅限于需要99%或更高遮光率的高阻隔阻隔性药品棒状包装。最终的结果将是一个渐进的重新平衡过程,而非突如其来的变革。

到2025年,粉状产品将占棒状包装市场57.35%的份额,这反映了其在即溶咖啡、膳食补充剂和运动营养混合物等领域的广泛应用。粉末状产品的高流动性使其能够快速填充并实现可靠的密封性能,从而带来优异的单位经济效益。然而,由于采用具有更佳黏度控制的连续运动垂直灌装封口(VFFS)平台,液体产品的复合年增长率预计将达到8.92%。正如Futamura公司利用水溶性薄膜製成的可堆肥小袋所展示的那样,性能差距正在缩小,液体棒状产品在旅行个人护理套装中也变得越来越常见。

机能饮料品牌非常重视液体棒提供的10毫升至15毫升的精准分装量,方便消费者根据需要取用胶原蛋白蛋白或电解质补充剂。在物流方面,液体棒包装采用平板车运输,而非笨重的宝特瓶,显着降低了运输成本和碳排放。随着机械製造商不断改进防滴漏喷嘴设计,预计到2031年,液体棒包装市场规模将达到6.73亿美元,虽然在绝对规模上落后于粉末包装,但其相对增长率却超过了粉末包装。由于对剪切力的要求较高且缺乏自动化选项,颗粒状和半固体填充物的增长速度预计将较为缓慢。

区域分析

预计到2025年,亚太地区将占据35.44%的收入份额,其中中国和印度不断壮大的中阶将推动对分量控制饮料和营养补充剂的需求。都市区消费者更青睐小袋装多包装产品,这种包装便于收纳于空间有限的厨房,并能与基于应用程式的生鲜配送服务无缝衔接。本土品牌商正受益于垂直整合的薄膜挤出丛集,这些集群能够缩短前置作业时间并降低最低订购量。同时,政府鼓励采用生物基聚合物的政策也开始影响材料的选择,推动了甘蔗衍生聚乙烯的早期试验。

北美是第二大区域贡献者,这得益于其高端定位以及在医药和营养保健品应用领域不断增长的渗透率。美国拥有众多机械设备原始设备製造商 (OEM) 和合约包装公司,形成了一个良性循环的生态系统,加速了新产品 (SKU) 的市场上市。然而,不断上涨的运输成本和波动的树脂价格带来了不利影响,迫使一些产能扩张计画转移到墨西哥等邻近地区。

欧洲一直是永续性的标竿。即将推出的包装和包装废弃物法规迫使加工商重新设计复合材料结构以提高其可回收性,该地区也因此成为单一材料PE/EVOH共混物的技术试验场。中东和非洲地区虽然绝对规模仍小规模,但其复合年增长率高达6.66%。可支配收入的成长和餐饮服务业的快速发展推动了单份咖啡、果汁和香辛料包装产品的应用,同时,区域各国政府正积极吸引外国直接投资(FDI)进入软包装製造业,以摆脱对石化行业的依赖。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 便利性和行动消费的蓬勃发展

- 对材料和重量减少的需求

- 软包装的永续性要求

- 药物微剂量和儿童剂型

- 用于大量客製化包装袋的数位印刷

- 电子商务中样品包的普遍性

- 市场限制

- 加强对一次性塑胶製品的监管

- 多层薄膜的可回收性局限性

- 阻隔级单材料薄膜短缺

- 高黏度灌装精度极限 > 15 道

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 激烈的竞争

- 关键绩效指标(KPI)

第五章 市场规模与成长预测

- 材料

- 塑胶

- 纸

- 金属箔

- 生质塑胶

- 按产品形式

- 粉末

- 颗粒

- 液体

- 半固体

- 按最终用户行业划分

- 食品/饮料

- 即溶饮料

- 膳食补充剂粉

- 糖和甜味剂

- 製药

- OTC

- Rx

- 化妆品和个人护理

- 工业和家用

- 食品/饮料

- 按包装器材通道数

- 1至3号车道

- 第4至10号车道

- 第11至20泳道

- 20条或更多车道

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 中东

- 以色列

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Amcor plc

- Constantia Flexibles Group GmbH

- Glenroy, Inc.

- Aranow Packaging Machinery SL

- Fres-Co System USA, Inc.

- Catalent, Inc.

- Winpak Ltd.

- Sonoco Products Company

- ePac Holdings, LLC

- GFR Pharma Ltd.

- Sonic Packaging Industries, Inc.

- Viking Masek Global Packaging Technologies sro

- Nichrome India Ltd.

- Unither Pharmaceuticals SAS

- Marchesini Group SpA

第七章 市场机会与未来展望

The stick packaging market was valued at USD 1.51 billion in 2025 and estimated to grow from USD 1.59 billion in 2026 to reach USD 2.09 billion by 2031, at a CAGR of 5.54% during the forecast period (2026-2031).

Growing demand for convenient single-serve formats, mounting regulatory pressure to curb plastic waste, and continuous improvements in flexible-film barrier performance underpin this outlook. Producers are investing in digital presses to serve personalized short-run orders, while brand owners lean on portion-control benefits to align with wellness trends. Resin price volatility and aluminum tariffs are increasing the relative attractiveness of lightweight laminates. At the same time, the need to meet e-commerce fulfilment efficiency targets is pushing suppliers to favor narrow, compact packs that optimize volumetric shipping costs. Consolidation among top converters is boosting purchasing leverage and accelerating the scale-up of recyclable mono-material structures.

Global Stick Packaging Market Trends and Insights

Convenience & On-the-Go Consumption Boom

City-centric lifestyles and rising female workforce participation have made portability a prime purchase criterion, steering consumers toward single-dose packs. Brand owners report higher household penetration when powder beverages, instant coffee, or electrolyte mixes are sold in slim sachets that fit pockets and gym bags. Quick-service chains are extending this logic to condiments, replacing bulky pouches with narrow sticks that reduce pack material by as much as 35%. In parallel, e-commerce grocery platforms value the rectangular footprint of stick packs because it minimizes void space and shipping fees. The self-reinforcing cycle between lifestyle convenience and channel efficiency places the stick packaging market in a favorable long-run demand position.

Demand for Material & Weight Reduction

Input-cost inflation is sharpening the focus on downgauged laminates. Corrugated board prices rose USD 70 per ton in early 2025, and aluminum foil attracts 25% import tariffs in the United States, widening the cost delta between rigid and flexible substrates. Stick formats typically consume 30-40% less film area per gram of product than pillow pouches, allowing brand owners to limit exposure to resin price swings. Suppliers are capitalizing by introducing thinner sealant layers and higher-yield PE-based barriers that do not compromise machinability. Together, these shifts are reinforcing the stick packaging market's competitiveness in inflationary environments.

Single-Use-Plastic Regulation Tightening

Bans on certain single-use articles and taxes on packaging containing less than 30% recycled resin are raising compliance costs for multi-layer laminates. Financial penalties in the United Kingdom can reach GBP 200 per ton for non-conforming packs, prompting retailers to pressure suppliers for verified PCR content. Although stick formats use less material, their narrow gauge complicates PCR incorporation because small film defects can impair line speeds. Converters must therefore accelerate the qualification of mass-balance certified resins to safeguard volume growth.

Other drivers and restraints analyzed in the detailed report include:

- Sustainability Mandates for Flexible Packs

- Pharma Micro-Dosing & Pediatric Formats

- Limited Recyclability of Multi-Layer Films

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The plastics family accounted for 63.42% of 2025 revenue, underpinned by cost-effective PE and PET structures that offer well-established processing windows. Demand for downgauged coextrusions and EVOH-based oxygen barriers helped the segment preserve share despite regulatory scrutiny. However, bioplastics are projecting a 10.24% CAGR, the fastest across the material spectrum. Producers such as Fraunhofer Institute have demonstrated PLA blends with 80% bio-based content that replicate LDPE flexibility, clearing a significant performance hurdle. Paper-foil hybrids remain niche but are gaining traction in condiment channels that tolerate shorter shelf life.

In value terms, traditional substrates will continue to dominate the stick packaging market size until at least 2028, yet the incremental gains will concentrate in bio-based films as traceable feedstock certification unlocks ESG procurement budgets. Early movers among multinational beverage brands are negotiating multi-year offtake contracts for bio-PE to secure volumes ahead of regulatory deadlines. Meanwhile, metal foils face cost inflation from tariff regimes, limiting their use to high-barrier pharmaceutical sticks that demand >99% light protection. The net result is a gradual rebalancing rather than a sudden disruption.

Powder applications retained 57.35% of the stick packaging market in 2025, reflecting entrenched usage in instant coffee, dietary supplements, and sports nutrition mixes. Their free-flowing nature enables high-speed filling and reliable seal integrity, supporting attractive unit economics. That said, liquids are on track for a brisk 8.92% CAGR, supported by continuous-motion vertical form-fill-seal (VFFS) platforms equipped with improved viscosity control. Futamura's demonstration of compostable film for aqueous sachets illustrates how performance gaps are narrowing, making liquid sticks a more common sight in personal-care travel kits.

Functional beverage brands value the precise 10 ml to 15 ml dose that liquid sticks deliver, enabling consumers to mix collagen shots or electrolyte boosters on demand. From a logistics standpoint, packs ship as flat carts rather than bulky PET bottles, slashing freight costs and carbon intensity. As machinery OEMs refine nozzle design to prevent drips, the stick packaging market size for liquids is expected to reach USD 673 million by 2031, outpacing powders in relative expansion though not absolute scale. Granular and semi-solid fillings will grow more moderately, held back by higher shearing requirements and fewer automated equipment options.

The Stick Packaging Market Report is Segmented by Material (Plastics, Paper, Metal Foils, Bioplastics), Product Form (Powders, Granules, Liquids, Semi-Solids), End-User Industry (Food & Beverages, Pharmaceuticals, Cosmetics & Personal Care, Industrial & Household), Packaging-Machinery Lane Count (1-3 Lanes, 4-10 Lanes, 11-20 Lanes, Greater Than 20 Lanes), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded a 35.44% revenue share in 2025, anchored by China's and India's expanding middle-class appetites for portion-controlled beverages and nutraceuticals. Urban consumers gravitate toward sachet multipacks that fit small kitchens and integrate seamlessly with app-based grocery delivery. Local brand owners benefit from vertically integrated film extrusion clusters, which shorten lead times and lower minimum order quantities. Meanwhile, government initiatives that encourage bio-based polymer adoption are beginning to influence material selection, fostering early experimentation with sugarcane-sourced PE.

North America ranks as the second-largest regional contributor, supported by premium positioning and greater penetration of pharmaceutical and nutraceutical applications. The United States also hosts a deep roster of machinery OEMs and contract packers, reinforcing a virtuous ecosystem that accelerates time-to-market for new SKUs. However, elevated freight costs and resin volatility create headwinds, pushing some capacity expansion plans toward nearshore sites in Mexico.

Europe remains the rule-setter on sustainability. The forthcoming Packaging and Packaging Waste Regulation is compelling converters to redesign laminate structures for recyclability, making the region a technology test bed for mono-material PE/EVOH blends. Middle East & Africa, while still small in absolute dollars, is on pace for a 6.66% CAGR. Rising disposable incomes and rapid food-service expansion support single-serve coffee, juice, and spice applications, while regional governments court FDI into flexible-pack manufacturing to diversify away from hydrocarbons.

- Amcor plc

- Constantia Flexibles Group GmbH

- Glenroy, Inc.

- Aranow Packaging Machinery S.L.

- Fres-Co System USA, Inc.

- Catalent, Inc.

- Winpak Ltd.

- Sonoco Products Company

- ePac Holdings, LLC

- GFR Pharma Ltd.

- Sonic Packaging Industries, Inc.

- Viking Masek Global Packaging Technologies s.r.o.

- Nichrome India Ltd.

- Unither Pharmaceuticals SAS

- Marchesini Group S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Convenience and on-the-go consumption boom

- 4.2.2 Demand for material and weight reduction

- 4.2.3 Sustainability mandates for flexible packs

- 4.2.4 Pharma micro-dosing and pediatric formats

- 4.2.5 Digital printing for mass-customised sachets

- 4.2.6 E-commerce sample sachet proliferation

- 4.3 Market Restraints

- 4.3.1 Single-use-plastic regulation tightening

- 4.3.2 Limited recyclability of multi-layer films

- 4.3.3 Barrier-grade mono-material film shortage

- 4.3.4 High-viscosity fill accuracy limits >15 lanes

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

- 4.8 Key Performance Indicators (KPIs)

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Plastics

- 5.1.2 Paper

- 5.1.3 Metal Foils

- 5.1.4 Bioplastics

- 5.2 By Product Form

- 5.2.1 Powders

- 5.2.2 Granules

- 5.2.3 Liquids

- 5.2.4 Semi-solids

- 5.3 By End-user Industry

- 5.3.1 Food and Beverages

- 5.3.1.1 Instant Beverages

- 5.3.1.2 Nutraceutical Powders

- 5.3.1.3 Sugar and Sweeteners

- 5.3.2 Pharmaceuticals

- 5.3.2.1 OTC

- 5.3.2.2 Rx

- 5.3.3 Cosmetics and Personal Care

- 5.3.4 Industrial and Household

- 5.3.1 Food and Beverages

- 5.4 By Packaging-Machinery Lane Count

- 5.4.1 1-3 Lanes

- 5.4.2 4-10 Lanes

- 5.4.3 11-20 Lanes

- 5.4.4 Greater than 20 Lanes

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 Amcor plc

- 6.4.2 Constantia Flexibles Group GmbH

- 6.4.3 Glenroy, Inc.

- 6.4.4 Aranow Packaging Machinery S.L.

- 6.4.5 Fres-Co System USA, Inc.

- 6.4.6 Catalent, Inc.

- 6.4.7 Winpak Ltd.

- 6.4.8 Sonoco Products Company

- 6.4.9 ePac Holdings, LLC

- 6.4.10 GFR Pharma Ltd.

- 6.4.11 Sonic Packaging Industries, Inc.

- 6.4.12 Viking Masek Global Packaging Technologies s.r.o.

- 6.4.13 Nichrome India Ltd.

- 6.4.14 Unither Pharmaceuticals SAS

- 6.4.15 Marchesini Group S.p.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

条状包装市场报告:按材料、填充类型、容量、应用和地区划分(2026-2034 年)

条状包装市场报告:按材料、填充类型、容量、应用和地区划分(2026-2034 年) 条状包装市场规模、份额及成长分析(按材料、终端用途产业及地区划分)-2026-2033年产业预测

条状包装市场规模、份额及成长分析(按材料、终端用途产业及地区划分)-2026-2033年产业预测 棒状包装市场规模、份额和趋势分析报告:按材料、应用、地区和细分市场预测(2025-2033 年)

棒状包装市场规模、份额和趋势分析报告:按材料、应用、地区和细分市场预测(2025-2033 年) 按最终用途产业、产品类型、材料和分销管道分類的棒状包装市场 - 全球预测 2025-2032

按最终用途产业、产品类型、材料和分销管道分類的棒状包装市场 - 全球预测 2025-2032 印楝棒市场:按产品类型、按应用、按最终用户、按分销管道、按地区

印楝棒市场:按产品类型、按应用、按最终用户、按分销管道、按地区 北美棒状包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)糖包装:市场占有率分析、产业趋势与统计、成长预测(2025-2030)

北美棒状包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)糖包装:市场占有率分析、产业趋势与统计、成长预测(2025-2030) 棒包装市场机会、成长动力、产业趋势分析及 2024 年至 2032 年预测

棒包装市场机会、成长动力、产业趋势分析及 2024 年至 2032 年预测