|

市场调查报告书

商品编码

1940619

摩擦材料:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Friction Material - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

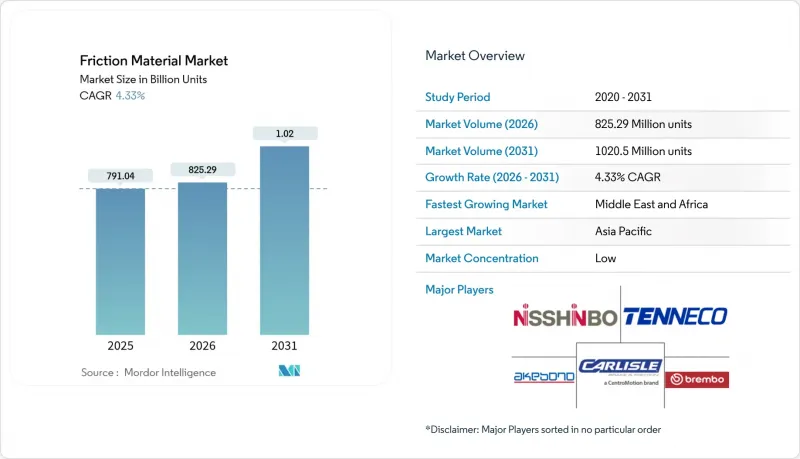

摩擦材料市场规模预计到 2026 年将达到 8.2529 亿单位,高于 2025 年的 7.9104 亿单位。

预计到 2031 年,销量将达到 10.205 亿辆,从 2026 年到 2031 年的复合年增长率为 4.33%。

欧7颗粒物排放法规等监管里程碑、对低粉尘煞车片的强劲需求以及不断增长的车辆保有量,正推动摩擦材料市场稳步成长。製造商正在重新设计煞车片的化学成分,以保持无铜特性,同时,配备感测器的「智慧煞车片」的普及也有助于拓展维护即服务(MaaS)的收入模式。亚太地区的汽车製造能力和完善的售后市场生态系统支撑着该地区最大的市场份额,而东欧成本优化工厂则帮助全球供应商平衡铜、芳香聚酰胺和陶瓷纤维价格波动带来的利润压力。中型区域专业企业和大规模跨国公司竞相将软体、预测分析和再生材料融入下一代产品,共同塑造了当前的竞争格局。

全球摩擦材料市场趋势与洞察

工业和非道路机械的需求不断增长

由于采矿、建筑和农业用重型设备的摩擦部件需要承受极端高温和污染,其单位体积的耗材量高于乘用车。自动驾驶矿用卡车使用配备感测器的碟片和煞车片组件,可将磨损数据即时传输至车队管理系统,从而减少非计划性停机时间。在新兴市场,由于本地支援有限,原始设备製造商 (OEM) 正在使用更高密度的衬片来延长使用寿命。整合式传动系统供应商正在将煞车、离合器和缓速器系统捆绑销售,以增加交叉销售机会。工业采购团队,尤其是在东南亚地区,越来越多地选择拥有本地库存的供应商,以缩短大型盘片的前置作业时间。由于政府持续为基础设施扩建和大吨位货物运输提供资金,预计中期内对驾驶员需求的衝击将保持强劲。

全球汽车保有量快速成长以及煞车皮更换週期

在印度、印尼和越南,车辆保有量的成长速度超过了新车销量,由于车龄超过九年,售后市场煞车片的需求持续强劲。在交通拥挤的都市区环境中,频繁的走走停停会加速煞车片的磨损,缩短更换週期,抵消了电气化带来的销售下滑。订阅制和叫车车队正在实施预防性维护计划,儘管陶瓷煞车片价格较高,但由于其磨损更可预测,因此更倾向于选择陶瓷煞车片。与汽车製造商合作的售后服务网络储备了适用于多种平台的煞车片,从而简化了跨车型代际的库存管理。高阶煞车片品牌正在利用线上管道,结合相容性数据,精准触达DIY消费者。从长远来看,这一因素预计将成为全球复合年增长率的最大积极贡献者。

高昂的生命週期成本与再生煞车减少磨损之间的权衡

都市区环境中电动乘用车的煞车片寿命已超过10万英里,与内燃机车型相比,更换频率显着降低。车队成本会计会权衡低粉尘煞车片的价格与降低的维修成本,这给售后市场通路带来了利润压力。配备主动式能源回收的混合动力SUV在紧急煞车时仍需要高摩擦係数的煞车来令片,这就需要高成本的双组分煞车片解决方案。市政公车业者报告称,随着能量回收煞车进入能量回收阶段,整个煞车系统的总拥有成本降低,从而延缓了煞车片的更换。儘管供应商正将营收重心从销售转向高附加价值涂层和分析技术,但此限制因素仍对摩擦材料市场的复合年增长率(CAGR)产生显着的抑製作用。

细分市场分析

到2025年,煞车皮将继续主导全球替换零件市场,占据摩擦材料市场40.85%的份额。煞车片相关摩擦材料市场规模庞大,反映了其高损耗率以及标准化设计模板带来的跨平台供应便利性。同时,煞车碟盘将以5.59%的复合年增长率成为成长最快的产品,因为整合式电子煞车系统需要更大尺寸、精密金属加工的煞车碟盘,从而推高了平均售价。

煞车片的改进主要集中在无铜有机混合物上,这种混合物能够在不牺牲摩擦係数稳定性的前提下抑製粉尘产生。豪华SUV为了降低簧下质量,纷纷采用通风式和碳陶瓷煞车盘,这推动了煞车盘需求的成长。铁路和重工业领域对煞车块和衬片的需求保持稳定,但自动化正在延长煞车块的更换週期。离合器摩擦片等小众零件正在推动机器人和工业自动化领域的成长。虽然煞车片仍然占据主导地位,但煞车碟盘的营收成长速度更快,这拓宽了全球供应商的策略关注范围。

到2025年,半金属复合材料将占据摩擦材料市场37.95%的份额,这主要得益于其优异的成本绩效。这类复合材料将钢纤维或铜纤维与有机黏合剂结合,兼具抗热衰减性和降噪性。陶瓷复合材料虽然落后于半金属复合材料,但其年复合成长率也达到了5.98%,这主要得益于欧7排放标准和高性能电动车的需求。

Brembo 的 GreenTor 雷射沉积转子涂层可降低 PM10 的排放,展现了陶瓷材料在改变法规遵循成本方面的潜力。烧结金属在铁路和航空领域至关重要,但市占率小规模。富含酰胺纤维的煞车片因其轻量化和高强度特性,在航太和高性能摩托车市场中占据了一席之地。分阶段的研发重点是生物基黏合剂,旨在减少碳排放,同时又不影响耐用性。

区域分析

亚太地区在2025年占据摩擦材料市场45.90%的主导地位,这主要得益于成熟的供应链、具有成本竞争力的劳动力以及中国、印度和东南亚国协汽车保有量的快速增长。中国转子製造商正将铸造厂和加工厂整合到同一产业园区,进而降低物流成本,并提升全球出口竞争力。印度在2024财年上半年实现了收入成长,这主要得益于摩托车销售的復苏和售后市场网络的扩张。日本在电动摩托车煞车套件领域保持主导地位,为高性能车辆专案相关的高端碟煞技术出口做出了贡献。

北美和欧洲拥有成熟的市场基础,这主要得益于其在环保领域的领先地位。欧盟7排放标准和加州铜排放法规使这些市场成为低粉尘光碟和感测器垫的试验场,随后扩展到了亚太地区。为了平衡成本,生产正向东转移至罗马尼亚、波兰和墨西哥,而设计和检验中心则仍设在德国、义大利和美国。

中东和非洲地区复合年增长率最高,达到4.66%,这主要得益于建筑业的蓬勃发展、矿产开采以及对需要耐候型煞车片的进口乘用车的需求。波湾合作理事会正在投资建设都会区域网路和轻轨,刺激了对煞车片和衬片的需求。撒哈拉以南非洲的矿用车辆正在采用专为重型卡车设计的大型湿式碟式煞车。在南美洲,儘管巴西汽车製造业正在逐步復苏,但由于货币波动抑制了售后市场支出,市场前景仍然低迷。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 工业和非公路机械的需求不断增长

- 全球汽车保有量快速成长以及煞车皮更换週期

- 由于对无铜和低噪音材料的法规日益严格,材料重新设计正在加速推进。

- 亚洲摩托车和微型交通工具的快速电气化

- 采用内建感测器的「智慧垫」进行预测性维护

- 市场限制

- 高昂的生命週期成本与再生煞车带来的磨损减少形成对比

- 铜、芳香聚酰胺和陶瓷纤维的价格波动

- 由于汽车製造商转向使用密封式、免维护变速箱,对离合器摩擦材料的需求正在下降。

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争程度

第五章 市场规模与成长预测

- 依产品类型

- 磁碟

- 软垫

- 堵塞

- 衬垫

- 其他类型

- 材料

- 陶瓷(包括碳陶瓷和碳碳陶瓷)

- 石棉

- 半金属

- 烧结金属

- 酰胺纤维

- 其他成分

- 透过使用

- 离合器和煞车系统

- 齿轮系统

- 其他用途

- 按最终用户行业划分

- 车

- 铁路

- 航太(民用和国防)

- 矿业

- 其他终端用户产业

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 东南亚国协

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧国家

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- ABS Friction

- Akebono Brake Industry Co., Ltd.

- ASK FRAS-LE FRICTION PVT LTD.

- Brembo SpA

- Carlisle Brake & Friction(CentroMotion)

- ContiTech Deutschland GmbH

- EBC Brakes

- Haldex

- Hindustan Composites Ltd.

- ITT Inc.

- Japan Brake Industrial Co., Ltd.

- Miba AG

- Nisshinbo Holdings Inc.

- SGL Carbon

- Tenneco Inc.

- Yantai Haina Brake Technology Co., Ltd.

第七章 市场机会与未来展望

Friction Material Market size in 2026 is estimated at 825.29 million units, growing from 2025 value of 791.04 million units with 2031 projections showing 1020.5 million units, growing at 4.33% CAGR over 2026-2031.

Regulatory milestones such as the Euro 7 particulate limits, brisk demand for low-dust discs and pads, and rising vehicle parc volumes keep the friction material market on a steady growth path. Manufacturers are re-engineering pad chemistry to remain copper-free, while adoption of sensor-enabled "smart pads" is broadening maintenance-as-a-service revenue models. The Asia-Pacific's vehicle production strength and deep aftermarket ecosystem anchor the largest regional volume share, whereas cost-optimized Eastern European plants help global suppliers balance margin pressure from volatile prices of copper, aramid, and ceramic fiber. Competitive intensity is shaped by mid-sized regional specialists and large multinational players racing to embed software, predictive analytics, and recycled inputs into next-generation products.

Global Friction Material Market Trends and Insights

Growing need for industrial and off-highway machinery

Heavy mining, construction, and agricultural equipment consume friction components that tolerate extreme heat and contamination, lifting unit volumes well above those of passenger vehicles. Autonomous mining trucks now feature sensor-fed disc and pad sets that transmit wear data in real-time to fleet dashboards, reducing unscheduled downtime. Original-equipment manufacturers adopt higher-density linings to extend service life in emerging markets where on-site support is scarce. Integrated drivetrain suppliers bundle brake, clutch, and retarder systems, boosting cross-selling potential. Industrial procurement teams increasingly select suppliers with localized stock points to reduce lead times on oversized discs, particularly in Southeast Asia. The driver's mid-term impact remains firm as governments fund infrastructure expansion and commodities continue to move at high tonnage.

Surging global vehicle parc and brake-pad replacement cycles

Vehicle fleets in India, Indonesia, and Vietnam are growing faster than new-car sales, as the average car age climbs past nine years, sustaining aftermarket pad demand. Replacement intervals shorten in dense urban traffic because stop-and-go conditions accelerate pad wear, offsetting electrification-driven volume losses. Subscription and ride-hailing fleets impose proactive maintenance schedules that favor predictable-wear ceramic pads despite higher ticket prices. OEM-aligned service networks stock multi-platform pad lines to streamline inventory across model generations. Premium pad brands utilize online channels, leveraging fitment data, to target do-it-yourself consumers. Over the long term, this driver adds the largest positive swing to the global CAGR.

High lifecycle cost versus regenerative-braking wear reduction

Electric passenger cars in urban duty show pad life stretching past 100,000 miles, slashing replacement events relative to internal-combustion models. Fleet calculations weigh the pricing of low-dust pads against fewer interventions, placing margin pressure on aftermarket channels. Hybrid SUVs with aggressive regen reclaim still demand robust pad friction for emergency stops, forcing costly dual-compound solutions. Municipal bus operators report a drop in total brake system cost of ownership once regenerative braking reaches recovery, delaying pad changeouts. Suppliers shift their revenue focus from volume to value-added coatings and analytics, but the restraint remains a noticeable drag on the CAGR of the friction material market.

Other drivers and restraints analyzed in the detailed report include:

- Stricter copper-free and low-noise regulations accelerating material reformulation

- Rapid electrification of two-wheelers and micro-mobility fleets in Asia

- Volatile prices of copper, aramid and ceramic fibers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Brake pads captured 40.85% of the friction material market share in 2025 and continue to form the backbone of the global replacement business. The friction material market size tied to pads reflects high wear rates and standardized design templates that simplify cross-platform supply. Discs, however, post the quickest 5.59% CAGR as integrated electronic braking systems demand larger rotors with precise metallurgy, nudging average selling prices upward.

Pad upgrades center on copper-free organic blends that limit dust without compromising coefficient stability. Rotor demand gains a tailwind from premium SUVs specifying ventilated or carbon-ceramic discs, which reduce unsprung mass. Block and lining volumes remain steady in rail and heavy industry, although automation is extending block change intervals. Other niche components, such as clutch facings, leverage growth in robotics and industrial automation. Aggregate dynamics keep pads dominant, although discs accrue incremental revenue faster, thereby widening the strategic focus for global suppliers.

Semi-metallic recipes accounted for 37.95% of the friction material market size in 2025, thanks to proven cost-performance trade-offs. These blends combine steel or copper fibers with organic binders, providing a balance between fade resistance and noise control. Ceramic formulations trail but expand at 5.98% CAGR, propelled by Euro 7 dust caps and high-performance electric vehicle demand.

Brembo's Greentell laser-deposited rotor coating reduces PM10 and demonstrates the ceramic's potential to shift the economics of regulatory compliance. Sintered metals remain essential for rail and aircraft, but they account for a smaller slice. Aramid-rich pads capture a niche share in the aerospace and performance motorcycle markets due to their lightweight strength. Incremental research and development efforts focus on bio-based binders, aiming to reduce the carbon footprint without compromising durability.

The Global Friction Material Market Report is Segmented by Product Type (Discs, Pads, Blocks, Linings, and Other Types), Material (Ceramic, Asbestos, Semi-Metallic, and More), Application (Clutch and Brake Systems, Gear Tooth Systems, and Other Applications), End-User Industry (Automotive, Railway, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Volume (Units).

Geography Analysis

The Asia-Pacific region held a commanding 45.90% market share of the friction material market in 2025, thanks to its entrenched supply chains, cost-competitive labor, and soaring vehicle ownership across China, India, and ASEAN. Chinese rotor producers integrate foundries and machining shops within a single industrial park, slashing logistics costs and supporting global export competitiveness. India reported a revenue growth in H1 2024, as two-wheeler sales rebounded and aftermarket networks expanded. Japan contributed premium disc technology exports tied to performance vehicle programs and maintained leadership in electric-motorcycle braking kits.

North America and Europe together form a mature volume base governed by environmental leadership. Euro 7 and California's copper restrictions position these markets as test beds for low-dust discs and sensorized pads, knowledge that subsequently scales to the Asia-Pacific region. Production shifts eastward to Romania, Poland, and Mexico, keeping cost parity, while design and validation centers stay in Germany, Italy, and the United States.

The Middle East and Africa represent the fastest-growing regional CAGR at 4.66%, driven by construction booms, mineral extraction, and the demand for imported passenger vehicles, which require climate-resilient pads. Gulf Cooperation Council projects funnel capital into metro networks and light-rail, spurring block and lining demand. Sub-Saharan mining fleets utilize oversized wet-disc brakes, specifically designed for heavy-haul trucks. South America exhibits a tempered outlook as currency volatility restrains aftermarket spending, despite a gradual recovery in Brazilian auto output.

- ABS Friction

- Akebono Brake Industry Co., Ltd.

- ASK FRAS-LE FRICTION PVT LTD.

- Brembo S.p.A.

- Carlisle Brake & Friction (CentroMotion)

- ContiTech Deutschland GmbH

- EBC Brakes

- Haldex

- Hindustan Composites Ltd.

- ITT Inc.

- Japan Brake Industrial Co., Ltd.

- Miba AG

- Nisshinbo Holdings Inc.

- SGL Carbon

- Tenneco Inc.

- Yantai Haina Brake Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing need for industrial and off-highway machinery

- 4.2.2 Surging global vehicle parc and brake-pad replacement cycles

- 4.2.3 Stricter copper-free and low-noise regulations accelerating material reformulation

- 4.2.4 Rapid electrification of two-wheelers and micro-mobility fleets in Asia

- 4.2.5 Adoption of sensor-embedded "smart pads" for predictive maintenance

- 4.3 Market Restraints

- 4.3.1 High lifecycle cost versus regenerative-braking wear reduction

- 4.3.2 Volatile prices of copper, aramid and ceramic fibers

- 4.3.3 OEM shift to sealed, maintenance-free transmissions cutting clutch friction demand

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Discs

- 5.1.2 Pads

- 5.1.3 Blocks

- 5.1.4 Linings

- 5.1.5 Other Types

- 5.2 By Material

- 5.2.1 Ceramic (incl. carbon-ceramic and carbon-carbon)

- 5.2.2 Asbestos

- 5.2.3 Semi-metallic

- 5.2.4 Sintered Metals

- 5.2.5 Aramid Fibers

- 5.2.6 Other Materials

- 5.3 By Application

- 5.3.1 Clutch and Brake Systems

- 5.3.2 Gear Tooth Systems

- 5.3.3 Other Applications

- 5.4 By End-user Industry

- 5.4.1 Automotive

- 5.4.2 Railway

- 5.4.3 Aerospace (Commercial and Defense)

- 5.4.4 Mining

- 5.4.5 Other End-User Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ABS Friction

- 6.4.2 Akebono Brake Industry Co., Ltd.

- 6.4.3 ASK FRAS-LE FRICTION PVT LTD.

- 6.4.4 Brembo S.p.A.

- 6.4.5 Carlisle Brake & Friction (CentroMotion)

- 6.4.6 ContiTech Deutschland GmbH

- 6.4.7 EBC Brakes

- 6.4.8 Haldex

- 6.4.9 Hindustan Composites Ltd.

- 6.4.10 ITT Inc.

- 6.4.11 Japan Brake Industrial Co., Ltd.

- 6.4.12 Miba AG

- 6.4.13 Nisshinbo Holdings Inc.

- 6.4.14 SGL Carbon

- 6.4.15 Tenneco Inc.

- 6.4.16 Yantai Haina Brake Technology Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment

摩擦改进剂市场:按类型、基础油相容性、应用、终端用户产业和销售管道划分-2026-2032年全球市场预测摩擦材料市场:2026-2032年全球市场预测(依产品类型、材料类型、应用、终端用户产业及销售管道)

摩擦改进剂市场:按类型、基础油相容性、应用、终端用户产业和销售管道划分-2026-2032年全球市场预测摩擦材料市场:2026-2032年全球市场预测(依产品类型、材料类型、应用、终端用户产业及销售管道) 全球摩擦材料市场规模、份额、趋势和成长分析报告(2026-2034年)

全球摩擦材料市场规模、份额、趋势和成长分析报告(2026-2034年) 摩擦改质剂市场 - 全球产业规模、份额、趋势、机会及预测(按类型、应用、地区和竞争格局划分,2021-2031年)

摩擦改质剂市场 - 全球产业规模、份额、趋势、机会及预测(按类型、应用、地区和竞争格局划分,2021-2031年) 2026-2030年全球摩擦产品市场摩擦改进剂市场-2026-2031年预测

2026-2030年全球摩擦产品市场摩擦改进剂市场-2026-2031年预测 摩擦改进剂市场规模、份额和成长分析(按类型、应用和地区划分)—2026-2033年产业预测

摩擦改进剂市场规模、份额和成长分析(按类型、应用和地区划分)—2026-2033年产业预测 摩擦改进剂添加剂市场报告:2030 年趋势、预测与竞争分析

摩擦改进剂添加剂市场报告:2030 年趋势、预测与竞争分析 摩擦改质剂市场规模、份额、趋势分析报告:按类型、应用、地区、细分市场预测,2024-2030 年

摩擦改质剂市场规模、份额、趋势分析报告:按类型、应用、地区、细分市场预测,2024-2030 年 摩擦材料市场(产品类型:金属、烧结金属、低金属、非石棉有机、陶瓷等)- 2024-2034 年全球产业分析、规模、份额、成长、趋势和预测

摩擦材料市场(产品类型:金属、烧结金属、低金属、非石棉有机、陶瓷等)- 2024-2034 年全球产业分析、规模、份额、成长、趋势和预测