|

市场调查报告书

商品编码

1940679

数位化货运代理:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Digital Freight Forwarding - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

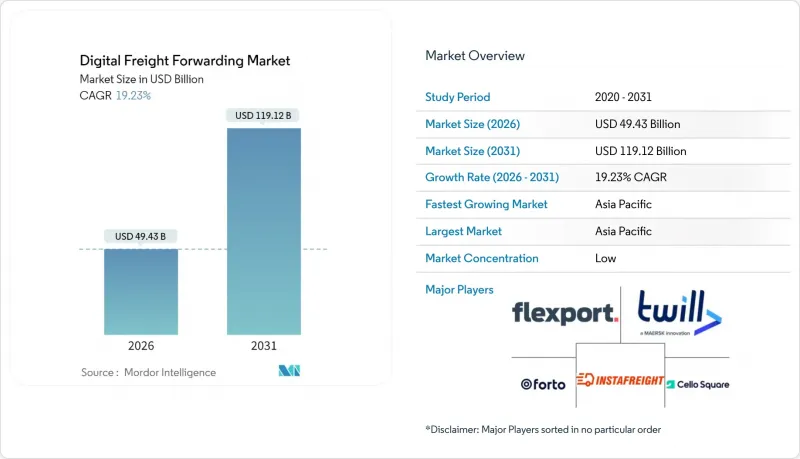

预计到 2026 年,数位货运代理市场规模将达到 494.3 亿美元,高于 2025 年的 414.6 亿美元。

预计到 2031 年将达到 1,191.2 亿美元,2026 年至 2031 年的复合年增长率为 19.23%。

跨境电子商务的快速发展、无纸化贸易的监管要求以及API赋能的承运商连接的扩展,共同推动着增长,托运人正逐步摆脱传统的纸质订舱流程。整合了票价搜寻、订舱、清关和即时视觉化功能的云端原生平台,如今已成为全球贸易协调的基础。亚太地区凭藉其作为出口导向製造业群的优势以及政府主导的中小企业数位化项目,保持着主导地位。同时,北美和欧洲正透过早期实现承运商API标准化和严格的资料准确性法规来扩大规模。竞争格局围绕着垂直整合展开,例如DSV与Schenker的整合,以及利用人工智慧进行线路级动态定价的纯技术型新参与企业。这导致人工仲介业者的利润率结构性压缩,并促使企业持续投资于加值数位服务,从而增加了托运人的转换成本。

全球数位化货运代理市场趋势与洞察

跨境电子商务的快速成长

预计到2027年,跨境零售贸易额将超过8兆美元,维持9%的复合年增长率,因为东南亚卖家无需透过批发商即可直接接触西方消费者。托运人越来越希望找到一个统一的介面来整合清关、关税计算和最后一公里物流追踪。数位货运代理平台能够自动完成欧盟ICS2计画要求的进口总申报,从而省去人工文书工作,减少过境延误。全通路零售商现在期望货运工具能够使用单一追踪ID来管理托盘级的B2B货运和小包裹级的B2C配送。那些整合了自动化合规功能和多承运商小包裹路由的平台营运商,正在获得相对于依赖电子表格和电子邮件的仲介业者的竞争优势。

基于云端的货运平台日益普及

本地部署的运输管理系统缺乏与现代承运商API整合的能力,也无法提供跨多种运输方式的亚分钟级即时可视性,因此71%的部署方案都基于云端。中型托运人正在接受随货运量扩展的订阅定价模式,而不是传统软体所需的大量资本投入。为符合GDPR而建置的资料本地化模组正在欧洲加速普及,供应商提供区域内託管和用户许可管治,进一步推动了受监管行业数位货运代理市场的稳步渗透。与主流ERP套件的预置连接器最大限度地减轻了IT负担,进一步降低了中小企业的进入门槛。

数据标准碎片化

物流资料集仍各自独立,铁路、公路、海运和航空业者使用的EDI和API规范互不相容。托运人仍需协调多个集成,这阻碍了端到端自动化,并加剧了IT预算的压力。区块链先导计画展现了其在透明度方面的潜力,但缺乏统一的数据字典限制了其规模化应用。各国政府正在推广自愿性框架,但在网路连结和资源有限的新兴地区,采用速度缓慢。在缺乏全球协议的情况下,数位货运代理市场仍在持续扩张,但却面临高成本的变通方案。

细分市场分析

到2025年,运输管理将占总收入的58.45%,凸显其作为托运人进军数位化货运代理市场的第一步的重要性。自动化的线路级路线规划和即时运价搜寻能够带来即时的投资收益,即使是注重成本的中小型企业也积极采用。人工智慧负载容量平衡提高了每英里卡车的收入,减少了空驶返程,而海运电子载货证券(eB/L)则加快了货物的交付速度。

从报关代理到供应链金融,附加价值服务是成长最快的领域,年复合成长率高达13.85%。这些服务透过将财务和合规营运嵌入平台,提升了客户忠诚度。随着全通路零售需要入库货物和履约中心之间更紧密的协调,与仓库管理系统的整合变得日益重要。拓展这些相关领域使平台能够占据更大的托运人支出份额,并透过简单的价格比较来避免同质化竞争。

到2025年,零售和电子商务产业将占据35.42%的市场份额,这主要得益于D2C品牌出口的成长以及对限时抢购配送需求的增加。服装和消费性电子产品的托运人非常欣赏数位货运平台提供的端到端可视性。

医疗保健和製药业是一个快速成长的领域,预计到2031年将维持10.95%的复合年增长率。温控货物监控、序列级可追溯性和严格的审核追踪需要专门的数位化工作流程。供应商正加速关注药品合规性,例如DHL已在其医疗保健网路中投资22亿美元,而能够确保2至8°C运输路线完整性的平台将成为竞争优势。

区域分析

预计到2025年,亚太地区将占全球收入的39.55%,年复合成长率达19.42%,这反映了製造业出口的主导地位以及支持中小企业数位化的公共政策。印度的快递物流业正朝着年增长10-12%的目标迈进,这主要得益于高速公路和机场的改善加快了货物运输速度。 《亚太贸易便利化报告》估计,数位化单证改革可降低平均贸易成本11%,进一步凸显了采用数位化单证改革的必要性。

北美受益于成熟的电子商务生态系统以及卡车运输和包裹运输公司API标准化的领先阶段。联邦海事委员会的数据准确性计划推广标准化事件代码,并支援平台间的互通性。加拿大和墨西哥正利用美墨加协定(USMCA)带来的近岸外包势头,推动对自动化海关模组和双语介面的需求。

在欧洲,诸如eFTI和ICS2等无纸化法规正迫使托运人数位化。德国DSV和Schenker的合併催生了10亿欧元(11亿美元)的数位化提昇预算,而北欧国家则正将其平台部署与绿色物流目标相契合。英国脱欧后的海关通讯协定推动了自动化合规的需求,进而促使货运代理业务转移到综合服务供应商。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 跨境电子商务的快速成长

- 云端货运平台的普及应用日益广泛

- 支援 API 的营运商连接

- 人工智慧驱动的动态定价市场

- 欧盟电子财务资讯技术法规强制要求数位化文件记录

- 卫星物联网路线优化工具

- 市场限制

- 数据标准的碎片化

- 网路安全和隐私风险

- 数位技能短缺

- 运输公司直接预订利润率面临压力

- 价值/供应链分析

- 监管环境

- 技术展望

- 投资情境分析

- 电子平台价值提案基准

- 全球动盪对贸易流量的影响

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场规模及成长预测(价值,十亿美元)

- 按功能

- 运输管理

- 土地

- 海洋

- 航空

- 仓库管理

- 附加价值服务

- 运输管理

- 最终用户

- 零售与电子商务

- 製造业

- 医疗保健和製药

- 车

- 其他的

- 透过部署模式

- 云

- 本地部署

- 按公司类型

- 小型企业

- 大型企业和政府机构

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 秘鲁

- 智利

- 阿根廷

- 南美洲其他地区

- 亚太地区

- 印度

- 中国

- 日本

- 澳洲

- 韩国

- 东南亚(新加坡、马来西亚、泰国、印尼、越南、菲律宾)

- 亚太其他地区

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 义大利

- 比荷卢经济联盟(比利时、荷兰、卢森堡)

- 北欧国家(丹麦、芬兰、冰岛、挪威、瑞典)

- 其他欧洲地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 奈及利亚

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Flexport

- Twill(Maersk)

- Forto

- Cello Square

- InstaFreight

- Transporteca

- Kontainers

- Kuehne+Nagel International AG(KN Freight Net)

- Turvo

- iContainers

- DHL Group

- DSV(Shipa Freight/myDSV)

- Sennder

- Cargo.one

- CEVA Logistics

- Shypple

- Zencargo

- Cubic

- Boxnbiz

- Freightwalla

第七章 市场机会与未来展望

Digital Freight Forwarding Market size in 2026 is estimated at USD 49.43 billion, growing from 2025 value of USD 41.46 billion with 2031 projections showing USD 119.12 billion, growing at 19.23% CAGR over 2026-2031.

Rapid cross-border e-commerce adoption, regulatory mandates for paperless trade, and the spread of API-enabled carrier connectivity collectively propel growth as shippers pivot away from analog booking processes. Integrated, cloud-native platforms that fuse rate discovery, booking, customs, and real-time visibility now form the backbone of global trade orchestration. Asia-Pacific retains leadership because of deep export manufacturing hubs and government-backed SME digitization programs, while North America and Europe scale through early carrier API standardization and strict data accuracy rules. Competitive dynamics center on vertical integrations like the DSV-Schenker combination and on pure-play technology entrants harnessing AI for lane-level dynamic pricing. The result is structural margin compression for manual intermediaries and sustained investment in value-added digital services that raise switching costs for shippers.

Global Digital Freight Forwarding Market Trends and Insights

Rapid Growth of Cross-Border E-commerce

Cross-border retail transactions are forecast to surpass USD 8 trillion by 2027, maintaining a 9% CAGR as Southeast Asian sellers reach Western consumers without wholesalers. Shippers increasingly demand unified customs clearance, duty calculation, and last-mile traceability in one interface. Digital freight forwarding market platforms automate entry summary declarations required under the European Commission's ICS2 program, eliminating manual paperwork and cutting border clearance delays. Omnichannel retailers now expect freight tools that manage pallet-level B2B moves alongside parcel-level B2C deliveries under a single tracking ID. Platform operators that embed automated compliance and multi-carrier parcel routing gain competitive advantage over intermediaries reliant on spreadsheets or email.

Rising Adoption of Cloud-Based Freight Platforms

Cloud models account for 71% of deployments because on-premise Transportation Management Systems cannot connect to modern carrier APIs or provide sub-minute visibility across modes. Mid-market shippers embrace subscription pricing that scales with shipment volumes, in contrast to the heavy capex demanded by legacy software. Data-localization modules built for GDPR compliance accelerate European uptake as vendors offer in-region hosting and consent governance, positioning the digital freight forwarding market for steady penetration in regulated verticals. Pre-built connectors into leading ERP suites minimize IT effort, further lowering barriers for SMEs.

Data-Standards Fragmentation

Logistics data sets remain siloed because rail, truck, ocean, and air parties adopt incompatible EDI and API specifications. Shippers must still juggle multiple integrations, hurting end-to-end automation and enlarging IT budgets. Blockchain pilots demonstrate transparency potential yet stall at scale for lack of unified data dictionaries. Governments push voluntary frameworks, but adoption lags in emerging regions where connectivity and resources are limited. Without global consensus, digital freight forwarding market expansion continues, albeit with costly workarounds.

Other drivers and restraints analyzed in the detailed report include:

- API-Enabled Carrier Connectivity

- AI-Driven Dynamic-Pricing Marketplaces

- Cyber-Security & Privacy Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation Management contributed 58.45% of 2025 revenue, underscoring its role as the first stop for shippers entering the digital freight forwarding market. Automated lane-level routing and live rate discovery generate immediate ROI, encouraging adoption even among cost-conscious SMEs. AI load-balancing elevates truck revenue per mile and trims empty backhauls, while electronic Bills of Lading in ocean freight hasten cargo releases.

Value-added Services, from customs clearance to supply-chain financing, is the fastest-growing slice, advancing at a 13.85% CAGR. These offerings stick customers to platforms by embedding financial and compliance workflows. Warehouse Management integration gains importance as omnichannel retail requires tight coordination between inbound freight and fulfillment centers. The expansion of these adjacencies positions platforms to capture a larger share of shipper spend and insulate against pure rate-comparison commoditization.

Retail & E-commerce dominated demand at 35.42% in 2025, propelled by direct-to-consumer brand exports and flash-sale delivery promises. Shippers of apparel and consumer electronics prize the end-to-end visibility that digital freight forwarding market platforms deliver.

Healthcare & Pharma is the breakout segment, on track for an 10.95% CAGR through 2031. Temperature-controlled cargo monitoring, serial-level traceability, and stringent audit trails demand specialized digital workflows. Investments such as DHL's USD 2.2 billion spend on healthcare networks amplify vendor focus on pharma compliance, differentiating platforms able to guarantee 2-8°C lane integrity.

The Digital Freight Forwarding Market Report is Segmented by Function (Transportation Management, Warehouse Management, Value-Added Services), End-Users (Retail & E-Commerce, and More), Deployment Mode (Cloud, On-Premise), Firm Type (SMEs, Large Enterprises and Government Entities), and Geography (North America, South America, Asia-Pacific, Europe, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific holds 39.55% of 2025 revenue and is set to expand at a 19.42% CAGR, reflecting dominant manufacturing exports and supportive public policy that subsidizes SME digitization. India's express logistics sector targets 10-12% annual growth with highway and airport upgrades quickening freight flows. The Asia-Pacific Trade Facilitation Report pegs average trade-cost cuts at 11% from digital documentation reforms, reinforcing adoption logic.

North America benefits from entrenched e-commerce ecosystems and early-stage API uniformity across truckload and parcel carriers. Federal Maritime Commission data-accuracy programs stimulate standardized event codes, aiding platform interoperability. Canada and Mexico ride USMCA nearshoring momentum, raising demand for automated border-clearance modules and bilingual interfaces.

Europe pushes paperless mandates via eFTI and ICS2, compelling shippers to digitize or lose market access. Germany gains from the DSV-Schenker merger's EUR 1 billion (USD 1.10 billion) digital enhancement budget, while Nordic countries pair platform adoption with green-logistics goals. Post-Brexit customs protocols in the United Kingdom intensify need for compliance automation, steering freight toward integrated service providers.

- Flexport

- Twill (Maersk)

- Forto

- Cello Square

- InstaFreight

- Transporteca

- Kontainers

- Kuehne + Nagel International AG (KN Freight Net)

- Turvo

- iContainers

- DHL Group

- DSV (Shipa Freight / myDSV)

- Sennder

- Cargo.one

- CEVA Logistics

- Shypple

- Zencargo

- Cubic

- Boxnbiz

- Freightwalla

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid growth of cross-border e-commerce

- 4.2.2 Rising adoption of cloud-based freight platforms

- 4.2.3 API-enabled carrier connectivity

- 4.2.4 AI-driven dynamic-pricing marketplaces

- 4.2.5 EU eFTI regulation mandating digital documents

- 4.2.6 Satellite-IoT route-optimisation tools

- 4.3 Market Restraints

- 4.3.1 Data-standards fragmentation

- 4.3.2 Cyber-security and privacy risks

- 4.3.3 Digital-skills talent gap

- 4.3.4 Carrier direct-booking margin squeeze

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Investment Scenario Analysis

- 4.8 Value-Proposition Benchmarking of E-Platforms

- 4.9 Impact of Global Disruptions on Trade Flows

- 4.10 Porter's Five Forces

- 4.10.1 Bargaining Power of Suppliers

- 4.10.2 Bargaining Power of Buyers

- 4.10.3 Threat of New Entrants

- 4.10.4 Threat of Substitutes

- 4.10.5 Competitive Rivalry Intensity

5 Market Size and Growth Forecasts (Value, USD Bn)

- 5.1 By Function

- 5.1.1 Transportation Management

- 5.1.1.1 Land

- 5.1.1.2 Sea

- 5.1.1.3 Air

- 5.1.2 Warehouse Management

- 5.1.3 Value-added Services

- 5.1.1 Transportation Management

- 5.2 By End-users

- 5.2.1 Retail and E-commerce

- 5.2.2 Manufacturing

- 5.2.3 Healthcare and Pharma

- 5.2.4 Automotive

- 5.2.5 Others

- 5.3 By Deployment Mode

- 5.3.1 Cloud

- 5.3.2 On-premise

- 5.4 By Firm Type

- 5.4.1 SMEs

- 5.4.2 Large Enterprises and Government Entities

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 Europe

- 5.5.4.1 United Kingdom

- 5.5.4.2 Germany

- 5.5.4.3 France

- 5.5.4.4 Spain

- 5.5.4.5 Italy

- 5.5.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.4.8 Rest of Europe

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab of Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East And Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, ... Recent Developments)

- 6.4.1 Flexport

- 6.4.2 Twill (Maersk)

- 6.4.3 Forto

- 6.4.4 Cello Square

- 6.4.5 InstaFreight

- 6.4.6 Transporteca

- 6.4.7 Kontainers

- 6.4.8 Kuehne + Nagel International AG (KN Freight Net)

- 6.4.9 Turvo

- 6.4.10 iContainers

- 6.4.11 DHL Group

- 6.4.12 DSV (Shipa Freight / myDSV)

- 6.4.13 Sennder

- 6.4.14 Cargo.one

- 6.4.15 CEVA Logistics

- 6.4.16 Shypple

- 6.4.17 Zencargo

- 6.4.18 Cubic

- 6.4.19 Boxnbiz

- 6.4.20 Freightwalla

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment