|

市场调查报告书

商品编码

1940684

数位借贷:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Digital Lending - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

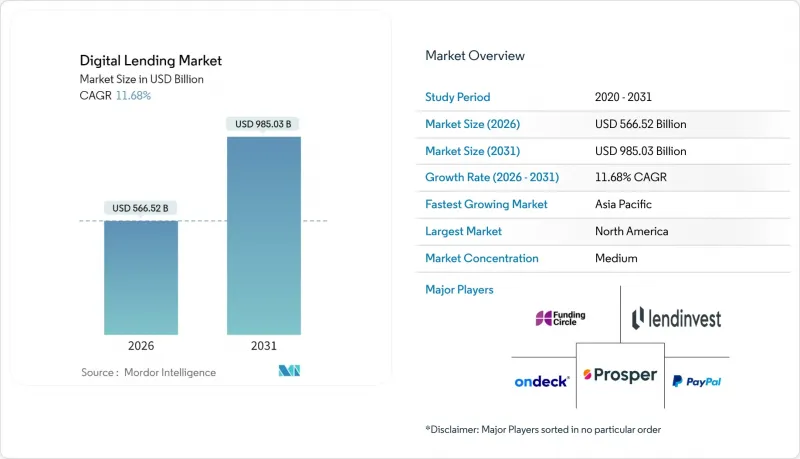

2025年数位借贷市场价值5,072.7亿美元,预计到2031年将达到9,850.3亿美元,高于2026年的5,665.2亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 11.68%。

这一成长趋势表明,技术驱动的信贷业务正稳步发展,嵌入式金融交易量不断增长,人工智慧承销技术也得到了机构的广泛认可。即时信贷决策、开放银行资料传输以及先买后付(BNPL)选项持续吸引借款人放弃分店分行。金融机构正投资云端原生贷款系统,以降低处理成本,并将贷款发放时间从数週缩短至数分钟。另类资料信用评分技术正在创造新的商机,例如针对信用记录不佳的客户以及跨境中小企业资金筹措。随着金融科技公司、传统银行和大型科技平台在关键地区争取同一群客户,竞争日益激烈。

全球数位借贷市场趋势与洞察

智慧型手机和网路的快速普及加速了行动优先贷款业务的发展。

到2024年,全球智慧型手机用户数量将达到68亿,这将使贷款机构能够透过行动应用程式直接接触借款人。光是亚太地区的数位钱包支付额就将达到9.8兆美元,将提升消费者对应用程式内信贷的接受度。如今,贷款机构正利用位置数据、设备元资料和行为模式在几秒钟内评估风险,从而向数百万首次借款人提供信贷。印度资料保护委员会和欧盟人工智慧法等监管机构正在规范资料使用,使贷款机构能够扩展合规的行动优先模式。

金融科技即时核准平台的兴起正在改变借款人的预期。

超过90%的数位贷款申请现在都经过自动化审核引擎,而Upstart无需上传文件即可达到80%的即时核准。机器学习模型即时分析数百项借款人属性,从而降低审核成本并提高客户满意度。那些无法将核准时间缩短至五分钟以内的银行,为了维持市场份额,正越来越多地选择与金融科技供应商建立白牌合作关係。

网路安全和资料隐私风险对平台扩充性构成挑战。

儘管金融机构仅有13%的IT预算用于安全,但它们的API使用量却不断扩大。到2024年,62%的受访贷款机构表示诈骗事件将会增加,监管机构也要求在GDPR和CCPA法规下采用零信任架构。不断上涨的网路保险费和强制性资料外洩通知要求正在推高合规成本,尤其是对于跨境平台而言。

细分市场分析

2025年,受个人金融和先买后付(BNPL)需求的推动,消费贷款占数位借贷市场的60.78%。同时,预计到2031年,小型企业贷款将以16.08%的复合年增长率增长,这主要得益于采用替代数据模型来评估营运资金缺口和实现即时现金流可见度。预计到2031年,小型企业数位借贷市场规模将达到2,460.9亿美元。贷款机构正在将会计软体与应用程式介面(API)集成,以收集发票、薪资和税务数据,从而将信贷审批週期从数週缩短至48小时。随着社群平台实现与消费者贷款组合相当的信贷损失率,全球银行正透过收益分成伙伴关係来确保分销管道的畅通。

在消费领域,融入电商支付流程的信贷服务持续扩大其在低收入群体中的渗透率。千禧世代的劳工阶级越来越多地利用薪资週期数据来预支薪资。先进的可解释人工智慧模型有效降低了偏见,表明大规模企业市场。

到2025年,个人贷款将占数位借贷市场规模的35.44%,这得益于其即时审批模式和低成本优势。汽车贷款也将紧随其后,利用销售点(POS)整合将经销商的处理时间缩短至60秒以内[UPSTART.COM]。由于抵押品审批和补贴规定复杂,房屋抵押贷款、住宅净值贷款和学生贷款领域的数位转型进程较为缓慢。

预计中小企业营运资金贷款的复合年增长率将达到10.52%。销售挂钩贷款将还款与每日信用卡销售挂钩,使企业在需求波动时拥有柔软性。嵌入企业资源计画 (ERP) 控制面板的应收帐款应收帐款承购平台可在发票开立后24小时内释放流动资金。这种嵌入式融资方式正吸引全球物流、农业和自由工作者生态系统,这些企业先前缺乏传统信贷额度所需的抵押品。

区域分析

到2025年,亚太地区将占据全球数位借贷市场39.35%的份额,这得益于超过235家持牌数位银行以及政府支持的支付基础设施,例如印度的UPI(平均每月交易量达120亿笔)。中国的超级应用程式透过将借贷功能迭加到电子钱包、叫车和外送服务之上,建构了强大的数据循环。新加坡和澳洲政府正在运行监管沙盒,将产品测试週期缩短至六个月,加快新金融机构进入市场的速度。

预计非洲将以21.85%的复合年增长率成为成长最快的地区,到2028年,其收入将达到470亿美元。肯亚和加纳率先开发的行动支付基础设施为小额贷款奠定了基础,透过分析话费购买和个人转帐来计算风险评分。尼日利亚和埃及的Start-Ups正在吸引国际创业投资资金,为非洲移民开发跨境预支工资解决方案。

北美和欧洲的普及率很高,但表面成长率正在放缓。儘管美国的「先买后付」(BNPL)相关法律仍处于不断变化之中,但PayPal的累计贷款额已超过300亿美元,展现出成熟企业的规模。在欧洲,PSD3和欧盟人工智慧法案的修订提供了统一的规则,并加强了跨境通行证制度。然而,多项消费信贷指令中的利率上限限制了高收入细分市场的发展。在拉丁美洲,基于即时支付的嵌入式金融交易(例如巴西的PIX)的兴起,为两位数的贷款成长奠定了基础,即使宏观经济波动,也能保持这一成长势头。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 智慧型手机和网路普及率快速成长

- 金融科技即时核准平台的激增

- 有利于开放银行和电子客户身份验证(e-KYC)的法规环境

- 微企业对快速营运资金贷款的需求

- 针对信用状况良好的借款人的替代数据信用评分

- 非银行应用程式内嵌入式贷款的兴起

- 市场限制

- 网路安全与资料隐私风险

- 监管利率上限和平台重新分类

- P2P市场违约激增引发投资人疲劳

- 第三方云端基础架构的集中风险

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按类型

- 消费者

- 大型企业/中小企业

- 按贷款类型

- 个人贷款

- 汽车贷款

- 学生贷款

- 房屋抵押贷款/房屋股权贷款

- 小规模企业营运资金贷款

- 透过部署模式

- 基于云端的平台

- 本地部署解决方案

- 杂交种

- 按经营模式

- P2P(市场)借贷

- 资产负债表(直接)融资

- 嵌入式融资/先买后付贷款

- 群众集资及以收益为准贷款

- 透过技术

- 利用人工智慧/机器学习进行信用筛选

- API和开放银行平台

- 基于区块链的贷款

- 巨量资料分析

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 中东

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 北美洲

第六章 竞争情势

- 市场集中度分析

- 策略性倡议(併购、合作、服务发布)

- 市占率分析(前 15 家公司,2024 年)

- 公司简介

- Ant Group Co., Ltd.

- WeBank Co., Ltd.

- PayPal Holdings, Inc.

- Klarna Bank AB(publ)

- LendingClub Corporation

- Upstart Holdings, Inc.

- Funding Circle Holdings plc

- On Deck Capital, Inc.

- Prosper Marketplace, Inc.

- SoFi Technologies, Inc.

- Kabbage, Inc.(American Express Co.)

- LendInvest plc

- Zopa Bank Ltd.

- Kaspi.kz JSC

- Ferratum Oyj

- CAN Capital, Inc.

- International Personal Finance plc

- Faircent Tech Pvt. Ltd.

- LenDenClub Techserve Pvt. Ltd.

- CapFloat Financial Services Pvt. Ltd.

- Oriente Group Limited

- Mercado Libre, Inc.

- Square Loans(Block, Inc.)

- PayU Finance India Pvt. Ltd.

- PagSeguro Digital Ltd.

第七章 市场机会与未来趋势

- 閒置频段与未满足需求评估

The digital lending market was valued at USD 507.27 billion in 2025 and estimated to grow from USD 566.52 billion in 2026 to reach USD 985.03 billion by 2031, at a CAGR of 11.68% during the forecast period (2026-2031).

This growth profile underscores steady gains in technology-mediated credit origination, rising embedded-finance volumes, and wider institutional acceptance of AI underwriting. Real-time credit decisioning, open-banking data transfers, and buy-now-pay-later (BNPL) options continue to draw borrowers away from branch channels. Institutions are investing in cloud-native loan-origination systems that trim processing costs and shrink disbursement times from weeks to minutes. New revenue opportunities have emerged around thin-file customers and cross-border small-business funding, aided by alternative-data credit scoring. Competitive intensity is strengthening as fintechs, traditional banks, and BigTech platforms converge on identical customer segments in every major region.

Global Digital Lending Market Trends and Insights

Surge in smartphone and internet penetration accelerates mobile-first lending

Global smartphone users totaled 6.8 billion in 2024, giving lenders a direct path to borrowers through mobile apps. In Asia-Pacific alone, digital-wallet payments hit USD 9.8 trillion, reinforcing customer readiness for in-app credit offers. Lenders now harness geolocation, device metadata, and behavioural signals to evaluate risk in seconds, opening credit lines to millions of first-time borrowers. Regulators such as India's Data Protection Board and the EU's AI Act are standardizing data use, which helps lenders scale compliant mobile-first models.

Proliferation of fintech instant-approval platforms transforms borrower expectations

More than 90% of digital loan applications are now routed through automated underwriting engines, and Upstart reports 80% instant approvals without document uploads. Machine-learning models digest hundreds of borrower attributes in real time, cutting origination costs and elevating customer satisfaction. Banks unable to match sub-five-minute approval windows increasingly choose white-label partnerships with fintech vendors to preserve market share.

Cyber-security and data-privacy risks challenge platform scalability

Financial institutions allocate just 13% of IT budgets to security even as API footprints widen. In 2024, 62% of surveyed lenders registered rising fraud incidents, and regulators now demand zero-trust architectures under GDPR and CCPA regimes. Higher cyber-insurance premiums and mandatory breach notifications inflate compliance costs, particularly for cross-border platforms.

Other drivers and restraints analyzed in the detailed report include:

- Favorable open-banking and e-KYC regulations enable data-driven underwriting

- MSME demand for rapid working-capital loans drives B2B adoption

- Investor fatigue in peer-to-peer markets curbs capital supply

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Consumer loans retained 60.78% of the digital lending market in 2025, propelled by personal finance and BNPL demand. At the same time, SME facilities are forecast to grow at a 16.08% CAGR to 2031, reflecting working-capital shortages and adoption of alternative-data models that reward real-time cash-flow visibility. The digital lending market size for SME products is projected to reach USD 246.09 billion by 2031. Lenders integrate APIs with accounting software to harvest invoices, payroll, and tax data, reducing underwriting cycles from weeks to 48 hours. As localized platforms achieve credit-loss rates on par with consumer portfolios, global banks are entering revenue-sharing partnerships to secure distribution.

In the consumer arena, embedded credit offers inside e-commerce checkouts continue to extend reach into lower-income cohorts. A growing share of salaried millennials now use pay-period data to unlock salary-advance options. Advanced explainable-AI models mitigate bias, pointing to downward pressure on charge-offs across large peer cohorts. Together, these forces preserve a solid base for consumer-loan volumes while opening an even faster-growing SME lane.

Personal loans represented 35.44% of the digital lending market size in 2025, fueled by instant-decision models and low acquisition costs. Auto loans follow, leveraging point-of-sale integrations that cut dealership desk time to under 60 seconds [UPSTART.COM]. Mortgage, home-equity, and student-loan categories are undergoing slower digital migration due to complex collateral checks and subsidy rules.

Working-capital loans to small businesses are projected to register a 10.52% CAGR. Revenue-based financing aligns repayments with daily card receipts, offering merchants flexibility during demand fluctuations. Invoice-factoring platforms that anchor inside enterprise-resource-planning dashboards unlock liquidity within 24 hours of invoice issuance. This embedded-finance route attracts global logistics, agriculture, and freelancer ecosystems that historically lacked collateral for traditional lines of credit.

The Digital Lending Market Report is Segmented by Type (Consumer, Enterprise/SME), Loan Type (Personal Loans, Auto Loans, and More), Deployment Mode (Cloud-Based, Hybrid and More), Business Model (Peer-To-Peer Marketplace Lending, Balance-Sheet Direct Lending, and More), Technology (AI/ML-driven Underwriting, API and Open-Banking Platforms, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 39.35% of the digital lending market in 2025, supported by more than 235 licensed digital banks and government-backed payment infrastructures such as India's UPI, which averaged 12 billion monthly transactions in 2025. China's super-apps layer credit on top of wallets, ride-hailing, and food-delivery services, creating powerful data loops. Governments in Singapore and Australia operate regulatory sandboxes that shorten product-testing cycles to six months, accelerating market entry for challenger lenders.

Africa recorded the fastest 21.85% CAGR and is forecast to reach USD 47 billion in revenues by 2028. Mobile-money rails pioneered in Kenya and Ghana form the backbone of microlending engines that evaluate airtime purchases and peer-to-peer transfers to score risk. Start-ups in Nigeria and Egypt attract international venture funds and develop cross-border payroll-advance solutions for the African diaspora.

North America and Europe exhibit high penetration but slower headline growth. U.S. BNPL legislation remains fluid, yet PayPal surpassed USD 30 billion in cumulative originations, demonstrating scale for mature players. In Europe, PSD3 upgrades and the EU AI Act provide unified rules that enhance cross-border passporting, though interest-rate caps in several consumer-credit directives restrain high-yield segments. Latin America sees growing embedded-finance deals anchored on real-time payments such as Brazil's PIX, creating a runway for double-digit lending growth despite macro volatility.

- Ant Group Co., Ltd.

- WeBank Co., Ltd.

- PayPal Holdings, Inc.

- Klarna Bank AB (publ)

- LendingClub Corporation

- Upstart Holdings, Inc.

- Funding Circle Holdings plc

- On Deck Capital, Inc.

- Prosper Marketplace, Inc.

- SoFi Technologies, Inc.

- Kabbage, Inc. (American Express Co.)

- LendInvest plc

- Zopa Bank Ltd.

- Kaspi.kz JSC

- Ferratum Oyj

- CAN Capital, Inc.

- International Personal Finance plc

- Faircent Tech Pvt. Ltd.

- LenDenClub Techserve Pvt. Ltd.

- CapFloat Financial Services Pvt. Ltd.

- Oriente Group Limited

- Mercado Libre, Inc.

- Square Loans (Block, Inc.)

- PayU Finance India Pvt. Ltd.

- PagSeguro Digital Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in smartphone and internet penetration

- 4.2.2 Proliferation of fintech instant-approval platforms

- 4.2.3 Favorable open-banking and e-KYC regulations

- 4.2.4 MSME demand for rapid working-capital loans

- 4.2.5 Alternative-data credit scoring for thin-file borrowers

- 4.2.6 Rise of embedded-finance lending inside non-bank apps

- 4.3 Market Restraints

- 4.3.1 Cyber-security and data-privacy risks

- 4.3.2 Regulatory interest-rate caps and platform re-classification

- 4.3.3 Investor fatigue in P2P markets after default spikes

- 4.3.4 Concentration risk on third-party cloud infrastructure

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Consumer

- 5.1.2 Enterprise / SME

- 5.2 By Loan Type

- 5.2.1 Personal Loans

- 5.2.2 Auto Loans

- 5.2.3 Student Loans

- 5.2.4 Mortgage / Home Equity

- 5.2.5 Small Business Working-Capital Loans

- 5.3 By Deployment Mode

- 5.3.1 Cloud-based Platforms

- 5.3.2 On-premise Solutions

- 5.3.3 Hybrid

- 5.4 By Business Model

- 5.4.1 Peer-to-Peer (Marketplace) Lending

- 5.4.2 Balance-Sheet (Direct) Lending

- 5.4.3 Embedded-Finance / BNPL Lending

- 5.4.4 Crowdfunding and Revenue-Based Financing

- 5.5 By Technology

- 5.5.1 AI / Machine-Learning-driven Underwriting

- 5.5.2 API and Open-Banking Platforms

- 5.5.3 Blockchain-based Lending

- 5.5.4 Big-Data Analytics

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 Saudi Arabia

- 5.6.4.1.2 United Arab Emirates

- 5.6.4.1.3 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Egypt

- 5.6.4.2.3 Rest of Africa

- 5.6.4.1 Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Analysis

- 6.2 Strategic Moves (M&A, Partnerships, Launches)

- 6.3 Market Share Analysis (Top-15, 2024)

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Ant Group Co., Ltd.

- 6.4.2 WeBank Co., Ltd.

- 6.4.3 PayPal Holdings, Inc.

- 6.4.4 Klarna Bank AB (publ)

- 6.4.5 LendingClub Corporation

- 6.4.6 Upstart Holdings, Inc.

- 6.4.7 Funding Circle Holdings plc

- 6.4.8 On Deck Capital, Inc.

- 6.4.9 Prosper Marketplace, Inc.

- 6.4.10 SoFi Technologies, Inc.

- 6.4.11 Kabbage, Inc. (American Express Co.)

- 6.4.12 LendInvest plc

- 6.4.13 Zopa Bank Ltd.

- 6.4.14 Kaspi.kz JSC

- 6.4.15 Ferratum Oyj

- 6.4.16 CAN Capital, Inc.

- 6.4.17 International Personal Finance plc

- 6.4.18 Faircent Tech Pvt. Ltd.

- 6.4.19 LenDenClub Techserve Pvt. Ltd.

- 6.4.20 CapFloat Financial Services Pvt. Ltd.

- 6.4.21 Oriente Group Limited

- 6.4.22 Mercado Libre, Inc.

- 6.4.23 Square Loans (Block, Inc.)

- 6.4.24 PayU Finance India Pvt. Ltd.

- 6.4.25 PagSeguro Digital Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-space and Unmet-Need Assessment

2026-2030年全球数位借贷市场

2026-2030年全球数位借贷市场 数位借贷平台市场预测至2032年:按组件、部署模式、贷款类型、应用、最终用户和地区分類的全球分析

数位借贷平台市场预测至2032年:按组件、部署模式、贷款类型、应用、最终用户和地区分類的全球分析 2025年借贷技术(LendTech)全球市场报告2025年全球数位借贷平台市场报告

2025年借贷技术(LendTech)全球市场报告2025年全球数位借贷平台市场报告 数位借贷平台市场规模、份额、趋势及预测(按类型、组件、部署模式、产业垂直领域及地区划分),2025 年至 2033 年

数位借贷平台市场规模、份额、趋势及预测(按类型、组件、部署模式、产业垂直领域及地区划分),2025 年至 2033 年 数位借贷平台市场按组件、类型、利率类型、贷款类型、应用、借款人类型和部署模式划分—2025-2030 年全球预测

数位借贷平台市场按组件、类型、利率类型、贷款类型、应用、借款人类型和部署模式划分—2025-2030 年全球预测 数位借贷平台市场规模、份额、趋势分析报告:按组件、部署、最终用途、地区、细分市场预测,2025 年至 2030 年

数位借贷平台市场规模、份额、趋势分析报告:按组件、部署、最终用途、地区、细分市场预测,2025 年至 2030 年 数位借贷平台市场规模、份额、成长分析(按组成部分、按贷款额金额、按部署模式、按订阅类型、按贷款类型、按地区)-2025 年至 2032 年产业预测

数位借贷平台市场规模、份额、成长分析(按组成部分、按贷款额金额、按部署模式、按订阅类型、按贷款类型、按地区)-2025 年至 2032 年产业预测 全球数位借贷平台市场规模(按产品、部署类型、最终用户、地理位置和预测)

全球数位借贷平台市场规模(按产品、部署类型、最终用户、地理位置和预测) 美国数位借贷:市场占有率分析、行业趋势和成长预测(2025-2030 年)

美国数位借贷:市场占有率分析、行业趋势和成长预测(2025-2030 年)