|

市场调查报告书

商品编码

1940691

乙烯基复合地板材料:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Vinyl Floor Covering - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

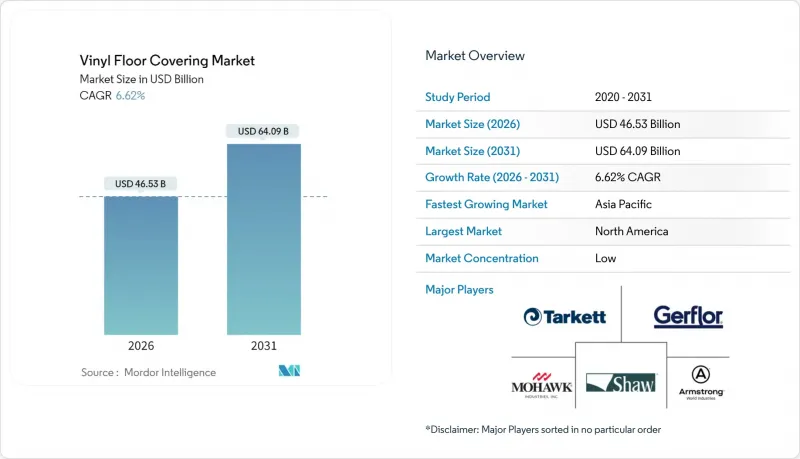

预计乙烯基地板材料市场将从 2025 年的 436.4 亿美元增长到 2026 年的 465.3 亿美元,并预计到 2031 年将达到 640.9 亿美元,2026 年至 2031 年的复合年增长率为 6.62%。

目前市场扩张主要得益于刚性芯材技术,该技术正在取代工程木地板和复合地板,使乙烯基复合地板材料市场免受建设产业波动的影响。循环经济的必要性、低维护成本和成本效益,以及住宅和商业维修需求,都在加速乙烯基复合地板的普及。虽然豪华乙烯基瓷砖(LVT)仍保持主导地位,但豪华乙烯基板材(LVP)在石材复合材料(SPC)和木塑复合材料(WPC)技术进步的推动下,正超越其竞争对手。亚太地区的规模优势、南美洲的成长动能以及北美地区的近岸外包倡议,凸显了全球产能和需求格局的重新调整。

全球PVC地板材料市场趋势与洞察

新兴经济体建筑需求復苏

随着新兴市场建筑业的扩张,各国政府优先考虑经济耐用的解决方案以应对快速的都市化,这推动了PVC地板材料市场的发展。印度的智慧城市计画和巴西的住宅奖励策略正集中资源升级地板材料,优先选择专为承受高人流而设计的SPC和WPC地板。製造商正利用越南的生产能力,凭藉具有竞争力的劳动成本,高效满足东协和拉丁美洲的需求。当地经销商将PVC地板的快速施工特性与紧凑的施工进度结合,以加快计划速度。这些因素共同作用,在原物料价格波动的情况下,提振了基准需求并支撑了价格稳定。

转向耐用性和低维护成本

医疗保健、教育和酒店业的设施管理人员正在拓展乙烯基(PVC)地板材料市场,将其作为瓷砖和木地板的替代品,以提高清洁效率和感染控制。乙烯基地板的无缝表面可抑制微生物滋生,而免胶铺设系统则便于在维护週期内快速更换。製造商正在采用超低挥发性有机化合物(VOC)配方和不含邻苯二甲酸酯的增塑剂,以满足日益严格的室内空气品质标准,同时又不影响其性能。设计师看重这些先进技术带来的高端定位,缩小了乙烯基地板与高级地面材料之间的认知差距。耐用性优势意味着更低的生命週期成本,这更符合注重预算的机构的需求。

PVC树脂和增塑剂价格波动

PVC树脂价格与能源和石脑油价格波动密切相关,对整个PVC地板材料市场带来成本衝击。儘管製造商透过长期合约对冲部分成本,但仍易受亚洲乙烯价格飙升的影响。小型製造商被迫压缩利润率以维持销售量,限制了研发预算和资本投资。全球买家协商的价格有效期限缩短,使大型计划的竞标过程更加复杂。虽然製造商正寻求透过将前端流程整合到回收製程来减少对原生PVC的依赖,但多层LVT的回收仍面临许多技术挑战。

细分市场分析

预计到2025年,豪华乙烯基瓷砖(LVT)将占据乙烯基地板材料市场74.12%的份额,这主要得益于其丰富的款式选择和卓越的耐用性,吸引了众多设施负责人和住宅。 LVT在医疗保健、教育和住宿设施的广泛应用,为其提供了稳定的需求基础,从而支撑了乙烯基地板材料市场的整体规模。同时,豪华乙烯基木地板预计到2031年将以6.79%的复合年增长率增长,这主要得益于其刚性芯材技术提升了尺寸稳定性并增强了木纹的逼真度。压纹精度、雾面饰面和压制倒角技术的进步进一步提升了其美观度,扩大了乙烯基地板在高端装修市场与工业实木地板竞争的潜力。抗菌和耐刮擦涂层的不断改进,也进一步拉大了LVT与陶瓷和强化复合地板产品之间的性能差距。

在预测期内,LVP的卡扣式组装缩短了安装週期,这对于面临劳动力短缺的专业安装人员来说极具吸引力。製造商将利用数位印刷技术减少图案库存,并在PVC价格波动的情况下改善现金流。为此,LVT製造商将推出更厚的耐磨层和整合式底层,用于企业办公室和多用户住宅走廊,旨在保持高人流量场所的市场份额。生物基PVC配方将率先应用于欧洲LVT产品线,以满足生态标章采购法规的要求。整个产品格局正在从低成本与高端的二元对立转变为由核心技术、表面处理和永续性认证定义的频谱。

到2025年,互锁式乙烯基地砖的销售额将占总销售额的56.20%,这反映出市场对可缩短计划施工时间并减少多用户住宅中黏合剂气味的浮动地板的需求日益增长。卡扣式结构提高了对不平整地面的适应性,因此在公寓翻新和办公空间装修中得到广泛应用,因为在这些场所,速度比持久性更为重要。自黏式地砖预计到2031年将以7.02%的复合年增长率成长,目前主要面向对尺寸稳定性要求极高的应用领域,例如机场、超市和工业组装。改良的聚氨酯接着剂和高摩擦背衬降低了翘曲风险,并使维护週期超过10年。

免胶铺装创新技术与互锁式地板相辅相成,其可重新定位的地板条设计,使得迎宾套房能够快速实现租户更换。整合式隔音垫无需额外铺设衬垫即可降低楼层间的噪音传播,这在高层建筑中尤其重要。製造商正投资于机器人加工技术,以实现完美的榫槽公差,从而减少施工现场的废弃物和保固索赔。黏合剂系统还能减少挥发性有机化合物(VOC)的排放,有助于取得LEED认证,并推动绿建筑专案中乙烯基地板材料市场的扩张。总而言之,应用技术正与视觉设计和原料的化学特性一起,成为关键的差异化因素。

区域分析

北美地区将占2025年总收入的36.20%,这主要得益于近岸外包业务,该业务降低了与UFLPA相关的供应风险,并缩短了改造项目的前置作业时间。乔治亚和田纳西州国内製造业产能的扩张,降低了对亚洲进口的依赖,并稳定了大型零售商和商业承包商的库存。同时,预计到2031年,亚太地区的复合年增长率将达到7.90%。随着中国、印度和东南亚的都市化和基础设施项目推动需求成长,越南新兴的製造业基地正利用其成本优势,既满足本地消费需求,也向美国出口产品。

韩国和澳洲可支配收入的成长正推动偏好转向高端硬芯地板,从而推高平均售价。印度的智慧城市计画和住宅政策正在打破传统陶瓷地板材料的垄断地位,直接将市场转向现代化的抗衝击地板材料。区域全面经济伙伴关係协定(RCEP)下的贸易协定正在简化亚洲内部运输,加速产品周转率和市场渗透。同时,加拿大日益严格的挥发性有机化合物(VOC)排放法规正促使消费者转向低排放的乙烯基产品。这些地理趋势凸显了供应链重组和多元化成长要素如何重塑全球乙烯基地板材料市场份额的分布模式。

南美洲的增产主要得益于巴西的「居家生活」住宅计画和智利对教育设施的维修,这两项计画都强调了耐用性和卫生性。货币稳定和资源出口支撑了家庭维修预算,并促进了乙烯基材料的消费。阿根廷的进口限制提振了当地SPC工厂的前景,而秘鲁则依赖北美进口来补充抗震重组材料。南方共同市场(Mercosur)的贸易协定正在简化区域内运输,并促进经销商的整合。随着市场信心的恢復,商业开发商正从花岗岩转向木纹SPC,以缩短工期并减轻结构荷载。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 新兴国家建筑需求的復苏

- 转向耐用、易于维护的地板材料

- 刚性芯材技术(SPC/WPC)的快速普及

- 住宅装修活动激增

- 基于循环经济的乙烯基地板材料回收义务

- 将LVT生产外包至北美和欧盟

- 市场限制

- 聚氯乙烯(PVC)和增塑剂的价格波动

- 人们对室内空气品质和挥发性有机化合物(VOC)排放的担忧

- 中美贸易摩擦和《美国工人自由选择法案》(UFLPA)导致供应链中断

- 多层LVT的报废回收所面临的挑战。

- 产业价值链分析

- 波特五力模型

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 洞察市场最新趋势与创新

- 深入了解市场近期发展动态(新产品发表、策略性倡议、投资、合作、合资、扩张、併购等)

第五章 市场规模与成长预测

- 依产品类型

- 豪华乙烯基瓷砖(LVT)

- 石塑复合材料(SPC)

- 木塑复合材料(WPC)

- 豪华乙烯基木地板(LVP)

- 乙烯基片材

- 其他(VCT,抗衝击乙烯基背衬橡胶混合材料)

- 豪华乙烯基瓷砖(LVT)

- 透过安装方法

- 自黏乙烯基瓷砖

- 黏合剂连接

- 互锁式乙烯基瓷砖

- 其他的

- 最终用户

- 住宅

- 商业的

- 饭店及休閒

- 零售商店和购物中心

- 医疗设施

- 教育

- 总公司

- 公共和政府设施

- 其他商业用户

- 依建筑类型

- 新房产

- 改造/维修

- 透过分销管道

- B2C/零售

- 家居建材商店

- 专业地板商店

- 在线的

- 其他分销管道

- B2B/承包商/建筑商

- B2C/零售

- 按地区

- 北美洲

- 加拿大

- 我们

- 墨西哥

- 南美洲

- 巴西

- 秘鲁

- 智利

- 阿根廷

- 其他南美洲

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 义大利

- 比荷卢经济联盟(比利时、荷兰、卢森堡)

- 北欧国家(丹麦、芬兰、冰岛、挪威、瑞典)

- 其他欧洲地区

- 亚太地区

- 印度

- 中国

- 日本

- 澳洲

- 韩国

- 东南亚

- 亚太其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 奈及利亚

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Mohawk Industries

- Tarkett SA

- Shaw Industries Group

- Armstrong World Industries

- Gerflor Group

- Mannington Mills

- Interface Inc.

- Beaulieu International Group

- Forbo Holding AG

- LG Hausys

- Novalis Innovative Flooring

- Milliken & Company

- Raskin Industries

- Congoleum Corporation

- IVCT(IndoFloor Vinyl Composite Tile)

- Karndean Designflooring

- CFL Flooring

- Responsive Industries

- Polyflor Ltd

- ShawContract

第七章 市场机会与未来展望

The vinyl floor covering market is expected to grow from USD 43.64 billion in 2025 to USD 46.53 billion in 2026 and is forecast to reach USD 64.09 billion by 2031 at 6.62% CAGR over 2026-2031.

Current expansion is propelled by rigid-core technologies that displace engineered wood and laminate, a move that shields the vinyl floor covering market from construction volatility. Adoption accelerates as circular-economy mandates, low-maintenance attributes, and cost efficiencies converge in residential remodeling and commercial retrofits. Luxury Vinyl Tile (LVT) retains leadership, yet Luxury Vinyl Plank (LVP) outpaces peers on the back of stone plastic composite (SPC) and wood plastic composite (WPC) advances. Asia-Pacific's scale advantage, South America's growth momentum, and near-shoring efforts in North America together highlight the global re-allocation of capacity and demand vectors.

Global Vinyl Floor Covering Market Trends and Insights

Construction Rebound in Emerging Economies

Emerging market build-outs expand the vinyl floor covering market as governments prioritize cost-effective, durable solutions for rapid urbanization. India's Smart Cities Mission and Brazil's residential stimulus funnel resources into flooring upgrades that favor SPC and WPC formats for heavy traffic endurance. Manufacturers leverage Vietnam-based capacity to serve ASEAN and Latin American demand efficiently, capitalizing on competitive labor rates. Local distributors pair vinyl's quick installation with constrained construction schedules, accelerating project turnovers. Collectively, these factors raise baseline demand and underpin positive price discipline amid raw-material swings.

Shift Toward Resilient, Low-Maintenance Flooring

Facility managers in healthcare, education, and hospitality sectors elevate cleaning efficiency and infection control, expanding the vinyl floor covering market as an alternative to ceramic tile and wood . Vinyl's seamless surfaces reduce microbial harborage, while loose-lay systems facilitate rapid replacement during maintenance cycles. Producers integrate ultra-low VOC recipes and phthalate-free plasticizers, addressing stricter indoor-air-quality codes without sacrificing performance . Specifiers reward these advances with premium positioning, narrowing the perception gap between vinyl and high-end surfaces. The durability narrative translates into lower lifecycle costs that resonate with budget-sensitive institutions.

Volatility in PVC and Plasticizer Prices

PVC resin tracks energy and naphtha inputs, producing cost shocks that ripple through the vinyl floor covering market. Producers hedge partially with long-term contracts but remain exposed when Asian ethylene values spike . Smaller firms thin margins to preserve volume, limiting R&D budgets and capital investment. Global buyers negotiate shorter price-validity windows, complicating tender processes for large-scale projects. Forward integration into recycling streams aims to lower virgin PVC dependence but faces technical hurdles in multilayer LVT reclamation.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Rigid-Core Technologies (SPC/WPC)

- Surge in Residential Remodeling Activity

- Indoor-Air-Quality & VOC Emission Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Luxury Vinyl Tile commanded 74.12% of the 2025 vinyl floor covering market share as facility planners and homeowners gravitated toward its broad design palette and proven durability. The segment's entrenched position across healthcare, education, and hospitality installations provides stable baseline volume that anchors the overall vinyl floor covering market size. Luxury Vinyl Plank, meanwhile, is projected to grow at a 6.79% CAGR through 2031 as rigid-core technology elevates dimensional stability and wood-look authenticity. Advancements in embossed-in-register textures, matte finishes, and pressed bevels heighten aesthetic realism, enabling vinyl to contest engineered hardwood in premium remodels. Continuous upgrades in antimicrobial and scratch-resistant coatings further widen the performance gap with ceramic and laminate alternatives.

Over the forecast horizon, LVP's click-lock assemblies shorten installation cycles, a feature that appeals to professional contractors juggling labor constraints. Makers capitalize on digital printing to reduce pattern inventory, improving cash flow amid PVC price swings. LVT producers respond with thicker wear layers and integrated underlayment aimed at corporate offices and multifamily corridors, preserving share in heavy-traffic venues. Bio-attributed PVC formulas debut first in European LVT lines to satisfy eco-label procurement rules. Collectively, the product landscape is shifting from a budget-versus-premium dichotomy toward a spectrum defined by core technology, surface finish, and sustainability credentials.

Interlocking vinyl tiles held 56.20% of 2025 revenue, underscoring buyer preference for floating floors that accelerate project timelines and minimize adhesive odors in occupied spaces. Click-lock geometries have grown increasingly tolerant of subfloor irregularities, encouraging adoption in multifamily renovations and office fit-outs where speed outweighs permanence. Glue-down formats, although forecast to climb at a 7.02% CAGR to 2031, now target applications demanding maximum dimensional stability such as airports, grocery aisles, and industrial assembly lines. Enhanced polyurethane adhesives and high-friction backings reduce curl risk, extending lifecycle beyond ten-year maintenance windows.

Loose-lay innovations complement the interlocking segment by offering repositionable planks that facilitate rapid tenant turnovers in hospitality suites. Integrated acoustic pads mitigate floor-to-floor sound transfer without adding separate underlayment, an advantage in high-rise construction. Manufacturers invest in robotic milling to perfect tongue-and-groove tolerances, shrinking on-site waste and warranty claims. Adhesive-free systems also lower VOC emissions, helping projects qualify for LEED credits and propelling the vinyl floor covering market size within green-building programs. Overall, installation technology has emerged as a primary differentiator alongside visual design and raw-material chemistry.

The Vinyl Floor Covering Market is Segmented by Product Type ( Product Type, Luxury Vinyl Plank (LVP), and Other), Installation Method (Self-Adhesive Vinyl Tiles, Glue-Down, and Other), End-User (Residential and Commercial), Construction Type (New Construction and Remodeling / Retrofit), and Distribution Channel(B2C / Retail and B2B / Contractors / Builders ). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 36.20% of 2025 revenue, supported by near-shoring that mitigates UFLPA-related supply risk and shortens lead times for remodel projects. Domestic capacity expansions in Georgia and Tennessee reduce dependency on Asian imports, stabilizing inventory for big-box retailers and commercial contractors. Asia-Pacific, in contrast, is poised for an 7.90% CAGR through 2031 as urbanization and infrastructure programs fuel demand in China, India, and Southeast Asia. Vietnam's burgeoning production hub leverages cost advantages while serving both regional consumption and U.S. re-export flows.

Rising disposable incomes in South Korea and Australia shift consumer preference toward premium rigid-core planks, elevating average selling prices. India's Smart Cities and housing initiatives pivot directly to modern resilient flooring, bypassing legacy ceramic dominance. Trade agreements under RCEP streamline intra-Asia shipments, accelerating product turnover and market penetration. Meanwhile, Canada tightens VOC regulations, nudging buyers toward low-emission vinyl lines. Collectively, the geographic dynamics illustrate how supply-chain realignment and disparate growth drivers reshape the global vinyl floor covering market share distribution.

South America records underpinned by Brazil's Minha Casa Minha Vida housing push and Chilean education upgrades that target durable, hygienic surfaces. Currency stability and commodity exports shore up household renovation budgets, uplifting vinyl consumption. Argentine import restrictions lift prospects for local SPC factories, while Peru leans on North American imports to replenish quake-resilient reconstruction stock. Trade pacts under Mercosur simplify intra-regional shipments, fostering cross-border distributor consolidation. As confidence rebounds, commercial developers shift from granite to wood-look SPC to shorten build schedules and cut structural loads.

- Mohawk Industries

- Tarkett SA

- Shaw Industries Group

- Armstrong World Industries

- Gerflor Group

- Mannington Mills

- Interface Inc.

- Beaulieu International Group

- Forbo Holding AG

- LG Hausys

- Novalis Innovative Flooring

- Milliken & Company

- Raskin Industries

- Congoleum Corporation

- IVCT (IndoFloor Vinyl Composite Tile)

- Karndean Designflooring

- CFL Flooring

- Responsive Industries

- Polyflor Ltd

- ShawContract

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Construction rebound in emerging economies

- 4.2.2 Shift toward resilient, low-maintenance flooring

- 4.2.3 Rapid adoption of rigid-core technologies (SPC/WPC)

- 4.2.4 Surge in residential remodeling activity

- 4.2.5 Circular-economy take-back mandates for vinyl floors

- 4.2.6 Near-shoring of LVT production in North America & EU

- 4.3 Market Restraints

- 4.3.1 Volatility in PVC and plasticizer prices

- 4.3.2 Indoor-air-quality & VOC emission concerns

- 4.3.3 U.S.-China trade & UFLPA supply-chain disruptions

- 4.3.4 End-of-life recycling challenges for multilayer LVT

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Luxury Vinyl Tile (LVT)

- 5.1.1.1 Stone Plastic Composite (SPC)

- 5.1.1.2 Wood Plastic Composite (WPC)

- 5.1.2 Luxury Vinyl Plank (LVP)

- 5.1.3 Sheet Vinyl

- 5.1.4 Others (VCT, Resilient Vinyl-Backed Rubber Hybrid)

- 5.1.1 Luxury Vinyl Tile (LVT)

- 5.2 By Installation Method

- 5.2.1 Self-Adhesive Vinyl Tiles

- 5.2.2 Glue-Down

- 5.2.3 Interlocking Vinyl Tiles

- 5.2.4 Others

- 5.3 By End-User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.2.1 Hospitality & Leisure

- 5.3.2.2 Retail & Shopping Centers

- 5.3.2.3 Healthcare Facilities

- 5.3.2.4 Education

- 5.3.2.5 Corporate Offices

- 5.3.2.6 Public & Government Buildings

- 5.3.2.7 Other Commercial Users

- 5.4 By Construction Type

- 5.4.1 New Construction

- 5.4.2 Remodeling / Retrofit

- 5.5 By Distribution Channel

- 5.5.1 B2C / Retail

- 5.5.1.1 Home Centers

- 5.5.1.2 Specialty Flooring Stores

- 5.5.1.3 Online

- 5.5.1.4 Other Distribution Channels

- 5.5.2 B2B / Contractors / Builders

- 5.5.1 B2C / Retail

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 Canada

- 5.6.1.2 United States

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Peru

- 5.6.2.3 Chile

- 5.6.2.4 Argentina

- 5.6.2.5 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.6.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 India

- 5.6.4.2 China

- 5.6.4.3 Japan

- 5.6.4.4 Australia

- 5.6.4.5 South Korea

- 5.6.4.6 South-East Asia

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East & Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East & Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Mohawk Industries

- 6.4.2 Tarkett SA

- 6.4.3 Shaw Industries Group

- 6.4.4 Armstrong World Industries

- 6.4.5 Gerflor Group

- 6.4.6 Mannington Mills

- 6.4.7 Interface Inc.

- 6.4.8 Beaulieu International Group

- 6.4.9 Forbo Holding AG

- 6.4.10 LG Hausys

- 6.4.11 Novalis Innovative Flooring

- 6.4.12 Milliken & Company

- 6.4.13 Raskin Industries

- 6.4.14 Congoleum Corporation

- 6.4.15 IVCT (IndoFloor Vinyl Composite Tile)

- 6.4.16 Karndean Designflooring

- 6.4.17 CFL Flooring

- 6.4.18 Responsive Industries

- 6.4.19 Polyflor Ltd

- 6.4.20 ShawContract

7 Market Opportunities & Future Outlook

- 7.1 Eco-Friendly Vinyl: Recyclable, Low-VOC, and Sustainable Materials

- 7.2 Luxury Vinyl Tiles (LVT) Surging with Hyper-Realistic Textures

- 7.3 DIY-Friendly Click-Lock and Peel-and-Stick Innovations

2026年全球PVC地板材料市场报告

2026年全球PVC地板材料市场报告 2035年PVC地板材料市场分析及预测:类型、产品类型、应用、技术、安装方式、材质类型、最终用户、功能、解决方案

2035年PVC地板材料市场分析及预测:类型、产品类型、应用、技术、安装方式、材质类型、最终用户、功能、解决方案 美国乙烯基复合地板材料:市场份额分析、产业趋势与统计、成长预测(2026-2031)

美国乙烯基复合地板材料:市场份额分析、产业趋势与统计、成长预测(2026-2031) 日本PVC地板材料市场规模、份额、趋势和预测:按产品类型、行业和地区划分,2026-2034年

日本PVC地板材料市场规模、份额、趋势和预测:按产品类型、行业和地区划分,2026-2034年 2025-2029年全球抗衝击PVC地板材料市场

2025-2029年全球抗衝击PVC地板材料市场 乙烯基复合地板材料市场规模、份额及成长分析(按产品、类型、安装方式、应用、销售管道和地区划分)-2026-2033年产业预测

乙烯基复合地板材料市场规模、份额及成长分析(按产品、类型、安装方式、应用、销售管道和地区划分)-2026-2033年产业预测 乙烯基地板材料市场按产品类型、安装方式、耐磨层厚度、应用和分销管道划分-2025-2032 年全球预测

乙烯基地板材料市场按产品类型、安装方式、耐磨层厚度、应用和分销管道划分-2025-2032 年全球预测 全球乙烯基地板材料市场2025 年至 2033 年乙烯基地板市场规模、份额、趋势及预测(按产品类型、产业和地区)

全球乙烯基地板材料市场2025 年至 2033 年乙烯基地板市场规模、份额、趋势及预测(按产品类型、产业和地区) 乙烯基地板市场-全球产业规模、份额、趋势、机会和预测,细分领域,按产品(乙烯基片材、乙烯基瓷砖、豪华乙烯基瓷砖)、按应用(住宅、商业)、按地区、按竞争,2020-2030 年预测

乙烯基地板市场-全球产业规模、份额、趋势、机会和预测,细分领域,按产品(乙烯基片材、乙烯基瓷砖、豪华乙烯基瓷砖)、按应用(住宅、商业)、按地区、按竞争,2020-2030 年预测