|

市场调查报告书

商品编码

1940746

美国退休市场:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)United States Senior Living - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

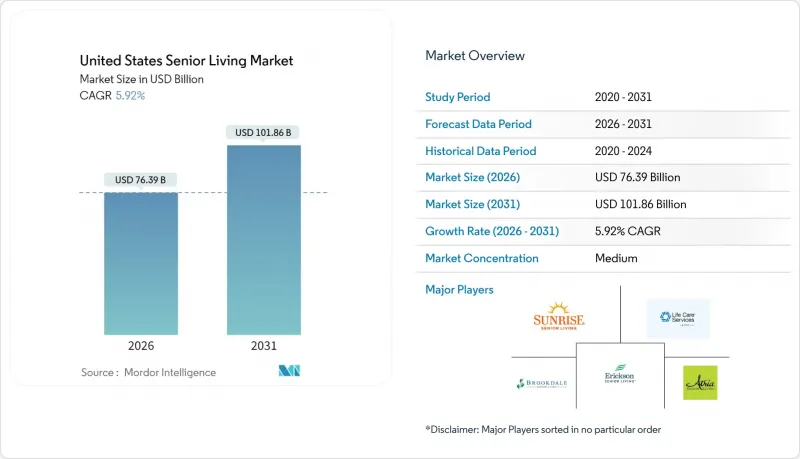

据估计,到 2026 年,美国养老市场价值将达到 763.9 亿美元,高于 2025 年的 721.1 亿美元。

预计到 2031 年将达到 1,018.6 亿美元,2026 年至 2031 年的复合年增长率为 5.92%。

人口老化带来的持续需求、有限的新增供应以及高额资本流入共同赋予营运商定价权,从而支撑了入住率的稳定成长。医疗保健服务的整合进一步巩固了竞争优势,因为整合了基层医疗和復健服务的社区可以获得更高的利润率、延长入住时间并减少转院次数。租金的柔软性使营运商能够快速适应不断上涨的工资和监管成本,即使在劳动力短缺的压力下也能维持营运利润率。机构投资者,尤其是医疗保健房地产投资信託基金(REITs),正透过合资企业和售后回租等方式维持开发平臺,在高利率环境下推动产业整合。从电子健康记录到预测分析等技术的应用,进一步改善了居住者的健康状况并提高了成本效益。

美国养老市场趋势与洞察

婴儿潮世代老化推动各级照护需求持续成长

到2033年,约6,900万婴儿潮世代几乎全部将年满70岁或以上,这将大大扩大美国养老市场的潜在居民群体。这一代人拥有较高的住宅拥有率和净资产,这让他们有能力自费支付养老费用;同时,他们对科技的广泛接受也提高了他们对数位化照护的接受度。预计到2040年,85岁及以上人口(他们最有可能需要专业护理和失智症护理)将翻一番,从而确保对先进医疗保健服务的需求。德克萨斯州和佛罗里达州等拥有优惠税收政策和宜居环境的州,预计将迎来尤为强劲的成长。那些能够优化设施、支付方案和行销,以吸引这个富裕且精通科技的群体的养老机构,将有机会获得终身价值。 Green Street估计,超过40%的老年人无需出售资产即可负担养老费用,这表明市场存在巨大的潜在需求。

资本市场和医疗保健房地产投资信託基金(REIT)的活性化支持发展和整合。

医疗保健房地产投资信託基金(REITs)正将创纪录的资金投入美国退休房地产。 Ventas在2024年管理了20亿美元的资产后,将其2025年的投资目标提高至15亿美元,这表明其对该行业基本面的长期信心。 Welltower以32亿美元收购Amica Senior Lifestyles,凸显了REITs为确保优质投资组合而进行的交易规模。债务资本仍充裕,Walker & Dunlop在2024年安排了一笔6亿美元的养老地产贷款。来自Fortress等私募股权巨头的竞争推高了估值,并促使养老地产营运品质得到提升。高流动性支持了供不应求的大都市地区的新建设,并为当地业主运营商提供了退出途径,加速了整个生态系统的整合和专业化进程。

人手不足和工资上涨给利润率和服务水准带来了压力。

几乎所有层级的护理机构都面临严重的员工短缺问题,迫使各机构提高时薪、扩大福利范围,并更加依赖临时工。美国医疗保险和医疗补助服务中心 (CMS) 规定每位居民每天至少需要 3.48 小时的护理时间,这项规定也波及到辅助住宅和独立生活设施,因为这些机构都在争夺合格的护理人员。目前,只有 6% 的护理机构能够满足 24 小时註册护理师的要求,这引发了全行业的竞标战,并挤压了利润空间。内华达州推动将护士时薪从 16 美元提高到 20 美元,凸显了通膨压力。联邦贸易委员会 (FTC) 提议禁止竞业禁止条款,这可能会进一步加剧离职率,并损害照护的连续性。农村地区的护理机构面临最大的挑战,有时不得不限制入院人数以维持规定的员工与居民比例。

细分市场分析

截至2025年,养老院将占美国老年生活市场的40.62%,并在2031年之前以6.29%的复合年增长率保持最高增长。需求成长的动力来自患有多种慢性疾病的居民,他们更倾向于在持续照顾环境中安享晚年,而不是转入医院。虽然辅助住宅仍然是主要的入门选择,但营运商正在维修记忆护理和亚急性护理服务区,以留住居民并创造价值。独立生活社区则专注于为重视自主性的年轻老年人提供生活方式设施、健身中心、厨师精心烹调的膳食和文化活动。记忆护理单元的日趋成熟,配备了以安全为中心的布局和接受过失智症培训的工作人员,这标誌着养老模式正在转变,在满足老年人高级医疗需求的同时,也保持着居住环境。持续照顾老年社区虽然仍属于小众市场,但在寻求透过合约获得多层次护理服务的富裕老年人中越来越受欢迎。

长期照护服务的优势正推动着对临床人员培训、负压病房和中心内治疗室的资本投资。营运商正在实施电子处方笺管理系统和智慧电梯,以提高安全性和效率。日益严重的健康问题促使营运商与保险公司合作,以降低再入院率,从而为美国退休市场增加由支付方主导的收入来源。然而,监管机构对人员配备比例、感染控制和补偿合理性等方面的审查依然严格,这需要完善的合规措施。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场洞察与趋势

- 市场概览

- 市场驱动因素

- 婴儿潮世代的老化正在推动对自主型、辅助生活和失智症照护设施的持续需求。

- 雄厚的资本市场和活跃的医疗保健房地产投资信託基金(REITs)支持开发和整合。

- 透过转向综合护理模式(基层医疗、復健、失智症护理)来增强价值提案

- 在许多大都会圈,透过出售住宅和退休储蓄金来累积财富,使得私人资金购买住宅变得更加可行。

- 透过科技应用(远端监控、电子健康记录、跌倒检测)提高护理品质和效率

- 市场限制

- 劳动力短缺和工资上涨正给利润率和服务水准带来压力。

- 各州繁杂的法规增加了合规成本和周转时间。

- 某些大都会地区缺乏经济适用房,运转率恢復不均衡。

- 价值/供应链分析

- 政策和法律规范(州指导方针、许可、奖励)

- 对正在进行和即将开展的计划的见解

- 对数位化和技术支援措施(远端医疗、智慧型设备)的见解

- 对经营模式和营运商演变的洞察

- 对投资和资金筹措趋势的洞察

- 对永续性和设计创新的洞察

- 波特五力模型

- 供应商的议价能力

- 买方和消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按属性类型

- 老年人照护住宅

- 独立生活

- 记忆护理

- 护理机构

- 按经营模式

- 完全所有权出售(永久产权)

- 长期租赁/出租

- 混合模式(销售+租赁)

- 按年龄

- 55至64岁

- 65至74岁

- 75至85岁

- 85岁或以上

- 按州

- 德克萨斯州

- 加州

- 佛罗里达

- 纽约

- 伊利诺州

- 美国其他州

第六章 竞争情势

- 市场集中度

- 策略趋势

- 公司简介

- Brookdale Senior Living Inc.

- Atria Senior Living Inc.

- LCS(Life Care Services)

- Erickson Senior Living

- Sunrise Senior Living

- Five Star Senior Living

- Holiday by Atria

- Kisco Senior Living

- Sonida Senior Living

- Watermark Retirement Communities

- Silverado Senior Living

- Trilogy Health Services

- Benchmark Senior Living

- Ensign Group Inc.

- Ventas Inc.

- Welltower Inc.

- Capital Senior Living(Grace Management)

- Pegasus Senior Living

- Frontier Management

- Merrill Gardens

第七章 市场机会与未来展望

United States senior living market size in 2026 is estimated at USD 76.39 billion, growing from 2025 value of USD 72.11 billion with 2031 projections showing USD 101.86 billion, growing at 5.92% CAGR over 2026-2031.

Continued demand from an aging population, constrained new-build supply, and sophisticated capital inflows combine to create pricing power for operators while supporting steady occupancy gains. Healthcare integration deepens competitive moats because communities that embed primary care and rehabilitation services capture higher margins, lift length of stay, and reduce hospital transfers. Rental pricing flexibility lets operators respond quickly to wage inflation and regulatory costs, helping to maintain operating margins despite labor pressures. Institutional investors, especially healthcare REITs, sustain development pipelines through joint ventures and sale-leasebacks, fueling consolidation even as interest rates remain elevated. Technology adoption, from electronic health records to predictive analytics, further enhances resident outcomes and cost efficiency.

United States Senior Living Market Trends and Insights

Aging Baby-Boomer Cohort Driving Sustained Demand Across Care Levels

Nearly all 69 million baby boomers will be 70 or older by 2033, dramatically enlarging the resident pool for the United States senior living market. Higher home ownership and net worth among this cohort underpin private-pay affordability, while broader acceptance of technology raises comfort with digitally enabled care. The 85-plus population, most likely to require skilled nursing and memory care, is set to double by 2040, guaranteeing demand for high-acuity services. States attracting retirees through favorable taxes and climate, such as Texas and Florida, will see especially strong growth. Operators that tailor amenities, payment plans, and marketing to this wealthier, tech-savvy generation are positioned to capture lifetime value. Green Street estimates show more than 40% of seniors can pay for senior housing without liquidating assets, indicating significant latent demand.

Deep Capital Markets and Active Healthcare REITs Supporting Development and Consolidation

Healthcare REITs are pouring record funds into United States senior living market assets. Ventas lifted its 2025 investment target to USD 1.5 billion after deploying USD 2 billion in 2024, signaling long-term conviction in sector fundamentals. Welltower's USD 3.2 billion acquisition of Amica Senior Lifestyles illustrates the scale REITs will transact to secure premier portfolios. Debt capital remains abundant, with Walker & Dunlop arranging USD 600 million in seniors-housing loans during 2024. Private equity heavyweights such as Fortress add further competition for assets, driving valuations and spurring operational upgrades. Strong liquidity supports new builds in undersupplied metros and offers exit paths for regional owner-operators, accelerating consolidation and professionalization across the ecosystem.

Labor Shortages and Wage Inflation Pressuring Margins and Service Levels

Severe staffing shortages plague virtually every care level, forcing communities to raise hourly wages, expand benefits, and rely heavily on agency labor. New CMS nursing-home staffing rules requiring 3.48 nursing hours per resident per day ripple into assisted and independent living through competition for licensed nurses. Only 6% of nursing homes currently meet the 24/7 RN mandate, driving cross-sector bidding wars that compress margins. Caregiver wage campaigns, such as Nevada's push from USD 16 to USD 20 per hour, spotlight inflationary pressures. The FTC's pending ban on non-compete clauses may further elevate turnover, undermining continuity of care. Operators in rural areas confront the steepest hurdles, sometimes restricting admissions to maintain mandated staff-resident ratios.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Healthcare-Integrated Models Enhancing Value Proposition and Resident Outcomes

- Home-Sale Equity and Retirement Savings Enabling Private-Pay Affordability

- State-by-State Regulatory Complexity Increasing Compliance Costs and Development Timelines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Nursing care facilities controlled 40.62% of the United States senior living market size in 2025 and will post the quickest 6.29% CAGR through 2031. Demand stems from residents with multiple chronic conditions who prefer aging in place within a continuum-of-care setting instead of hospital transfers. Assisted-living remains the mainstream entry point, yet operators retrofit wings for memory-care or sub-acute services to retain residents and capture value. Independent-living communities focus on lifestyle amenities, fitness centers, chef-led dining, and cultural programs, geared toward younger seniors who prize autonomy. The maturation of memory-care units, complete with secured layouts and dementia-trained staff, illustrates the sector's pivot to higher acuity while preserving residential ambience. Continuing-care retirement communities, though niche, gain traction among affluent seniors desiring contractual access to multiple care levels.

Nursing-care dominance compels capital investment in clinical staff training, negative-pressure rooms, and on-site therapy suites. Operators deploy electronic medication-administration records and smart lifts to boost safety and efficiency. Rising acuity also attracts insurer partnerships seeking reduced readmissions, adding payer-driven revenue to the United States senior living market. However, regulatory scrutiny on staffing ratios, infection control, and reimbursement adequacy remains intense, requiring sophisticated compliance infrastructures.

The United States Senior Living Market Report is Segmented by Property Type (Assisted Living, Independent Living, Memory Care, Nursing Care), by Business Model (Outright Sale (Freehold), Long-Lease / Rental, Hybrid (Sale + Lease)), by Age (55 To 64 Years, 65 To 74 Years, and More), and by States (Texas, California, Florida, New York, Illinois, Rest of US). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Brookdale Senior Living Inc.

- Atria Senior Living Inc.

- LCS (Life Care Services)

- Erickson Senior Living

- Sunrise Senior Living

- Five Star Senior Living

- Holiday by Atria

- Kisco Senior Living

- Sonida Senior Living

- Watermark Retirement Communities

- Silverado Senior Living

- Trilogy Health Services

- Benchmark Senior Living

- Ensign Group Inc.

- Ventas Inc.

- Welltower Inc.

- Capital Senior Living (Grace Management)

- Pegasus Senior Living

- Frontier Management

- Merrill Gardens

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Insights and dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging baby-boomer cohort driving sustained demand across independent, assisted, and memory care

- 4.2.2 Deep capital markets and active healthcare REITs supporting development and consolidation

- 4.2.3 Shift to healthcare-integrated models (primary care, rehab, memory care) enhancing value proposition

- 4.2.4 Home-sale equity and retirement savings enabling private-pay affordability in many metros

- 4.2.5 Technology adoption (remote monitoring, EHRs, fall detection) elevating care quality and efficiency

- 4.3 Market Restraints

- 4.3.1 Labor shortages and wage inflation pressuring margins and service levels

- 4.3.2 State-by-state regulatory complexity increasing compliance costs and timelines

- 4.3.3 Affordability gaps and uneven occupancy recovery in certain secondary markets

- 4.4 Value / Supply-Chain Analysis

- 4.5 Policy & Regulatory Framework (state guidelines, licensing, incentives)

- 4.6 Insight on Upcoming and Ongoing Projects

- 4.7 Insights on Digital & Tech Enablers (telemedicine, smart amenities)

- 4.8 Insights on Business Model & Operator Evolution

- 4.9 Insights on Investment & Financing Trends

- 4.10 Insights Sustainability & Design Innovation

- 4.11 Porter's Five Forces

- 4.11.1 Bargaining Power of Suppliers

- 4.11.2 Bargaining Power of Buyers/Consumers

- 4.11.3 Threat of New Entrants

- 4.11.4 Threat of Substitutes

- 4.11.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Property Type

- 5.1.1 Assisted Living

- 5.1.2 Independent Living

- 5.1.3 Memory Care

- 5.1.4 Nursing Care

- 5.2 By Business Model

- 5.2.1 Outright Sale (Freehold)

- 5.2.2 Long-Lease / Rental

- 5.2.3 Hybrid (Sale + Lease)

- 5.3 By Age

- 5.3.1 55 to 64 years

- 5.3.2 65 to 74 years

- 5.3.3 75 to 85 years

- 5.3.4 Above 85 years

- 5.4 By States

- 5.4.1 Texas

- 5.4.2 California

- 5.4.3 Florida

- 5.4.4 New York

- 5.4.5 Illinois

- 5.4.6 Rest of US

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.3.1 Brookdale Senior Living Inc.

- 6.3.2 Atria Senior Living Inc.

- 6.3.3 LCS (Life Care Services)

- 6.3.4 Erickson Senior Living

- 6.3.5 Sunrise Senior Living

- 6.3.6 Five Star Senior Living

- 6.3.7 Holiday by Atria

- 6.3.8 Kisco Senior Living

- 6.3.9 Sonida Senior Living

- 6.3.10 Watermark Retirement Communities

- 6.3.11 Silverado Senior Living

- 6.3.12 Trilogy Health Services

- 6.3.13 Benchmark Senior Living

- 6.3.14 Ensign Group Inc.

- 6.3.15 Ventas Inc.

- 6.3.16 Welltower Inc.

- 6.3.17 Capital Senior Living (Grace Management)

- 6.3.18 Pegasus Senior Living

- 6.3.19 Frontier Management

- 6.3.20 Merrill Gardens

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

环保生活市场:按组件、技术、最终用户、部署模式、连接类型、应用和分销管道划分-2026-2032年全球预测

环保生活市场:按组件、技术、最终用户、部署模式、连接类型、应用和分销管道划分-2026-2032年全球预测 美国老年住宅市场:市场规模、份额和趋势分析(按设施和地区划分),细分市场预测(2026-2033 年)

美国老年住宅市场:市场规模、份额和趋势分析(按设施和地区划分),细分市场预测(2026-2033 年) 全球环保生活(AAL)市场规模、份额、趋势和成长分析报告(2026-2034)

全球环保生活(AAL)市场规模、份额、趋势和成长分析报告(2026-2034) 环境生活协助市场-全球产业规模、份额、趋势、机会、预测:按服务、技术、应用、地区和竞争对手划分,2021-2031年

环境生活协助市场-全球产业规模、份额、趋势、机会、预测:按服务、技术、应用、地区和竞争对手划分,2021-2031年 印度居住市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)养老住房市场规模、份额和趋势分析报告:按设施、地区和细分市场预测(2025-2033 年)

印度居住市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)养老住房市场规模、份额和趋势分析报告:按设施、地区和细分市场预测(2025-2033 年) 全球无障碍智慧家庭解决方案市场:预测至 2032 年—按组件、无障碍类型、技术、分销管道、应用、最终用户和地区进行分析

全球无障碍智慧家庭解决方案市场:预测至 2032 年—按组件、无障碍类型、技术、分销管道、应用、最终用户和地区进行分析 2025年全球辅助生活科技市场报告

2025年全球辅助生活科技市场报告 全球环境生活辅助市场

全球环境生活辅助市场 环境辅助生活市场,按产品、按技术、按感测器、按服务、按国家和地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测

环境辅助生活市场,按产品、按技术、按感测器、按服务、按国家和地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测