|

市场调查报告书

商品编码

1940801

社群媒体聆听:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Social Media Listening - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

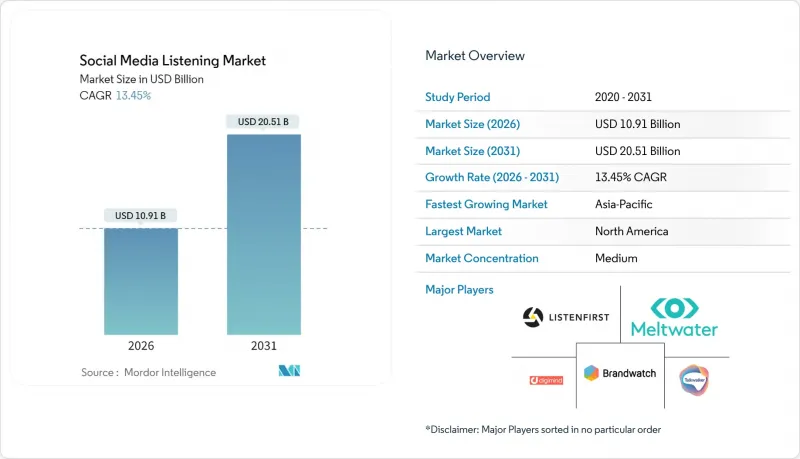

预计到 2025 年,社群媒体监听市场价值将达到 96.2 亿美元,到 2031 年将达到 205.1 亿美元,高于 2026 年的 109.1 亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 13.45%。

这一上升趋势主要源自于企业转向主动互动,依赖于社交平臺上捕捉到的早期情绪讯号。北美地区保持主导地位,这得益于几起备受瞩目的危机事件后,人们对品牌安全的日益关注。同时,亚太地区成长最快,这主要得益于在地化平台的扩张和智慧型手机普及率的加速提升。儘管软体仍然是核心投资领域,但随着企业需要客製化的工作流程和人工智慧模型的训练,对专业服务的需求也在不断增长。虽然文本分析仍然占据主导地位,但随着短影片在许多网络上的传播量超过文本,影片分析的规模正在迅速扩大。

全球社群媒体聆听市场趋势与洞察

在主导的危机中降低品牌风险

随着网红争议造成的经济损失日益加剧,即时社群媒体情报已成为企业风险管理团队的必备工具。拥有成熟监听系统的品牌,其征兆侦测与反应速度比仅依赖传统监控方式的品牌快4.3倍,进而显着降低损失。企业风险管理仪錶板整合了运作警报系统,使公关、法务和顾客关怀部门能够协调快速回应。这种迫切性在面向消费者的产业尤为突出,因为一则病毒式传播的贴文就可能毁掉数月累积的品牌价值。这种策略转变促使各大平台增加了对危机应变模组的预算投入。能够提供预测评分和自动化工作流程的供应商正成为风险规避型负责人的首选。

生成式人工智慧情感分析提升亚太地区零售业投资报酬率

大规模语言模型 (LLM) 正在重新定义情绪分析的准确性,尤其是在那些因语码转换和俚语而难以进行传统自然语言处理 (NLP) 的市场中。 GPT-4 在二元情绪分析任务中达到了 93% 的准确率,从而能够跨多语言地区提供高度精准的洞察。亚太地区的零售商正在迅速利用这项进步来优化促销活动和产品改进。跨境经销商尤其受惠于 LLM 无需额外分析师团队即可处理多种亚洲语言的能力。澳洲保健品製造商 Blackmores 利用以微信为中心的监测来识别消费者日益增长的担忧,并调整通讯,从而帮助其扩大了在中国的市场份额。这项投资报酬率高的成功案例正在加速那些注重低利润、高销售量的电商企业采用 LLM 技术。

资料隐私监管碎片化

各地隐私法规的差异迫使供应商应对区域性的特定退出机制、删除权和资料居住义务。 《加州消费者隐私法案》(CCPA) 带来了营运负担,要求对敏感资讯进行精细化的消费者控制和独特的流程管理。小型供应商难以资金筹措持续的法规更新费用,随着合规成本的上升,产业整合也正在加速。企业买家通常会部署独立的区域实例,这削弱了全球整合控制面板的价值,并降低了投资报酬率预期。

细分市场分析

至2025年,软体将占据社群媒体监听市场67.20%的份额,巩固其作为企业社交智慧核心基础的地位。负责人倾向于选择整合监听、互动和分析功能,并将洞察结果直接与宣传活动管理工具对接的套件。为此,供应商正在整合API层,以连接客户资料平台和商业智慧仓库,从而支援更广泛的数位体验策略。这种商品搭售的趋势能够保障授权收入,即使基础监控功能日趋普及。

业务收益虽然规模较小,但正以16.02%的复合年增长率增长,因为企业越来越将社交智能视为一种以结果为导向的能力,而非即插即用的工具集。服务提供者现在提供危机模拟、竞争情报作战室以及针对特定产业术语的大型语言模型 (LLM) 客製化调优服务。缺乏全天候服务的中型企业更青睐託管服务,而人工智慧调优合约则在需要领域安全模型的受监管行业中开闢了一片天地。这种双轨成长使得纯粹的社群媒体监听服务供应商和混合型服务供应商都能在社群媒体监听市场保持竞争力。

到2025年,大型企业将占总支出的64.10%,因为它们正将监听结果整合到CRM、产品和合规系统的资料湖架构中。多品牌集团利用可视化区域情绪波动的仪錶板来协调反驳论点和拓展宣传活动。此外,随着资讯长们优先考虑简化的合约和提供ISO认证安全框架的供应商,企业采购週期正在推动整合。

然而,中小企业是成长最快的细分市场,年复合成长率(CAGR)高达 15.35%。云端定价、基于模板的部署和互动式使用者介面正在降低准入门槛。经合组织的一项调查预测,中小企业采用人工智慧工具的比例将从 2024 年的 26% 上升到 2025 年的 39%,这反映了数位化的加速。将社群媒体「对话」策略与客户评价结合的小规模出口企业表示,客户获取效率得到了提升,验证了这项投资的价值。供应商正以捆绑式免费加值产品瞄准这一细分市场,当需要更深入的分析或多用户访问时,这些产品会过渡到付费计划。

区域分析

北美地区预计到2025年将维持41.20%的收入份额,这得益于其技术成熟度和在近期危机后加强的严格品牌保护策略。金融服务和医疗保健公司正在将社交资料整合到受监管的申诉处理系统中,以遵守诸如《加州消费者隐私法案》(CCPA)等赋予消费者广泛资料权利的法规。持续的投资重点在于高精度风险检测模组,以在贴文病毒式传播之前保护品牌价值。

亚太地区预计到2031年将以16.02%的复合年增长率成长,这主要得益于平台普及率的飙升和行动商务的强势地位。中国封闭式的网路环境要求供应商对语言模型和API连接器进行精细化调整。一些品牌,例如微信上的Blackmores,已经成功应对了这种复杂性,并实现了市场份额的快速成长。在印度市场,智慧型手机的普及以及区域语言社交网路的兴起,使得多语言支援成为必然之选。东南亚市场用户参与度很高,但需要能够适应不同方言的自然语言处理技术,这推动了对服务合作伙伴的需求。

在欧洲,GDPR带来的负担与机会之间的平衡正在推动隐私保护分析领域的创新。媒体预算向社群影片的转移,带动了对多模态声量份额(SOV)仪錶板的需求。拉丁美洲和中东及非洲地区虽然面积不大,但充满活力,其成长主要集中在都市区中心和寻求衡量当地民意指标的跨国公司。海湾国家政府正在加速采用社群媒体监听技术来追踪大众对服务品质的看法,从而扩大了公共部门对社群媒体监听市场的需求。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 危机期间以网红为主导的品牌风险缓解策略(北美)

- 生成式人工智慧情感分类提升亚太地区零售业投资报酬率

- 欧洲电视广告支出向社群影片的转移正在推动对SOV分析的需求。

- 银行、金融和保险 (BFSI) 行业申诉的监管回应时间要求

- 游戏和直播的爆炸式增长正在创造丰富的影片和音讯资料集。

- 开放API行销技术生态系统推动平台集成

- 市场限制

- 资料隐私法规碎片化(GDPR、CCPA、PDPA)

- 低资源语言中多语言人工智慧的准确率差距

- X(Twitter)和 Meta 提高了 API 存取费用

- 由于与内部BI/CDP重复采购,导致采购疲劳。

- 技术展望

- 监理展望

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 宏观经济因素评估

第五章 市场规模与成长预测

- 按组件

- 软体

- 服务

- 按组织规模

- 大公司

- 中小企业

- 按分析类型

- 文字分析

- 影像分析

- 影片分析

- 语音/音讯分析

- 透过使用

- 品牌健康追踪

- 客户经验管理

- 竞争标竿分析

- 潜在客户开发和销售监控

- 宣传活动管理

- 危机管理

- 按行业

- 零售与电子商务

- BFSI

- 资讯科技和电信

- 媒体与娱乐

- 医疗保健和生命科学

- 旅游与饭店

- 教育

- 其他(政府机构、非政府组织)

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 东南亚

- 澳洲和纽西兰

- 亚太其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东

- 海湾合作委员会国家

- 土耳其

- 以色列

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 肯亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Meltwater

- Sprinklr

- Brandwatch(Cision LLC)

- NetBase Quid

- Talkwalker

- Digimind

- Khoros

- Clarabridge(Qualtrics)

- Mention

- Hootsuite Inc.

- Agorapulse

- Awario

- Zignal Labs

- ListenFirst

- Synthesio(Ipsos)

- Reputology

- Linkfluence

- Socialbakers(Astute)

- Keyhole Inc.

- Brand24

- Vendor Positioning Matrix

第七章 市场机会与未来展望

The social media listening market was valued at USD 9.62 billion in 2025 and estimated to grow from USD 10.91 billion in 2026 to reach USD 20.51 billion by 2031, at a CAGR of 13.45% during the forecast period (2026-2031).

The uptrend stems from enterprises shifting toward proactive engagement that relies on early sentiment signals captured on social platforms. North America retains leadership, aided by heightened brand-safety concerns following several high-profile crises, while Asia-Pacific records the steepest growth as localized platforms expand and smartphone adoption accelerates. Software remains the core investment category, although demand for expert services is climbing because firms need tailored workflows and AI model training. Text analytics still dominates, but video analytics is scaling quickly as short-form video overtakes text on many networks.

Global Social Media Listening Market Trends and Insights

Brand-risk Mitigation Amid Influencer-led Crises

Escalating financial fallout from influencer controversies is making real-time social intelligence indispensable for corporate risk teams. Brands with mature listening setups now detect brewing issues and respond 4.3 times faster than peers relying only on traditional monitoring, sharply limiting damage. Always-on alerts are being plugged into enterprise risk dashboards so PR, legal, and customer-care units can coordinate rapid remediation. Consumer-facing sectors feel the greatest urgency because a single viral post can erase months of equity building. The strategic shift elevates budget allocation for crisis-specific modules inside leading platforms. Vendors that embed predictive scoring and automated workflows gain preference among risk-averse buyers.

Generative-AI Sentiment Classification Boosting APAC Retail ROI

Large language models are rewriting sentiment analysis accuracy in markets where code-switching and slang frustrated legacy NLP. GPT-4 attains 93% precision on binary sentiment tasks, unlocking high-fidelity insights for multilingual regions. Retailers in Asia-Pacific quickly exploit the advance to fine-tune promotions and product tweaks. Cross-border sellers gain particular leverage because LLMs handle multiple Asian languages without separate analyst teams. Australian supplement maker Blackmores used WeChat-centric monitoring to spot rising consumer concerns and recast messaging, contributing to share gains in China. The ROI narrative accelerates adoption among e-commerce brands mindful of razor-thin margins.

Fragmented Data-Privacy Regimes

Divergent privacy statutes force vendors to juggle opt-outs, deletion rights, and data-residency mandates that vary by region. The California Consumer Privacy Act exemplifies the operational burden, requiring granular consumer controls and unique workflows for sensitive information. Smaller suppliers struggle to fund continuous rule updates, accelerating consolidation as compliance costs escalate. Enterprise buyers often deploy separate regional instances, diluting the value of unified global dashboards and dampening ROI expectations.

Other drivers and restraints analyzed in the detailed report include:

- Shift of TV Ad Spend to Social Video in Europe Raises SOV Analytics Demand

- Regulatory Response-Time Mandates for BFSI Complaints

- Multilingual AI Accuracy Gaps for Low-Resource Languages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for a 67.20% share of the social media listening market in 2025, cementing its role as the backbone of enterprise social intelligence stacks. Buyers prefer integrated suites that merge listening, engagement, and analytics so that insights flow directly into campaign orchestration tools. Platform vendors respond by embedding API layers that connect to customer data platforms and BI warehouses, supporting broader digital-experience strategies. The bundling trend protects license revenue even as basic monitoring commoditizes.

Services revenue, though smaller, is advancing at 16.02% CAGR because firms increasingly view social intelligence as an outcome-driven function rather than a plug-and-play toolset. Providers now offer crisis simulations, competitive war-rooms, and bespoke LLM fine-tuning that map to sector-specific jargon. Managed services resonate with mid-market brands lacking 24/7 coverage, while AI-tuning engagements carve a niche among regulated sectors that need domain-safe models. The dual-track growth keeps both pure-play and hybrid vendors relevant in the social media listening market.

Large enterprises commanded 64.10% of 2025 spending because they integrate listening outputs into data-lake architectures that span CRM, product, and compliance systems. Multi-brand conglomerates rely on dashboards that surface sentiment spikes per region, enabling coordinated rebuttal or campaign amplification. Enterprise buying cycles also drive consolidation as CIOs favor vendors offering contractual simplicity and ISO-certified security frameworks.

SMEs, however, represent the fastest-growing cohort with a projected 15.35% CAGR. Cloud pricing tiers, template-based onboarding, and conversational UI lower entry barriers. OECD research shows that 39% of SMEs used AI tools in 2025, up from 26% in 2024, mirroring broader digital acceleration. Small exporters pairing listening with social "talking" tactics report sharper customer gains, validating investment. Vendors target this segment with bundled freemium offerings that graduate to paid tiers once analytic depth and multiseat access become essential.

The Social Media Listening Market Report is Segmented by Component (Software, and Services), Organization Size (Large Enterprises, Small and Medium-Sized Enterprises), Analytics Type (Text Analytics, Image Analytics, and More), Application (Brand Health Tracking, Crisis Management, and More), Industry Vertical (Retail and E-Commerce, BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained a 41.20% revenue lead in 2025, supported by technology maturity and stringent brand-protection postures following recent crises. Financial-services and healthcare firms integrate social data into regulated complaint systems to comply with statutes like the California Consumer Privacy Act, which grants consumers sweeping data rights. Ongoing investment focuses on high-precision risk detection modules that shield brand equity before posts trend.

Asia-Pacific is forecast to grow at 16.02% CAGR to 2031, propelled by soaring platform penetration and the dominance of mobile commerce. China's walled-garden networks oblige vendors to fine-tune language models and API connectors; brands that master this complexity, such as Blackmores on WeChat, unlock rapid share gains. India's rise combines smartphone affordability with regional-language social networks that demand multilingual coverage. Southeast Asian markets present high engagement but require dialect-adaptive NLP, keeping service partners busy.

Europe balances opportunity with heavy GDPR compliance overhead, spurring innovation in privacy-preserving analytics. The pivot of media budgets toward social video intensifies demand for multimodal share-of-voice dashboards. Latin America, the Middle East, and Africa are smaller yet dynamic, with growth centered in urban hubs and among multinationals that need regional sentiment gauges. Gulf governments increasingly adopt listening to track public opinion on service quality, expanding public-sector demand in the social media listening market.

- Meltwater

- Sprinklr

- Brandwatch (Cision LLC)

- NetBase Quid

- Talkwalker

- Digimind

- Khoros

- Clarabridge (Qualtrics)

- Mention

- Hootsuite Inc.

- Agorapulse

- Awario

- Zignal Labs

- ListenFirst

- Synthesio (Ipsos)

- Reputology

- Linkfluence

- Socialbakers (Astute)

- Keyhole Inc.

- Brand24

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Brand-risk mitigation amid influencer-led crises (North America)

- 4.2.2 Generative-AI sentiment classification boosting APAC retail ROI

- 4.2.3 Shift of TV ad spend to social video in Europe raises SOV analytics demand

- 4.2.4 Regulatory response-time mandates for BFSI complaints

- 4.2.5 Gaming and livestreaming surge generating rich video/audio data sets

- 4.2.6 Open-API martech ecosystems driving platform consolidation

- 4.3 Market Restraints

- 4.3.1 Fragmented data-privacy regimes (GDPR, CCPA, PDPA)

- 4.3.2 Multilingual AI accuracy gaps for low-resource languages

- 4.3.3 API access fee hikes from X (Twitter) and Meta

- 4.3.4 Overlap with in-house BI/CDP causing procurement fatigue

- 4.4 Technological Outlook

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Assessment of Macroeconomic Factors

5 Market Size and Growth Forecasts (Value)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium-sized Enterprises (SMEs)

- 5.3 By Analytics Type

- 5.3.1 Text Analytics

- 5.3.2 Image Analytics

- 5.3.3 Video Analytics

- 5.3.4 Voice/Audio Analytics

- 5.4 By Application

- 5.4.1 Brand Health Tracking

- 5.4.2 Customer Experience Management

- 5.4.3 Competitive Benchmarking

- 5.4.4 Lead Generation and Sales Monitoring

- 5.4.5 Campaign Management

- 5.4.6 Crisis Management

- 5.5 By Industry Vertical

- 5.5.1 Retail and E-commerce

- 5.5.2 BFSI

- 5.5.3 IT and Telecom

- 5.5.4 Media and Entertainment

- 5.5.5 Healthcare and Life Sciences

- 5.5.6 Travel and Hospitality

- 5.5.7 Education

- 5.5.8 Others (Government, NGOs)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Nordics

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Southeast Asia

- 5.6.3.6 Australia and New Zealand

- 5.6.3.7 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East

- 5.6.5.1 GCC Countries

- 5.6.5.2 Turkey

- 5.6.5.3 Israel

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Kenya

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Meltwater

- 6.4.2 Sprinklr

- 6.4.3 Brandwatch (Cision LLC)

- 6.4.4 NetBase Quid

- 6.4.5 Talkwalker

- 6.4.6 Digimind

- 6.4.7 Khoros

- 6.4.8 Clarabridge (Qualtrics)

- 6.4.9 Mention

- 6.4.10 Hootsuite Inc.

- 6.4.11 Agorapulse

- 6.4.12 Awario

- 6.4.13 Zignal Labs

- 6.4.14 ListenFirst

- 6.4.15 Synthesio (Ipsos)

- 6.4.16 Reputology

- 6.4.17 Linkfluence

- 6.4.18 Socialbakers (Astute)

- 6.4.19 Keyhole Inc.

- 6.4.20 Brand24

- 6.5 Vendor Positioning Matrix

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment