|

市场调查报告书

商品编码

1940890

5G基地台市场占有率分析、产业趋势与统计、成长预测(2026-2031年)5G Base Station - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

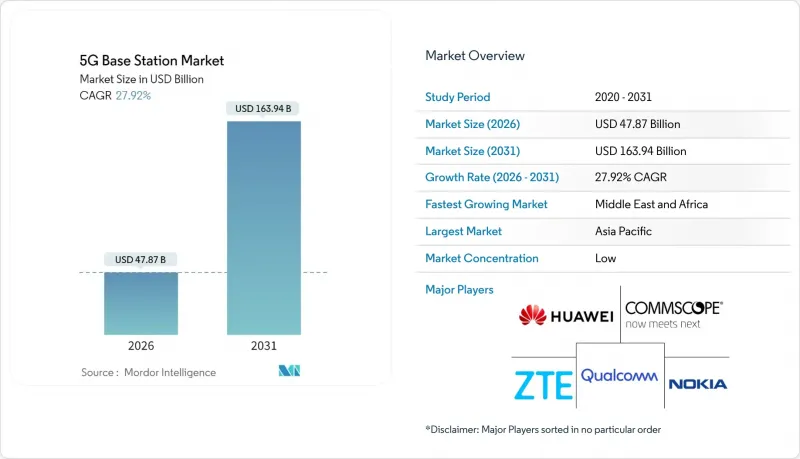

2025年,5G基地台市场价值为374.4亿美元,预计到2031年将达到1,639.4亿美元,而2026年为478.7亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 27.92%。

强劲成长的驱动因素包括:各国政府将频谱竞标转化为基础设施奖励策略;营运商升级至开放式无线存取网(Open-RAN);以及企业寻求为自动化和公共系统提供超可靠、低延迟的连线。中国目前已拥有超过440万个运作站点,而美国和欧洲主要市场则强调开放式架构,以降低供应商风险并促进创新。近期半导体短缺促使供应链多元化,推动供应商增设区域製造地并采用氮化镓功率放大器,从而将站点电力成本降低高达50%。智慧工厂、港口和智慧城市走廊对专用网路的需求,进一步加速了小型基地台、大规模MIMO无线电和毫米波节点的密集化部署。

全球5G基地台市场趋势与洞察

政府频谱竞标和基础设施奖励策略

世界各国政府正将频谱销售作为政策工具,以扩大网路覆盖范围并促进本地製造业发展。美国根据《基础设施投资和就业创造法案》拨款424.5亿美元,用于促进农村宽频建设,并在尚未覆盖的地区部署5G网路。印度推出的120亿美元生产挂钩补贴计画鼓励无线电设备和天线的国内生产,从而缩短供应链并加速农村地区的部署。完善的竞标机制和补贴计画为营运商提供可预测的现金流,从而实现多年投资週期,并刺激大型基地台和小型基地台层面的5G基地台市场发展。

现有设备的开放式无线存取网升级週期

开放式无线接取网路(Open RAN)将无线设备、基频和软体解耦,使通讯业者能够整合各领域的领先供应商,降低采购成本并实现自动更新。沃达丰承诺在2027年将其在英国的2600个站点迁移到Open RAN,目标是降低30%的成本并实现供应商多元化。德国电信正在德国和波兰扩大多供应商试验,以提高柔软性并促进本土创新。儘管系统整合仍然复杂,但早期商业化带来的效能展示正在影响未来网路密集化阶段的采购标准,从而推动5G基地台市场的发展。

高额资本投入和较长的投资回收期

通讯业者面临数十亿美元的部署成本,其投资回收期也比上一代网路更长。 Verizon每年在5G无线电设备和光纤回程传输的支出超过100亿美元,预计投资回收期为7-10年,而LTE的投资回收期约为5年。农村地区的计划获利能力更低,迫使营运商将重点放在人口稠密的都市区,除非有补贴弥补获利能力差距。融资紧张正在减缓全国范围内的网路覆盖速度,并限制低收入国家5G基地台市场的扩张。

细分市场分析

到2025年,大型基地台将占据5G基地台市场60.62%的份额(226.9亿美元),提供广域覆盖和移动锚点服务。然而,小型基地台预计将以28.85%的复合年增长率成长,到2031年,其在5G基地台市场的份额将达到736亿美元。通讯业者正在部署数千个街边节点,以缓解体育场、交通走廊和企业园区等场所的广域基地台拥塞。光是Verizon一家就已安装了超过5万个低功率单元,用于消除室内讯号盲点并实现对称Gigabit速度。

虽然许可审批和场地限制曾经阻碍了小型基地台的扩张,但联邦通讯委员会的放鬆管制已将地方政府的审批时间从数月缩短至不到60天。对专用网路的需求也在增长,小型基地台提供专用的本地覆盖,无需依赖公共频谱。像Crown Castle这样的垂直资产所有者报告称,室内合约签署量实现了三位数的成长,这证实了网路密集化正在推动全球5G基地台市场的发展。

至2025年,非独立组网部署占总部署份额的57.95%,通讯业者利用其现有的LTE核心网路实现快速服务上线。然而,独立组网市场规模将维持快速成长,年复合成长率达29.35%,到2031年将占5G基地台市场总量的60%以上。 AT&T已为需要确定性延迟的工业客户运作独立组网切片,而T-Mobile则已扩展其在全国范围内的独立组网覆盖范围,以提供差异化的性能水平。

独立架构能够实现非独立架构无法实现的功能,例如网路切片、分散式边缘运算和进阶加密。 DISH Network 避开了传统基础设施,建立了一个完全云端原生的网络,从而降低了营运成本并实现了快速的功能发布週期。虽然核心网路迁移增加了复杂性和技能要求,但通讯业者认识到其带来的长期收入成长潜力,并正在加快相容无线电设备和核心网路软体的订单。

区域分析

到2025年,亚太地区将占据41.10%的市场份额,这主要得益于中国440万个运作站点以及到2025年实现近乎全国覆盖的5G网路。日本和韩国在采用独立网路和边缘运算方面已取得早期进展,并已将网路切片商业化应用于製造业和媒体服务。印度2024年的频谱竞标吸引了来自Bharti Airtel和Reliance Jio的大量资金,计划于2025年在23个城市启动第一阶段的5G网路部署,并计划于2027年扩展到遍远地区。台湾和韩国的半导体产业丛集正在为5G基地台提供零件供应,从而增强该地区在全球5G基地台市场的影响力。

北美在规模上略显落后,但在毫米波创新方面却处于主导。 Verizon 已在 26 个州运作了Gigabit固定无线接入服务,而 AT&T 则专注于面向云端和边缘工作负载的企业专用蜂窝业务。在加拿大,频谱竞标正在为农村地区的网路扩张提供资金,而开放接入漫游政策也进一步推动了对基地台的需求。儘管县市层级的监管差异在某些地区减缓了审批速度,但奖励策略资金和铁塔公司签订的建设租赁协议帮助北美在 5G基地台市场保持了稳健的贡献。

中东和非洲地区成长最快,复合年增长率达29.55%。沙乌地阿拉伯的「2030愿景」数位计画正在资助全国范围内的5G部署,并将利雅德打造成为阿拉伯语内容传送的技术中心。阿拉伯联合大公国已在其人口稠密地区97%的区域部署了5G网络,目前正在进行5G高级服务的试验。在非洲,肯亚和奈及利亚优先考虑无线而非光纤,以促进宽频和金融科技的普及,但汇率风险和能源成本推高了计划预算。因此,多边银行和供应商融资机制在实现非洲大陆的5G愿景中发挥越来越重要的作用。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 行动数据流量和智慧型手机普及率的成长

- 5G 具有更低的延迟和更高的频宽优势。

- 政府频谱竞标和基础设施奖励策略

- 现有设备的开放式无线存取网升级週期

- 为工业专用5G部署小型毫米波基地台

- 节能型氮化镓功率放大器可降低全厂营运成本。

- 市场限制

- 高额资本投入和较长的投资回收期

- 频谱碎片化和监管延迟

- 射频前端元件供应瓶颈

- 永续性措施推高了场地成本。

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 竞争对手之间的竞争

- 替代品的威胁

- 投资分析

第五章 市场规模与成长预测

- 按类型

- 小型基地台

- 大型基地台

- 建筑设计

- 独立版 (SA)

- 非独立式(NSA)

- 按频段

- 6GHz 以下频段

- 毫米波频段(24-40 GHz)

- 按额定输出

- 10瓦或以下

- 10-40 W

- 40瓦或以上

- MIMO技术

- 传统MIMO

- 大规模 MIMO(64T64R 或更高)

- 最终用户

- 商业行动通讯业者

- 住宅/消费者 FWA

- 工业专用网络

- 政府/国防

- 智慧城市与公共

- 其他最终用户

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 南美洲其他地区

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 印尼

- 泰国

- 马来西亚

- 越南

- 菲律宾

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 以色列

- 卡达

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 肯亚

- 埃及

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Huawei Technologies Co. Ltd

- ZTE Corporation

- Nokia Corporation

- Telefonaktiebolaget LM Ericsson

- Samsung Electronics Co. Ltd

- CommScope Holding Company Inc.

- Qualcomm Incorporated

- Qorvo Inc.

- Alpha Networks Inc.

- NEC Corporation

- Fujitsu Ltd

- Airspan Networks Holdings Inc.

- Mavenir Systems Inc.

- Parallel Wireless Inc.

- Baicells Technologies Co. Ltd

- JMA Wireless

- Comba Telecom Systems Holdings

- Sercomm Corp.

- ACE Technologies Corp.

- NEC Platforms, Ltd.

第七章 市场机会与未来展望

The 5G Base Station Market was valued at USD 37.44 billion in 2025 and estimated to grow from USD 47.87 billion in 2026 to reach USD 163.94 billion by 2031, at a CAGR of 27.92% during the forecast period (2026-2031).

Robust growth stems from governments turning spectrum auctions into infrastructure stimulus, operators upgrading to Open-RAN, and enterprises seeking ultra-reliable low-latency connections for automation and public-safety systems. China already operates more than 4.4 million live sites, while the United States and key European markets emphasize open architectures to cut vendor risk and spur innovation. Supply-chain diversification has become urgent after recent semiconductor shortages, pushing vendors to add regional manufacturing and gallium-nitride power amplifiers that lower energy bills by up to 50% at each site. Demand for private networks in smart factories, ports, and smart-city corridors further accelerates densification with small cells, massive-MIMO radios, and millimeter-wave nodes.

Global 5G Base Station Market Trends and Insights

Government Spectrum Auctions and Infrastructure Stimulus

Governments are turning spectrum sales into policy tools that expand coverage and local manufacturing. The United States allocated USD 42.45 billion under the Infrastructure Investment and Jobs Act, targeting rural broadband and 5G build-outs in underserved counties. India's USD 12 billion Production-Linked Incentive scheme rewards domestic production of radios and antennas, shortening supply chains and accelerating rural rollouts. Stable auction roadmaps and subsidy programs give operators cash-flow visibility that unlocks multi-year investment cycles and lifts the 5G base station market across both macro and small-cell layers.

Open-RAN Driven Brown-Field Upgrade Cycle

Open-RAN disaggregates radios, baseband, and software so carriers can blend best-of-breed vendors, slash procurement cost, and automate updates. Vodafone committed to swapping 2,600 United Kingdom sites to Open-RAN by 2027, targeting 30% cost savings and broader supplier diversity. Deutsche Telekom is extending multivendor trials across Germany and Poland to raise flexibility and spur domestic innovation. Although system integration remains complex, early commercial launches validate performance and are influencing procurement criteria for upcoming densification waves, boosting the 5G base station market.

High CAPEX and Long ROI Horizon

Operators face multi-billion-dollar rollouts with longer payback than prior network generations. Verizon disclosed spending above USD 10 billion per year on 5G radios and fiber backhaul and estimates a seven-to-ten-year return window versus about five years for LTE. Rural projects are even less economical, forcing carriers to focus on dense urban clusters unless subsidies cover viability gaps. The stretched cash cycle tempers the pace of nationwide coverage and limits 5G base station market expansion in lower-income countries.

Other drivers and restraints analyzed in the detailed report include:

- mmWave Small-Cell Roll-Outs for Private Industrial 5G

- Energy-Efficient GaN Power Amplifiers Cutting Total Site OPEX

- RF-Front-End Component Supply Bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Macro cells represented USD 22.69 billion and 60.62% of the 2025 5G base station market share, providing umbrella coverage and mobility anchor services. Yet small cells are forecast to expand at a 28.85% CAGR, pushing their slice of the 5G base station market size toward USD 73.6 billion by 2031. Carriers deploy thousands of street-level nodes to relieve macro congestion in sports venues, transit corridors, and enterprise campuses. Verizon alone installed more than 50,000 low-power units that fill indoor dead zones and enable symmetrical gigabit rates.

Permitting challenges and aesthetic restrictions once hampered small-cell scaling, but streamlined Federal Communications Commission rulings shortened municipal review from several months to under 60 days. Private networks further lift demand because small cells create dedicated on-premises coverage without relying on public spectrum. Vertical asset owners such as Crown Castle now report triple-digit growth in signed indoor contracts, underscoring how densification underpins the global 5G base station market.

Non-standalone deployments still held 57.95% share in 2025 as operators leveraged existing LTE cores for quick service launches. However the standalone cohort is maintaining a steep 29.35% CAGR, and its share of the 5G base station market size will exceed 60% by 2031. ATandT activated standalone slices for industrial clients needing deterministic latency, while T-Mobile extended nationwide standalone coverage that enables differentiated performance tiers.

Standalone architecture unlocks network slicing, distributed edge computing, and advanced encryption that non-standalone cannot deliver. Dish Network avoided legacy anchors and built an entirely cloud-native network, demonstrating lower operating expenses and rapid feature release cycles. Although core migration raises complexity and skills requirements, operators recognize the long-term revenue upside, accelerating orders for compatible radios and core software.

The 5G Base Station Market Report is Segmented by Type (Small Cell, Macro Cell), Architecture (Stand-Alone SA, Non-Stand-Alone NSA), Frequency Band (Sub-6 GHz, Mmwave 24-40 GHz), Power Rating (<=10 W, 10-40 W, >=40 W), MIMO Technology (Conventional MIMO, Massive MIMO >=64T64R), End User (Commercial Mobile Operators, Residential/Consumer FWA, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 41.10% share in 2025 thanks to China's 4.4 million live sites and a national mandate for near-universal coverage by 2025. Japan and South Korea moved early into standalone and edge-computing deployments, commercializing network slicing for manufacturing and media services. India's 2024 spectrum auctions unlocked capital from Bharti Airtel and Reliance Jio, with first-wave deployments in twenty-three cities during 2025 and rural extensions scheduled by 2027. Local semiconductor clusters in Taiwan and South Korea anchor component supply, reinforcing the region's influence on the global 5G base station market.

North America trails only marginally in volume and leads on millimeter-wave innovation. Verizon activated gigabit fixed wireless access in twenty-six states, while ATandT concentrates on enterprise private-cellular projects for cloud and edge workloads. Canada's auctions raised funding for rural expansion and mandated open-access roaming, stimulating incremental base-station demand. Regulatory patchwork at county and city levels slows permitting in some corridors, yet stimulus funds and tower-company build-leases sustain a healthy North American contribution to the 5G base station market.

The Middle-East and Africa region is the fastest-growing at 29.55% CAGR. Saudi Arabia's Vision 2030 digital blueprint finances nationwide 5G and positions Riyadh as a tech-hub for Arabic content delivery. The United Arab Emirates rolled out 5G across 97% of populated areas and now trials 5G-Advanced services. In Africa, Kenya and Nigeria favor wireless over fiber for broadband and fintech inclusion, but currency risk and energy cost inflate project budgets. Multilateral banks and vendor-financing schemes thus play a bigger role in realizing the continent's 5G aspirations.

- Huawei Technologies Co. Ltd

- ZTE Corporation

- Nokia Corporation

- Telefonaktiebolaget LM Ericsson

- Samsung Electronics Co. Ltd

- CommScope Holding Company Inc.

- Qualcomm Incorporated

- Qorvo Inc.

- Alpha Networks Inc.

- NEC Corporation

- Fujitsu Ltd

- Airspan Networks Holdings Inc.

- Mavenir Systems Inc.

- Parallel Wireless Inc.

- Baicells Technologies Co. Ltd

- JMA Wireless

- Comba Telecom Systems Holdings

- Sercomm Corp.

- ACE Technologies Corp.

- NEC Platforms, Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising mobile data traffic and smartphone penetration

- 4.2.2 Superior latency and bandwidth advantages of 5G

- 4.2.3 Government spectrum auctions and infrastructure stimulus

- 4.2.4 Open-RAN driven brown-field upgrade cycle

- 4.2.5 mmWave small-cell roll-outs for private industrial 5G

- 4.2.6 Energy-efficient GaN PAs cutting total site OPEX

- 4.3 Market Restraints

- 4.3.1 High CAPEX and long ROI horizon

- 4.3.2 Spectrum fragmentation and regulatory delays

- 4.3.3 RF-front-end component supply bottlenecks

- 4.3.4 Sustainability compliance inflating site costs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitutes

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Small Cell

- 5.1.2 Macro Cell

- 5.2 By Architecture

- 5.2.1 Stand-Alone (SA)

- 5.2.2 Non-Stand-Alone (NSA)

- 5.3 By Frequency Band

- 5.3.1 Sub-6 GHz

- 5.3.2 mmWave (24-40 GHz)

- 5.4 By Power Rating

- 5.4.1 Less than or equal to 10 W

- 5.4.2 10-40 W

- 5.4.3 More than or equal to 40 W

- 5.5 By MIMO Technology

- 5.5.1 Conventional MIMO

- 5.5.2 Massive MIMO (More than 64T64R)

- 5.6 By End User

- 5.6.1 Commercial Mobile Operators

- 5.6.2 Residential/Consumer FWA

- 5.6.3 Industrial Private Networks

- 5.6.4 Government and Defense

- 5.6.5 Smart Cities and Public Safety

- 5.6.6 Other End Users

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Chile

- 5.7.2.4 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 United Kingdom

- 5.7.3.2 Germany

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 Australia

- 5.7.4.6 Indonesia

- 5.7.4.7 Thailand

- 5.7.4.8 Malaysia

- 5.7.4.9 Vietnam

- 5.7.4.10 Philippines

- 5.7.4.11 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 Saudi Arabia

- 5.7.5.1.2 United Arab Emirates

- 5.7.5.1.3 Turkey

- 5.7.5.1.4 Israel

- 5.7.5.1.5 Qatar

- 5.7.5.1.6 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Nigeria

- 5.7.5.2.3 Kenya

- 5.7.5.2.4 Egypt

- 5.7.5.2.5 Rest of Africa

- 5.7.5.1 Middle East

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Huawei Technologies Co. Ltd

- 6.4.2 ZTE Corporation

- 6.4.3 Nokia Corporation

- 6.4.4 Telefonaktiebolaget LM Ericsson

- 6.4.5 Samsung Electronics Co. Ltd

- 6.4.6 CommScope Holding Company Inc.

- 6.4.7 Qualcomm Incorporated

- 6.4.8 Qorvo Inc.

- 6.4.9 Alpha Networks Inc.

- 6.4.10 NEC Corporation

- 6.4.11 Fujitsu Ltd

- 6.4.12 Airspan Networks Holdings Inc.

- 6.4.13 Mavenir Systems Inc.

- 6.4.14 Parallel Wireless Inc.

- 6.4.15 Baicells Technologies Co. Ltd

- 6.4.16 JMA Wireless

- 6.4.17 Comba Telecom Systems Holdings

- 6.4.18 Sercomm Corp.

- 6.4.19 ACE Technologies Corp.

- 6.4.20 NEC Platforms, Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026年5G基地台全球市场报告

2026年5G基地台全球市场报告 5G基地台市场-全球产业规模、份额、趋势、机会与预测:按类型、网路架构、核心网、工作频率、最终用户、地区和竞争格局划分,2021-2031年

5G基地台市场-全球产业规模、份额、趋势、机会与预测:按类型、网路架构、核心网、工作频率、最终用户、地区和竞争格局划分,2021-2031年 5G基地台市场规模、份额和成长分析(按类型、组件、网路架构、运作频率和地区划分)-产业预测(2026-2033年)

5G基地台市场规模、份额和成长分析(按类型、组件、网路架构、运作频率和地区划分)-产业预测(2026-2033年) 5G 基地台市场,按组件、类型、核心网路技术、频段、最终用户、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

5G 基地台市场,按组件、类型、核心网路技术、频段、最终用户、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测 5G基地台市场规模、份额、趋势分析报告:按类型、组件、网路架构、核心网路、运作频率、最终用途、地区、细分市场预测,2024-2030年

5G基地台市场规模、份额、趋势分析报告:按类型、组件、网路架构、核心网路、运作频率、最终用途、地区、细分市场预测,2024-2030年 2030 年 5G基地台市场预测:按类型、组件、部署模式、频段、网路架构、最终用户和地区进行的全球分析5G基地台市场报告:2030年趋势、预测与竞争分析

2030 年 5G基地台市场预测:按类型、组件、部署模式、频段、网路架构、最终用户和地区进行的全球分析5G基地台市场报告:2030年趋势、预测与竞争分析 2030 年亚太地区 5G 基地台市场预测 - 区域分析 - 按组件、频段、小区类型和最终用户

2030 年亚太地区 5G 基地台市场预测 - 区域分析 - 按组件、频段、小区类型和最终用户 北美 5G 基地台市场预测至 2030 年 - 区域分析 - 按组件、频段、小区类型和最终用户

北美 5G 基地台市场预测至 2030 年 - 区域分析 - 按组件、频段、小区类型和最终用户 欧洲 5G 基地台市场预测至 2030 年 - 区域分析 - 按组件、频段、小区类型和最终用户

欧洲 5G 基地台市场预测至 2030 年 - 区域分析 - 按组件、频段、小区类型和最终用户