|

市场调查报告书

商品编码

1940894

西班牙医药物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Spain Pharmaceutical Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

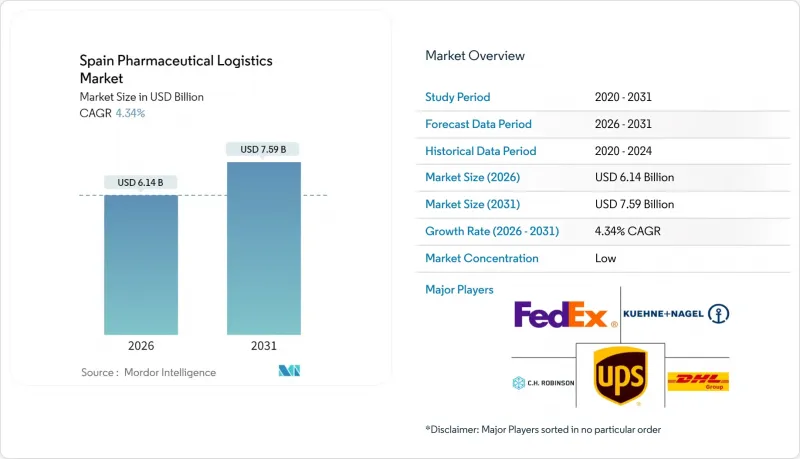

预计到 2026 年,西班牙医药物流市场规模将达到 61.4 亿美元。

预计该产业规模将从 2025 年的 58.8 亿美元成长到 2031 年的 75.9 亿美元,2026 年至 2031 年的复合年增长率为 4.34%。

西班牙强大的公路、港口和机场基础设施使其成为通往南欧的门户,缩短了对温度敏感的药品的前置作业时间,并推动了对端到端可视性工具的需求。沿着地中海和大西洋走廊分布的物流园区加速了跨境药品流向法国和义大利的进程,鑑于80%的欧洲药品需要温控,这一点至关重要。有关GDP认证的监管改革强化了品质标准,并有利于拥有自动化监控系统的营运商。随着全球领导企业向西班牙物流能力投资数十亿欧元,竞争日益激烈,加速了技术应用并推动了产业整合。

西班牙医药物流市场趋势与洞察

国内药品销售量增加

西班牙国内药品销售额超过230亿欧元(250亿美元),支撑着超过26万个就业岗位,并为物流业成长奠定了坚实的基础。 1,340亿欧元(1,430亿美元)的公共医疗支出为西班牙药品物流市场创造了稳定的需求。人均药品支出477欧元(510美元),高于欧洲平均水平,进一步巩固了销售量的稳定性。然而,2024年药品短缺率激增41%,影响到4983种产品,暴露了补货週期中的脆弱性。 2024年1月,947种产品缺货,凸显了预测性库存管理工具的必要性,以减少对医疗服务造成的连锁干扰。

人口老化和慢性病发病率上升将推动最后一公里配送需求。

长期人口预测显示,到2074年,65岁及以上人口的比例将大幅增加。慢性病发生率的上升正促使处方药的配送模式转向定时送处方笺上门,这增加了西班牙药品物流市场「最后一公里」配送的复杂性。数位健康平台整合了远端医疗和药房网络,对心血管和糖尿病药物的定时配送提出了更高的要求。主导的学名药的兴起,在提高药品可负担性的同时也提高了配送频率。 PharmaMar的个人化癌症治疗方法需要针对特定病患、可追溯的低温运输运输,从医院药局一直延伸到居家医疗机构。

司机短缺和劳动成本飙升

低温运输业者占伊比利半岛食品GDP的2.5%,但严重的司机短缺导致人事费用飙升。 DHL已推出一项20亿欧元(约20.8亿美元)的医疗保健物流计划,优先推进自动化,以应对劳动力短缺问题。 UPS的目标是到2026年将其医疗保健收入翻一番,达到200亿美元,并致力于透过机器人技术和配送路线优化软体来提高生产力。儘管有资金注入,即时短缺的现状限制了运力,而此时流感疫苗的需求正处于高峰期,这阻碍了西班牙医药物流市场的扩张。

细分市场分析

截至2025年,运输业占西班牙医药物流市场的59.30%。这主要得益于连接巴塞隆纳、瓦伦西亚和阿尔赫西拉斯港口的15,825公里高速公路网。这项核心基础设施透过Logista和DHL营运的网络,将药品分销至欧洲20万个销售点。儘管道路运输凭藉其次日达能力仍是主要运输方式,但空运(经由赫罗纳和萨拉戈萨机场)也在不断扩张,以满足生物製药的迫切需求。为实现排放目标,托运人正越来越多地转向海铁联运走廊;据西班牙生物製品协会(SEBA)称,冷藏海运航线可减少70%的排放。预计到2031年,附加价值服务和其他细分市场将以4.66%的复合年增长率增长,因为GDP文件、配套包装和后期定制将成为标准合约条款。 FedEx 于 2025 年获得 CEIV 製药企业认证,并赢得价值 4 亿美元的医疗保健合同,这完美地诠释了合规卓越如何带来商业性成果。

随着西班牙医院扩大外包业务,西班牙医药物流市场的附加价值服务和其他细分领域预计将会成长。运输方式正转向配备物联网感测器的温控货柜,这些货柜产生的资料流可透过预测路线检验服务来实现货币化。 UPS整合Frigo-Trans和BPL后,扩大了其在欧洲2-8°C的运输覆盖范围,为西班牙医药出口商提供涵盖陆运、海运和空运的单一发票解决方案。永续性也是推动因素之一,CEVA旗下FORPLANET品牌的电动卡车服务于马德里的诊所,预计到2024年将减少2.6万吨的排放。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 国内药品销售量增加

- 人口老化和慢性病发病率上升将推动最后一公里配送需求。

- 生物製药和温度敏感疗法的扩张

- 欧盟假药指令序列化截止日期生效

- RRF支援的低温运输基础设施投资

- 医院网路向外包供应模式转型

- 市场限制

- 司机短缺和劳动成本上升

- 在极端气候变化期间确保端到端的温度控制

- 冷库房地产所有权结构分散

- 能源成本上涨正在影响冷藏仓库的利润率。

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 地缘政治和疫情对市场的影响

第五章 市场规模与成长预测

- 按服务类型

- 运输

- 公路货运

- 空运

- 海上运输

- 铁路货运

- 仓储

- 附加价值服务及更多

- 运输

- 按操作模式

- 低温运输物流

- 非低温运输物流

- 依产品类型

- 处方药

- 非处方药

- 生物製药和生物相似药

- 疫苗和血液製品

- 临床试验材料

- 细胞和基因治疗

- 医疗设备与诊断

- 动物用药品

- 其他的

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- DHL Supply Chain Spain

- FedEx Express

- Kuehne+Nagel SA

- United Parcel Service(UPS)

- CH Robinson

- CEVA Logistics

- DSV

- Movianto

- Eurotranspharma

- Primafrio

- Cencora

- Yusen Logistics(Part of NYK Line)

- Scan Global Logistics

- Rhenus Logistics

- Geodis

- TIBA

- Logista Pharma

- Noatum Logistics

- Ibercondor

- Logisber

第七章 市场机会与未来展望

The Spain Pharmaceutical Logistics Market size in 2026 is estimated at USD 6.14 billion, growing from 2025 value of USD 5.88 billion with 2031 projections showing USD 7.59 billion, growing at 4.34% CAGR over 2026-2031.

Robust motorway, port, and airport capacity positions Spain as a Southern European gateway that reduces lead times for temperature-sensitive medicines and heightens demand for end-to-end visibility tools. Logistic parks clustered along the Mediterranean and Atlantic corridors speed cross-border flows into France and Italy, which is critical as 80% of European medicines now require temperature control. Regulatory reforms around GDP certification tighten quality thresholds and reward operators with automated monitoring systems. Competitive intensity is rising because global leaders are injecting billions into Spanish capacity, accelerating technology adoption, and sparking consolidation.

Spain Pharmaceutical Logistics Market Trends and Insights

Rising Domestic Pharmaceutical Sales Volume

Annual domestic drug revenue exceeds EUR 23 billion (USD 25 billion) and supports more than 260,000 jobs, which strengthens the baseline for logistics growth. Public health spending at EUR 134 billion (USD 143 billion) creates dependable demand across the Spanish pharmaceutical logistics market. Per-capita medicine outlays at EUR 477 (USD 510) surpass European averages, reinforcing volume stability. Yet drug shortages jumped 41% in 2024, with 4,983 items affected, exposing vulnerabilities in replenishment cycles. January 2024 recorded 947 unavailable products, underscoring the need for predictive inventory tools that reduce cascading care disruptions.

Ageing Population & Chronic Disease Burden Intensifying Last-Mile Demand

Long-term demographic projections show a sharply rising proportion of citizens older than 65 by 2074. Chronic illnesses shift dispensing patterns toward repeat prescriptions delivered to patients' homes, which magnifies last-mile complexity within Spain pharmaceutical logistics market. Digital health platforms integrate telemedicine with pharmacy networks and require timed deliveries of cardiovascular and diabetes drugs. Generic penetration led by Kern Pharma and Teva supports affordability but raises shipment frequency. Personalized oncology regimens from PharmaMar demand traceable, patient-specific cold-chain movements that extend beyond hospital pharmacies into home-care settings.

Driver Shortage & Escalating Labour Costs

Cold-chain operators represent 2.5% of Iberian food GDP and face acute driver shortages that inflate wage bills. DHL answered with a EUR 2 billion (USD 2.08 billion) health-logistics program that prioritizes automation to counter labor gaps. UPS seeks to double healthcare revenue to USD 20 billion by 2026, banking on robotics and routing software to lift productivity. Despite capital injections, immediate driver scarcity restricts capacity during influenza vaccine peaks, restraining Spain pharmaceutical logistics market expansion.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Biologics & Temperature-Sensitive Therapies

- EU Falsified Medicines Directive Serialization Deadline Enforcement

- Rising Energy Costs Impacting Refrigerated-Warehouse Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation captured 59.30% of Spain pharmaceutical logistics market share in 2025, propelled by 15,825 km of motorways connecting ports at Barcelona, Valencia, and Algeciras. This backbone delivers medicines to 200,000 European points of sale through networks managed by Logista and DHL. Road haulage remains the preferred mode for its overnight reach, but airfreight is scaling via Girona and Zaragoza airports to meet urgent biologic demand. Sea and rail corridors increasingly attract shippers pursuing carbon-reduction targets, with CEVA citing 70% lower emissions for refrigerated sea lanes. Value-added services & others are expected to post a 4.66% CAGR to 2031 as GDP documentation, kitting, and late-stage customization become standard contract inclusions. FedEx secured a CEIV Pharma Corporate Certificate in 2025 and won USD 400 million in healthcare contracts, illustrating the commercial payoff from compliance excellence.

Spain pharmaceutical logistics market size for value-added services & others is forecast to rise, aligned with expanding outsourcing by Spanish hospitals. The modal mix will tilt toward temperature-controlled containers that embed IoT sensors, creating data streams monetized through predictive lane validation services. UPS's integration of Frigo-Trans and BPL widens its European 2-8 °C footprint and offers Spanish pharma exporters a single invoice solution spanning road, sea and air. Sustainability is another driver, with electric trucks now servicing inner-city clinics in Madrid under CEVA's FORPLANET label, reducing emissions by 26,000 tons in 2024.

The Spain Pharmaceutical Logistics Market Report is Segmented by Service Type (Transportation, Warehousing & Storage, and Value-Added Services & Others), Mode of Operation (Cold-Chain Logistics and Non-Cold-Chain Logistics), Product Type (Prescription Drugs, OTC Drugs, Biologics & Biosimilars, Vaccines & Blood Products, Cell & Gene Therapies, Veterinary Medicine, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- DHL Supply Chain Spain

- FedEx Express

- Kuehne + Nagel S.A.

- United Parcel Service (UPS)

- C.H. Robinson

- CEVA Logistics

- DSV

- Movianto

- Eurotranspharma

- Primafrio

- Cencora

- Yusen Logistics (Part of NYK Line)

- Scan Global Logistics

- Rhenus Logistics

- Geodis

- TIBA

- Logista Pharma

- Noatum Logistics

- Ibercondor

- Logisber

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising domestic pharmaceutical sales volume

- 4.2.2 Ageing population & chronic disease burden intensifying last-mile demand

- 4.2.3 Expansion of biologics & temperature-sensitive therapies

- 4.2.4 EU Falsified Medicines Directive serialization deadline enforcement

- 4.2.5 RRF-backed cold-chain infrastructure investments

- 4.2.6 Hospital network shift toward outsourced supply models

- 4.3 Market Restraints

- 4.3.1 Driver shortage & escalating labour costs

- 4.3.2 Ensuring end-to-end temperature integrity amid climate extremes

- 4.3.3 Fragmented cold-storage real-estate ownership

- 4.3.4 Rising energy costs impacting refrigerated-warehouse margins

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Geopolitics & Pandemic on the Market

5 Market Size & Growth Forecasts (Value)

- 5.1 By Service Type

- 5.1.1 Transportation

- 5.1.1.1 Road Freight

- 5.1.1.2 Air Freight

- 5.1.1.3 Sea Freight

- 5.1.1.4 Rail Freight

- 5.1.2 Warehousing & Storage

- 5.1.3 Value-added Services and Others

- 5.1.1 Transportation

- 5.2 By Mode of Operation

- 5.2.1 Cold-Chain Logistics

- 5.2.2 Non-Cold-Chain Logistics

- 5.3 By Product Type

- 5.3.1 Prescription Drugs

- 5.3.2 OTC Drugs

- 5.3.3 Biologics & Biosimilars

- 5.3.4 Vaccines & Blood Products

- 5.3.5 Clinical Trail Materials

- 5.3.6 Cell & Gene Therapies

- 5.3.7 Medical Devices & Diagnostics

- 5.3.8 Veterinary Medicine

- 5.3.9 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 DHL Supply Chain Spain

- 6.4.2 FedEx Express

- 6.4.3 Kuehne + Nagel S.A.

- 6.4.4 United Parcel Service (UPS)

- 6.4.5 C.H. Robinson

- 6.4.6 CEVA Logistics

- 6.4.7 DSV

- 6.4.8 Movianto

- 6.4.9 Eurotranspharma

- 6.4.10 Primafrio

- 6.4.11 Cencora

- 6.4.12 Yusen Logistics (Part of NYK Line)

- 6.4.13 Scan Global Logistics

- 6.4.14 Rhenus Logistics

- 6.4.15 Geodis

- 6.4.16 TIBA

- 6.4.17 Logista Pharma

- 6.4.18 Noatum Logistics

- 6.4.19 Ibercondor

- 6.4.20 Logisber

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

生物製药物流市场:依产品类型、服务类型、运输方式、温度需求及最终用户划分-2026-2032年全球市场预测

生物製药物流市场:依产品类型、服务类型、运输方式、温度需求及最终用户划分-2026-2032年全球市场预测 2026年全球生物製药物流市场报告

2026年全球生物製药物流市场报告 全球医药物流市场规模、份额、趋势及成长分析报告(2026-2034)全球生物製药物流市场规模、份额、趋势和成长分析报告(2026-2034)医药物流市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年

全球医药物流市场规模、份额、趋势及成长分析报告(2026-2034)全球生物製药物流市场规模、份额、趋势和成长分析报告(2026-2034)医药物流市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年 美国医学流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

美国医学流:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 全球医药物流市场:依产品类型、服务、运输方式、物流类型、应用、国家及地区划分-产业分析、市场规模、份额及2025年至2032年未来预测

全球医药物流市场:依产品类型、服务、运输方式、物流类型、应用、国家及地区划分-产业分析、市场规模、份额及2025年至2032年未来预测 2025-2029年全球医学流市场

2025-2029年全球医学流市场 医药物流市场-全球产业规模、份额、趋势、机会、预测:按类型、按组件、按地区和竞争对手划分,2021-2031年医药物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

医药物流市场-全球产业规模、份额、趋势、机会、预测:按类型、按组件、按地区和竞争对手划分,2021-2031年医药物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)