|

市场调查报告书

商品编码

1934782

美国医学流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)United States Pharmaceutical Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

2025年美国医药物流市场价值为759.6亿美元,预计到2031年将达到926.7亿美元,高于2026年的785.3亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 3.38%。

美国药品物流市场规模预测报告重点指出,合规期限和生物製药需求正在重塑成本结构和服务设计。将于2025年8月到期的《药品供应链安全法案》(DSCSA)更为严格的实施期限,迫使资金雄厚的运营商进行序列化投资,而这些投资只有在具备相应条件的情况下才可行,从而赋予他们收取溢价的自由裁量权。基于GLP-1的体重管理疗法的快速增长、细胞和基因疗法的稳步发展以及直接面向患者(DTP)服务的扩张,进一步扩大了美国药品物流市场,要求运营商迅速提升其温控能力。同时,製造商正在开发现有药物的常温稳定版本,以降低不断上涨的运输成本。这减缓了非冷藏配送的相对成长,但为附加价值服务(VAS)供应商创造了新的包装和标籤业务。区域网络正在重组,中西部地区作为全国枢纽的份额不断扩大,而南部地区的运力扩张则缓解了沿海走廊的拥挤状况。

美国医学流市场趋势与洞察

需要严格温度控制的特殊生技药品的扩张

温控运输成本是常温运输的三到五倍,在已开发市场分销的治疗药物中,目前有80%需要在2-8°C的温度下储存,这进一步增加了低温运输的复杂性。 UPS采取了先发制人的行动,于2025年4月以16亿美元收购了Andlauer Healthcare Group,新增了170万平方英尺符合GDP认证的仓库空间,并扩展了其-80°C的冷冻库网路。生物製药需要更短的订单到交货週期,因此对高频补货路线的需求高于大宗货物运输。小型承运商难以资金筹措持续监控系统的资金,这些系统需接受FDA的偏差记录审核,加速了产业的整合。次市场低温运输设施的激增为营运商提供了地域上的柔软性,但也需要在额外的交接点进行库存调整,这进一步凸显了基于人工智慧的路线可视性的重要性。

DSCSA序列化截止日期推动了追踪和溯源投资。

美国食品药物管理局 (FDA) 强制要求处方药在 2025 年 8 月前实现全程单元级可追溯性,这使得美国药品物流市场分为两类:一类是具备序列化能力的供应商,另一类是权限有限的供应商。 TraceLink 的 B2N 网路在 90 天内处理了 600 万个 EPCIS 事件,但资料错误率高达 30%,这可能导致每日产品隔离,凸显了实施的复杂性。预计每件可售产品的初始系统成本为 0.06 美元,这促使第三方物流专家采用共享解决方案。将 DSCSA 合规性纳入附加价值服务(VAS) 包的供应商不仅可以获得固定费用,还能加深买家对数位生态系统的依赖,从而实现召回管理、缺货预防和契约製造监管。

燃油价格波动推高了配送成本。

由于2024年至2025年间WTI原油现货价格波动幅度高达23%,药品托运商面临燃油额外费用计算公式不稳定、落后于成本飙升数週的困境。温控卡车由于冷冻装置的运作,柴油消耗量增加了12%,加剧了风险。液化天然气和电动牵引车的试验前景可观,但续航里程的限制和充电网路的不足制约了它们在东西向跨大西洋航线上的应用。路线优化软体和多站点运输模式可以减少空驶里程,但产品完整性规则仍然限制了货物的整合。

细分市场分析

儘管运输仍然是收入的基础,但美国医药物流市场正明显地向一体化解决方案转型。 2025年,运输收入占比为70.45%,但预计从2026年到2031年,附加价值服务将以4.75%的复合年增长率超越运输收入,这主要得益于客户对序列化、重新贴标和套件组装等服务以及货运需求的增加。公路货运的份额依然强劲,这主要得益于最后一公里配送和向乡村诊所的配送,而感测器和双隔间拖车的应用也有助于加强合规性。儘管空运成本较高,但它在细胞疗法和其他特殊用途货物的运输方面仍然占据着独特的地位,因为这些货物的运输不容延误。随着托运人越来越多地使用温控冷藏集装箱来运输从亚洲到美国的稳定药物原料药,海运业务正在扩张,这不仅符合ESG目标,还能在空运运力短缺时提供运力。

由于缺乏符合GDP标准的转运点,铁路运输仍受到限制。由于《药品分销安全法》(DSCSA)提高了可追溯性要求,仓储需求紧张。仓库正在转型为数位化序列化中心,以便在发货前检验二维资料矩阵码,而自动化计划(视觉系统扫描器和自动托盘运输车)正在减少合规性检查的延误。成长最快的是附加价值服务(VAS)领域,其中包括托盘重新配置、紧急客製化以及进出口差异的记录。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 扩大需要严格温度控制的特殊生技药品。

- DSCSA序列化截止日期推动可追溯性投资

- GLP-1类肥胖症和糖尿病药物分销的快速成长给低温运输能力带来了压力。

- 转变运输方式,注重永续性:从空运转向海运

- 直接面向患者的交付模式的成长

- 利用人工智慧驱动的「控制塔」进行路线优化和预测性损耗分析,以缩短前置作业时间

- 市场限制

- 燃油价格波动推高了分销成本。

- 学名药价格下跌给物流利润带来压力。

- 低温技术人员和驾驶人短缺

- 针对物联网冷链基础设施的网路攻击

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按服务类型

- 运输

- 公路货运

- 空运

- 海上运输

- 铁路货运

- 仓储和存储

- 附加价值服务及更多

- 运输

- 按操作模式

- 低温运输物流

- 非低温运输物流

- 依产品类型

- 处方药

- 非处方药

- 生物製药和生物相似药

- 疫苗和血液製品

- 临床试验材料

- 细胞和基因治疗

- 医疗设备和诊断试剂

- 动物医药

- 其他的

- 按地区(美国)

- 东北

- 中西部

- 南部

- 西

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- DHL Supply Chain & Global Forwarding

- FedEx

- UPS

- Cencora

- CH Robinson

- XPO Logistics

- Ryder System

- Penske Logistics

- Expeditors International

- SEKO Logistics

- LifeScience Logistics

- MD Logistics

- DSV

- Kuehne+Nagel

- Hub Group

- Nippon Express

- CEVA Logistics

- GXO Logistics

- KRC Logistics

- Langham Logistics

- Crown LSP Group

第七章 市场机会与未来展望

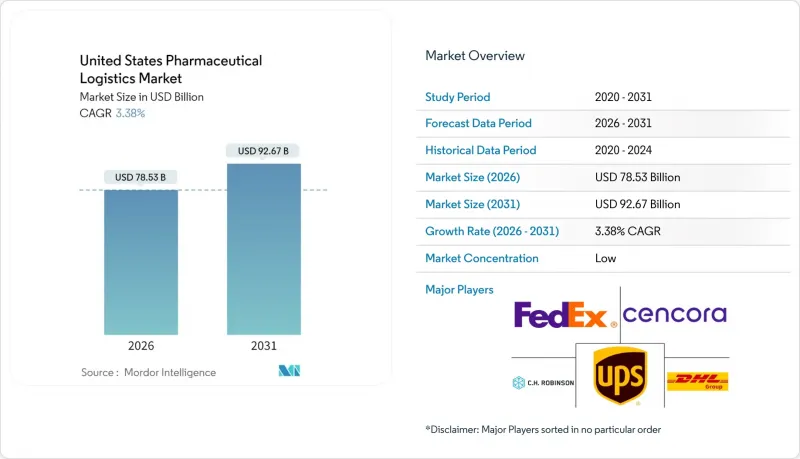

The United States Pharmaceutical Logistics Market was valued at USD 75.96 billion in 2025 and estimated to grow from USD 78.53 billion in 2026 to reach USD 92.67 billion by 2031, at a CAGR of 3.38% during the forecast period (2026-2031).

The United States pharmaceutical logistics market size projection underscores how compliance deadlines and biologics demand are reshaping cost structures and service design. A tightening Drug Supply Chain Security Act (DSCSA) timetable, expiring in August 2025, forces serialization investments that only well-capitalized providers can execute, granting them premium pricing latitude. Surging GLP-1 weight-management therapies, the steady rise of cell and gene treatments, and direct-to-patient (DTP) fulfillment further enlarge the United States pharmaceutical logistics market, pressing operators to expand temperature-controlled capacity at speed. Manufacturers are simultaneously formulating ambient-stable versions of existing drugs to curb rising freight costs, tempering the relative growth of non-cold-chain flows yet creating new packaging and labeling work for value-added service (VAS) providers. Regional network redesign is underway, with the Midwest gaining share as a national hub while capacity additions in the South ease congestion on coastal corridors.

United States Pharmaceutical Logistics Market Trends and Insights

Expansion of Specialty Biologics Requiring Strict Temperature Control

Temperature-controlled transport costs three to five times more than ambient freight, and 80% of therapies shipped in developed markets now need 2°-8 °C custody, elevating cold-chain complexity. UPS moved early by paying USD 1.6 billion for Andlauer Healthcare Group in April 2025, adding 1.7 million ft2 of GDP-certified storage and extending its -80 °C freezer network. Biologics also shorten order-to-delivery cycles, driving demand for high-frequency replenishment lanes rather than bulk shipments. Smaller carriers struggle to finance the continuous monitoring systems the FDA now audits for excursion logs, accelerating consolidation. As cold-chain nodes multiply in secondary markets, operators gain geographic flexibility but must coordinate inventory at added hand-off points, intensifying the need for AI-driven route visibility.

DSCSA Serialization Deadline Boosting Trace-and-Trace Investments

The FDA requires full unit-level traceability on prescription medicines by August 2025, splitting the United States pharmaceutical logistics market between serialization-ready providers and those facing restricted access. Implementation complexity is evident in TraceLink's B2N network, which processed 6 million EPCIS events in 90 days yet logged a 30% data-error rate that could trigger daily product quarantines. Up-front system costs, estimated at USD 0.06 per saleable unit, invite pooling solutions run by third-party logistics specialists. Providers that embed DSCSA compliance into VAS packages not only lock in retainer fees but also deepen buyer dependence on their digital ecosystems for recall management, shortage mitigation, and contract manufacturing oversight.

Fuel-Price Volatility Inflating Distribution Costs

WTI spot prices swung 23% in 2024-2025, leaving pharma carriers with unmatched fuel-surcharge formulas that lag cost spikes by weeks. Temperature-controlled trucks burn 12% more diesel to power reefers, amplifying exposure. While LNG and electric tractor pilots show promise, range limits and sparse charging networks curtail adoption on coast-to-coast lanes. Route-optimization software and multi-stop milk-run models reduce empty miles, but product-integrity rules still cap load consolidation.

Other drivers and restraints analyzed in the detailed report include:

- Surge in GLP-1 Obesity/Diabetes Drug Volumes Stressing Cold-Chain Capacity

- Growth of Direct-to-Patient Distribution Models

- Generic-Drug Price Erosion Squeezing Logistics Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation still anchors revenue, yet the United States pharmaceutical logistics market shows a clear migration toward bundled solutions. In 2025, transportation delivered 70.45% of turnover, but value-added services are expected to outpace at a 4.75% CAGR (2026-2031) as clients seek serialization, relabeling, and kitting alongside freight. Road freight's share remains resilient due to final-mile and rural clinic deliveries, with sensors and dual-compartment trailers adding compliance. Air freight, while costly, preserves its niche for cell therapy and compassionate-use shipments that tolerate no delay. Ocean carriage gains as shippers divert stable formulation APIs to controlled-atmosphere reefers on Asia-to-US lanes, aligning with ESG goals and securing uplift during air-capacity crunches.

Rail remains marginal, hindered by limited GDP-certified hand-off nodes. Warehouse & storage demand tightens as DSCSA elevates traceability, turning depots into digital serialization hubs where 2D data-matrix codes are verified before release. This pushes automation projects-vision-system scanners and autonomous pallet movers-to squeeze latency out of compliance checks. The fastest growth occurs in VAS, including pallet reconfiguration, late-stage customization, and documentation for import-export variance.

The United States Pharmaceutical Logistics Market Report is Segmented by Service Type (Transportation, Warehousing & Storage, and Value-Added Services & Others), Mode of Operation (Cold-Chain Logistics and Non-Cold-Chain Logistics), Product Type (Prescription Drugs, Biologics & Biosimilars, Veterinary Medicine, and More), Region (Northeast, Midwest, South, and West). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- DHL Supply Chain & Global Forwarding

- FedEx

- UPS

- Cencora

- C.H. Robinson

- XPO Logistics

- Ryder System

- Penske Logistics

- Expeditors International

- SEKO Logistics

- LifeScience Logistics

- MD Logistics

- DSV

- Kuehne + Nagel

- Hub Group

- Nippon Express

- CEVA Logistics

- GXO Logistics

- KRC Logistics

- Langham Logistics

- Crown LSP Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of specialty biologics requiring strict temperature control

- 4.2.2 DSCSA serialization deadline boosting trace-and-trace investments

- 4.2.3 Surge in GLP-1 obesity/diabetes drug volumes stressing cold-chain capacity

- 4.2.4 Sustainability-driven modal shift from air to sea freight

- 4.2.5 Growth of direct-to-patient distribution models

- 4.2.6 AI-enabled "control-tower" routing and predictive spoilage analytics reducing lead times

- 4.3 Market Restraints

- 4.3.1 Fuel-price volatility inflating distribution costs

- 4.3.2 Generic-drug price erosion squeezing logistics margins

- 4.3.3 Shortage of ultra-low-temperature technicians & drivers

- 4.3.4 Cyber-attacks on IoT cold-chain infrastructure

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Service Type

- 5.1.1 Transportation

- 5.1.1.1 Road Freight

- 5.1.1.2 Air Freight

- 5.1.1.3 Sea Freight

- 5.1.1.4 Rail Freight

- 5.1.2 Warehousing & Storage

- 5.1.3 Value-added Services and Others

- 5.1.1 Transportation

- 5.2 By Mode of Operation

- 5.2.1 Cold-Chain Logistics

- 5.2.2 Non-Cold-Chain Logistics

- 5.3 By Product Type

- 5.3.1 Prescription Drugs

- 5.3.2 OTC Drugs

- 5.3.3 Biologics & Biosimilars

- 5.3.4 Vaccines & Blood Products

- 5.3.5 Clinical Trail Materials

- 5.3.6 Cell & Gene Therapies

- 5.3.7 Medical Devices & Diagnostics

- 5.3.8 Veterinary Medicine

- 5.3.9 Others

- 5.4 By Region (United States)

- 5.4.1 Northeast

- 5.4.2 Midwest

- 5.4.3 South

- 5.4.4 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 DHL Supply Chain & Global Forwarding

- 6.4.2 FedEx

- 6.4.3 UPS

- 6.4.4 Cencora

- 6.4.5 C.H. Robinson

- 6.4.6 XPO Logistics

- 6.4.7 Ryder System

- 6.4.8 Penske Logistics

- 6.4.9 Expeditors International

- 6.4.10 SEKO Logistics

- 6.4.11 LifeScience Logistics

- 6.4.12 MD Logistics

- 6.4.13 DSV

- 6.4.14 Kuehne + Nagel

- 6.4.15 Hub Group

- 6.4.16 Nippon Express

- 6.4.17 CEVA Logistics

- 6.4.18 GXO Logistics

- 6.4.19 KRC Logistics

- 6.4.20 Langham Logistics

- 6.4.21 Crown LSP Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

生物製药物流市场:依产品类型、服务类型、运输方式、温度需求及最终用户划分-2026-2032年全球市场预测

生物製药物流市场:依产品类型、服务类型、运输方式、温度需求及最终用户划分-2026-2032年全球市场预测 2026年全球生物製药物流市场报告

2026年全球生物製药物流市场报告 全球医药物流市场规模、份额、趋势及成长分析报告(2026-2034)全球生物製药物流市场规模、份额、趋势和成长分析报告(2026-2034)医药物流市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年

全球医药物流市场规模、份额、趋势及成长分析报告(2026-2034)全球生物製药物流市场规模、份额、趋势和成长分析报告(2026-2034)医药物流市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年 西班牙医药物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

西班牙医药物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 全球医药物流市场:依产品类型、服务、运输方式、物流类型、应用、国家及地区划分-产业分析、市场规模、份额及2025年至2032年未来预测

全球医药物流市场:依产品类型、服务、运输方式、物流类型、应用、国家及地区划分-产业分析、市场规模、份额及2025年至2032年未来预测 2025-2029年全球医学流市场

2025-2029年全球医学流市场 医药物流市场-全球产业规模、份额、趋势、机会、预测:按类型、按组件、按地区和竞争对手划分,2021-2031年医药物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

医药物流市场-全球产业规模、份额、趋势、机会、预测:按类型、按组件、按地区和竞争对手划分,2021-2031年医药物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)