|

市场调查报告书

商品编码

1398379

网路营运商预测(~2028 年):资本支出将在 2023 年下降后恢復,并在 2028 年增长至约 6500 亿美元,生成式人工智慧推动资本支出和员工人数减少Network Operator Forecast Through 2028: After 2023 Dip, Capex Will Bounce Back, Growing to Reach ~$650B by 2028, GenAI Will Drive Both Capex and Job Cuts |

|||||||

预计到2024年,三类网路营运商的收入将达到4.38兆美元(2022年为4.11兆美元)。 此外,资本投资预计为5,520亿美元(2022年为5,630亿美元),员工人数预计为871万人(2022年为888万人)。

本报告分析了全球网路营运商市场(电信公司、网路扩展商、营运商中立网路营运商(CNNO) 等)的业务绩效前景和资本投资趋势,并提供了超过175 家公司的最新信息。除了按季度调查和估计业绩趋势(2011年至2022年的收入、资本投资额、员工人数等)和未来前景(截至2028年)外,我们还检查按部门划分的详细趋势和过去的预测结果。我们将为您提供比较等资讯。

总体基于数量的分析结果

电信、网路规模和营运商中立三个细分市场的总收入将在 2022 年增长至 41,090 亿美元,到 2028 年将增长至 53,440 亿美元。 2022年,这三个部门的资本支出为5,630亿美元,2023年和2024年均减少至约5,500亿美元,2028年增加至6,620亿美元。 网路规模的资本支出最近已趋于平稳,但从长远来看,该领域占网路营运商成长的大部分。 2011年,网路规模占资本支出的比例不到10%;到2022年将超过36%,到2028年将超过43%。 预计 CNNO 到 2028 年将占资本支出的 7%,较目前略有增加,而电信公司预计到 2028 年将占网路营运商资本支出的略低于 50%。 就资本密集度而言,2022年所有业者的平均为13.7%,但2028年仅为12.4%。 电信公司是这项运动的关键推动者。 电信公司的年化资本密集度在 2023 年第一季达到 18.7% 的峰值,随着大多数 5G 网路的建成,资本密集度开始迅速下降。 资本密集度预计将于 2027 年开始回升,并于 2028 年达到 17.1%。 到了 2022 年,网路扩展器的资本密集度也创下 9.1% 的历史新高,但这一趋势现在正在放缓。 然而,随着营运商填满现有资料中心,网路扩展器用于网路的资本支出比例正在增加。 与往常一样,营运商中立的资本密集度最高,在预测期内远高于 30%。

过去十年,三大业者部门的员工数量大幅增加,从 2011 年的 648 万人增加到 2022 年的 888 万人。 这与 2021 年的数字大致相同。 电信公司在 2022 年加速裁员,多家网路扩容商也宣布裁员。 2023年员工总数为876万人,较前一年略有减少,但这主要是由于电信公司持续裁员所致。 展望未来,预计电信公司的削减速度将加快,部分原因是产生人工智慧的贡献。 到 2025 年,网路扩展器将出现一些成长,但此后将开始稳定下降。 特别是对于像Amazon和JD.com这样以电子商务为导向的网路扩展商来说,多年来在机器人和人工智慧方面的大规模研发投资将开始取得成果,从而降低劳动力成本。 CNNO 预计将僱用超过 10 万名员工。 按细分市场划分,CNNO 的每位员工销售额迄今为止最高,约为 876,000 美元,而网路规模的销售额为 562,000 美元,电信公司的销售额为 391,000 美元,到 2023 年。 随着 2026 年劳动力开始下降,该指标的成长将达到网路规模最高。 电信公司的员工人均收入成长最慢,儘管对裁员的假设相当激进。 另一种情况是电信公司高层主动部署生成式人工智慧,以支援短期裁员,尤其是销售和行销部门。 英国电信 (BT) 是发现这种情况的电信公司之一。 然而,大多数电信公司可能对在网路营运等敏感领域立即部署生成式人工智慧持谨慎态度。

主要分析结果:依网路营运商类型划分

此预测提供了三种网路营运商类型中每种类型的详细分类。 以下是按细分市场划分的主要调查结果摘要:

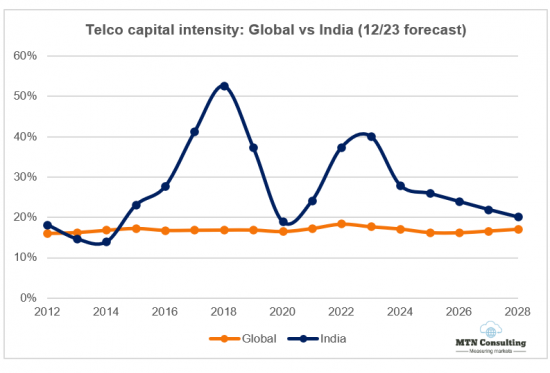

电信:正如我们一直所说,电信本质上是一个零成长产业。 由于市场份额的变化、成长週期时间的差异以及併购,某些国家和公司会不时实现成长。 然而,自2011年以来,全球电信公司收入一直维持在窄幅区间(1.7兆美元至1.9兆美元),而这种情况可能会持续到2028年。 预计2022年营收为1.78兆美元,2023年小幅下降,然后年平均成长1.4%,2028年达到1.93兆美元。 由于技术更新周期(例如 5G)和政府行动(例如新频谱产品和本地光纤补贴),资本支出不断变化。 2022年资本投资总额将为3,280亿美元,占营收的18.1%。 这是我们时间范围内(2011 年至今)有史以来最高的年度资本密集度。 然而,预计到 2025 年,资本投资将略有下降,然后在 2028 年再次小幅上升,达到 3,310 亿美元(资本密集度为 17.1%)。 2022年美国资本投资激增,但2023年和2024年将大幅下降。 软体资本支出的成长可能会慢于预期,并且在预测期内仍低于总资本支出的 20%。 电信业从业人员数量下降速度快于预期,预计将从2022年的略低于460万降至2028年的不到420万。 随着电信公司培养更多以 IT/软体为中心的劳动力队伍,人均劳动成本预计将在 2023 年恢復成长。

网路扩展器:在过去的十年中,网路规模的成长推动了整个网路营运商市场。 在新冠疫情期间,网路扩展商的各项指标都出现了激增,包括收入、资本支出和就业。 对资料中心晶片及相关设备的需求也激增。 但该产业去年成长放缓,并且正在削减成本、资本支出和员工人数。 2023年营收约2.32兆美元,连续第二年年比仅成长4%。 到 2028 年,复合年增长率预计将在 7% 左右。 到 2022 年,网路规模资本支出将达到 2,030 亿美元,较 2021 年实现健康成长。 然而,预计到 2024 年底,资本支出将保持停滞状态,经过几年的产能吸收,并将于 2025 年再次开始增加。 在淡季期间,大部分资本支出将用于网路/IT/软体。 网路扩展器的研发支出仍将保持在高位,但将从 2022 年的创纪录水准(占营收的 12.0%)下降到 2028 年的略高于 10%。 随着网路扩展商的收入成长变得更加困难,我们相信他们将变得更加重视成本和短期导向。

营运商中立:营运商中立产业规模仍然较小,2022 年营收为 950 亿美元,但到 2028 年将成长至约 1,240 亿美元。 网路扩展商和电信公司将越来越依赖 CNNO 来扩展其资料中心、塔和光纤足迹。 电信公司正在将部分基础设施转移给第三方,包括传统的CNNO(例如TASC Towers,它从Zain 和Ooredoo 收购了30,000 座塔)以及合资企业,例如AT&T 和Blackrock 之间的合作伙伴Gigapower。我认为它会继续走出去。 CNNO 2022 年的总资本投资将为 330 亿美元,2028 年将增至约 450 亿美元。 到2028 年,CNNO 部门将拥有约380 万个蜂窝塔(2022 年:330 万个)、1,718 个资料中心(2022 年:1,223 个)和113 万英里的光纤线路(2022 年:945,000 英里)处于控制之下。

目标范围

目标公司

|

|

目录

本报告的主要部分:

- 1. 概述

- 2. 网路营运商总数

- 3.电信公司

- 4.电信公司 - 区域细分

- 5.网路规模

- 6.操作员中立 (CNNO)

- 7. 主要业者的支出前景

- 8.概述

本报告中的主要分析结果标籤- “网路营运商总数”、“电信公司”、“电信公司- 区域细分”、“网路规模” 、 "运营商" 中性(CNNO)" - 包含许多分析结果。

"网路营运商总计" 标籤上发布的数字清单:

- 按细分市场划分的资本投资预测:2023 年 12 月和 2022 年 12 月展望,差异(单位:%)

- 按细分市场划分的资本投资预测:2023 年 12 月与 2022 年 12 月之间的展望与差异(单位:十亿美元)

- 所有业者的营收成长率:新旧预测

- 电信公司营收成长率:新旧预测

- 资本密集度、电信公司:新旧预测

- 资本密集度、网路扩展器:新旧预测

- 资本强度,CNNO:新旧预测

- 收入,依业者类型(单位:十亿美元,2011-2028 年)

- 按运营商类型划分的资本投资(单位:十亿美元,2011-2028 年)

- 按运营商类型划分的资本投资(占总数的百分比,2011-2028 年)

- 依业务类型划分的资本强度(2011-2028 年)

- 员工人数:依业务类型划分

- 每位以业务类型划分的员工收入(单位:1000 美元)

- 网路营运商收入:按类型划分,全球范围(占 GDP 的百分比)

- 网路营运商员工及其占世界人口的百分比

- 电信公司每名用户的收入和资本投资(2011-2022 年)

- 支出□□前 50 名的公司:年化资本投资(单位:十亿美元,2023 年第三季)

- 50强企业:长期资本密集度(2019年第四季至2023年第三季平均值)

This forecast report presents our latest projections for the network operator market, spanning telecommunications operators (telcos), webscalers, and carrier-neutral network operators (CNNOs). The forecast is based on our quarterly coverage of over 175 operators. Our forecast includes revenues, capex and employee totals for all segments, and additional metrics for each individual segment. In 2024, we expect the three operator groups to account for $4.38 trillion (T) in revenues (2022: $4.11T), $552 billion (B) in capex (2022: $563B), and 8.71 million (M) employees (2022: 8.88M). This report provides 2011-22 actuals and projections through 2028, and includes projections from past forecasts for reference.

VISUALS

Top line quantitative results

Revenues from the aggregate of our three segments - telco, webscale, and carrier-neutral - were $4,109 billion (B) in 2022, and will grow to $5,344B by 2028. Three segment capex ended 2022 at $563B, will fall to ~$550B for both 2023 and 2024, then grow to $662B in 2028. Webscale capex has flattened recently but over the longer timeframe this sector accounts for most network operator growth. In 2011, webscale was less than 10% of capex, but exceeded 36% in 2022 and will be over 43% by 2028. CNNOs will represent 7% of 2028 capex, a bit more than today, while telcos will capture just under 50% of expected 2028 network operator capex. In capital intensity terms, the all-operator average was 13.7% in 2022 but that will be just 12.4% in 2028. That's largely because of telcos: their annualized capital intensity peaked at 18.7% in 1Q23 and has begun to come down rapidly, now that most 5G networks are built. That will start to come back in 2027 and hit 17.1% in 2028. Webscalers also saw an all-time high capital intensity in 2022, of 9.1%, which is now easing. The portion of webscalers' capex spent on the network is rising, though, as operators fill up existing data centers. Capital intensity is highest in carrier-neutral, as usual, well over 30% for the whole forecast period.

Headcount across the three operator segments has grown dramatically in the last decade, from 6.48 million in 2011 to 8.88M in 2022. That is roughly the same as the 2021 figure: telcos accelerated headcount reductions in 2022, and several webscalers announced layoffs. In 2023, total headcount will be 8.76M, a bit down YoY, due mainly to ongoing telco cuts. Looking forward, we expect telco reductions to slightly accelerate, with contributions from GenAI. Webscalers will grow a bit through 2025 but then headcount will begin to decline steadily. All the years of big R&D investments into robotics and AI will start to really pay off after this, lowing workforce costs, especially for the ecommerce-oriented webscalers like Amazon and JD.Com. CNNO employment will stay just above 100,000. By segment, revenue per employee is by far the highest in CNNO, at ~$876K in 2023, versus $562K for webscale and $391K for telco. Growth in this metric will be highest in webscale, though, as the workforce starts to shrink in 2026. Telcos' growth in revenues per employee is the slowest, even with our fairly aggressive assumptions about job cuts. There is another scenario possible, in which telco execs implement GenAI aggressively in order to support near-term layoffs, especially in sales & marketing; BT is one telco which has pointed to this scenario. Most telcos will be cautious about immediate GenAI implementation for sensitive areas such as network operations, though.

Key findings by network operator type

This forecast includes detailed breakouts for each of the three network operator types. Here is a summary of some of the key findings, by segment:

Telcos: as we keep saying, telecom is essentially a zero-growth industry. Specific countries and companies do grow from time to time, in part from market share shifts, the different timing of growth cycles, or M&A. But global telco revenues have hovered in a narrow range ($1.7-$1.9 trillion) since 2011, and this will likely remain true through 2028. In 2022, revenues were $1.78T, will fall a bit in 2023, then will grow an average annual rate of 1.4% to reach $1.93T by 2028. Capex continues to vary with technology upgrade cycles (e.g. 5G) and government actions (e.g. newly issued spectrum, or rural fiber subsidies). In 2022, capex totaled $328B, or 18.1% of revenues; that's an annual all-time high capital intensity, for our coverage timeframe (2011-present). Capex will decline slightly through 2025, though, and then rise modestly again to reach $331B in 2028, which would be a 17.1% capital intensity. US capex surged in 2022, but will drop significantly in both 2023 and 2024; we already expected this, though, so the current forecast is not significantly different. Software capex is growing more slowly than expected, and now likely to remain under 20% of total capex for the forecast period. Headcount in telecom is declining faster than expected, and now likely to fall below 4.2 million in 2028, from just under 4.6 million in 2022. Labor costs per head will revert to a growth trajectory in 2023, as telcos develop a more IT/software-centric workforce.

Webscalers: growth from webscale has lifted the overall network operator market over the last decade. Webscalers surged during COVID, by all measures - revenues, capex, employment. Demand for data center chips and related gear also surged. The sector saw slower growth last year, though, and is cutting back on costs, capex, and headcount. In 2023, revenues will be about $2.32 trillion, up just 4% YoY for the second straight year. We expect revenues to grow at a ~7% CAGR through 2028. Webscale capex was $203B in 2022, a healthy increase from 2021; capex will be in a holding pattern through end of 2024 though, allowing for a couple years of capacity absorption, and start to grow again in 2025. During the lull, a larger portion of capex will be for Network/IT/software investments R&D spending by webscalers will remain high but fall from the record-breaking level of 2022 (12.0% of revenues), to a bit over 10% in 2028. As topline growth gets harder for webscalers, they will become more cost conscious and short-term oriented.

Carrier-neutral: the carrier-neutral sector remains tiny, with just $95B in 2022 revenues, but will grow to about $124B by 2028. Webscalers and telcos alike will both rely more on CNNOs over time for expansion of their data center, tower and fiber footprints. Telcos will continue to spin out portions of their infrastructure to third-parties - both traditional CNNOs (e.g. TASC Towers, which just bought 30,000 towers from Zain and Ooredoo), and joint ventures like Gigapower, the AT&T-Blackrock partnership. Total CNNO capex for 2022 was $33B, and will grow to about $45B by 2028; a large chunk of the CNNO sector's expansion will be inorganic, though, via acquisition of existing assets from other sectors. By 2028, the CNNO sector will have under its management approximately 3.8 million cell towers (2022: 3.3M), 1,718 data centers (2022: 1,223), and 1.13M route miles of fiber (2022: 945K).

Key changes since last forecast

We publish a full forecast every 6 months. Here are some factors we considered in developing this latest forecast update:

Macroeconomics: Interest rates have risen a bit more, inflation shows signs of cooling, but economic growth forecasts from the IMF remain lackluster: "The baseline forecast is for global growth to slow from 3.5 percent in 2022 to 3.0 percent in 2023 and 2.9 percent in 2024, well below the historical (2000-19) average of 3.8 percent."

Generative AI: interest and adoption of generative AI (GenAI)-based tools and apps has continued to accelerate, and operators increasingly point to GenAI as a driver for infra investment, especially in the data center. The initial impact is to drive the carrier-neutral market, enticing more investment from private equity firms to have a position in the market. There is a lot of unmeasured private market activity in the data center market, and ongoing pull from PE firms to take assets private (e.g. in 2023, Bain-ChinData, and Brookfield-Cyxtera). GenAI will help webscale capex to lift off again starting 2025.

Telco business models: Telcos continue to spin off assets and search for new business models as 5G revenue growth fails to materialize. Among the many examples: in August 2023, Austria's A1 Telkom divested a portfolio of 12,900 cell towers across 5 countries, allowing it to shed 1B Euros in debt; also in 3Q23, Polish operator Polsat made strides in scaling up its new renewable energy business line, signing a deal to sell wind-generated power to Google, commissioning 2 wind farms, one solar farm, and 2 public hydrogen refueling stations. Expansion into new markets like energy requires new capex, but that is possible for telcos who choose to move towards an asset-light business model by selling off passive assets.

Telco capex: Telcos were already guiding down capex for 2024, but the guidance became even more negative with 2Q23 and 3Q23 earnings releases. Telco capex fell 8% YoY in 3Q23, and revenues for vendors selling into the telco market fell by over 10% YoY (preliminary). We already expected capex to start to decline in 2023, but it's started a bit sooner than expected. Telcos are pushing on every cost lever they can find, whether opex- or capex-related. The smarter ones are accepting that, as we expected, webscalers and other tech players are likely to reap most of the spoils of the world's new 5G networks. Telco execs need to stick to their knitting.

Headcount: Employment levels continue to go down steadily in the telecom industry, and have plateaued in the webscale sector. There is a lot of enthusiasm among execs in the potential for GenAI to reduce headcount levels, including in the telecom industry; we have increased the rate of employee attrition in this market.

Conflict: Russia's war on Ukraine remains ongoing, but hasn't expanded to new countries. China has not invaded Taiwan as of yet, although this is a serious risk over the 5-year forecast horizon.

Climate change: global warming news continues to worsen. Intergovernmental efforts to address it are still disappointingly watered down and toothless, as the recent COP28 event confirmed. Private efforts are full of greenwashing and baby steps. Many industries are taking real change slowly, in hopes that someone else will do the heavy lifting. Within our universe of operators, there are a few webscalers and CNNOs with impressive environmental records, though most of these built their networks from scratch in the last decade. The telco market is a problem; it needs to do more in 2024. Converting to 100% renewable energy as fast as reasonable will soon be on every operator's agenda, and this will come with some upfront investment. We don't forecast energy-related capex, but we do expect green energy to account for a growing share of capex budgets over time. Offsetting this capex burden is that early moving operators will be able to stabilize their energy spending, boost their green credentials legitimately, and possibly develop a new business line (for examples, see China Tower, Indus, and Polsat).

The net impact of these factors can be seen in the individual forecast tabs within this report.

COVERAGE

Companies mentioned:

|

|

Table of Contents

Key sections include:

- 1. Abstract

- 2. Network Operator Totals

- 3. Telco

- 4. Telco - Regional Splits

- 5. Webscale

- 6. Carrier-neutral (CNNO)

- 7. Spending outlook for top operators

- 8. About

This report has a large number of figures on each of the main result tabs: totals, telco, telco - regional splits, webscale, and carrier-neutral (CNNO).

A list of figures on the "Totals" tab:

- Capex forecast by segment: Dec 2023 v. Dec 2022 outlook, % difference

- Capex forecast by segment: Dec 2023 v. Dec. 2022 outlook, $B difference

- Revenue growth rates, all operators: New vs. old forecast

- Revenue growth rates, Telcos: New vs. old forecast

- Capital intensity, Telcos: New vs. old forecast

- Capital intensity, Webscalers: New vs. old forecast

- Capital intensity, Carrier-neutral operators: New vs. old forecast

- Revenue by operator type, 2011-28 (US$B)

- Capex by operator type, 2011-28 (US$B)

- Capex by operator type, 2011-28: % of total

- Capital intensity by operator type, 2011-28

- Employees by operator type (M)

- Revenues/employee by operator type (US$K)

- Network operator revenues by type, % global GDP

- Network operator employees (M), and % global population

- Telco revenues and capex per sub, 2011-22

- Top 50 spending operators, annualized 3Q23 capex ($B)

- Top 50 operators based on long-term capital intensity (4Q19-3Q23 avg)

2025年全球虚拟网路营运商市场报告

2025年全球虚拟网路营运商市场报告 Apps Run The World - 应用市场分析与买家洞察

Apps Run The World - 应用市场分析与买家洞察 虚拟网路营运商市场(按营运模式、服务技术和地区)

虚拟网路营运商市场(按营运模式、服务技术和地区) 营运商中立网路营运商 (CNNO) 市场回顾(2024 年第四季):生成式人工智慧 (Generic AI) 热潮加速私募股权投资

营运商中立网路营运商 (CNNO) 市场回顾(2024 年第四季):生成式人工智慧 (Generic AI) 热潮加速私募股权投资 关税情势如何影响美国再生能源成本

关税情势如何影响美国再生能源成本 关税情势对美国的再生能源成本带来的影响- 数据

关税情势对美国的再生能源成本带来的影响- 数据 通讯网路营运商市场回顾(2024年第三季):营收復苏,但持续的支出削减导致年度资本支出低于3,000亿美元大关

通讯网路营运商市场回顾(2024年第三季):营收復苏,但持续的支出削减导致年度资本支出低于3,000亿美元大关 网路营运商资本支出展望(2024 年第四季版):电信公司持平,但人工智慧驱动的生成式资料中心炒作将推动电信资本支出在 2024 年超过 6,000 亿美元,其中 Scalers 预计将引领市场

网路营运商资本支出展望(2024 年第四季版):电信公司持平,但人工智慧驱动的生成式资料中心炒作将推动电信资本支出在 2024 年超过 6,000 亿美元,其中 Scalers 预计将引领市场 网路营运商永续发展策略的全球市场:2024-2029

网路营运商永续发展策略的全球市场:2024-2029 Direct-to-Cell 全球市场:2024-2029

Direct-to-Cell 全球市场:2024-2029