|

市场调查报告书

商品编码

1666565

小型水力发电市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Small Hydropower Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

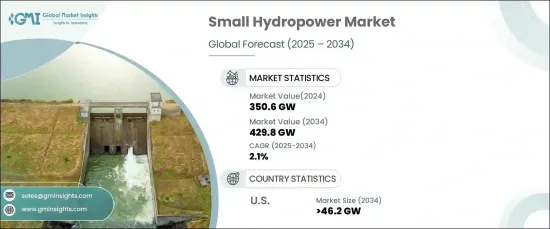

预计到 2024 年全球小型水力发电市场容量将达到 350.6 吉瓦,预计 2025 年至 2034 年期间复合年增长率为 2.1%。

小型水力发电是指容量在 100 千瓦至 10 兆瓦之间的水力发电系统,是偏远地区、小型公用事业和当地社区可采用的选择。这些系统的可扩展性和多功能性使其成为全球转向分散能源解决方案的关键贡献者。这些系统支援离网和微电网设置,满足缺乏可靠电网接入的地区的需求。技术改进,特别是涡轮机效率和成本的改进,进一步增强了全球采用小水力发电系统的可行性。

在美国,受联邦政府减少温室气体排放和整合更多再生能源措施的推动,小水力发电市场预计到 2034 年将超过 46.2 吉瓦。激励措施、税收优惠和补助等优惠政策也正在鼓励广泛采用。这种更清洁的能源提供了实用可靠的解决方案,符合向更永续能源结构过渡的目标。

在亚太地区,小水力发电正成为解决偏远和服务不足地区能源挑战的重要手段。这些系统利用当地的水资源提供可靠的电力,最大限度地减少对化石燃料的依赖,同时提高能源安全。小型水力发电计画能够独立于国家电网运行,这对偏远社区尤其有利。透过促进自给自足和减少对环境的影响,小水力发电作为农村供电的有效解决方案继续受到关注。

目录

第 1 章:方法论与范围

- 市场定义

- 基础估算与计算

- 预测计算

- 资料来源

- 基本的

- 次要

- 有薪资的

- 民众

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 监管格局

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- PESTEL 分析

第四章:竞争格局

- 战略仪表板

- 创新与永续发展格局

第五章:市场规模及预测:按地区,2021 – 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 义大利

- 俄罗斯

- 土耳其

- 挪威

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 世界其他地区

- 巴西

- 伊朗

第六章:公司简介

- 24H - Hydro Power

- Agder Energi

- Andritz Hydro

- Derwent Hydroelectric Power

- Fortum

- General Electric

- Lanco Group

- RusHydro

- Siemens

- Statkraft

- Voith

The Global Small Hydropower Market is projected to achieve a capacity of 350.6 GW by 2024 and is expected to grow at a CAGR of 2.1% between 2025 and 2034. This growth is largely driven by rising demand for renewable energy, increased focus on sustainability, and advancements in technology.

Small hydropower refers to hydroelectric systems with a capacity between 100 kW and 10 MW, making them an accessible option for remote areas, small utilities, and local communities. Their scalability and versatility make these systems a key contributor to the global transition towards decentralized energy solutions. These systems support off-grid and microgrid setups, addressing the needs of regions lacking reliable grid access. Technological improvements, particularly in turbine efficiency and cost, further enhance the feasibility of adopting small hydropower systems globally.

In the United States, the small hydropower market is expected to surpass 46.2 GW by 2034, fueled by federal initiatives aimed at reducing greenhouse gas emissions and integrating more renewable energy sources. Favorable policies, such as incentives, tax benefits, and grants, are also encouraging widespread adoption. This cleaner energy source offers a practical and reliable solution, aligning with goals to transition to a more sustainable energy mix.

In the Asia Pacific, small hydropower is emerging as an essential tool to address energy challenges in remote and underserved regions. These systems leverage local water resources to deliver reliable power, minimizing reliance on fossil fuels while improving energy security. The ability of small hydropower projects to operate independently of national grids makes them particularly beneficial for isolated communities. By promoting self-sufficiency and reducing environmental impact, small hydropower continues to gain traction as an effective solution for powering rural areas.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's Analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL Analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Region, 2021 – 2034 (GW)

- 5.1 Key trends

- 5.2 North America

- 5.2.1 U.S.

- 5.2.2 Canada

- 5.2.3 Mexico

- 5.3 Europe

- 5.3.1 UK

- 5.3.2 Germany

- 5.3.3 France

- 5.3.4 Spain

- 5.3.5 Italy

- 5.3.6 Russia

- 5.3.7 Turkey

- 5.3.8 Norway

- 5.4 Asia Pacific

- 5.4.1 China

- 5.4.2 Japan

- 5.4.3 India

- 5.4.4 Australia

- 5.5 Rest of World

- 5.5.1 Brazil

- 5.5.2 Iran

Chapter 6 Company Profiles

- 6.1 24H - Hydro Power

- 6.2 Agder Energi

- 6.3 Andritz Hydro

- 6.4 Derwent Hydroelectric Power

- 6.5 Fortum

- 6.6 General Electric

- 6.7 Lanco Group

- 6.8 RusHydro

- 6.9 Siemens

- 6.10 Statkraft

- 6.11 Voith

2026-2034年全球小规模水力发电市场规模、份额、趋势和成长分析报告

2026-2034年全球小规模水力发电市场规模、份额、趋势和成长分析报告 日本小规模水力发电市场规模、份额、趋势和预测:按容量、组成部分和地区划分,2026-2034年

日本小规模水力发电市场规模、份额、趋势和预测:按容量、组成部分和地区划分,2026-2034年 2026年全球小型水力市场报告

2026年全球小型水力市场报告 小型水力发电市场-全球产业规模、份额、趋势、机会和预测,按类型、应用、容量(微型水力发电、小型水力发电)、组件、地区和竞争格局划分,2021-2031年预测

小型水力发电市场-全球产业规模、份额、趋势、机会和预测,按类型、应用、容量(微型水力发电、小型水力发电)、组件、地区和竞争格局划分,2021-2031年预测 小型水力市场规模、份额及成长分析(按容量、类型、组件和地区划分)-2026-2033年产业预测全球小型水力市场-2025-2030年预测

小型水力市场规模、份额及成长分析(按容量、类型、组件和地区划分)-2026-2033年产业预测全球小型水力市场-2025-2030年预测 全球小型水力发电市场:市场规模、市场占有率、趋势、行业分析(按类型、容量、组件和地区)、未来预测(2025-2034 年)

全球小型水力发电市场:市场规模、市场占有率、趋势、行业分析(按类型、容量、组件和地区)、未来预测(2025-2034 年) 小型水力市场:按组件、容量、类型和地区划分

小型水力市场:按组件、容量、类型和地区划分 小型水力市场规模、份额、趋势分析报告:按容量、类型、组件、地区、细分市场预测,2025-2030 年

小型水力市场规模、份额、趋势分析报告:按容量、类型、组件、地区、细分市场预测,2025-2030 年 亚太地区小水力发电 -市场占有率分析、产业趋势与统计、成长预测(2025-2030)

亚太地区小水力发电 -市场占有率分析、产业趋势与统计、成长预测(2025-2030)