|

市场调查报告书

商品编码

1666908

区域供热管网市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测District Heating Pipeline Network Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

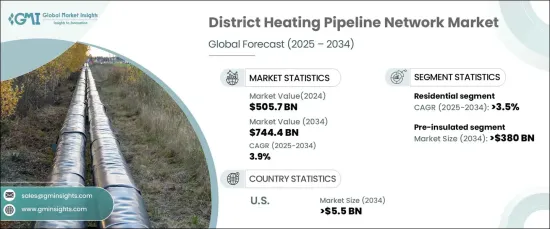

2024 年全球区域供热管道网路市场价值为 5057 亿美元,预计在 2025 年至 2034 年期间将以 3.9% 的复合年增长率稳步增长。区域供热管道透过减少热量损失、提高能源节约和符合全球永续发展目标,为现代能源挑战提供了解决方案。

随着城市人口的增加和政府实施更严格的能源标准,区域供热解决方案的采用将会加速。这些系统不仅提高了能源效率,而且显着降低了碳排放,使其成为智慧城市计画的基石。它们整合生物质能、太阳热能和地热能等再生能源的能力凸显了它们在创造有弹性、环保的基础设施方面的重要性。此外,经济效益(降低能源成本和长期运作效率)使区域供热管道成为全球住宅、商业和工业应用的有吸引力的投资。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 5057亿美元 |

| 预测值 | 7444亿美元 |

| 复合年增长率 | 3.9% |

随着永续基础设施投资的不断增加,预製绝缘区域供热管道网路预计到 2034 年将产生 3,800 亿美元的收入。这些管道经过精心设计,可承受高温并具有无与伦比的耐用性,非常适合需要大量供暖的地区。其创新设计最大限度地减少了热量损失,优化了能源消耗,并支持大型城市计画。随着开发商优先考虑节能技术,预绝缘管道已成为现代永续供热系统的代名词。它们在降低热效率和降低温室气体排放方面发挥作用,使其成为城市实现环境基准的关键解决方案。

在住宅领域,到 2034 年,区域供热管道市场预计将以 3.5% 的速度增长。区域供热系统为家庭供暖和供应热水提供了一种无缝且经济有效的方法,同时减少了对单一加热装置的依赖。它们与再生能源的兼容性进一步增强了它们的吸引力,使家庭能够转向更绿色的能源选择。随着各国政府强调碳中和和能源效率,住宅采用区域供热系统预计将激增,使其成为未来城市规划不可或缺的一部分。

在美国,区域供热管网市场预计到 2034 年将创收 55 亿美元。全国各地的城市正在实施先进的区域供热系统,以满足能源需求和脱碳目标。预製绝缘管道具有减少热损失、提高运作效率的能力,已成为城市供热项目中不可或缺的一部分。随着各市政当局努力降低温室气体排放并将再生能源纳入其框架,对尖端供热解决方案的需求持续上升,使得美国成为区域供热网路的关键市场。

目录

第 1 章:方法论与范围

- 市场范围和定义

- 市场估计和预测参数

- 预测计算

- 资料来源

- 基本的

- 次要

- 有薪资的

- 民众

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 监管格局

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- PESTEL 分析

第四章:竞争格局

- 介绍

- 战略展望

- 创新与永续发展格局

第五章:市场规模及预测:按管道,2021 – 2034 年

- 主要趋势

- 预绝缘钢

- 聚合物

第六章:市场规模及预测:依直径,2021 – 2034 年

- 主要趋势

- 20-100 毫米

- 101-300 毫米

- ≥300毫米

第 7 章:市场规模与预测:按应用,2021 – 2034 年

- 主要趋势

- 住宅

- 商业的

- 工业的

第 8 章:市场规模与预测:按地区,2021 – 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 波兰

- 瑞典

- 俄罗斯

- 义大利

- 英国

- 芬兰

- 丹麦

- 亚太地区

- 中国

- 日本

- 韩国

第九章:公司简介

- Aquatherm

- Brugg Pipes

- CPV

- Golan Plastic Products

- Isoplus

- Ke Kelit

- Logstor

- Mannesmann Line Pipe

- Microflex

- Perma-Pipe

- Pipelife

- Rehau

- Thermaflex

- Uponor

The Global District Heating Pipeline Network Market, valued at USD 505.7 billion in 2024, is set to grow at a steady CAGR of 3.9% between 2025 and 2034. This growth reflects a transformative shift toward sustainable energy technologies and a heightened demand for energy-efficient heating systems. District heating pipelines offer a solution to modern energy challenges by reducing heat loss, improving energy conservation, and aligning with global sustainability goals.

As urban populations expand and governments enforce stricter energy standards, the adoption of district heating solutions is poised to accelerate. These systems not only enhance energy efficiency but also significantly lower carbon emissions, making them a cornerstone of smart city initiatives. Their ability to integrate renewable energy sources such as biomass, solar thermal, and geothermal energy underscores their importance in creating resilient, eco-friendly infrastructure. Furthermore, the economic benefits-reduced energy costs and long-term operational efficiency-make district heating pipelines an attractive investment for residential, commercial, and industrial applications worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $505.7 Billion |

| Forecast Value | $744.4 Billion |

| CAGR | 3.9% |

The pre-insulated district heating pipeline network is anticipated to generate USD 380 billion by 2034, driven by increasing investments in sustainable infrastructure. These pipelines are engineered to endure high temperatures and deliver unmatched durability, making them ideal for regions with extensive heating requirements. Their innovative design minimizes heat loss, optimizes energy consumption, and supports large-scale urban projects. As developers prioritize energy-efficient technologies, pre-insulated pipelines have become synonymous with modern, sustainable heating systems. Their role in reducing thermal inefficiencies and lowering greenhouse gas emissions positions them as a pivotal solution for cities aiming to achieve environmental benchmarks.

In the residential sector, the district heating pipeline market is projected to grow at a rate of 3.5% through 2034. The rising preference for eco-friendly heating solutions in densely populated urban areas is a key factor propelling this growth. District heating systems provide a seamless and cost-effective method for heating homes and supplying hot water while reducing reliance on individual heating units. Their compatibility with renewable energy sources further enhances their appeal, enabling households to transition toward greener energy options. With governments emphasizing carbon neutrality and energy efficiency, residential adoption of district heating systems is expected to surge, making them an integral part of future urban planning.

In the United States, the district heating pipeline network market is forecasted to generate USD 5.5 billion by 2034. Significant investments in urban development and energy-efficient infrastructure are driving this growth. Cities across the country are implementing advanced district heating systems to meet energy mandates and decarbonization goals. Pre-insulated pipelines, with their ability to reduce thermal losses and improve operational efficiency, are becoming indispensable for urban heating projects. As municipalities strive to lower greenhouse gas emissions and incorporate renewable energy into their frameworks, the demand for cutting-edge heating solutions continues to rise, positioning the US as a pivotal market for district heating networks.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Pipe, 2021 – 2034 (km & USD Billion)

- 5.1 Key trends

- 5.2 Pre-insulated steel

- 5.3 Polymer

Chapter 6 Market Size and Forecast, By Diameter, 2021 – 2034 (km & USD Billion)

- 6.1 Key trends

- 6.2 20-100 mm

- 6.3 101-300 mm

- 6.4 ≥300 mm

Chapter 7 Market Size and Forecast, By Application, 2021 – 2034 (km & USD Billion)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial

- 7.4 Industrial

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (km & USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 Poland

- 8.3.3 Sweden

- 8.3.4 Russia

- 8.3.5 Italy

- 8.3.6 UK

- 8.3.7 Finland

- 8.3.8 Denmark

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 South Korea

Chapter 9 Company Profiles

- 9.1 Aquatherm

- 9.2 Brugg Pipes

- 9.3 CPV

- 9.4 Golan Plastic Products

- 9.5 Isoplus

- 9.6 Ke Kelit

- 9.7 Logstor

- 9.8 Mannesmann Line Pipe

- 9.9 Microflex

- 9.10 Perma-Pipe

- 9.11 Pipelife

- 9.12 Rehau

- 9.13 Thermaflex

- 9.14 Uponor

区域供热市场按应用、管网类型、厂容、能源来源、最终用途和供热温度划分-2025-2032年全球预测

区域供热市场按应用、管网类型、厂容、能源来源、最终用途和供热温度划分-2025-2032年全球预测 2025年区域供热全球市场报告

2025年区域供热全球市场报告 区域供热市场机会、成长动力、产业趋势分析及2025-2034年预测

区域供热市场机会、成长动力、产业趋势分析及2025-2034年预测 区域供热市场 - 2025 年至 2030 年预测全球热力网路市场

区域供热市场 - 2025 年至 2030 年预测全球热力网路市场 区域供热的全球市场:厂房类型·热源·用途·各地区 (~2032年)区域供热市场规模、份额、趋势分析报告:按热源、应用、工厂类型、地区、细分市场预测,2025-2030 年

区域供热的全球市场:厂房类型·热源·用途·各地区 (~2032年)区域供热市场规模、份额、趋势分析报告:按热源、应用、工厂类型、地区、细分市场预测,2025-2030 年 按工厂类型、热源、应用和地区分類的区域供热市场

按工厂类型、热源、应用和地区分類的区域供热市场 区域供热:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)英国区域供热 -市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

区域供热:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)英国区域供热 -市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)