|

市场调查报告书

商品编码

1692507

英国区域供热 -市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)UK District Heating - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

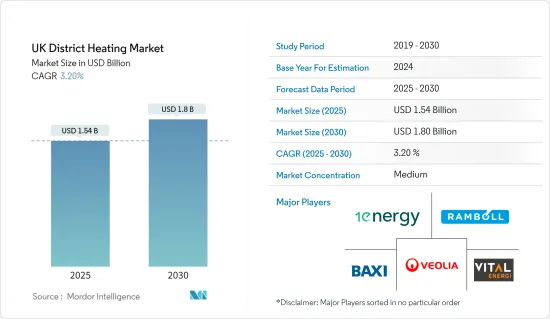

英国区域供热市场规模预计在 2025 年为 15.4 亿美元,预计到 2030 年将达到 18 亿美元,预测期内(2025-2030 年)的复合年增长率为 3.2%。

主要亮点

- 根据永续发展情境(SDS),区域供热、热泵、可再生能源供热和氢气等清洁供热技术预计将促进区域供热网路的销售并对市场需求产生积极影响。

- 对节能供暖解决方案的需求不断增长,推动了新技术的采用。根据英国政府的一项研究,预计到2030年,英国14-20%的供暖需求将由热力网络满足,到2050年这一比例将达到43%。英国消耗的能源中约有一半用于供热。商业、住宅和公共部门占最终能源消耗的三分之二。热量主要用于住宅/家庭和商业建筑的热水和空间供暖。

- 第五代区域供热系统正成为现有第四代区域供热系统的新替代方案。第五代区域供热製冷系统是一种双向、分散、近地面温度网络,透过利用冷储存和热回流直接交换来完美平衡热量需求。

- 政府也主导了多项扩大该国热力网络的倡议,为所研究市场的成长创造了良好的前景。例如,2022 年底,英国政府宣布从政府 3.2 亿英镑(3.99 亿美元)的热力网络投资计划(HNIP) 中拨款 1,910 万英镑(2,380 万美元),旨在支持英格兰和威尔斯的热力网络。

- 然而,与市场替代方案相比,区域供热系统属于资本密集系统。 DHC 系统需要沟渠网路以及泵浦和系统的持续维护。这些因素阻碍了对 DHC 系统的需求。

- 此外,在现有城市和建筑物中安装区域供热水管非常困难且成本高昂,使安装过程变得复杂,因此继续对所研究市场的成长构成重大挑战。

英国区域供热市场趋势

都市化和工业化进程不断加快,推动市场

- 英国和世界各地的快速都市化正在推动需求并支持向再生能源来源的转变,以实现中央供暖和製冷。这有助于减少二氧化碳排放,提高效率并满足都市区日益增长的能源需求,并提供具有成本效益的温度控制。例如,在英国,都市化导致北部地区集中式系统的使用迅速增加。

- 根据世界银行预测,到2022年英国都市化将达到84.39%,比过去十年提高了近三个百分点。儘管成长缓慢,但趋势始终是正面的,对市场成长产生了重大影响。

- 鑑于寒冷天气条件的普遍性,英国在全球 DHC 解决方案需求中所占份额过大,大部分配电网路位于该地区的都市区。该地区在 20 世纪下半叶发展了广泛的供热基础设施。它们仍然是都市区供暖和热水的主要能量。

- 区域能源系统受益于并支持这样的环境,并且本质上适合城市景观。由于该技术与环境条件和劳动力需求协同效应,因此非常适合城市人口。城市中心的发展促进了区域网络的建立。英国、伦敦、威尔斯和诺丁汉就是典型的例子。除了需要一定规模的开发外,热管网的高资本成本还要求在尽可能小的空间内提供能源服务,以最大限度地增加最终用户的数量。因此,密集的城市发展非常适合分散供暖。

住宅和家庭领域占据了很大的市场占有率

- 家庭供暖占英国总排放的近 14%(根据政府研究所的数据),需要紧急解决,以符合政府实现碳减排目标的雄心。区域供热是向英国各地家庭提供低碳热能的有效解决方案。目前,英国仅有 2% 多一点的住宅接入区域供热网路(根据能源节约信託基金的数据),但随着英国在未来几十年内逐步实现净零排放,预计会有更多住宅接入区域供热网路。

- 英国目前安装的大多数区域供热系统都采用燃气热电联产 (CHP) 系统。公寓大楼或多用户住宅中的单一热电联产装置通常效率较高,并且比每个家庭中的燃气锅炉所需的维护更少。英国政府气候变迁委员会 (CCC) 预测,到 2050 年,约有 12% 的家庭供暖将由区域供热提供。

- 英国有超过 17,000 个供热网络,连接约 50 万人。在人口密集的都市区,热力网络被视为特别有吸引力的选择。热网是解决燃料贫穷问题并降低住宅管理成本的有效方法。

- 热力网络可以是任意规模,并且可以随着时间的推移添加更便宜、低碳的热源,而无需进行挖掘道路或重建住宅等重大变化。因此,住宅领域减少碳排放的力道不断加大将支持研究市场的成长。例如,根据英国商业、能源和产业战略部等消息来源,预计2040年英国住宅房地产领域的二氧化碳排放将达到6,800万吨。

- 此外,英国计划于2025年实施的未来住宅标准将要求新建住宅的二氧化碳排放量比按照现行标准建造的住宅减少75%至80%。为了从电网脱碳和供暖电气化中受益,住宅需要「零碳准备」并且不需要进行任何维修。新建住宅可能会禁止使用石化燃料供暖,从而转向热网等低碳供暖技术。

英国区域供热产业概况。

英国区域供热市场竞争适中,主要参与者包括 Vital Energi、1 Energy Group Limited、Baxi Heating UK、Ramboll UK Limited 和 Veolia Environnement SA。市场上的公司正在采取联盟和收购等策略来增强其产品供应并获得永续的竞争优势。

2023年5月,英国政府向英格兰各地七个尖端热力网路计划提供政府资助。其中包括英国首个地下热能提取系统,该系统有可能为约 4,000 户家庭提供低成本暖气。英国政府表示,这些已确定的计划将从政府的绿色热能网路基金中获得 9,100 万英镑(1.136 亿美元)的资助。

2023 年 4 月,电力公司 Pinnacle Power 与 DIF Capital Partners 签署协议,在英国各地建造和部署价值 10 亿英镑(12.5 亿美元)的低碳热力网路。两家公司之间的新伙伴关係将加速「城镇规模热力网络」的推出,这可能有助于英国各地多个住宅和建筑的脱碳。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 技术分析

- 宏观经济情势如何影响市场

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 竞争对手之间的竞争强度

- 替代品的威胁

- 产业供应链分析

- 政府措施和计划

- 区域供热合约/现场竞标

第五章市场动态

- 市场驱动因素

- 对节能、经济的暖气系统的需求不断增加

- 都市化和工业化进程

- 市场挑战

- 基础设施成本高

第六章市场区隔

- 按最终用户

- 住宅/家庭用途

- 非家庭用途

- 热网能源结构现况及未来趋势

- 按行业和客户分類的热网连接数量

- 热能储存的使用与未来的可能性

- 基于区域的热网密度

- 消费者对热力网络的态度

- 热网机会

第七章竞争格局

- 公司简介

- Vital Energi Utilities Ltd.

- 1Energy Group Limited

- Baxi Heating UK

- Ramboll UK Limited

- Veolia Environnement SA

- Sweco UK(AWECO AB)

- Vanttenfall(Vattenfall AB)

- Equans Services Limited

- E.ON PLC

第八章投资分析

第九章:市场的未来

The UK District Heating Market size is estimated at USD 1.54 billion in 2025, and is expected to reach USD 1.80 billion by 2030, at a CAGR of 3.2% during the forecast period (2025-2030).

Key Highlights

- To meet the Sustainable Development Scenario (SDS), clean heating technologies, such as district heating, heat pumps, and renewable and hydrogen-based heating, are expected to increase the sales of district heating networks, positively influencing market demand.

- The rising demand for energy-efficient heating solutions is pushing for the adoption of new technologies. As per the UK government's research, 14-20 percent of the heat demand in the United Kingdom is expected to be met by heat networks by 2030 and 43 percent by 2050. Around half of the energy consumed in the United Kingdom is used as heat. The commercial, domestic, and public sectors accounted for two-thirds of the final energy consumption. Heat is primarily used for water and space heating in residential/domestic and commercial buildings.

- The fifth generation is emerging as a new system to replace the existing fourth-generation district heating system. 5th generation district heating & cooling systems are bi-directional, decentralized, close-to-ground temperature networks that use the direct exchange of cold and warm thermal storage and return flows to balance the thermal demand in full measure.

- Several government-led initiatives to expand the heat networks in the country also create a favorable outlook for the growth of the studied market. For instance, in late 2022, the UK Government announced GBP19.1 million (USD 23.8 million) funding that came from the government's GBP320 million (USD 399 million) Heat Networks Investment Project (HNIP), aimed at supporting heat networks across England and Wales.

- However, district heating systems are more capital-intensive as compared to alternatives in the market. The DHC system requires a network of trenches and continuous maintenance of pumps and systems. These factors hinder the demand for DHC systems.

- Furthermore, it becomes difficult and costly to install distribution pipes for district heating in pre-existing cities/buildings that were not planned for such features, thereby adding complexity to the installation process, which continues to remain among the major challenging factors for the growth of the studied market.

UK District Heating Market Trends

Rising Urbanization and Industrialization to Drive the Market

- Rapid urbanization across the world, including in the UK, is driving the demand and pushing the switch to renewable energy sources for centralized heating & cooling, which can help reduce CO2 emissions, improve efficiency, increase urban energy needs, and provide cost-effective temperature control. For instance, driven by urbanization, the United Kingdom has rapidly increased its use of centralized systems in its northern regions.

- In the United Kingdom, urbanization amounted to 84.39% in 2022, as per the World Bank. This presents almost a three percentage point increase over the past decade. Though slow, the upward trend has been consistently positive, significantly influencing the market growth.

- Considering the prominence of cold weather conditions, the UK commands a prominent share of the global demand for DHC solutions, and a major share of the distribution network is situated in urban areas in the region. Large heat distribution infrastructures were developed during the second half of the 20th century in the region. These remain the principal ways to provide energy for space and water heating in urban areas.

- District energy systems benefit from and support this environment and are inherently appropriate to urban landscapes. The technology's synergy with the environmental conditions and the working population's needs are well suited for urban demographics. The growth of urban centers facilitates the construction of district networks. England, London, Wales, and Nottingham are some of the best examples in the market. In addition to requiring a particular scale of development, the high capital costs of heat networks demand energy services be delivered in the tightest space possible to maximize the number of end users. Thus, dense urban developments are highly suitable for distributed heat provision.

Residential and Domestic Segment Holds Significant Market Share

- Domestic heating accounts for nearly 14 percent of all emissions in the United Kingdom (according to the Institute for Government) and needs to be tackled urgently in line with the government's aim to meet its carbon reduction targets. District heating offers an effective solution for the supply of low-carbon heat to homes across the United Kingdom. While just over 2 percent of residences in the United Kingdom are currently connected to a district heating network (as per Energy Saving Trust), more are expected to come online as the country transitions to net zero over the coming decades.

- Most district heating systems currently installed in the United Kingdom use a gas-powered combined heat and power system (CHP), which generates electricity. A single CHP is usually more efficient in a housing estate or block of flats and requires less maintenance than a gas-powered boiler in every flat or house. The UK government's Committee for Climate Change (CCC) estimates that around 12 percent of domestic heat will be supplied by district heating by 2050.

- There are over 17,000 heat networks in place in the United Kingdom, and around half a million connections to them, most of them being domestic customers (as per Energy Saving Trust). They are perceived as a particularly attractive option in dense urban areas. They are an effective way of dealing with fuel poverty while reducing housing management costs.

- The establishment of heat networks, which can vary widely in size, implies that cheaper, lower-carbon sources of heat generation can be added over time without abrupt changes, such as digging up roads or changing people's homes. Hence, the growing efforts to reduce the carbon footprint of the residential sector will support the studied market's growth. For instance, according to sources like the UK Department for Business, Energy and Industrial Strategy, carbon dioxide emission from the residential real estate sector in the United Kingdom is anticipated to reach 68 million metric tons by 2040.

- Furthermore, the Future Homes Standard, expected to be introduced in the United Kingdom in 2025, requires carbon emissions produced by new homes to be around 75-80 percent lower than those built to current standards. Houses will have to be 'zero carbon ready,' with no retrofit work needed to benefit from the electricity grid's decarbonization and the heating's electrification. Fossil fuel heating may be banned in new houses, with an expected shift toward low-carbon heating technologies, such as heat networks.

UK District Heating Industry Overview

The UK district heating market is moderately competitive, with the presence of major players like Vital Energi, 1 Energy Group Limited, Baxi Heating UK, Ramboll UK Limited, and Veolia Environnement SA. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

In May 2023, the UK Government awarded government funding to 7 state-of-the-art heat network projects across England, which includes the UK's first system drawing heat from underground, with the potential of providing low-cost heating for nearly 4,000 homes. According to the government, the identified projects will receive a share of GBP 91 million (USD 113.6 million) from the government's Green Heat Network Fund.

In April 2023, Utility company Pinnacle Power entered an agreement with DIF Capital Partners to build and deploy GBP 1 billion (USD 1.25 billion) worth of low-carbon heat networks across the UK. The new partnership between the companies will accelerate the deployment of "town-and-city-scale heat networks" that will likely help to decarbonize several homes and buildings across the country.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Technological Analysis

- 4.3 Impact of Macroeconomic Scenarios on the Market

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Intensity of Competitive Rivalry

- 4.4.5 Threat of Substitutes

- 4.5 Industry Supply Chain Analysis

- 4.6 Government Initiatives and Programs

- 4.7 District Heating Contracts/Live Tenders

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Augmented Demand for Energy-efficient and Cost-effective Heating Systems

- 5.1.2 Rising Urbanization and Industrialization

- 5.2 Market Challenges

- 5.2.1 High Infrastructure Cost

6 MARKET SEGMENTATION

- 6.1 By End User

- 6.1.1 Residential/Domestic

- 6.1.2 Non-domestic

- 6.2 Current Energy Mix of Heat Networks and Future Trends

- 6.3 Heat Network Connections by Sectors and Customers

- 6.4 Thermal Storage Usage and Future Potential

- 6.5 Heat Networks Density Based on Regions

- 6.6 Consumer Attitudes to Heat Networks

- 6.7 Opportunities for Heat Network

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Vital Energi Utilities Ltd.

- 7.1.2 1Energy Group Limited

- 7.1.3 Baxi Heating UK

- 7.1.4 Ramboll UK Limited

- 7.1.5 Veolia Environnement SA

- 7.1.6 Sweco UK (AWECO AB)

- 7.1.7 Vanttenfall (Vattenfall AB)

- 7.1.8 Equans Services Limited

- 7.1.9 E.ON PLC

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

住宅区域供热市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2024-2032 年)商业区域供热市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2024-2032)

住宅区域供热市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2024-2032 年)商业区域供热市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2024-2032) 区域供热市场按应用、管网类型、厂容、能源来源、最终用途和供热温度划分-2025-2032年全球预测

区域供热市场按应用、管网类型、厂容、能源来源、最终用途和供热温度划分-2025-2032年全球预测 2025年区域供热全球市场报告

2025年区域供热全球市场报告 区域供热市场机会、成长动力、产业趋势分析及2025-2034年预测区域供热市场 - 2025 年至 2030 年预测

区域供热市场机会、成长动力、产业趋势分析及2025-2034年预测区域供热市场 - 2025 年至 2030 年预测 全球热力网路市场

全球热力网路市场 区域供热的全球市场:厂房类型·热源·用途·各地区 (~2032年)

区域供热的全球市场:厂房类型·热源·用途·各地区 (~2032年) 区域供热市场规模、份额、趋势分析报告:按热源、应用、工厂类型、地区、细分市场预测,2025-2030 年

区域供热市场规模、份额、趋势分析报告:按热源、应用、工厂类型、地区、细分市场预测,2025-2030 年 按工厂类型、热源、应用和地区分類的区域供热市场

按工厂类型、热源、应用和地区分類的区域供热市场