|

市场调查报告书

商品编码

1644598

欧洲区域供热 -市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Europe District Heating - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

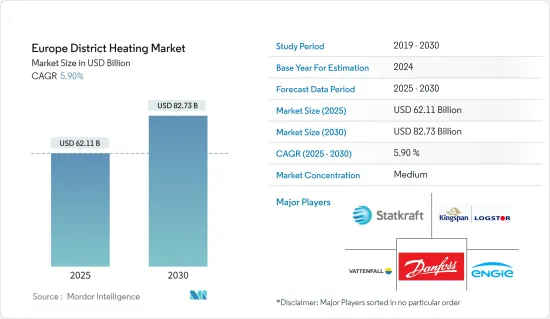

预计 2025 年欧洲区域供热市场规模为 621.1 亿美元,到 2030 年将达到 827.3 亿美元,预测期内(2025-2030 年)的复合年增长率为 5.9%。

机器学习、物联网服务和智慧电錶等新技术的引入有助于优化加热週期,以满足欧洲各地的不同需求。

关键亮点

- 区域供热系统有助于提高能源效率并降低住宅和商业用户的成本。预计该解决方案的需求会很高,尤其是在欧洲。预计未来几年的投资将会更高。根据欧洲热路线图的资料,如果都市化趋势持续下去并且实施正确的投资,到 2050 年区域供热可以满足欧洲近一半的热量需求。

- 目前,约有 6,000 万欧盟公民使用区域供热,另有 1.4 亿欧盟公民居住在至少拥有一个区域供热系统的城市。根据欧盟和国际能源总署的报告,区域供暖目前透过 6,000 个区域供热和製冷网路满足了欧盟约 11-12% 的热量需求。

- 世界各国政府越来越重视从石化燃料转向可再生能源,预计将为区域供热市场的创新提供重大机会。例如,2022年2月,欧洲暖气市场同意逐步淘汰化石气体,这是非政府组织和工业界的联合倡议。

- 例如芬兰计划在2030年将可再生能源在其能源消耗中的比例提高到50%左右。此外,也公布了2030年中期气候变迁计画。芬兰计划在2030年前逐步关闭燃煤热电联产电厂,并在2025年前为转向高效能生质热电联产和新供热技术的营运商提供资金支持。由于电厂退役,区域供热热电联产容量预计会下降。其余区域供热热电联产电厂可转换为 100% 生质能。

- 此外,随着世界各地(尤其是欧洲)越来越关注脱碳,正在实施多项措施和计划,促进区域供热系统从石化燃料转向再生能源的转变。此外,Vattenfall AB 计划对其在该城市的生产组合进行脱碳。脱碳过程将首先涉及2030年逐步淘汰煤炭/煤炭,随后在2050年取代化石气体。

- 然而,安装区域供热系统通常需要大量的前期投资成本。这一成本因素可能成为市场成长的限制因素。区域供热系统可能还需要协助,为较小的供热负载或电网空间有限的地区提供有效的供热解决方案。

- 此外,俄罗斯入侵乌克兰对全球,特别是欧洲的能源和粮食市场产生重大影响。自2021年下半年以来,该地区能源价格急剧上涨。俄乌战争导致燃料价格上涨,也引发民众对该地区能源供应安全的担忧。俄罗斯决定切断对多个欧盟成员国的天然气供应,进一步影响了局势。

欧洲暖气市场的趋势

住宅终端用户市场预计将占据主要市场占有率

- 在欧洲,透过区域供热系统的住宅消费占有很大份额。这导致大量碳排放,阻碍2050年零排放的目标实现。因此,各国政府正在积极制定法规,以有效管理居民的区域供热。多家公司正在创新有效的解决方案来应对欧洲紧迫的能源挑战和不断上升的碳排放。例如,2022年2月,威尔斯启动了氢气加热试验,以测试「世界上第一个氢混合加热系统」。

- 此外,英国政府目前正在为热泵的初始资本支出提供资助,其中空气源热泵的成本和安装资助最高可达 5,000 英镑(约 6,110 美元),地源热泵的资助最高可达 6,000 英镑(约 7,332 美元)。然而,电热泵的初始安装成本仍然是全国许多潜在用户的障碍。

- 根据欧盟委员会统计,建筑物占欧洲能源消耗的40%。冷气、暖气、生活热水等各种功能占居民能源消耗的80%。这显示家庭和建筑物区域供热系统所需的能源总量,需要更好的能源管理。因此,欧洲向开发更环保的空间供暖和其他中东和北非供暖相关服务解决方案的公司敞开了大门。

- 欧盟委员会也指出,超过3000万栋建筑物能源消耗过高。这笔超额消耗大约是普通建筑物的2.5倍,从而推高了家庭能源费用。这凸显了欧洲家庭的高能源需求,但同时也显示实施节能区域供热解决方案也有空间。公司正在安装由可再生能源驱动的个人化暖气解决方案。

- 随着电费上涨,家庭每天都依靠天然气来提供暖气系统。天然气也是一种可以储存并加以充分利用的石化燃料。安装由太阳能或地热等可再生能源驱动的暖气系统可以有效管理能源成本,并为减少二氧化碳排放、实现欧洲 2050 年的环境目标做出积极贡献。

预计德国将引领欧洲市场成长

- 根据德国联邦统计局的数据,截至2022年12月31日,德国人口为8,436万,高于2021年的8,324万。根据climate-data.org报导,德国的年平均气温约为 8.7 度。这些人口统计数据表明,德国主要属于寒冷地区,人口密集,是建立区域供热厂的理想地区。

- 德国的能源消费价格整体高于其他地区。例如,根据globalpetrolprices.com的数据,2022年9月德国住宅用电价为0.620美元/千瓦时,企业用电价为0.918美元/千瓦时,而全球平均住宅用电价为0.335美元/千瓦时,企业用电价为0.261美元/千瓦时。这清楚地表明了为了应对不断上涨的电费,建筑物对替代热水和加热解决方案的需求。因此,德国是区域供热解决方案和热泵的一个有前景的市场。

- 多项政府法规正在促进区域供热领域采用可再生能源,并鼓励企业使用先进技术。德国政府制定了 2050 年气候行动计划,采取了长期而严肃的方针。例如,根据联邦环境、自然保护、核能安和消费者保护部 (BMUV) 的说法,气候行动计划的目标是到 2030 年将二氧化碳排放在 1990 年的基础上减少 66-67%,到 2050 年在德国全国范围内实现几乎气候中性的供热。这些热情的倡议为其他热衷于在德国实施更环保的区域供热解决方案的公司铺平了道路。

- 在德国,区域供热几乎仅用于普通家庭供暖。工业供暖消耗往往高度依赖经济趋势,製造业倾向于使用区域供热和製冷而不是工业製程。在商业和贸易服务中,它用于供暖以及热水和其他加热和冷却过程。

- 在德国,区域供热和製冷被视为减少初级能源消耗和提高德国供应安全性的一项特别重要的措施。据区域供热协会AGFW称,到2030年,区域供热与热电联产相结合可以减少4%的初级能源消耗和15%的国内能源进口。

欧洲供热产业概况

欧洲区域供热市场呈现半整合状态,主要参与者包括 Vattenfall AB、Danfoss AS、Engie SA、Statkraft AS 和 Logstor AS。市场参与企业正在采取联盟和收购等策略来加强其产品供应并获得可持续的竞争优势。

2022 年 9 月,德国政府宣布了一项为期 2026 年的 30 亿欧元(32 亿美元)补贴计划,用于支持建设使用至少 75%可再生能源的区域供热网路。

2023 年 4 月,都柏林理工学院宣布将在都柏林能源机构 Codema 的支持下与南都柏林郡议会 (SDCC) 合作,建造爱尔兰首个低碳区域供热系统。非营利 Heatworks 区域供热网络最初将为都柏林理工大学和圣地亚哥社区学院的 32,800平方公尺公共建筑供热,併计划到 2025 年扩大到为 133 套经济适用公寓供热。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- 产业价值链分析

- 宏观经济趋势如何影响市场

- 政府针对区域供热和製冷转型的倡议和计划

- 区域供热技术的发展

第五章 市场动态

- 市场驱动因素

- 对节能、经济的暖气系统的需求不断增加

- 都市化和工业化进程

- 市场问题

- 基础设施成本高

第六章 市场细分

- 按最终用户

- 住宅

- 商业/工业

- 按国家

- 德国

- 法国

- 波兰

- 捷克共和国

- 奥地利

第七章 竞争格局

- 公司简介

- Vattenfall AB

- Danfoss AS

- Engie SA

- Statkraft AS

- Logstor AS

- Vital Energi Ltd

- Goteborg Energi

- Alfa Laval AB

- Ramboll Group AS

第八章投资分析

第九章:未来市场展望

The Europe District Heating Market size is estimated at USD 62.11 billion in 2025, and is expected to reach USD 82.73 billion by 2030, at a CAGR of 5.9% during the forecast period (2025-2030).

Introducing new technologies like machine learning, IoT services, and smart meters has helped optimize the heating cycles according to the varying demands in Europe.

Key Highlights

- A district heating system helps achieve energy efficiency and reduces the cost for both residential and commercial users. The demand for the solutions is expected to be particularly high in Europe. It is expected to see higher investments over the coming years. According to the Heat Roadmap Europe data, if the urbanization trend continues and appropriate investments are implemented, district heating could meet almost half of Europe's heat demand by 2050.

- Approximately 60 million EU (European Union) citizens are currently served by district heating, with an additional 140 million people living in cities with at least one district heating system. According to EU and the IEA reports, DH currently meets around 11-12 percent of the EU's heat demand via 6,000 district heating and cooling networks.

- The increasing focus on the shift toward renewable energy sources, instead of fossil fuels, by the governments of multiple countries across the globe is expected to offer great opportunities for innovations in the district heating market. For instance, in February 2022, the European heating market agreed to phase out fossil gas, a joint decision undertaken by NGOs and industry.

- For instance, Finland plans to increase the renewable energy share in its energy consumption to about 50 percent by 2030. Further, a medium-term climate change plan for 2030 was released. Finland plans to close coal-fired CHP plants slowly by 2030, along with financially supporting operators that switch to efficient biomass CHP and new heating technologies by 2025. It is expected to decrease the district heating CHP capacity due to the decommissioning of plants. The remaining district heating CHP plants can be converted to 100 percent biomass.

- Additionally, the increasing decarbonization initiatives across the globe, specifically in Europe, led to initiatives and programs that fuel the transition of district heating systems from fossil fuels to renewables. Moreover, Vattenfall AB has plans to decarbonize its production portfolio in the cities. The decarbonization process is expected to be implemented first, with the coal/peat phase-out by 2030, followed by the replacement of fossil gas by 2050.

- However, the installation of district heating systems often requires significant initial investment costs. This cost factor can act as a restraint on the market growth. The district heating systems may also need help in providing efficient heating solutions for small heating loads or in areas with limited space for distribution grids.

- Moreover, Russia's invasion of Ukraine has highly impacted energy and food markets across the globe, especially in Europe. Since the second half of 2021, there has been a sharp increase in energy prices in the region. The price of fuels has risen as a consequence of the Russia-Ukraine war, which has also led to concerns related to the security of the energy supply in the region. Russia's decision to suspend gas deliveries to several EU member states has further impacted the situation.

Europe District Heating Market Trends

Residential End User Segment is Expected to Hold Significant Market Share

- The residential consumption from the district heat systems accounts for a major share in Europe. This leads to many carbon emissions, hampering the countries' zero-emission goals of 2050. Hence, governments are actively forming regulations to manage district heat among residents efficiently. Several companies are innovating efficient solutions to cope with the pressing energy problems and increasing carbon emissions in Europe. For instance, in February 2022, a hydrogen heating trial began in Wales to test the 'world's first hydrogen hybrid heating system.

- Further, the UK Government is presently offering contributions to the initial capital outlay on heat pumps, with GBP 5,000 (~USD 6,110) of the cost and installation of an air source heat pump and GBP 6,000 (~USD 7,332) for ground source heat pumps. However, the initial installation costs of an electric heat pump are still an off-putting hurdle to many potential users in the country.

- According to the European Commission, Buildings account for 40 percent of Europe's energy consumption. Various functions like cooling, heating, and domestic hot water form 80 percent of the energy consumed by the citizens. This indicates the total energy requirement for district heating systems for households and buildings, demanding better energy management. Hence, the European region is open to companies developing greener solutions for space heating and other district heating-related services.

- The European Commission also indicates that more than 30 million building units consume excessive energy. This excess consumption accounts for nearly 2.5 times more than average buildings, which drives up households' energy bills. It highlights the high energy requirements for families in Europe, but it also makes room for energy-efficient district heating solutions. Companies are introducing individual heating solutions using renewable energy resources.

- As the electricity prices hike, households rely on natural gas to fuel their heating systems daily. Natural gas is another fossil fuel that can be preserved and put to better use. Introducing heating systems fueled by renewable energy resources like solar energy, geothermal energy, and others will help manage the energy expenses effectively and contribute actively to reducing the CO2 emission footprint for 2050 environmental goals in Europe.

Germany is anticipated to Drive the Market Growth in Europe

- According to the Federal Statistical Office (Germany), in 2022, the population in Germany, as of December 31 of that year, amounted to 84.36 million people, an increase from 83.24 million in 2021. The average annual temperature in Germany, reported by climate-data.org, is about 8.7 degrees Celsius. These demographics show Germany's primarily cold and densely populated demography, making it a perfect region for district heating facilities.

- The overall prices for energy consumption are higher in Germany compared to other regions. For instance, according to globalpetrolprices.com, the electricity prices in Germany in September 2022 accounted for USD 0.620 USD per kWh for households and 0.918 USD for businesses, compared to the world average electricity prices of USD 0.335/kWh for households and USD 0.261/kWh for businesses. This clearly states how the demand for alternative hot water and heating solutions for buildings becomes necessary to tackle the high electricity prices. Hence, Germany is a promising district heating solutions and heat pumps market.

- Several Government regulations promote the adoption of renewable energy resources in the district heating sector, encouraging the companies to use advanced technologies. The German government takes serious and long-term steps under the Climate Action Plan 2050. For instance, according to BMUV (Federal Ministry for the Environment, Nature Conservation, Nuclear Safety, and Consumer Protection), the Climate Action Plan aims to reduce CO2 emissions by 66-67 percent by 2030 compared to the emissions in 1990, to achieve virtually climate-neutral heat by 2050 across Germany. Such dedicated measures pave the way for companies looking forward to introducing greener district heating solutions in the country.

- In German private households, district heating is used for the most part for space heating. Heating consumption in the industry tends to be more dependent on economic developments; manufacturing businesses tend to use district heating and cooling instead of industrial processes. In the commerce/trade/services sector, in addition to using space heating, use for heating water and other heating and cooling processes also plays a role.

- In Germany, district heating and cooling are considered a particularly important instrument in reducing primary energy consumption and improving Germany's security of supply. According to the district heating association AGFW, until 2030, the combined use of district heating and combined heat and power production could reduce primary energy consumption by 4 percent and national energy imports by 15 percent.

Europe District Heating Industry Overview

The European district heating market is Semiconsloidated, with the presence of major players like Vattenfall AB, Danfoss AS, Engie SA, Statkraft AS, and Logstor AS. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

In September 2022, The German government announced the EUR 3 billion (USD 3.20 billion) subsidy scheme until 2026 that would sustain the construction of district heating grids that use at least 75 percent renewable energy.

In April 2023, TU Dublin, in collaboration with South Dublin County Council (SDCC) with the assistance of the Dublin energy agency, Codema, announced that it would be part of Ireland's first low-carbon sourced district heating system, with its Tallaght campus part of an innovative, low-carbon initiative. The not-for-profit Heatworks district heating network will initially provide heat to 32,800 sq mts of local public buildings at TU Dublin and SDCC, expanding to heat 133 affordable apartments in 2025.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Defnition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 The Impact of Macroeconomic Trends on the Market

- 4.5 Government Initiatives and Programs on District Heating/Cooling Transition

- 4.6 Development of District Heating Technology

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Augmented Demand for Energy-efficient and Cost effective Heating Systems

- 5.1.2 Rising Urbanization and Industrialization

- 5.2 Market Challenges

- 5.2.1 High Infrastructure Cost

6 MARKET SEGMENTATION

- 6.1 By End User

- 6.1.1 Residential

- 6.1.2 Commercial and Industrial

- 6.2 By Country

- 6.2.1 Germany

- 6.2.2 France

- 6.2.3 Poland

- 6.2.4 Czech Republic

- 6.2.5 Austria

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Vattenfall AB

- 7.1.2 Danfoss AS

- 7.1.3 Engie SA

- 7.1.4 Statkraft AS

- 7.1.5 Logstor AS

- 7.1.6 Vital Energi Ltd

- 7.1.7 Goteborg Energi

- 7.1.8 Alfa Laval AB

- 7.1.9 Ramboll Group AS

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF MARKET

住宅区域供热市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2024-2032 年)

住宅区域供热市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2024-2032 年) 区域供热市场按应用、管网类型、厂容、能源来源、最终用途和供热温度划分-2025-2032年全球预测

区域供热市场按应用、管网类型、厂容、能源来源、最终用途和供热温度划分-2025-2032年全球预测 2025年区域供热全球市场报告

2025年区域供热全球市场报告 区域供热市场机会、成长动力、产业趋势分析及2025-2034年预测区域供热市场 - 2025 年至 2030 年预测

区域供热市场机会、成长动力、产业趋势分析及2025-2034年预测区域供热市场 - 2025 年至 2030 年预测 全球热力网路市场

全球热力网路市场 区域供热的全球市场:厂房类型·热源·用途·各地区 (~2032年)

区域供热的全球市场:厂房类型·热源·用途·各地区 (~2032年) 区域供热市场规模、份额、趋势分析报告:按热源、应用、工厂类型、地区、细分市场预测,2025-2030 年

区域供热市场规模、份额、趋势分析报告:按热源、应用、工厂类型、地区、细分市场预测,2025-2030 年 按工厂类型、热源、应用和地区分類的区域供热市场

按工厂类型、热源、应用和地区分類的区域供热市场 区域供热:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

区域供热:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)