|

市场调查报告书

商品编码

1689777

区域供热:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)District Heating - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

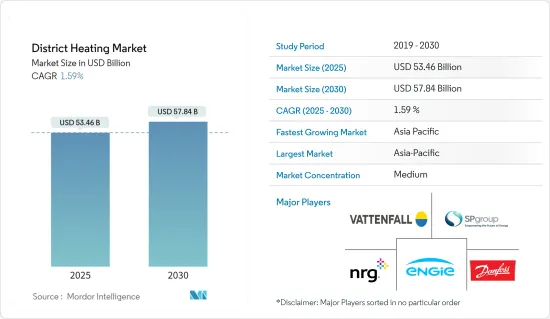

区域供热市场规模预计在 2025 年为 534.6 亿美元,预计到 2030 年将达到 578.4 亿美元,预测期内(2025-2030 年)的复合年增长率为 1.59%。

受全球经济体设定的积极气候目标的推动,区域能源是全球快速成长的产业。初步评估发现,这些区域供热和冷冻公司透过替代持有结构具有更大的机会实现惊人的成长和价值潜力。在区域供热供应中加入电热泵可以使更高水准的可再生能源用于供热目的,从而实现能源系统之间的整合和平衡。随着全球风力发电机容量的快速增加,大型热泵将在2050年维持绿色能源发展和摆脱石化燃料发挥关键作用。

主要亮点

- 区域供热是一种透过高度绝缘的管道分配网以热水的形式向建筑物(住宅或商业)提供热能的方法。将工业製程转化为区域供热的可能性有限,因为热负荷因工业和製程的类型而异,因此扩大工业区域供热使用的潜力有限。

- 然而,转向区域供热可减少 11% 的电力使用和 40% 的石化燃料使用,将整个产业的最终能源使用量降低 6%。

- 转变工业流程每年可减少全球二氧化碳排放112,000吨。然而,预计住宅和商业市场将占据相当大的份额。

- 约有 6,000 万欧盟公民使用区域供热,另有 1.4 亿欧盟公民居住在至少拥有一个区域供热系统的城市。根据欧盟和国际能源总署的报告,区域供热透过 6,000 个区域供热和製冷网路满足了欧盟约 11-12% 的热量需求。

- 其想法是利用机器学习从客户和营运资料中预测热负荷,并将其与天气预报、节日和工作日等资料相结合,以优化和规划热量生产,减少热量损失并满足尖峰负载。这种潜力扩展到故障检测中的智慧演算法,以识别由于漏水、加热系统效率低下或与单一组件相关的故障而导致的错误。

- 2024 年 6 月,瑞典 SMR计划开发商 Kahnfl Next 与芬兰 Steady Energy 建立策略合作伙伴关係,在瑞典引进 SMR 用于区域供热。此次合作旨在利用 Karnfur 独特的资金筹措结构和供应模式,将 Steady Energy 着名的区域供热核子反应炉引入瑞典市场。

区域供热市场趋势

住宅推动成长

- 区域供热在世界各国已开发国家普遍采用。区域供热相对于单一建筑系统有几个优点,包括提高安全性和可靠性、降低排放气体和提高燃料灵活性(特别是在使用生物质或废物等替代燃料时)。

- 区域供热广泛应用于单户住宅、多用户住宅、高层建筑和特大城镇。需要区域供热的主要住宅用途是空间供热和热水供热。区域供热市场在气候寒冷的国家已经很成熟,例如丹麦、冰岛、德国、美国、其他欧盟国家和加拿大。

- 然而,由再生能源来源动力来源动力的区域供热网路可以显着减少排放,并帮助政府实现排放目标。各国政府正在製定法律承诺和奖励,如补贴、津贴和能源税,以增加可再生能源在火力发电中的份额。

- 此外,区域供热以前主要来自发电厂、垃圾焚化发电设施和工业活动。但瑞典现在正在拥抱更多的可再生能源。竞争帮助这家社区电力公司成为全国领先的家庭供暖公司。

- 据 BDH 称,2023 年,德国售出了约 79 万套燃气暖气系统。其中约94,000台机组采用传统低温技术,超过6,96,500台机组选择了冷凝锅炉技术。

亚太地区占区域供热市场的大部分份额

- 推动中国市场成长的主要因素是可支配收入的增加、对二氧化碳排放的日益关注以及供暖和製冷系统的高利用率。此外,经合组织预测,到2060年,印度和中国的人均GDP将成长7倍。

- 亚太地区各国政府也正与当地企业合作开发住宅市场。例如,北京区域热力集团是中国一家大型供热公司。本公司为北京中央政府及军队、中国驻外使领馆、重要企事业单位、一般市民提供暖气解决方案。我们在其他省份也有许多计划。

- 现代区域供热系统对东南亚国家尤其重要,因为这些国家的空气污染造成了长期的经济成本并导致数十万人过早死亡。 《东南亚製冷的未来》研究了到 2040 年能源消耗、尖峰电力需求和二氧化碳排放的预期成长。

- 印度和澳洲是该地区最大的两个市场。区域供热和製冷解决方案的投资不断增加,以及政府为推广这些解决方案而开展的活动活性化,推动了这个区域市场的发展。

- 为了应对能源危机和气候变化,韩国政府制定了推广零能耗建筑的国家计划,并且最近还推出了多项针对新建和现有建筑的节能政策来实现这些计划。

区域供热产业概况

区域供热市场竞争较为温和,有许多全球性和地区性公司。这些公司正在努力扩大其全球消费者群体。该公司还优先考虑研发支出,用于开发创新解决方案、策略联盟以及其他有机和无机成长策略,以在预测期内获得竞争优势。

2023年5月,Vattenfall AB和可口可乐在瑞典宣布合作,制定了雄心勃勃的气候变迁目标,到2040年实现整个价值链的净零排放。两家公司已经启动了先导计画,其中设立了三个充电站,以满足电动交通的电力需求。

2023 年 3 月,NRG Energy 将完成对 Vivint Smart Home 的收购,加速 NRG 以消费者为中心的成长策略,为消费者提供简单、互联的体验,以智慧方式为其家庭供电、保护和管理。 NRG 处于能源和家庭服务的交汇处,提供以卓越的客户体验为基础的独特的端到端智慧家庭生态系统。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- 产业价值链分析

- COVID-19 市场影响

- 政府针对区域供热转型的措施和计划

- 区域供热的主要趋势和创新

第五章 市场动态

- 市场驱动因素

- 对节能、经济的暖气系统的需求不断增加

- 都市化和工业化进程

- 市场限制

- 基础设施成本高

第六章 市场细分

- 按植物类型

- 锅炉

- 热电联产 (CHP)

- 按热源分类

- 煤炭

- 天然气

- 可再生能源

- 石油和石油产品

- 按应用

- 住宅

- 商业和工业

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

第七章 竞争格局

- 公司简介

- Vattenfall AB

- SP Group

- Danfoss Group

- Engie

- NRG Energy Inc.

- Statkraft AS

- Logstor AS

- Shinryo Corporation

- Vital Energi Ltd

- Gteborg Energi

- Alfa Laval AB

- Ramboll Group AS

- Keppel Corporation Limited

- FVB Energy

第八章投资分析

第九章:未来机会

The District Heating Market size is estimated at USD 53.46 billion in 2025, and is expected to reach USD 57.84 billion by 2030, at a CAGR of 1.59% during the forecast period (2025-2030).

District energy is a quick-growing industry globally, supported by the aggressive climate objectives set by the global economies. Based on initial assessments, these district heating and cooling companies have been recognized as operations that could produce more extraordinary growth and value potential with an alternative holding structure. By including electrically powered heat pumps in the district heating supply, higher renewable energy levels can be used for thermal purposes, generating integration and balance between energy systems. With a burgeoning global wind turbine capacity, big heat pumps will play a meaningful role in the sustained global green energy development and phasing out fossil fuels by 2050.

Key Highlights

- District heating provides a method of delivering thermal energy to buildings (homes and commercial space) in the form of hot water through a distribution network of highly insulated pipelines. The potential for increased use of industrial district heating is limited because conversions of industrial processes to district heating involve varying heat loads amongst types of industries and processes.

- However, the conversion to district heating serves an 11% reduction in the use of electricity and a 40% reduction in the use of fossil fuels, with a total energy end-use saving of 6% among industries.

- Converting the industrial processes has led to a potential reduction of global carbon dioxide emissions by 112,000 tons per year. However, the residential and commercial markets are expected to hold a significant share.

- Approximately 60 million EU citizens are served by district heating, and an additional 140 million people live in cities with at least one district heating system. According to reports by the EU and the IEA, DH meets around 11-12% of the EU's heat demand via 6,000 district heating and cooling networks.

- With machine learning, the idea is to predict heat loads from customer data and operational data, along with weather forecasts, national holidays, weekdays, etc., to optimize and plan heat production, thereby lowering heat loss and handling peak loads. The potential is extended to intelligent algorithms in fault detection to identify leakages, inefficient heating systems, or errors from failure related to single components.

- In June 2024, Swedish SMR project developer Karnfull Next has strategically partnered with Finnish counterpart Steady Energy to introduce SMRs for district heating in Sweden. The collaboration aims to capitalize on Karnfull's unique financing structures and delivery models to introduce Steady Energy's renowned district heating reactors to the Swedish market.

District Heating Market Trends

Residential to Witness the Growth

- District heating is commonly used in industrialized nations worldwide. It has several advantages over individual building equipment, including improved safety and dependability, lower emissions, and greater fuel flexibility, particularly when utilizing alternative fuels such as biomass or garbage.

- District heating is widely utilized in single-family houses, multi-family dwellings, high-rise buildings, and mega townships. The primary home uses that require district heating are space and water heating. District heating markets are well-established in several cold-climate nations, such as Denmark, Iceland, Germany, the United States, other EU countries, and Canada.

- However, the District heating networks powered by renewable energy sources may significantly reduce emissions and help governments meet their emission reduction objectives. Various governments have established statutory responsibilities and incentives, such as grants, subsidies, and energy taxes, to boost the percentage of renewables in heat generation.

- Moreover, District heating was previously primarily powered by byproducts of power plants, waste-to-energy facilities, and industrial activities. However, Sweden is now incorporating more renewable energy sources into the mix. Due to competition, this localized kind of electricity has risen to the national top home-heating industry.

- According to BDH, in 2023, Germany saw sales of approximately 790,500 gas heating systems. Among these, approximatly 94,000 employed traditional low-temperature technology, with the majority, over 696,500, opting for condensing boiler technology.

Asia-Pacific Holds a Significant Share in the District Heating Market

- The primary reasons driving the market's growth in China are rising disposable income, increased worries about CO2 emissions, and high usage of heating and cooling systems. Moreover, OECD states that projections for India and China's per capita GDP might climb sevenfold by 2060.

- Governments in the Asia-Pacific region are also collaborating with local businesses to develop the home market. For example, the Beijing District Heating Group is a major heating firm in China. The firm provided heating solutions to the central Beijing government and army, Chinese embassies, significant corporations and organizations, and the general people. It also has a large number of projects in other provinces.

- Modern district heating systems are especially important for Southeast Asian countries, where air pollution causes long-term economic expenses and hundreds of thousands of premature fatalities. The Future of Cooling in Southeast Asia investigates the anticipated growth in energy consumption, peak power demand, and CO2 emissions by 2040.

- India and Australia are two of the region's biggest marketplaces. The regional market is rising due to increased investment in district heating and cooling solutions and increased government activities to promote these solutions.

- To respond to energy crises and climate change, the South Korean government established a national plan to promote zero energy buildings, and several energy efficiency policies for new and existing buildings in recent years have been developed to achieve these plans.

District Heating Industry Overview

The district heating market is moderately competitive and has many global and regional players. These companies are working hard to broaden their consumer base globally. To gain a competitive advantage during the predicted term, they also prioritize R&D expenditure in developing innovative solutions, strategic collaborations, and other organic and inorganic growth tactics.

In May 2023, Vattenfall AB and Coca-Cola announced the collaboration in Sweden and have set ambitious climate targets for net zero emissions across their entire value chains by 2040. The companies have initiated a pilot project with three charging stations to meet the need for powering electric transport.

In March 2023, NRG Energy Inc completed its acquisition of Vivint Smart Home, Inc. by accelerating NRG's consumer-focused growth strategy and offering consumers simple, connected experiences to power, protect, and manage their homes intelligently. NRG is at the intersection of energy and home services, with a unique end-to-end smart home ecosystem underpinned by our exceptional customer experience.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 on the Market

- 4.5 Government Initiatives and Programs on District Heating Transition

- 4.6 Key Trends and Innovations in District Heating

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Augmented Demand for Energy-efficient and Cost-effective Heating Systems

- 5.1.2 Rising Urbanization and Industrialization

- 5.2 Market Restraints

- 5.2.1 High Infrastructure Cost

6 MARKET SEGMENTATION

- 6.1 By Plant Type

- 6.1.1 Boiler

- 6.1.2 Combined Heat and Power (CHP)

- 6.2 By Heat Source

- 6.2.1 Coal

- 6.2.2 Natural Gas

- 6.2.3 Renewables

- 6.2.4 Oil and Petroleum Products

- 6.3 By Application

- 6.3.1 Residential

- 6.3.2 Commercial and Industrial

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Vattenfall AB

- 7.1.2 SP Group

- 7.1.3 Danfoss Group

- 7.1.4 Engie

- 7.1.5 NRG Energy Inc.

- 7.1.6 Statkraft AS

- 7.1.7 Logstor AS

- 7.1.8 Shinryo Corporation

- 7.1.9 Vital Energi Ltd

- 7.1.10 Gteborg Energi

- 7.1.11 Alfa Laval AB

- 7.1.12 Ramboll Group AS

- 7.1.13 Keppel Corporation Limited

- 7.1.14 FVB Energy

8 INVESTMENT ANALYSIS

9 FUTURE OPPORTUNITIES

英国区域供热:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

英国区域供热:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 全球区域供热市场规模、份额、趋势和成长分析报告(2026-2034年)住宅区域供热市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测商业区域供热市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测

全球区域供热市场规模、份额、趋势和成长分析报告(2026-2034年)住宅区域供热市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测商业区域供热市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测 2026年全球区域供热市场报告

2026年全球区域供热市场报告 区域供热市场规模、份额和趋势分析报告:按热源、类型、应用、工厂类型、地区和细分市场预测(2026-2033 年)

区域供热市场规模、份额和趋势分析报告:按热源、类型、应用、工厂类型、地区和细分市场预测(2026-2033 年) 区域供热市场机会、成长动力、产业趋势分析及2025-2034年预测

区域供热市场机会、成长动力、产业趋势分析及2025-2034年预测 全球热力网路市场

全球热力网路市场 区域供热的全球市场:厂房类型·热源·用途·各地区 (~2032年)

区域供热的全球市场:厂房类型·热源·用途·各地区 (~2032年) 按工厂类型、热源、应用和地区分類的区域供热市场

按工厂类型、热源、应用和地区分類的区域供热市场