|

市场调查报告书

商品编码

1685083

可食用包装市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测Edible Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

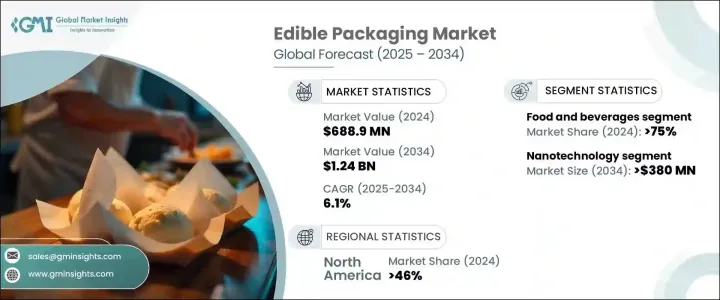

2024 年全球可食用包装市场规模达到 6.889 亿美元,预计 2025 年至 2034 年期间将以 6.1% 的强劲复合年增长率成长。随着全球对塑胶污染的担忧加剧,这一显着增长很大程度上受到对永续和环保包装解决方案的需求不断增长的推动。随着环境问题继续成为讨论的焦点,企业和消费者越来越多地寻求传统包装方法的替代品。可食用包装提供了一种符合全球永续发展目标的无浪费、可生物降解的选择,提供了一个有前景的解决方案。此外,人们日益意识到消费主义,以及对减少环境足迹的包装解决方案的需求,也推动了市场的扩张。对永续生产流程的关注度不断提高以及创新材料的兴起进一步支持了这个市场的加速发展,使可食用包装成为未来包装技术的关键参与者。

市场按终端使用行业进行细分,其中食品和饮料行业在 2024 年将占据 75% 的主导份额。这种主导地位归因于消费者对环保产品的偏好日益增长。随着消费者对更多永续选择的需求,食品和饮料产业正迅速采用可食用包装,认为这不仅可以减少浪费,还能吸引有环保意识的消费者。这些包装解决方案的开发融合了功能性和环保性,在不影响产品品质的情况下提供了便利的替代方案。同时,製药业也在挖掘可食用包装的潜力,儘管其份额较小,仅满足于小众应用。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 6.889 亿美元 |

| 预测值 | 12.4 亿美元 |

| 复合年增长率 | 6.1% |

就包装製程而言,市场分为抗菌、奈米技术、电流体动力、涂层和微生物。其中,奈米技术领域有望实现令人印象深刻的成长,预计复合年增长率为 6.5%。到2034年,可食用包装奈米技术预计将创造3.8亿美元的市场价值。该技术在分子层面上增强了材料特性,创造出更薄、更耐用的薄膜,可以更好地保持食品的完整性,同时提供卓越的包装解决方案。材料强度和保质期的提高是推动奈米技术在食用包装领域应用的关键优势。

北美引领全球可食用包装市场,到 2024 年将占据 46% 的份额。美国处于这一趋势的前沿,各行业越来越重视永续性。随着环保实践的动力不断增强,消费者对环保、创新包装选择的需求(尤其是食品和饮料包装)持续上升。此外,个人化包装和互动功能的结合有望塑造可食用包装的未来,增强其对那些在包装选择上不仅仅追求功能性的消费者的吸引力。

目录

第 1 章:方法论与范围

- 市场范围和定义

- 基础估算与计算

- 预测计算

- 资料来源

- 基本的

- 次要

- 付费来源

- 公共资源

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 影响价值链的因素

- 中断

- 未来展望

- 製造商

- 经销商

- 利润率分析

- 重要新闻及倡议

- 监管格局

- 衝击力

- 成长动力

- 扩大植物性和有机包装材料

- 食品和饮料业采用可食用包装

- 电子商务和包装食品配送的成长

- 功能性和营养性包装越来越受欢迎

- 转向零废弃包装解决方案

- 产业陷阱与挑战

- 提高耐久性和防水性的技术挑战

- 食用材料中过敏原污染的风险

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第 5 章:市场估计与预测:按材料,2021 年至 2034 年

- 主要趋势

- 海藻

- 多醣

- 脂质

- 其他的

第 6 章:市场估计与预测:按产品类型,2021-2034 年

- 主要趋势

- 电影

- 涂料

- 汤匙和叉子

- 其他的

第 7 章:市场估计与预测:依封装工艺,2021-2034 年

- 主要趋势

- 抗菌

- 奈米科技

- 电流体动力

- 涂料

- 微生物

第 8 章:市场估计与预测:按最终用途产业,2021 年至 2034 年

- 主要趋势

- 食品和饮料

- 药品

第 9 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中东及非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- Amtrex

- Contibelt

- Devro

- Ecolotec

- Edible Cutlery

- EdiblePro

- Evoware

- FlexSea

- Glanbia

- Incredible Eats

- Mantrose

- Sorbos

- Sunpack

- Tsukioka

- UseEco

- Xampla

The Global Edible Packaging Market reached USD 688.9 million in 2024 and is projected to grow at a robust CAGR of 6.1% from 2025 to 2034. This remarkable growth is largely driven by the escalating demand for sustainable and eco-friendly packaging solutions, as concerns over plastic pollution intensify globally. As environmental issues continue to dominate discussions, businesses and consumers are increasingly seeking alternatives to traditional packaging methods. Edible packaging presents a promising solution by offering a waste-free, biodegradable option that aligns with global sustainability goals. Additionally, the growing shift toward conscious consumerism and the desire for packaging solutions that reduce environmental footprints are fueling the market's expansion. The increased focus on sustainable production processes and the rise of innovative materials further support the acceleration of this market, positioning edible packaging as a key player in the future of packaging technology.

The market is segmented by end-use industries, with the food and beverages sector holding a dominant 75% share in 2024. This dominance is attributed to the growing consumer preference for eco-conscious products. As consumers demand more sustainable options, the food and beverage industry is quickly adopting edible packaging, seeing it as a way to not only reduce waste but also appeal to the environmentally aware consumer. These packaging solutions are being developed to combine functionality and eco-friendliness, offering a convenient alternative without compromising product quality. Meanwhile, the pharmaceutical industry is also tapping into the potential of edible packaging, though it holds a smaller share, catering to niche applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $688.9 Million |

| Forecast Value | $1.24 Billion |

| CAGR | 6.1% |

In terms of packaging processes, the market is categorized into antimicrobial, nanotechnology, electrohydrodynamic, coatings, and microorganisms. Among these, the nanotechnology segment is poised for impressive growth, projected to expand at a CAGR of 6.5%. By 2034, nanotechnology in edible packaging is expected to generate USD 380 million in market value. This technology enhances material properties at the molecular level, creating thinner, more durable films that better preserve food integrity while delivering superior packaging solutions. The improvements in material strength and shelf-life are key benefits driving the adoption of nanotechnology in the edible packaging sector.

North America is leading the global edible packaging market, holding a 46% share in 2024. The U.S. is at the forefront of this trend, with a growing emphasis on sustainability across various industries. Consumer demand for eco-friendly, innovative packaging options, particularly within food and beverages, continues to rise as the push for environmentally responsible practices gains momentum. Furthermore, the incorporation of personalized packaging and interactive features is expected to shape the future of edible packaging, enhancing its appeal to consumers who seek more than just functionality in their packaging choices.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Disruptions

- 3.1.3 Future outlook

- 3.1.4 Manufacturers

- 3.1.5 Distributors

- 3.2 Profit margin analysis

- 3.3 Key news & initiatives

- 3.4 Regulatory landscape

- 3.5 Impact forces

- 3.5.1 Growth drivers

- 3.5.1.1 Expansion of plant-based and organic packaging materials

- 3.5.1.2 Adoption of edible packaging in the food and beverage sector

- 3.5.1.3 Growth in e-commerce and packaged food deliveries

- 3.5.1.4 Increasing popularity of functional and nutritional packaging

- 3.5.1.5 Shift towards zero-waste packaging solutions

- 3.5.2 Industry pitfalls & challenges

- 3.5.2.1 Technical challenges in improving durability and water resistance

- 3.5.2.2 Risk of allergen contamination in edible materials

- 3.5.1 Growth drivers

- 3.6 Growth potential analysis

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Material, 2021-2034 (USD Million & Kilo Tons)

- 5.1 Key trends

- 5.2 Seaweeds & algae

- 5.3 Polysaccharides

- 5.4 Lipids

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 Films

- 6.3 Coatings

- 6.4 Spoon & fork

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Packaging Process, 2021-2034 (USD Million & Kilo Tons)

- 7.1 Key trends

- 7.2 Antimicrobial

- 7.3 Nanotechnology

- 7.4 Electro hydrodynamic

- 7.5 Coatings

- 7.6 Microorganisms

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Million & Kilo Tons)

- 8.1 Key trends

- 8.2 Food and beverages

- 8.3 Pharmaceuticals

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million & Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Amtrex

- 10.2 Contibelt

- 10.3 Devro

- 10.4 Ecolotec

- 10.5 Edible Cutlery

- 10.6 EdiblePro

- 10.7 Evoware

- 10.8 FlexSea

- 10.9 Glanbia

- 10.10 Incredible Eats

- 10.11 Mantrose

- 10.12 Sorbos

- 10.13 Sunpack

- 10.14 Tsukioka

- 10.15 UseEco

- 10.16 Xampla

2026年全球食用薄膜和涂层市场报告

2026年全球食用薄膜和涂层市场报告 全球可食用包装薄膜市场预测至2032年:依材料类型、产品形式、经营模式、技术、应用及地区划分

全球可食用包装薄膜市场预测至2032年:依材料类型、产品形式、经营模式、技术、应用及地区划分 可食用包装市场规模、份额和成长分析(按原料来源、配料、包装製程、最终用户和地区划分)-2026-2033年产业预测可食用和可生物降解包装市场预测至2032年:按形式、材料、分销管道、应用和地区分類的全球分析

可食用包装市场规模、份额和成长分析(按原料来源、配料、包装製程、最终用户和地区划分)-2026-2033年产业预测可食用和可生物降解包装市场预测至2032年:按形式、材料、分销管道、应用和地区分類的全球分析 食用涂层市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测(2025-2033 年)

食用涂层市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测(2025-2033 年) 可食用包装材料市场机会、成长驱动因素、产业趋势分析及预测

可食用包装材料市场机会、成长驱动因素、产业趋势分析及预测 可食用包装市场(按材料类型、包装形式、应用、最终用户、来源和技术)—2025-2032 年全球预测食用薄膜和涂层市场按成分类型、应用和最终用户划分 - 全球预测 2025-2032全球可食用包装市场:预测(至 2032 年)-按形状、材料、分销管道、应用和地区进行分析

可食用包装市场(按材料类型、包装形式、应用、最终用户、来源和技术)—2025-2032 年全球预测食用薄膜和涂层市场按成分类型、应用和最终用户划分 - 全球预测 2025-2032全球可食用包装市场:预测(至 2032 年)-按形状、材料、分销管道、应用和地区进行分析 2025 年至 2033 年可食用包装市场规模、份额、趋势及预测(按材料类型、来源、最终用户和地区)

2025 年至 2033 年可食用包装市场规模、份额、趋势及预测(按材料类型、来源、最终用户和地区)