|

市场调查报告书

商品编码

1766174

培养肉生物反应器市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Cultured Meat Bioreactors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

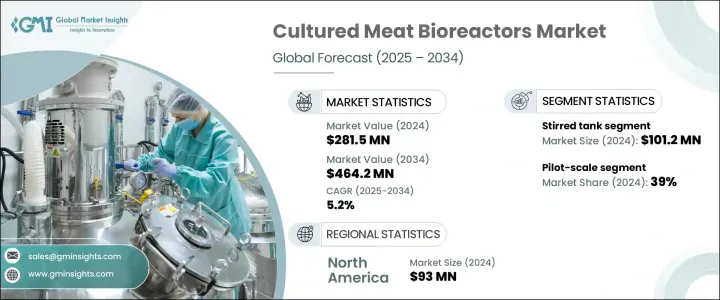

2024年,全球培养肉生物反应器市值为2.815亿美元,预计2034年将以5.2%的复合年增长率成长,达到4.642亿美元。该市场透过先进的生物反应器系统,实现了实验室培养肉类的大规模生产,在培养肉类领域中发挥着至关重要的作用。这些生物反应器为动物细胞培养创造了精心控制的环境,因此无需屠宰动物即可生产肉类。各种生物反应器类型,包括搅拌槽式、灌注式、气升式和中空纤维系统,在可扩展性、营养输送和剪切力管理方面各有优势。生物反应器设计、细胞培养基和规模化方法的创新提高了培养肉品生产的成本效益。

随着技术的进步,生产成本预计将下降,使培养肉更加经济实惠且易于取得。质地、风味和品质的提升也是提升消费者接受度并推动市场成长的关键因素。永续性仍然是主要驱动力,培养肉提供了一种环保且更符合道德的传统肉类生产替代方案。消费者对肉类替代品的兴趣日益浓厚,进一步刺激了对这项技术的需求,儘管高昂的初始资本和营运成本仍然是重大障碍,尤其是对于新创公司而言。建立生产需要能够支援工业规模细胞生长的专用生物反应器。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 2.815亿美元 |

| 预测值 | 4.642亿美元 |

| 复合年增长率 | 5.2% |

搅拌槽式生物反应器细分市场在2024年引领市场,产值达1.012亿美元。搅拌槽式生物反应器因其可靠性和可扩展性而备受青睐,是商业规模细胞培养的理想选择。凭藉在生物製药和发酵应用领域的卓越业绩,它们为培养肉生产商带来了较低的技术风险。这些系统可以从1-10公升的小型实验室规模扩展到超过10,000公升的工业规模,为研发和大规模生产提供了至关重要的灵活性。对于致力于以具有竞争力的价格实现培养肉商业化的公司而言,这种可扩展性至关重要。

2024年,中试规模市场占39%的份额。由于培养肉产业正从研究阶段向商业化生产转型,中试规模生物反应器发挥至关重要的桥樑作用。许多处于商业化前阶段的公司使用中试规模系统来改进细胞系、优化组织工程工艺,并模拟大规模生产,而无需承担大规模设施的高成本。这些生物反应器所需的资本投入较低,因此新创公司和正在申请监管审批或开发商业模式的公司都可以使用。

2024年,北美培养肉生物反应器市场规模达9,300万美元。美国透过明确的法规,为从事培养肉的投资者和企业创造了有利的环境。继2023年政府批准培养鸡肉上市后,美国已成为全球培养肉商业化销售的领导者,推动了对生物反应器技术和基础设施的投资。该地区拥有一些最先进的生物技术和食品科技公司,这些公司专注于生物反应器的开发和製程创新,并得到了领先研究机构的支持。此外,北美消费者,尤其是千禧世代和Z世代,对符合道德规范生产的环保食品表现出强烈的偏好,这推动了对培养肉的需求,并鼓励企业扩大生产规模并创新生物反应器系统。

全球培养肉生物反应器产业的领导公司包括默克集团 (Merck KGaA)、ABEC、阿法拉伐 (Alfa Laval)、生物工程股份公司 (Bioengineering AG)、Esco Lifesciences Group、赛多利斯股份公司 (Sartorius AG)、基伊埃 (GEA)、Infors HT、艾本德股份公司 (Sartorius AG)、基伊埃 (GEA)、Infors HT、艾本德股份公司 (EppenOVA, Biotechnc年, Biotechnd GmBH、OLLITAL Technology、颇尔集团 (Pall Corporation)、Solaris Biotech 和 Vogtlin Instruments GmbH。市场领导者采用的关键策略重点在于创新与协作,以提升其市场地位。

企业在研发方面投入巨资,旨在改进生物反应器设计、优化细胞培养基,并提高可扩展性,从而实现经济高效的生产。与培养肉品生产商建立策略伙伴关係,有助于实现技术整合和製程改进。企业也优先考虑扩大产能并进入新兴市场,以利用不断增长的需求。在行销活动中强调永续性和符合道德标准的食品生产有助于吸引具有环保意识的消费者。此外,企业注重法规合规性和智慧财产权保护,以保障创新成果。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商概况

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 对可持续蛋白质的需求不断增长

- 生物反应器设计的技术进步

- 不断增加对培养肉新创企业的投资

- 产业陷阱与挑战

- 资本和营运成本高

- 扩大生产的复杂性

- 机会

- 供应链优化

- 成长动力

- 成长潜力分析

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按类型

- 监管格局

- 标准和合规性要求

- 区域监理框架

- 认证标准

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按类型,2021 年至 2034 年

- 主要趋势

- 中空纤维

- 气升式反应器

- 搅拌槽

- 其他的

第六章:市场估计与预测:依规模,2021 年至 2034 年

- 主要趋势

- 实验室规模

- 中试规模

- 商业规模

第七章:市场估计与预测:依营运模式,2021 年至 2034 年

- 主要趋势

- 批次

- 补料分批

- 连续的

第 8 章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 牛肉

- 家禽

- 猪肉

- 其他的

第九章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 培养肉製造商

- 合约製造组织

- 研发机构/研究所

第十章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第 11 章:公司简介

- ABEC

- Alfa Laval

- Bioengineering AG

- Eppendorf AG

- Esco Lifesciences Group

- GEA

- Infors HT

- INNOVA Bio-meditech

- KBiotech GmBH

- Merck KGaA

- OLLITAL Technology

- Pall Corporation

- Sartorius AG

- Solaris Biotech

- Vogtlin Instruments GmbH

The Global Cultured Meat Bioreactors Market was valued at USD 281.5 million in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 464.2 million by 2034. This market plays a critical role in the cultivated meat sector by enabling large-scale production of lab-grown meat through sophisticated bioreactor systems. These bioreactors create carefully controlled environments for animal cell cultures, allowing meat production without the need for animal slaughter. Various bioreactor types, including stirred-tank, perfusion, airlift, and hollow-fiber systems, each provide distinct advantages in terms of scalability, nutrient delivery, and management of shear forces. Innovations in bioreactor design, cell culture media, and scaling methods have enhanced the cost-efficiency of cultured meat production.

As technology advances, production costs are expected to decline, making cultivated meat more affordable and accessible. Improved texture, flavor, and quality are also key factors that will boost consumer acceptance and drive market growth. Sustainability remains a major motivator, with cultured meat offering an eco-friendly and more ethical alternative to traditional meat production. Rising consumer interest in meat alternatives further fuels demand for this technology, though high initial capital and operating costs remain significant barriers, especially for startups. Establishing production requires specialized bioreactors capable of supporting cell growth at industrial scales.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $281.5 Million |

| Forecast Value | $464.2 Million |

| CAGR | 5.2% |

The stirred-tank bioreactor segment led the market in 2024, generating USD 101.2 million. Stirred-tank bioreactors are highly favored for their reliability and scalability, making them ideal for commercial-scale cell cultivation. With a strong track record in biopharmaceutical and fermentation applications, they present low technical risks to cultivated meat producers. These systems can scale from small laboratory sizes of 1-10 liters to industrial capacities exceeding 10,000 liters, offering vital flexibility for research, development, and full-scale manufacturing. This scalability is essential for companies aiming to commercialize cultured meat at competitive prices.

The pilot-scale segment held a 39% share in 2024. Since the cultured meat industry is transitioning from research to commercial production, pilot-scale bioreactors serve as a critical bridge. Many companies at the pre-commercial stage use pilot-scale systems to refine cell lines, optimize tissue engineering processes, and simulate large-scale production without the high costs associated with full-scale facilities. These bioreactors require lower capital investment, making them accessible to startups and firms working on regulatory approvals or business model development.

North America Cultured Meat Bioreactors Market accounted for USD 93 million in 2024. The United States has fostered a supportive environment for investors and companies involved in cultivated meat through clear regulations. Following government approval for marketing cultured chicken in 2023, the U.S. has become a global leader in commercial cultured meat sales, boosting investments in bioreactor technology and infrastructure. The region hosts some of the most advanced biotech and food tech companies specializing in bioreactor development and process innovation, supported by leading research institutions. Moreover, North American consumers, particularly millennials and Gen Z, show strong preferences for ethically produced, environmentally friendly food products, driving demand for cultured meat and encouraging companies to scale production and innovate bioreactor systems.

Leading companies operating in the Global Cultured Meat Bioreactors Industry include Merck KGaA, ABEC, Alfa Laval, Bioengineering AG, Esco Lifesciences Group, Sartorius AG, GEA, Infors HT, Eppendorf AG, INNOVA Bio-meditech, KBiotech GmBH, OLLITAL Technology, Pall Corporation, Solaris Biotech, and Vogtlin Instruments GmbH. Key strategies adopted by market leaders focus heavily on innovation and collaboration to boost their market positioning.

Companies invest extensively in research and development to improve bioreactor designs, optimize cell culture media, and enhance scalability for cost-effective production. Forming strategic partnerships with cultivated meat producers enables technology integration and process refinement. Firms also prioritize expanding production capacities and entering emerging markets to capitalize on rising demand. Emphasizing sustainability and ethical food production in marketing campaigns helps attract eco-conscious consumers. Additionally, players focus on regulatory compliance and securing intellectual property to safeguard innovations.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Scale

- 2.2.4 Mode of Operation

- 2.2.5 Application

- 2.2.6 End Use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for sustainable protein

- 3.2.1.2 Technological advancements in bioreactor design

- 3.2.1.3 Growing investments in cultured meat startups

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High capital and operating costs

- 3.2.2.2 Complexity in scaling up production

- 3.2.3 Opportunities

- 3.2.4 Supply chain optimization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 (USD Million) (Units)

- 5.1 Key trends

- 5.2 Hollow fiber

- 5.3 Airlift reactor

- 5.4 Stirred tank

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Scale, 2021 – 2034 (USD Million) (Units)

- 6.1 Key trends

- 6.2 Lab-scale

- 6.3 Pilot-scale

- 6.4 Commercial-scale

Chapter 7 Market Estimates and Forecast, By Mode of Operation, 2021 – 2034 (USD Million) (Units)

- 7.1 Key trends

- 7.2 Batch

- 7.3 Fed-batch

- 7.4 Continuous

Chapter 8 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Million) (Units)

- 8.1 Key trends

- 8.2 Beef

- 8.3 Poultry

- 8.4 Pork

- 8.5 Others

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2034 (USD Million) (Units)

- 9.1 Key trends

- 9.2 Cultured meat manufacturers

- 9.3 Contract manufacturing organizations

- 9.4 R&D organizations/Institutes

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million) (Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 ABEC

- 11.2 Alfa Laval

- 11.3 Bioengineering AG

- 11.4 Eppendorf AG

- 11.5 Esco Lifesciences Group

- 11.6 GEA

- 11.7 Infors HT

- 11.8 INNOVA Bio-meditech

- 11.9 KBiotech GmBH

- 11.10 Merck KGaA

- 11.11 OLLITAL Technology

- 11.12 Pall Corporation

- 11.13 Sartorius AG

- 11.14 Solaris Biotech

- 11.15 Vogtlin Instruments GmbH

全球培养肉市场规模、份额、趋势和成长分析报告(2026-2034年)

全球培养肉市场规模、份额、趋势和成长分析报告(2026-2034年) 2032年替代蛋白和培养肉市场预测:按产品、成分、分销管道、技术、应用、最终用户和地区分類的全球分析精准发酵和细胞培养食品市场预测至2032年:按产品类型、形态、生产方法、技术、应用、最终用户和地区分類的全球分析

2032年替代蛋白和培养肉市场预测:按产品、成分、分销管道、技术、应用、最终用户和地区分類的全球分析精准发酵和细胞培养食品市场预测至2032年:按产品类型、形态、生产方法、技术、应用、最终用户和地区分類的全球分析 培养肉市场:市场机会、成长驱动因素、产业趋势分析及预测(2026-2035)人造肉配料市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)全球人造肉类和人造禽市场预测至2032年:按产地、包装类型、技术、应用、最终用户和地区分類的分析全球培养肉成分市场预测(至2032年):按肉类型、细胞来源、培养基、支架和组织化技术、技术、应用和地区进行分析全球培养肉市场-2025-2030年预测2032 年培养肉和细胞食品市场预测:按产品类型、分销管道、最终用户和地区进行的全球分析2032 年培养肉市场预测:按来源、生产、通路、应用、最终用户和地区分類的全球分析

培养肉市场:市场机会、成长驱动因素、产业趋势分析及预测(2026-2035)人造肉配料市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)全球人造肉类和人造禽市场预测至2032年:按产地、包装类型、技术、应用、最终用户和地区分類的分析全球培养肉成分市场预测(至2032年):按肉类型、细胞来源、培养基、支架和组织化技术、技术、应用和地区进行分析全球培养肉市场-2025-2030年预测2032 年培养肉和细胞食品市场预测:按产品类型、分销管道、最终用户和地区进行的全球分析2032 年培养肉市场预测:按来源、生产、通路、应用、最终用户和地区分類的全球分析