|

市场调查报告书

商品编码

1797760

沥青涂料市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Bituminous Coatings Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

2024年,全球沥青涂料市场规模达30亿美元,预计到2034年将以4.5%的复合年增长率成长,达到46亿美元。随着时间的推移,该行业已从传统的热施沥青系统过渡到更先进、更永续的涂料解决方案。历史上,高温涂料因其在大型基础设施应用中能够承受恶劣环境而备受青睐,但此后市场已转向更高效、更环保的替代品。创新发挥了核心作用,製造商推出了乳液和热塑性塑胶等增强配方,使其更易于施工,排放更低。

这种转变很大程度上源于对适应现代建筑需求的长效多功能涂料日益增长的需求。随着永续性成为基础设施发展的关键因素,市场正受益于持续的研发投入,以开发智慧、高效能的沥青产品。聚合物改质沥青 (PMB) 和冷涂乳液在城市和住宅项目中的应用日益增多,这直接反映了不断变化的建筑标准、安全隐患和气候适应性。虽然热涂涂料仍然是重防腐应用的首选,但新技术正在重塑全球多个地区的市场格局。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 30亿美元 |

| 预测值 | 46亿美元 |

| 复合年增长率 | 4.5% |

热涂沥青涂料市场在2024年创造了8.258亿美元的收入。这类涂料以其强大的附着力、耐潮性和超长的使用寿命而闻名,广泛应用于隧道、地基和桥面等基础设施项目,尤其是在易受机械磨损或极端天气影响的环境中。其耐用性和成本效益使其成为土木工程领域可靠的解决方案,尤其是在北美和亚洲部分地区。

2024年,屋顶涂料市场占有34.5%的份额。沥青涂料因其防水、隔热和抗紫外线损伤等特性而在该领域备受青睐。这些特性使其成为新建和翻新工程的理想选择,尤其适用于平屋顶和低坡屋顶。其易于施工和价格实惠的特点进一步巩固了其在住宅和商业建筑中的主导地位。

2024年,中国沥青涂料市场规模达4.73亿美元,占全球市场份额的40%。亚太地区是成长最快的市场,得益于交通、电信、卫生和电力基础设施领域的大规模投资。受城市发展和政府支持大型计画的推动,这项快速扩张持续推高了沥青涂料的需求。越南、印尼和印度等国家基础建设也呈现强劲势头,进一步推动了区域成长。

全球沥青涂料市场的竞争格局涵盖多家主要参与者,尤其是道达尔能源公司 (TotalEnergies SE)、埃克森美孚公司 (ExxonMobil Corporation)、巴斯夫公司 (BASF SE)、西卡公司 (Sika AG) 和尼纳斯公司 (Nynas AB)。沥青涂料市场的公司正在采取各种策略来巩固其市场地位。产品创新是主要关注点,研发投资旨在开发环保配方,降低排放并保持耐用性。许多公司正在转向冷施工和聚合物改质解决方案,以满足不断变化的环境和安全标准。与建筑公司建立策略伙伴关係有助于提高产品的应用和分销效率。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商概况

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 加大基础建设投资和都市化

- 气候变迁调适与极端天气防护需求

- 能源效率和建筑性能要求

- 维护和生命週期成本优化需求

- 产业陷阱与挑战

- 原物料价格波动与成本压力

- 环境法规和永续性要求

- 应用复杂性和熟练劳动力要求

- 来自替代防水技术的竞争

- 市场机会

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 价格趋势

- 按地区

- 按产品

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 专利态势

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依产品类型,2021 - 2034 年

- 主要趋势

- 热施工沥青涂料

- 冷涂沥青涂料

- 聚合物改质沥青(PMB)涂料

- 沥青乳液

- 自黏沥青体系

- 生物基和可持续沥青涂料

第六章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 屋顶

- 防水

- 道路和基础设施

- 工业和防护涂料

- 专业应用

- 停车场涂料和交通承载

- 绿色屋顶系统与永续发展

- 运动设施及休閒场所

第七章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 住宅建筑

- 单户住宅

- 多户住宅和公寓大楼

- 住宅翻新改造

- 商业建筑

- 办公大楼和商业房地产

- 零售和购物中心

- 饭店及娱乐设施

- 商业装修及维护

- 工业建筑

- 製造设施和工业厂房

- 仓储和配送中心

- 能源和公用事业基础设施

- 工业维护

- 基础设施和公共工程

- 交通基础设施和高速公路

- 水和废水处理设施

- 政府大楼及公共设施

- 特殊最终用途

- 医疗机构和医院

- 教育机构及学校建筑

- 体育和娱乐设施

- 紧急情况和灾难復原

第八章:市场估计与预测:按技术,2021 - 2034 年

- 主要趋势

- 传统沥青技术

- 传统沥青基配方

- 标准应用方法与设备

- 先进的聚合物改质技术

- SBS(苯乙烯-丁二烯-苯乙烯)改质体系

- App(无规聚丙烯)改质技术

- 混合聚合物系统和先进配方

- 永续和生物基技术

- 生物沥青和植物性替代品

- 再生材料整合与循环经济解决方案

- 低挥发性有机化合物 (VOC) 和环保配方

- 智慧先进技术

- 自修復和自适应涂层技术

- 奈米科技增强配方

- 物联网整合监控维护系统

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第十章:公司简介

- BASF SE

- Carlisle Coatings & Waterproofing

- ExxonMobil Corporation

- GAF Materials Corporation

- Graco Inc.

- Johns Manville (Berkshire Hathaway)

- Nynas AB

- Owens Corning Corporation

- Polyglass USA, Inc

- Shell Global Solutions

- Sika AG

- SOPREMA Group

- Titan Tool Inc

- Total Energies SE

- Tremco Roofing and Building Maintenance

- Polyguard Products, Inc

- Sika AG

- Soprema Group

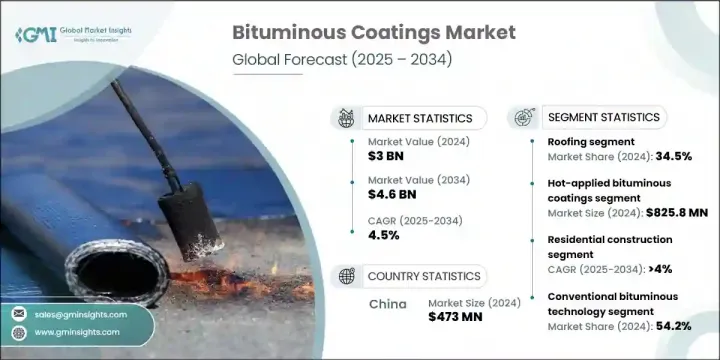

The Global Bituminous Coatings Market was valued at USD 3 billion in 2024 and is estimated to grow at a CAGR of 4.5% to reach USD 4.6 billion by 2034. Over time, the industry has transitioned from traditional hot-applied bitumen systems to more advanced and sustainable coating solutions. Historically, high-temperature coatings were favored for their ability to withstand harsh environments in large infrastructure applications, but the market has since moved toward more efficient, environmentally friendly alternatives. Innovation has played a central role, with manufacturers introducing enhanced formulations like emulsions and thermoplastics that offer easier application and lower emissions.

This shift is largely driven by the increasing demand for long-lasting, versatile coatings that adapt to modern construction needs. As sustainability becomes a key factor in infrastructure development, the market is benefitting from continued investment in R&D to develop intelligent, high-performance bituminous products. The growing use of polymer-modified bitumen (PMB) and cold-applied emulsions in urban and residential projects is a direct response to changing construction standards, safety concerns, and climate adaptability. While hot-applied coatings remain a top choice for heavy-duty applications, newer technologies are reshaping the market dynamics across multiple global regions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3 Billion |

| Forecast Value | $4.6 Billion |

| CAGR | 4.5% |

The hot-applied bituminous coatings segment generated USD 825.8 million in 2024. Known for their strong adhesion, moisture resistance, and extended service life, these coatings are widely used in infrastructure projects like tunnels, foundations, and bridge decks, particularly in environments subject to mechanical wear or extreme weather. Their durability and cost-effectiveness continue to make them a reliable solution in civil engineering, especially in North America and parts of Asia.

The roofing segment held 34.5% share in 2024. Bituminous coatings are favored in this segment for their waterproofing capabilities, thermal insulation, and resistance to UV damage. These attributes make them ideal for both new construction and renovation projects, especially for flat and low-pitched roofs. Their ease of application and affordability contribute further to their dominance in both residential and commercial buildings.

China Bituminous Coatings Market generated USD 473 million and accounting for 40% share in 2024. The Asia Pacific region is the fastest-growing market, supported by massive investments in transport, telecommunications, sanitation, and power infrastructure. This rapid expansion-driven by urban growth and large-scale state-backed projects-continues to boost demand for bituminous coatings. Countries such as Vietnam, Indonesia, and India are also seeing strong momentum in infrastructure development, further fueling regional growth.

The competitive landscape of the Global Bituminous Coatings Market includes several major players, notably TotalEnergies SE, ExxonMobil Corporation, BASF SE, Sika AG, and Nynas AB. Companies in the bituminous coatings market are adopting a variety of strategies to reinforce their market position. A primary focus is on product innovation, with R&D investments targeted at creating eco-friendly formulations that lower emissions while maintaining durability. Many firms are transitioning toward cold-applied and polymer-modified solutions to meet changing environmental and safety standards. Strategic partnerships and collaborations with construction firms help improve product application and distribution efficiency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Application

- 2.2.4 End Use

- 2.2.5 Technology

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing Infrastructure Investment and Urbanization

- 3.2.1.2 Climate Change Adaptation and Extreme Weather Protection Needs

- 3.2.1.3 Energy Efficiency and Building Performance Requirements

- 3.2.1.4 Maintenance and Lifecycle Cost Optimization Demands

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Raw Material Price Volatility and Cost Pressures

- 3.2.2.2 Environmental Regulations and Sustainability Requirements

- 3.2.2.3 Application Complexity and Skilled Labor Requirements

- 3.2.2.4 Competition from Alternative Waterproofing Technologies

- 3.2.3 Market opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation Landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Hot-applied bituminous coatings

- 5.3 Cold-applied bituminous coatings

- 5.4 Polymer-modified bitumen (PMB) coatings

- 5.5 Bituminous emulsions

- 5.6 Self-adhesive bituminous systems

- 5.7 Bio-based and sustainable bituminous coatings

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Roofing

- 6.3 Waterproofing

- 6.4 Road and infrastructure

- 6.5 Industrial and protective coatings

- 6.6 Specialty applications

- 6.6.1 Parking deck coatings and traffic-bearing

- 6.6.2 Green roof systems and sustainable

- 6.6.3 Sports facility and recreational surface

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Residential construction

- 7.2.1 Single-family housing

- 7.2.2 Multi-family housing and apartment complex

- 7.2.3 Residential renovation and retrofit

- 7.3 Commercial construction

- 7.3.1 Office buildings and commercial real estate

- 7.3.2 Retail and shopping center

- 7.3.3 Hospitality and entertainment facility

- 7.3.4 Commercial renovation and maintenance

- 7.4 Industrial construction

- 7.4.1 Manufacturing facilities and industrial plants

- 7.4.2 Warehouse and distribution center

- 7.4.3 Energy and utility infrastructure

- 7.5 Industrial maintenance

- 7.5.1 Infrastructure and public works

- 7.5.2 Transportation infrastructure and highway

- 7.5.3 Water and wastewater treatment facilities

- 7.5.4 Government buildings and public facilities

- 7.6 Specialty end use

- 7.6.1 Healthcare facilities and hospital

- 7.6.2 Educational institutions and school buildings

- 7.6.3 Sports and recreation facilities

- 7.6.4 Emergency and disaster recovery

Chapter 8 Market Estimates and Forecast, By Technology, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Conventional bituminous technology

- 8.2.1 Traditional asphalt-based formulations

- 8.2.2 Standard application methods and equipment

- 8.3 Advanced polymer-modified technology

- 8.3.1 SBS (styrene-butadiene-styrene) modification systems

- 8.3.2 App (atactic polypropylene) modification technologies

- 8.3.3 Hybrid polymer systems and advanced formulations

- 8.4 Sustainable and bio-based technology

- 8.4.1 Bio-bitumen and plant-based alternative

- 8.4.2 Recycled content integration and circular economy solutions

- 8.4.3 Low-voc and environmentally friendly formulations

- 8.5 Smart and advanced technology

- 8.5.1 Self-healing and adaptive coating technologies

- 8.5.2 Nanotechnology-enhanced formulations

- 8.5.3 IOT-integrated monitoring and maintenance systems

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 BASF SE

- 10.2 Carlisle Coatings & Waterproofing

- 10.3 ExxonMobil Corporation

- 10.4 GAF Materials Corporation

- 10.5 Graco Inc.

- 10.6 Johns Manville (Berkshire Hathaway)

- 10.7 Nynas AB

- 10.8 Owens Corning Corporation

- 10.9 Polyglass U.S.A., Inc

- 10.10 Shell Global Solutions

- 10.11 Sika AG

- 10.12 SOPREMA Group

- 10.13 Titan Tool Inc

- 10.14 Total Energies SE

- 10.15 Tremco Roofing and Building Maintenance

- 10.16 Polyguard Products, Inc

- 10.17 Sika AG

- 10.18 Soprema Group

沥青乳化剂市场分析及预测(至2035年):类型、产品、应用、技术、组成成分、最终用户、剂型、材料类型、製程、解决方案沥青市场分析及预测(至2035年):依类型、产品类型、应用、技术、最终用户、形态、材质、製程及功能划分环保沥青生产市场分析及预测(至2035年):类型、产品、服务、技术、应用、形式、材料类型、製程、最终用户、设备

沥青乳化剂市场分析及预测(至2035年):类型、产品、应用、技术、组成成分、最终用户、剂型、材料类型、製程、解决方案沥青市场分析及预测(至2035年):依类型、产品类型、应用、技术、最终用户、形态、材质、製程及功能划分环保沥青生产市场分析及预测(至2035年):类型、产品、服务、技术、应用、形式、材料类型、製程、最终用户、设备 沥青:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

沥青:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 2026年全球沥青市场报告

2026年全球沥青市场报告 沥青市场-全球产业规模、份额、趋势、机会、预测:按产品类型、应用、地区和竞争格局划分,2021-2031年

沥青市场-全球产业规模、份额、趋势、机会、预测:按产品类型、应用、地区和竞争格局划分,2021-2031年 沥青市场规模、份额和成长分析(按产品类型、形态、原材料、製造流程、等级、分销管道、应用和地区划分)-2026-2033年产业预测

沥青市场规模、份额和成长分析(按产品类型、形态、原材料、製造流程、等级、分销管道、应用和地区划分)-2026-2033年产业预测![中国沥青市场评估:依类型[铺路沥青、氧化沥青、聚合物改质沥青、其他]、应用[道路建设、防水、黏合剂、其他]、地区、机会及预测(2018-2032)](/sample/img/cover/42/default_cover_mx.png) 中国沥青市场评估:依类型[铺路沥青、氧化沥青、聚合物改质沥青、其他]、应用[道路建设、防水、黏合剂、其他]、地区、机会及预测(2018-2032)印度沥青市场评估:依类型[铺路沥青、氧化沥青、聚合物改质沥青、其他]、应用[道路建设、防水、黏合剂、其他]、地区、机会及预测(2019-2033 年)日本沥青市场评估:依类型[铺路沥青、氧化沥青、聚合物改质沥青、其他]、应用[道路建设、防水、黏合剂、其他]、地区、机会及预测(2019-2033年)

中国沥青市场评估:依类型[铺路沥青、氧化沥青、聚合物改质沥青、其他]、应用[道路建设、防水、黏合剂、其他]、地区、机会及预测(2018-2032)印度沥青市场评估:依类型[铺路沥青、氧化沥青、聚合物改质沥青、其他]、应用[道路建设、防水、黏合剂、其他]、地区、机会及预测(2019-2033 年)日本沥青市场评估:依类型[铺路沥青、氧化沥青、聚合物改质沥青、其他]、应用[道路建设、防水、黏合剂、其他]、地区、机会及预测(2019-2033年)