|

市场调查报告书

商品编码

1797784

高压 BCD 电源 IC 市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测High-Voltage BCD Power IC Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

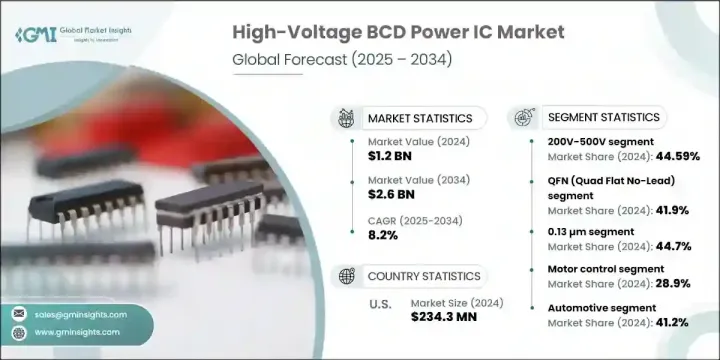

2024年,全球高压BCD电源IC市场规模达12亿美元,预计2034年将以8.2%的复合年增长率成长,达到26亿美元。这一增长主要得益于市场对紧凑型节能电源管理系统日益增长的需求。各行各业正转向基于BCD的电源IC,这种IC将高压DMOS、类比双极型和CMOS逻辑元件整合到单一晶片上。这种配置显着节省空间,减少元件数量,并提高能源效率。这些整合解决方案对于电动和混合动力汽车、电信基础设施和工业自动化尤其重要,因为它们能够提高电源控制精度、热性能和运行永续性,同时降低碳足迹。

功能丰富的智慧电源IC的发展正在改变关键产业的应用。先进的BCD装置现已具备可程式设定、故障监控、软开关和热保护等功能。这些功能降低了维护需求,简化了系统架构,并提高了可靠性,使其成为汽车ECU、医疗设备、机器人和物联网系统的理想选择。它们与SoC和数位控制系统的整合在终端市场持续成长。汽车和工业OEM厂商正在推动BCD的采用,以提高安全性、效率和即时系统反应。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 12亿美元 |

| 预测值 | 26亿美元 |

| 复合年增长率 | 8.2% |

2024年,200V-500V电压段以5.351亿美元的市场规模领先市场。这些IC广泛应用于电动车电源模组、工业控制器和电信设备。它们的吸引力在于能够在高性能、易整合性和成本效益之间取得平衡,使其适用于各种高压应用。由于该段与全球日益增长的电气化运动、工厂现代化和智慧基础设施部署息息相关,其发展前景广阔。

0.13 µm 製程节点市场在 2024 年的市场规模为 5.3589 亿美元。由于其稳健性、较低的生产成本以及在单晶片上整合类比、数位和高压 DMOS 技术的能力,该节点仍占据主导地位。由于其在极端工作条件下的可靠性以及对功率密度要求的满足,该节点已成为汽车系统、工业驱动和耐用消费性电子产品中关键任务应用的标准。

美国高压BCD功率IC市场在2024年创收2.343亿美元,预计2034年复合年增长率将达到7.9%。美国受益于强大的半导体生产基础、不断扩张的电动车基础设施以及工业领域的自动化程度提高。其他成长动力包括下一代电信服务的推出、国防系统的投资、清洁能源的推广。联邦政府计划下的公共资金以及支持国内晶片製造的激励措施,正在进一步增强美国市场的地位。

全球高压 BCD 电源 IC 市场的知名参与者包括 Vishay Intertechnology、Power Integrations、Renesas Electronics、Maxim Integrated、安森美半导体 (onsemi)、Dialog Semiconductor、意法半导体、罗姆半导体、Diodes Incorporated、仪器、Alalpha & Omquira) Technology、英飞凌科技、ADI、Presto Engineering、恩智浦半导体、GlobalFoundries、台积电、联华电子和 Magnachip Semiconductor。为了加强市场定位,领先的参与者正在大力投资下一代 BCD 架构的研发,以支援更高的电压范围、增强的热处理和数位整合。一些公司正在扩大其代工合作伙伴关係,以确保获得可扩展且具有成本效益的製造能力。汽车级认证被高度重视,以符合严格的安全和可靠性标准。本公司也专注于满足特定应用功率配置的模组化晶片设计。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商概况

- 利润率

- 成本结构

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 汽车和工业领域电气化程度不断提高

- 对节能和紧凑设计的需求不断增长

- 5G基础设施和资料中心的扩展

- 政府对电动车充电和电力基础设施的奖励措施

- 智慧型电源 IC 功能的进步(SoC 整合、诊断、保护)

- 产业陷阱与挑战

- 先进BCD製程开发的复杂性与成本

- 高压下的热管理和功耗问题

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 新兴商业模式

- 合规性要求

- 永续性措施

- 永续材料评估

- 碳足迹分析

- 循环经济实施

- 永续性认证和标准

- 永续性投资报酬率分析

- 全球消费者情绪分析

- 专利分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 市场集中度分析

- 按地区

- 关键参与者的竞争基准

- 财务绩效比较

- 收入

- 利润率

- 研发

- 产品组合比较

- 产品范围广度

- 科技

- 创新

- 地理位置比较

- 全球足迹分析

- 服务网路覆盖

- 各区域市场渗透率

- 竞争定位矩阵

- 领导者

- 挑战者

- 追踪者

- 利基市场参与者

- 战略展望矩阵

- 财务绩效比较

- 2021-2024 年关键发展

- 併购

- 伙伴关係和合作

- 技术进步

- 扩张和投资策略

- 永续发展倡议

- 数位转型倡议

- 新兴/新创企业竞争对手格局

第五章:市场估计与预测:按电压等级类型,2021 - 2034 年

- 主要趋势

- 60伏-100伏

- 100伏-200伏

- 200伏-500伏

- 500V以上

第六章:市场估计与预测:按工艺节点,2021 - 2034 年

- 主要趋势

- 0.35 微米

- 0.18 微米

- 0.13 微米

- 90奈米以下

第七章:市场估计与预测:依包装类型,2021 - 2034 年

- 主要趋势

- QFN(四方扁平无引线)

- WLCSP(晶圆级晶片尺寸封装)

- BGA(球栅阵列)

- 晶片/板上晶片(用于整合模组)

第八章:市场估计与预测:按最终用途产业,2021 - 2034 年

- 主要趋势

- 汽车(EV/HEV动力系统、ADAS、照明)

- 消费性电子产品(电源供应器、电池管理、快速充电器)

- 工业(马达驱动器、自动化设备、机器人)

- 电信(5G基础设施、功率放大器)

- 医疗器材(便携式诊断和治疗设备)

- 航太与国防(雷达系统、通讯设备)

- 资料中心和云端基础设施(伺服器电源、DC-DC转换器)

第九章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 电源管理

- 马达控制

- 电池管理系统(BMS)

- LED照明驱动器

- 电压调节与转换

- 信号调理与保护

- 音讯放大器

第十章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第 11 章:公司简介

- STMicroelectronics

- Texas Instruments

- Infineon Technologies

- Infineon Technologies

- NXP Semiconductors

- Renesas Electronics

- Rohm Semiconductor

- Analog Devices (ADI)

- Diodes Incorporated

- Microchip Technology

- TSMC

- GlobalFoundries

- UMC

- Vishay Intertechnology

- Dialog Semiconductor

- Maxim Integrated

- Power Integrations

- Alpha & Omega Semiconductor (AOS)

- Magnachip Semiconductor

- Presto Engineering

The Global High-Voltage BCD Power IC Market was valued at USD 1.2 billion in 2024 and is estimated to grow at a CAGR of 8.2% to reach USD 2.6 billion by 2034. This growth is largely fueled by the increasing demand for compact and energy-efficient power management systems. Industries are moving toward BCD-based power ICs that integrate high-voltage DMOS, analog Bipolar, and CMOS logic components onto a single chip. This configuration offers notable space savings, reduces the number of components, and improves energy efficiency. These integrated solutions are particularly essential for use in electric and hybrid vehicles, telecom infrastructure, and industrial automation, as they improve power control precision, thermal performance, and operational sustainability while lowering the carbon footprint.

The development of intelligent, feature-rich power ICs is transforming applications across key sectors. Advanced BCD devices now include features such as programmable settings, fault monitoring, soft-switching, and thermal safeguards. These capabilities make them ideal for automotive ECUs, medical devices, robotics, and IoT systems by lowering maintenance needs, simplifying system architecture, and improving reliability. Their integration with SoCs and digital control systems continues to gain momentum across end-use markets. Automotive and industrial OEMs are driving adoption to enhance safety, efficiency, and real-time system response.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.2 Billion |

| Forecast Value | $2.6 Billion |

| CAGR | 8.2% |

In 2024, the 200V-500V voltage segment led the market with USD 535.1 million. These ICs are widely used in EV power modules, industrial controllers, and telecom equipment. Their appeal lies in their ability to deliver a balance of high performance, integration ease, and cost-effectiveness, making them suitable across a wide array of high-voltage applications. This segment is gaining traction due to its relevance in the growing electrification movement, factory modernization, and smart infrastructure deployments worldwide.

The 0.13 µm process node segment accounted for USD 535.89 million in 2024. It remains dominant due to its robustness, lower production costs, and ability to support integration of analog, digital, and high-voltage DMOS technologies on a single chip. This node has become a standard for mission-critical applications in automotive systems, industrial drives, and durable consumer electronics due to its reliability under extreme operating conditions and compliance with power density demands.

U.S. High-Voltage BCD Power IC Market generated USD 234.3 million in 2024 and is expected to register a CAGR of 7.9% through 2034. The country benefits from a robust base in semiconductor production, expanding EV infrastructure, and increasing automation in industrial sectors. Additional growth drivers include the rollout of next-generation telecom services, investment in defense systems, and a push toward clean energy adoption. Public funding under federal initiatives and incentives supporting domestic chip manufacturing is further strengthening the U.S. market presence.

Notable players in the Global High-Voltage BCD Power IC Market include Vishay Intertechnology, Power Integrations, Renesas Electronics, Maxim Integrated, ON Semiconductor (onsemi), Dialog Semiconductor, STMicroelectronics, Rohm Semiconductor, Diodes Incorporated, Texas Instruments, Alpha & Omega Semiconductor (AOS), Microchip Technology, Infineon Technologies, Analog Devices (ADI), Presto Engineering, NXP Semiconductors, GlobalFoundries, TSMC, UMC, and Magnachip Semiconductor. To strengthen market positioning, leading players are heavily investing in R&D for next-generation BCD architectures that support higher voltage ranges, enhanced thermal handling, and digital integration. Several companies are expanding their foundry partnerships to secure access to scalable and cost-effective fabrication capabilities. A strong emphasis is placed on automotive-grade qualification, enabling compliance with stringent safety and reliability standards. Firms are also focusing on modular chip designs that cater to application-specific power profiles.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry snapshot

- 2.2 Key market trends

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing electrification in automotive & industrial sectors

- 3.2.1.2 Rising demand for energy-efficient and compact designs

- 3.2.1.3 Expansion of 5G infrastructure and data centers

- 3.2.1.4 Government incentives for EV charging and power infrastructure

- 3.2.1.5 Advances in smart power IC features (SoC integration, diagnostics, protection)

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complexity and cost of advanced BCD process development

- 3.2.2.2 Thermal management and power dissipation issues at high voltages

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Sustainability measures

- 3.10.1 Sustainable materials assessment

- 3.10.2 Carbon footprint analysis

- 3.10.3 Circular economy implementation

- 3.10.4 Sustainability certifications and standards

- 3.10.5 Sustainability ROI analysis

- 3.11 Global consumer sentiment analysis

- 3.12 Patent analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Voltage Rating Type, 2021 - 2034 (USD Billion and Units)

- 5.1 Key trends

- 5.2 60V - 100V

- 5.3 100V - 200V

- 5.4 200V-500V

- 5.5 Above 500V

Chapter 6 Market Estimates and Forecast, By Process Node, 2021 - 2034 (USD Billion and Units)

- 6.1 Key trends

- 6.2 0.35 µm

- 6.3 0.18 µm

- 6.4 0.13 µm

- 6.5 Below 90 nm

Chapter 7 Market Estimates and Forecast, By Packaging Type, 2021 - 2034 (USD Billion and Units)

- 7.1 Key trends

- 7.2 QFN (Quad Flat No-Lead)

- 7.3 WLCSP (Wafer-Level Chip-Scale Package)

- 7.4 BGA (Ball Grid Array)

- 7.5 Die/Chip-on-Board (for integrated modules)

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion and Units)

- 8.1 Key trends

- 8.2 Automotive (EV/HEV powertrain, ADAS, lighting)

- 8.3 Consumer Electronics (power adapters, battery management, fast chargers)

- 8.4 Industrial (motor drives, automation equipment, robotics)

- 8.5 Telecommunications (5G infrastructure, power amplifiers)

- 8.6 Medical Devices (portable diagnostic and therapeutic devices)

- 8.7 Aerospace & Defense (radar systems, communication equipment)

- 8.8 Data Centers & Cloud Infrastructure (server power supplies, DC-DC converters)

Chapter 9 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion and Units)

- 9.1 Key trends

- 9.2 Power Management

- 9.3 Motor Control

- 9.4 Battery Management Systems (BMS)

- 9.5 LED Lighting Drivers

- 9.6 Voltage Regulation and Conversion

- 9.7 Signal Conditioning & Protection

- 9.8 Audio Amplifiers

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion and Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 STMicroelectronics

- 11.2 Texas Instruments

- 11.3 Infineon Technologies

- 11.4 Infineon Technologies

- 11.5 NXP Semiconductors

- 11.6 Renesas Electronics

- 11.7 Rohm Semiconductor

- 11.8 Analog Devices (ADI)

- 11.9 Diodes Incorporated

- 11.10 Microchip Technology

- 11.11 TSMC

- 11.12 GlobalFoundries

- 11.13 UMC

- 11.14 Vishay Intertechnology

- 11.15 Dialog Semiconductor

- 11.16 Maxim Integrated

- 11.17 Power Integrations

- 11.18 Alpha & Omega Semiconductor (AOS)

- 11.19 Magnachip Semiconductor

- 11.20 Presto Engineering

世界功率半导体市场、材料与技术

世界功率半导体市场、材料与技术 NFC标籤IC市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、形状、材质、最终用户及功能划分双极电晶体市场分析及预测(至2035年):依类型、产品类型、技术、应用、材料类型、元件、最终用户、功能、装置及製程划分

NFC标籤IC市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、形状、材质、最终用户及功能划分双极电晶体市场分析及预测(至2035年):依类型、产品类型、技术、应用、材料类型、元件、最终用户、功能、装置及製程划分 全球BCD功率IC市场规模、份额、趋势和成长分析报告(2026-2034年)

全球BCD功率IC市场规模、份额、趋势和成长分析报告(2026-2034年) 全球半导体电源完整性市场:预测(至 2034 年)-按解决方案类型、组件、技术、应用、最终用户和地区分類的分析

全球半导体电源完整性市场:预测(至 2034 年)-按解决方案类型、组件、技术、应用、最终用户和地区分類的分析 2026年全球高压双极型、互补金属氧化物半导体(BCD)及扩散金属氧化物半导体(DMOS)功率积体电路(IC)市场报告

2026年全球高压双极型、互补金属氧化物半导体(BCD)及扩散金属氧化物半导体(DMOS)功率积体电路(IC)市场报告 全球BCD功率IC市场,2026-2030年

全球BCD功率IC市场,2026-2030年 功率半导体:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

功率半导体:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 硅(Si)功率元件市场规模、份额和成长分析(按类型、应用和地区划分)-2026-2033年产业预测

硅(Si)功率元件市场规模、份额和成长分析(按类型、应用和地区划分)-2026-2033年产业预测 功率半导体市场规模、份额及成长分析(按组件、材料、应用及地区划分)-2026-2033年产业预测

功率半导体市场规模、份额及成长分析(按组件、材料、应用及地区划分)-2026-2033年产业预测