|

市场调查报告书

商品编码

1797809

着色剂和助剂市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Colorants and Auxiliaries Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

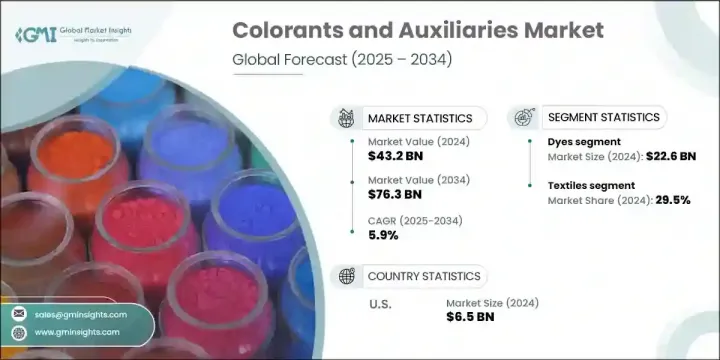

2024年,全球着色剂和助剂市场规模达432亿美元,预计到2034年将以5.9%的复合年增长率成长,达到763亿美元。着色剂和助剂对于提升汽车、塑胶、建筑和纺织等关键产业的产品外观、稳定性和功能性至关重要。这些配方包含染料、颜料、分散剂、紫外线稳定剂和加工助剂等高性能添加剂,所有这些添加剂都有助于提高色彩精度、产品耐久性和生产效率。随着各行各业面临越来越大的环保压力,市场对环保且注重性能的解决方案的需求日益强烈。

製造商越来越重视符合法规合规性和永续发展目标的生物基和低VOC产品线。向先进製造和智慧材料的转变正在推动该行业的创新,尤其是在数位着色系统和多功能添加剂技术领域。这些进步与注重资源效率和生态影响的全球标准和永续发展倡议相一致。全行业的创新持续加速下一代着色剂的开发,旨在应对现代生产挑战并满足消费者偏好。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 432亿美元 |

| 预测值 | 763亿美元 |

| 复合年增长率 | 5.9% |

2024年,纺织品领域占了29.5%的市场。在这一领域,着色剂对于在织物处理中创造丰富持久的色调和功能性整理至关重要。这些添加剂在提供紫外线防护、鲜艳外观和耐磨性方面也发挥着重要作用。在市占率领先的建筑业中,着色剂被广泛用于提升材料的美观度和增强表面在环境暴露下的耐久性。汽车产业紧随其后,该产业高度依赖专用的耐热颜料和添加剂来获得卓越的表面光洁度和极端条件下的色彩表现。

2024年,染料市场产值达226亿美元,成为全球着色剂和助剂市场最突出的贡献者之一。由于纺织、皮革、造纸和个人护理等行业对鲜艳持久的色彩应用需求旺盛,该领域持续蓬勃发展。人们对环保和可生物降解染料的日益青睐,以及活性染料和分散染料配方的创新,进一步推动了市场扩张。

2024年,美国着色剂和助剂市场产值达65亿美元。美国市场主导地位得益于其完善的製造业基础、强大的研发生态系统以及先进着色技术的早期应用。食品、塑胶、纺织和汽车等行业的旺盛需求持续推动市场成长。各公司越来越注重永续配方,以降低毒性并实现卓越的色彩表现。创新驱动、安全环保的着色解决方案在美国市场日益受到青睐。

影响全球着色剂和助剂市场的主要行业参与者包括朗盛股份公司、赢创工业股份公司、巴斯夫欧洲公司、杜邦公司、费罗公司、德司达集团、亨斯迈公司、科慕公司、昂高管理有限公司和科莱恩股份公司。为了巩固竞争地位,着色剂和助剂行业的公司正在投资研发,旨在推出可持续的多功能解决方案。他们正在与材料科学创新者和消费品品牌合作,为各种应用客製化高性能添加剂。透过合併、收购和新建生产设施进行策略性地域扩张是有效满足区域需求的另一个重点。此外,许多参与者正在透过数位着色技术和生物基替代品来增强其产品组合,以符合不断变化的环境法规和消费者期望。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 市场机会

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 依材料类型

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 专利态势

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考虑

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依产品类型,2021-2034

- 主要趋势

- 染料市场分析

- 活性染料

- 分散染料

- 酸性染料

- 直接染料

- 还原染料

- 硫化染料

- 碱性染料

- 其他染料

- 颜料市场分析

- 无机颜料

- 二氧化钛

- 氧化铁

- 氧化铬

- 炭黑

- 其他无机颜料

- 有机颜料

- 偶氮颜料

- 酞菁颜料

- 喹吖啶酮颜料

- 其他有机颜料

- 特种颜料

- 无机颜料

- 助剂市场分析

- 界面活性剂

- 增稠剂

- 分散剂

- 消泡剂

- 润湿剂

- 流平剂

- 其他辅助材料

第六章:市场估计与预测:按应用,2021-2034

- 主要趋势

- 纺织品

- 棉纺织品

- 合成纺织品

- 羊毛和丝绸

- 技术纺织品

- 油漆和涂料

- 建筑涂料

- 汽车涂料

- 工业涂料

- 船舶涂料

- 粉末涂料

- 塑胶和聚合物

- 包装塑胶

- 汽车塑料

- 建筑塑胶

- 消费品塑料

- 印刷油墨

- 胶印油墨

- 数位印刷油墨

- 柔版印刷油墨

- 凹印油墨

- 网版印刷油墨

- 食品和饮料

- 饮料

- 糖果

- 烘焙产品

- 乳製品

- 加工食品

- 化妆品和个人护理

- 纸和纸浆

- 皮革

- 其他应用

第七章:市场估计与预测:按最终用途产业,2021-2034 年

- 主要趋势

- 建筑业

- 汽车产业

- 包装产业

- 医疗保健和製药

- 电子和电气

- 农业

- 航太和国防

- 海洋产业

- 其他行业

第八章:市场估计与预测:依形式,2021-2034

- 主要趋势

- 液体形式

- 粉状

- 颗粒

- 糊状

- 其他形式

第九章:市场估计与预测:按地区,2021-2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第十章:公司简介

- BASF SE

- Clariant AG

- DuPont de Nemours, Inc.

- Huntsman Corporation

- Archroma Management GmbH

- DyStar Group

- LANXESS AG

- Evonik Industries AG

- The Chemours Company

- Ferro Corporation

The Global Colorants and Auxiliaries Market was valued at USD 43.2 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 76.3 billion by 2034. Colorants and auxiliary agents are critical to enhancing product appearance, stability, and functionality across key industries such as automotive, plastics, construction, and textiles. These formulations consist of high-performance additives like dyes, pigments, dispersants, UV stabilizers, and processing aids, all of which contribute to improved color precision, product durability, and manufacturing efficiency. With growing pressure on industries to adopt eco-conscious practices, the market is seeing strong demand for environmentally friendly and performance-oriented solutions.

Manufacturers are increasingly prioritizing bio-based and low-VOC product lines that align with regulatory compliance and sustainability targets. The shift toward advanced manufacturing and smart materials is fueling innovation in the sector, particularly in digital coloration systems and multifunctional additive technologies. These advancements align with global standards and sustainability initiatives focused on resource efficiency and ecological impact. Industry-wide innovation continues to accelerate the development of next-generation colorants designed to meet modern production challenges and consumer preferences.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $43.2 Billion |

| Forecast Value | $76.3 Billion |

| CAGR | 5.9% |

In 2024, the textiles segment accounted for a 29.5% share. In this segment, colorants are essential for creating rich, lasting hues and functional finishes in fabric treatments. These additives also play an important role in delivering UV protection, vibrant appearance, and resistance to wear. In the construction industry, which leads in market share, colorants are widely used for enhancing material aesthetics and boosting surface durability against environmental exposure. The automotive sector follows closely, relying heavily on specialized, heat-tolerant pigments and additives for premium surface finishes and color performance under extreme conditions.

The dyes segment generated USD 22.6 billion in 2024, making it one of the most prominent contributors to the global colorants and auxiliaries market. This segment continues to thrive due to high demand from industries such as textiles, leather, paper, and personal care, where vibrant and long-lasting color application is critical. The growing preference for eco-friendly and biodegradable dyes, alongside innovations in reactive and disperse dye formulations, has further supported market expansion.

U.S. Colorants and Auxiliaries Market generated USD 6.5 billion in 2024. The country's dominance is supported by its well-established manufacturing base, robust R&D ecosystem, and early adoption of advanced coloring technologies. High demand from industries such as food, plastics, textiles, and automotive continues to drive growth. Companies are increasingly focused on sustainable formulations that reduce toxicity while delivering high color performance. The trend toward innovation-driven, safe, and eco-friendly coloring solutions is gaining momentum across the U.S. market.

Major industry players influencing the Global Colorants and Auxiliaries Market include LANXESS AG, Evonik Industries AG, BASF SE, DuPont de Nemours, Inc., Ferro Corporation, DyStar Group, Huntsman Corporation, The Chemours Company, Archroma Management GmbH, and Clariant AG. To reinforce their competitive position, companies in the colorants and auxiliaries sector are investing in research and development aimed at introducing sustainable and multifunctional solutions. They are forming collaborations with material science innovators and consumer product brands to tailor high-performance additives for diverse applications. Strategic geographic expansion through mergers, acquisitions, and new production facilities is another key focus to meet regional demand efficiently. Additionally, many players are enhancing their product portfolios with digital coloration technologies and bio-based alternatives to comply with evolving environmental regulations and consumer expectations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Application trends

- 2.2.3 End user trends

- 2.2.4 Form trends

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By material type

- 3.9 Future market trends

- 3.10 Technology and Innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent Landscape

- 3.12 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Dyes market analysis

- 5.2.1 Reactive dyes

- 5.2.2 Disperse dyes

- 5.2.3 Acid dyes

- 5.2.4 Direct dyes

- 5.2.5 Vat dyes

- 5.2.6 Sulfur dyes

- 5.2.7 Basic dyes

- 5.2.8 Other dyes

- 5.3 Pigments market analysis

- 5.3.1 Inorganic pigments

- 5.3.1.1 Titanium dioxide

- 5.3.1.2 Iron oxide

- 5.3.1.3 Chrome oxide

- 5.3.1.4 Carbon black

- 5.3.1.5 Other inorganic pigments

- 5.3.2 Organic pigments

- 5.3.2.1 Azo pigments

- 5.3.2.2 Phthalocyanine pigments

- 5.3.2.3 Quinacridone pigments

- 5.3.2.4 Other Organic pigments

- 5.3.3 Specialty pigments

- 5.3.1 Inorganic pigments

- 5.4 Auxiliaries market analysis

- 5.4.1 Surfactants

- 5.4.2 Thickeners

- 5.4.3 Dispersants

- 5.4.4 Defoamers

- 5.4.5 Wetting agents

- 5.4.6 Leveling agents

- 5.4.7 Other auxiliaries

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Textiles

- 6.2.1 Cotton textiles

- 6.2.2 Synthetic textiles

- 6.2.3 Wool and silk

- 6.2.4 Technical textiles

- 6.3 Paints and coatings

- 6.3.1 Architectural coatings

- 6.3.2 Automotive coatings

- 6.3.3 Industrial coatings

- 6.3.4 Marine coatings

- 6.3.5 Powder coatings

- 6.4 Plastics and polymers

- 6.4.1 Packaging plastics

- 6.4.2 Automotive plastics

- 6.4.3 Construction plastics

- 6.4.4 Consumer goods plastics

- 6.5 Printing inks

- 6.5.1 Offset printing inks

- 6.5.2 Digital printing inks

- 6.5.3 Flexographic inks

- 6.5.4 Gravure inks

- 6.5.5 Screen printing inks

- 6.6 Food and beverages

- 6.6.1 Beverages

- 6.6.2 Confectionery

- 6.6.3 Bakery products

- 6.6.4 Dairy products

- 6.6.5 Processed foods

- 6.7 Cosmetics and personal care

- 6.8 Paper and pulp

- 6.9 Leather

- 6.10 Other applications

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Construction industry

- 7.3 Automotive industry

- 7.4 Packaging industry

- 7.5 Healthcare and pharmaceuticals

- 7.6 Electronics and electrical

- 7.7 Agriculture

- 7.8 Aerospace and defense

- 7.9 Marine industry

- 7.10 Other industries

Chapter 8 Market Estimates and Forecast, By Form, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Liquid form

- 8.3 Powder form

- 8.4 Granules

- 8.5 Paste form

- 8.6 Other forms

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 BASF SE

- 10.2 Clariant AG

- 10.3 DuPont de Nemours, Inc.

- 10.4 Huntsman Corporation

- 10.5 Archroma Management GmbH

- 10.6 DyStar Group

- 10.7 LANXESS AG

- 10.8 Evonik Industries AG

- 10.9 The Chemours Company

- 10.10 Ferro Corporation

全球纺织加工化学品市场规模、份额、趋势和成长分析报告(2026-2034年)

全球纺织加工化学品市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球纺织化学品市场报告2026年全球纺织品整理化学品市场报告

2026年全球纺织化学品市场报告2026年全球纺织品整理化学品市场报告 纺织品精炼剂市场按纤维类型、产品类型、製造流程、应用和分销管道划分,全球预测(2026-2032年)纺织品防水剂市场按剂型、配方、应用及最终用途产业划分-2026-2032年全球预测

纺织品精炼剂市场按纤维类型、产品类型、製造流程、应用和分销管道划分,全球预测(2026-2032年)纺织品防水剂市场按剂型、配方、应用及最终用途产业划分-2026-2032年全球预测 日本纺织化学品市场报告(按纤维类型、产品类型、应用和地区划分,2026-2034年)

日本纺织化学品市场报告(按纤维类型、产品类型、应用和地区划分,2026-2034年) 纺织化学品市场规模、份额和趋势分析:按製程、产品、应用、地区和细分市场预测(2025-2033 年)2025-2033年纺织化学品市场报告(按纤维类型、产品类型、应用和地区)

纺织化学品市场规模、份额和趋势分析:按製程、产品、应用、地区和细分市场预测(2025-2033 年)2025-2033年纺织化学品市场报告(按纤维类型、产品类型、应用和地区) 纺织化学品市场-全球产业规模、份额、趋势、机会及预测,按类型(着色剂、助剂、其他)、按应用(技术纺织品、家纺、服装、其他)、按地区及竞争情况划分,2020-2030 年预测纺织品整理化学品市场按化学品类型、应用、技术和纤维类型划分-2025-2032年全球预测

纺织化学品市场-全球产业规模、份额、趋势、机会及预测,按类型(着色剂、助剂、其他)、按应用(技术纺织品、家纺、服装、其他)、按地区及竞争情况划分,2020-2030 年预测纺织品整理化学品市场按化学品类型、应用、技术和纤维类型划分-2025-2032年全球预测