|

市场调查报告书

商品编码

1822660

藻类蛋白市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Algae Protein Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

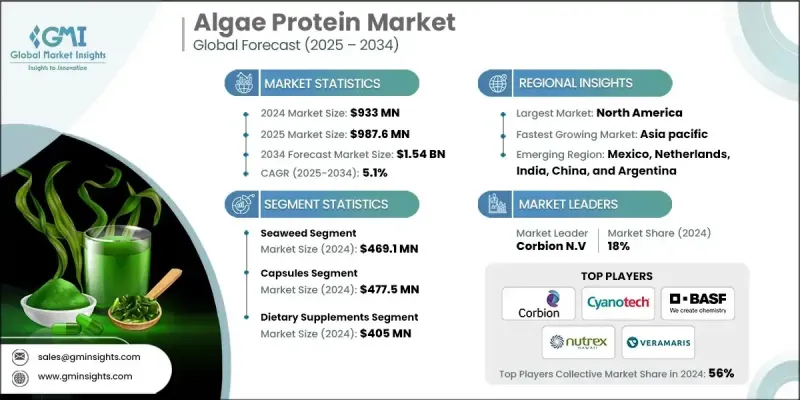

根据 Global Market Insights, Inc. 发布的最新报告,2024 年全球藻类蛋白市场价值为 9.33 亿美元,预计将从 2025 年的 9.876 亿美元增长到 2034 年的 15.4 亿美元,复合年增长率为 5.1%。全球向植物性饮食、永续来源产品和藻类产品的功能性健康益处的转变是决定市场方向的关键力量。

海藻和微藻蛋白,尤其是来自螺旋藻和小球藻的蛋白,在食品饮料、膳食补充剂和营养保健品中越来越常见。它们是生物利用度最高的蛋白质之一,营养全面,富含必需胺基酸,有益于增强免疫力、提升能量和肌肉。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 9.33亿美元 |

| 预测值 | 15.4亿美元 |

| 复合年增长率 | 5.1% |

关键驱动因素:

- 以植物为基础的纯素食生活方式正变得越来越普遍:人们正在积极寻求可持续的、无残忍的和全蛋白质的食物。

- 藻类蛋白的实际益处:藻类成分支持能量、新陈代谢和免疫系统功能,并具有抗发炎作用。

- 培养和极小的空间使用:藻类的生产需要更少的自然资源,这符合全球永续发展倡议。

- 在食品饮料和膳食补充剂应用中的用途增加:藻类蛋白在胶囊、粉末和强化食品生产中的用途大幅增加,特别是在运动和营养健康应用中。

关键参与者:

藻类蛋白市场由前 7 大公司主导:Corbion NV、Cyanotech Corporation、BASF SE、Nutrex Hawaii Inc.、Veramaris、ENERGYbits Inc. 和 Roquette Freres,它们在 2024 年共占据约 56% 的市场份额,面临以下主要挑战:

主要挑战:

- 某些地区消费者意识较低:提高消费者对藻类的健康和永续性益处的认识是需要克服的关键挑战。

- 风味与质地:某些藻类蛋白质具有泥土或海洋风味,有时不适合某些食品应用。

- 地理监管的复杂性:在某些地区,藻类被归类为新型食品,这阻碍了它在市场上的发展。

1. 依来源分类-海藻占据市场主导地位

海藻蛋白因其天然普遍性、永续生产以及在食品和营养保健领域的多种应用,将在2024年引领藻类蛋白市场。红藻和褐藻都富含蛋白质和生物活性成分,有助于促进代谢健康。

2. 依剂型分类-胶囊维持强劲份额

胶囊已成为藻类蛋白补充品市场的宠儿。胶囊具有便利性、更长的保质期和精准的剂量,这些优势能够提升消费者的信任度,并促进他们坚持健康养生。

3. 依应用分类-膳食补充品领先

膳食补充剂在 2024 年占据了最大的应用。藻类蛋白作为天然产品和浓缩营养素不断引入营养领域,在复合维生素、免疫增强剂和运动营养方面开闢了更多的应用。

4. 按地区划分-北美市场占据主导地位;

北美地区仍然是藻类蛋白的主要区域市场,因为消费者的健康意识不断增强,对清洁标籤和永续产品的需求不断增长,以及藻类补充剂品牌在零售和电子商务中的存在感不断增强。

藻类蛋白质产业的主要参与者包括 AlgalR NutraPharms Pvt Ltd、BASF SE、Corbion、Cyanotech Corporation、ENERGYbits Inc、Far East Bio-Tec Co. Ltd、福清金达姆萨螺旋藻有限公司、Heliae Development LLC、JUNE Spirulina、Nutrex Hawaii 和 Verquette Fres。

现有企业正在投资研发、地理扩张和垂直整合,以提高藻类培养、萃取技术和产品品质。 Roquette Freres 和 Veramaris 专注于基于可持续性的海藻种植和用于补充剂级用途的优质蛋白质提取。 ENERGYbits Inc. 和 Cyanotech Corporation 正在为运动员和健康爱好者开发胶囊产品。与食品科技企业的合作以及将藻类纳入即食产品形式,进一步提升了市场占有率。

目录

第一章:方法论与范围

第 2 章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商概况

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 全球对永续和环保蛋白质来源的需求不断增长。

- 素食主义和植物性饮食日益普及。

- 政府采取措施促进藻类产品生产。

- 产业陷阱与挑战

- 藻类蛋白质培养的生产成本高且可扩展性有限。

- 消费者对藻类营养的认知度低且了解有限。

- 市场机会

- 对永续和植物性蛋白质替代品的需求不断增长。

- 生物技术和栽培技术的进步。

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 价格趋势

- 按地区

- 按产品

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 专利态势

- 贸易统计资料(HS 编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 多边环境协定

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按来源,2021 - 2034 年

- 主要趋势

- 海藻

- 褐藻

- 绿藻

- 红藻

- 微藻

- 螺旋藻(蓝绿藻)

- 小球藻(绿藻)

- 其他的

第六章:市场估计与预测:按剂型,2021 - 2034

- 主要趋势

- 胶囊

- 液体

- 粉末

- 其他的

第七章:市场估计与预测:按应用,2021 - 2034

- 主要趋势

- 膳食补充剂

- 食品和饮料

- 烘焙和糖果

- 蛋白质饮料

- 早餐麦片

- 小吃

- 动物饲料

- 化妆品

- 其他的

第八章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第九章:公司简介

- AlgalR NutraPharms Pvt Ltd

- BASF SE

- Corbion

- Cyanotech Corporation

- ENERGYbits Inc

- Far East Bio-Tec Co. Ltd

- Fuqing King Dnarmsa Spirulina Co., Ltd

- Heliae Development LLC

- JUNE Spirulina

- Nutrex Hawaii Inc

- Roquette Freres

- Veramaris

The global algae protein market was valued at USD 933 million in 2024 and is projected to grow from USD 987.6 million in 2025 to USD 1.54 billion by 2034, expanding at a CAGR of 5.1%, according to the latest report published by Global Market Insights, Inc. The global movement toward plant-based diets, sustainably sourced products, and the functional health benefits of algae-based products are the key forces defining the direction of the market.

Seaweed and microalgal protein-especially from spirulina and chlorella-are increasingly commonplace in food and beverage, dietary supplements, and nutraceuticals. It has one of the highest bioavailable proteins, is nutritionally complete with essential amino acids, and benefits immunity, energy, and muscle.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $933 Million |

| Forecast Value | $1.54 Billion |

| CAGR | 5.1% |

Key Drivers:

- The plant-based and vegan way of life is becoming increasingly common: Individuals are actively seeking sustainable, cruelty-free, and whole protein foods.

- The real-world benefits of algae protein: Algae ingredients support energy, metabolism, and immune system function and have anti-inflammatory effects.

- Cultured and very minimal space use: Algae needs fewer natural resources to produce, which aligns with global sustainability initiatives.

- Increased uses in food & beverage and dietary supplement applications: Algae protein has substantially increased uses in the production of capsules, powders, and fortified foods, especially in applications for sports and nutritional health.

Key Players:

The algae protein market is dominated by the top 7 players: Corbion N.V, Cyanotech Corporation, BASF SE, Nutrex Hawaii Inc., Veramaris, ENERGYbits Inc. and Roquette Freres, which together comprise approximately 56% of the market share in 2024, with the following key challenges:

Key Challenges:

- Low consumer awareness in certain geography: Raising consumer awareness of the health and sustainability benefits of algae is a key challenge to overcome.

- Flavor and texture: Certain algae proteins have earthy or oceanic flavors that are sometimes unsuitable for certain food applications.

- Geographical regulatory complexities: Algae is classified as a novel food in some geographies, and this is holding it up in the market.

1. By Source - Seaweed Dominates the Market

Seaweed proteins lead the algae protein market in 2024 because of their natural prevalence, sustainable production and multiple applications in food and nutraceutical sectors. Both red and brown seaweeds are particularly rich in protein and bioactive components that assist in metabolic health.

2. By Dosage Form - Capsules Maintain Strong Share

Capsules became the favored format in the algae protein supplement market. Capsules provide convenience, improved shelf life, and precise dosing-drivers of consumer trust and adherence to wellness regimens.

3. By Application - Dietary Supplements Lead

Dietary supplements held the largest application share in 2024. The continual introduction of algae protein into the nutrition space as a natural product and concentrated nutrients has opened even more applications in multivitamins, immunity boosters and sports nutrition.;

4. By Region - North America Topped the Market;

The North America region remains the leading regional market for algae protein because of the growing health-conscious consumer segment, the rising demand for clean-label and sustainable products, and the growing presence of algae-based supplement brands in retail and e-commerce.

Key players in the algae protein industry are AlgalR NutraPharms Pvt Ltd, BASF SE, Corbion, Cyanotech Corporation, ENERGYbits Inc, Far East Bio-Tec Co. Ltd, Fuqing King Dnarmsa Spirulina Co., Ltd, Heliae Development LLC, JUNE Spirulina, Nutrex Hawaii Inc, Roquette Freres, and Veramaris.

Incumbent players are investing in R&D, geographic expansion, and vertical integration to increase algae culture, extraction technologies, and product quality. Roquette Freres and Veramaris are emphasizing seaweed cultivation based on sustainability and protein quality extraction for supplement-grade usage. ENERGYbits Inc. and Cyanotech Corporation are developing capsule product offerings for athletes and health enthusiasts. Collaborations with food tech ventures and the inclusion of algae in ready-to-consume formats are further driving market presence.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Source

- 2.2.3 Dosage Form

- 2.2.4 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing global demand for sustainable and eco-friendly protein sources.

- 3.2.1.2 Rising prevalence of veganism and plant-based diets.

- 3.2.1.3 Government initiatives to boost algae products production.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs and scalability limitations in algae protein cultivation.

- 3.2.2.2 Low consumer awareness and limited familiarity with algae-based nutrition.

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for sustainable and plant-based protein alternatives.

- 3.2.3.2 Advancements in biotechnology and cultivation techniques.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation Landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Source, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Seaweed

- 5.2.1 Brown algae

- 5.2.2 Green algae

- 5.2.3 Red algae

- 5.3 Micro algae

- 5.3.1 Spirulina (blue-green algae)

- 5.3.2 Chlorella (green algae)

- 5.3.3 Others

Chapter 6 Market Estimates and Forecast, By Dosage Form, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Capsules

- 6.3 Liquid

- 6.4 Powder

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Dietary supplements

- 7.3 Food & beverage

- 7.3.1 Bakery & confectionery

- 7.3.2 Protein drinks

- 7.3.3 Breakfast cereals

- 7.3.4 Snacks

- 7.4 Animal feed

- 7.5 Cosmetics

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 AlgalR NutraPharms Pvt Ltd

- 9.2 BASF SE

- 9.3 Corbion

- 9.4 Cyanotech Corporation

- 9.5 ENERGYbits Inc

- 9.6 Far East Bio-Tec Co. Ltd

- 9.7 Fuqing King Dnarmsa Spirulina Co., Ltd

- 9.8 Heliae Development LLC

- 9.9 JUNE Spirulina

- 9.10 Nutrex Hawaii Inc

- 9.11 Roquette Freres

- 9.12 Veramaris