|

市场调查报告书

商品编码

1871090

植物蛋白市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Plant-Based Protein Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

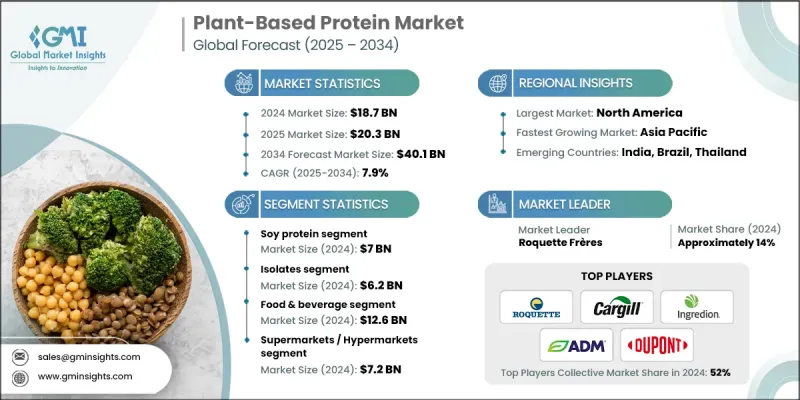

2024 年全球植物蛋白市场价值为 187 亿美元,预计到 2034 年将以 7.9% 的复合年增长率增长至 401 亿美元。

过去几年,在消费者日益关注健康、永续性和免疫力提升的推动下,植物蛋白已从利基市场发展成为全球主流市场。新冠疫情进一步加速了这项需求,消费者寻求保质期长、营养丰富且不含肉类的蛋白质替代品。由于人们对红肉和加工肉类对环境和健康的影响日益关注,北美和欧洲市场成长尤为强劲。弹性素食的日益普及以及消费者对永续植物性食品兴趣的不断增长,促使各大品牌拓展产品线。包括奶昔、高蛋白食品和乳製品替代品在内的无肉替代品已被广泛接受,进一步巩固了市场的快速扩张和长期成长势头。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 187亿美元 |

| 预测值 | 401亿美元 |

| 复合年增长率 | 7.9% |

2024年,大豆蛋白市场规模达70亿美元,预计2025年至2034年间将以7.2%的复合年增长率成长。大豆、豌豆和小麦蛋白因其高蛋白质含量和成熟的加工网络,仍是主要的蛋白质来源。大豆蛋白在肉类替代品和无乳製品生产中继续占据主导地位,而豌豆蛋白因其不含过敏原和非基因改造特性而日益受到关注。小麦蛋白因其组织化形式而备受欢迎,这些形式是烘焙产品和即食食品的必需原料。

2024年,分离蛋白市场规模达到62亿美元,预计2034年将以8%的复合年增长率成长。分离蛋白具有高纯度和生物利用度,在运动营养、膳食补充剂和蛋白饮料领域占据主导地位。浓缩蛋白价格实惠且营养均衡,在主流食品中保持良好的市场地位。组织化蛋白能够提供肉类替代品所需的咀嚼感和口感,进而推动植物肉和即食食品的创新。

2024年美国植物蛋白市场规模达45亿美元,预计2025年至2034年将以7.3%的复合年增长率成长。此市场成长的主要驱动力是富含蛋白质的功能性食品、清洁标籤膳食补充剂以及植物性替代品的广泛零售通路。成熟的供应链和强大的品牌影响力使得产品能够透过超市和线上健康平台快速渗透市场。功能性食品中对豌豆蛋白、大豆蛋白和米蛋白的需求不断增长,促使食品科技公司加大投资。符合FDA标准的包装高蛋白食品受益于强调健康益处的行销策略和监管框架。

植物蛋白市场的主要参与者包括罗盖特兄弟公司 (Roquette Freres)、ADM(阿彻丹尼尔斯公司)、嘉吉公司 (Cargill)、英联食品公司 (Ingredion Inc.) 和杜邦营养品公司 (DuPont Nutrition)。这些公司正利用创新、策略合作和全球扩张来巩固其市场地位。研发投入的重点在于提升蛋白质的功能性、风味和营养价值,以吸引主流消费者。与食品製造商、零售连锁店和线上平台的合作确保了更广泛的分销管道和更快的市场渗透。各公司强调永续性和清洁标籤认证,以符合消费者价值观和监管要求。产品多元化,涵盖肉类替代品、功能性饮料和乳製品替代品,有助于吸引更多消费族群。透过宣传健康益处、不含过敏原以及环保生产方式的行销活动,企业得以建立品牌信誉。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基准估算和计算

- 基准年计算

- 市场估算的关键趋势

- 初步研究和验证

- 原始资料

- 预测模型

- 研究假设和局限性

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 产业陷阱与挑战

- 市场机会

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 价格趋势

- 按地区

- 未来市场趋势

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 专利格局

- 贸易统计(註:仅提供重点国家的贸易统计)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依类型划分,2025-2034年

- 主要趋势

- 大豆蛋白

- 豌豆蛋白

- 小麦蛋白

- 米蛋白

- 马铃薯蛋白

- 菜籽蛋白

- 其他的

第六章:市场估算与预测:依产品类型划分,2025-2034年

- 主要趋势

- 分离物

- 浓缩物

- 组织化蛋白

- 水解物

第七章:市场估计与预测:依应用领域划分,2025-2034年

- 主要趋势

- 食品和饮料

- 肉类替代品及类似物

- 乳製品替代品

- 烘焙和糖果

- 运动营养补充品

- 功能性饮料

- 动物饲料(宠物食品、牲畜饲料)

- 化妆品及个人护理

- 製药

第八章:市场估算与预测:依配销通路划分,2025-2034年

- 主要趋势

- 线上零售

- 超市/大型超市

- 专卖店

- 企业对企业(B2B 供应)

第九章:市场估计与预测:依地区划分,2025-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第十章:公司简介

- Roquette Freres

- Cargill

- Ingredion Inc.

- ADM (Archer Daniels)

- DuPont Nutrition

- Kerry Group

- Burcon NutraScience

- Tate & Lyle

- Glanbia Nutritionals

- Puris

- CHS Inc.

- Farbest Brands

- Beneo GmbH

- Emsland Group

- NOW Health Group

The Global Plant-Based Protein Market was valued at USD 18.7 Billion in 2024 and is estimated to grow at a CAGR of 7.9% to reach USD 40.1 Billion by 2034.

Over the past several years, plant-based protein has transitioned from a niche segment to a mainstream global market, driven by growing consumer focus on health, sustainability, and immune support. The COVID-19 pandemic further accelerated demand as consumers sought shelf-stable, nutritious, and meat-free protein options. North America and Europe are witnessing particularly strong growth due to rising awareness around the environmental and health impacts of red and processed meat. The increasing popularity of flexitarian diets and growing interest in sustainable, plant-based foods have encouraged brands to diversify their offerings. Meat-free alternatives, including shakes, protein-rich foods, and dairy substitutes, have become widely accepted, reinforcing the market's rapid expansion and long-term growth trajectory.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $18.7 Billion |

| Forecast Value | $40.1 Billion |

| CAGR | 7.9% |

The soy protein segment generated USD 7 Billion in 2024 and is expected to grow at a CAGR of 7.2% between 2025 and 2034. Soy, pea, and wheat proteins remain the dominant sources due to high protein content and established processing networks. Soy continues to lead in the production of meat alternatives and dairy-free products, while pea protein is gaining traction for being allergen-free and non-GMO. Wheat protein remains popular for its textured forms, which are essential for bakery products and ready meals.

The isolates segment reached USD 6.2 Billion in 2024 and is forecasted to grow at 8% CAGR through 2034, as isolates provide high purity and bioavailability, dominating sports nutrition, dietary supplements, and protein beverages. Concentrates remain cost-effective with balanced nutrition, sustaining their presence in mainstream food products. Textured proteins drive innovation in plant-based meats and ready-to-eat meals by delivering the chew and texture expected in meat analogues.

U.S. Plant-Based Protein Market was valued at USD 4.5 Billion in 2024 and is projected to grow at a CAGR of 7.3% from 2025 to 2034. Growth is driven by protein-enriched functional foods, clean-label supplements, and broad retail distribution of plant-based alternatives. A mature supply chain and strong branding enable rapid market penetration through supermarkets and online health platforms. Increasing demand for pea, soy, and rice proteins in functional foods has spurred significant investments by food technology companies. High-protein packaged foods with FDA-compliant label claims benefit from marketing strategies and regulatory frameworks that emphasize health benefits.

Major players operating in the Plant-Based Protein Market include Roquette Freres, ADM (Archer Daniels), Cargill, Ingredion Inc., and DuPont Nutrition. Companies in the Plant-Based Protein Market are leveraging innovation, strategic partnerships, and global expansion to strengthen their market position. Investment in research and development focuses on improving protein functionality, flavor, and nutritional profiles to appeal to mainstream consumers. Partnerships with food manufacturers, retail chains, and online platforms ensure wider distribution and faster market penetration. Companies emphasize sustainability and clean-label certifications to align with consumer values and regulatory compliance. Product diversification into meat alternatives, functional beverages, and dairy substitutes helps capture multiple consumer segments. Marketing campaigns highlighting health benefits, allergen-free attributes, and eco-friendly production practices are used to build brand credibility.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Form

- 2.2.4 Application

- 2.2.5 Distribution Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2025 - 2034 (USD Million, Kilo Tons)

- 5.1 Key trends

- 5.2 Soy Protein

- 5.3 Pea Protein

- 5.4 Wheat Protein

- 5.5 Rice Protein

- 5.6 Potato Protein

- 5.7 Canola Protein

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Form, 2025 - 2034 (USD Million, Kilo Tons)

- 6.1 Key trends

- 6.2 Isolates

- 6.3 Concentrates

- 6.4 Textured Proteins

- 6.5 Hydrolysates

Chapter 7 Market Estimates and Forecast, By Application, 2025 - 2034 (USD Million, Kilo Tons)

- 7.1 Key trends

- 7.2 Food & Beverage

- 7.2.1 Meat Substitutes & Analogues

- 7.2.2 Dairy Alternatives

- 7.2.3 Bakery & Confectionery

- 7.2.4 Sports & Nutritional Supplements

- 7.2.5 Functional Beverages

- 7.3 Animal Feed (Pet Food, Livestock Feed)

- 7.4 Cosmetics & Personal Care

- 7.5 Pharmaceuticals

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2025 - 2034 (USD Million, Kilo Tons)

- 8.1 Key trends

- 8.2 Online Retail

- 8.3 Supermarkets/Hypermarkets

- 8.4 Specialty Stores

- 8.5 Business-to-Business (B2B Supply)

Chapter 9 Market Estimates and Forecast, By Region, 2025 - 2034 (USD Million, Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East & Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 Roquette Freres

- 10.2 Cargill

- 10.3 Ingredion Inc.

- 10.4 ADM (Archer Daniels)

- 10.5 DuPont Nutrition

- 10.6 Kerry Group

- 10.7 Burcon NutraScience

- 10.8 Tate & Lyle

- 10.9 Glanbia Nutritionals

- 10.10 Puris

- 10.11 CHS Inc.

- 10.12 Farbest Brands

- 10.13 Beneo GmbH

- 10.14 Emsland Group

- 10.15 NOW Health Group