|

市场调查报告书

商品编码

1871093

冷链物流设备市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Cold Chain Logistics Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

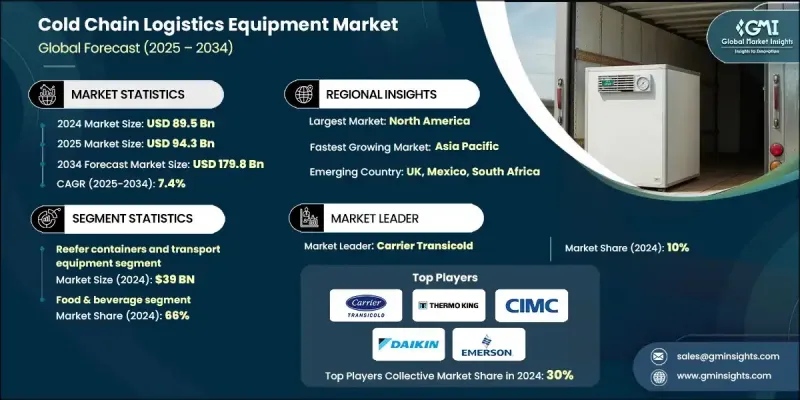

2024年全球冷链物流设备市场价值为895亿美元,预计2034年将以7.4%的复合年增长率成长至1,798亿美元。

全球对温度敏感型产品(例如药品、生物製剂、疫苗、新鲜农产品、海鲜、乳製品和冷冻食品)的需求不断增长,推动了市场成长。製药业高度依赖超低温储存和运输系统来保存生物製剂和mRNA疗法,对先进的冷藏物流设备产生了强劲的需求。同样,新鲜和有机食品消费量的成长也促使企业投资冷藏储存和运输系统,以确保整个供应链的产品安全和品质。随着全球化将易腐货物的流通范围扩展到各大洲,物流供应商越来越多地采用温控解决方案来保持产品完整性并减少变质。人们对食品安全和永续性的日益关注也加速了向先进冷链系统的转型,这些系统旨在从生产到最终交付始终保持稳定的温度条件。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 895亿美元 |

| 预测值 | 1798亿美元 |

| 复合年增长率 | 7.4% |

2024年,冷藏货柜及运输设备市场规模达390亿美元。这些冷藏货柜对国际物流至关重要,可在海运、铁路和公路等多模式过程中提供高效的温度控制,确保易腐货物在长途运输中保持品质。其适应性和可靠性使其成为全球冷链营运不可或缺的一部分。

2024年,食品饮料产业占了66%的市场份额,这主要得益于消费者对新鲜、天然和即食产品的偏好日益增长。为了防止产品变质和污染,精准的温度控制至关重要,这促使生产商、零售商和分销商大力投资先进的製冷基础设施,包括冷库、温度感测系统和冷藏运输车辆。这些投资有助于产品从农场到零售店的无缝流通,同时确保产品的高安全性和新鲜度。

2024年,美国冷链物流设备市场占78.2%的市场份额,市场规模达249亿美元。美国完善的基础设施、严格的监管环境以及对温控货物的强劲需求,使其成为全球冷链营运的重要枢纽。对智慧监控技术、冷库扩建和高效运输系统的持续投资,进一步巩固了美国在该领域的领先地位。蓬勃发展的电子商务、食品配送和製药业也为此成长提供了支撑,这些产业高度依赖可靠的冷链系统。

全球冷链物流设备市场的主要参与者包括开利运输冷冻(联合技术公司)、艾默生电气(科普兰)、江森自控、瑞科德、丹佛斯、ORBCOMM、德纳钢铁、大金工业、冷王(特灵科技)、博瑞达贸易製冷、TSSC、热力动力、中国国际海运冷王(特灵科技)、博瑞达贸易製冷、TSSC、热力动力、中国国际海运货柜运输有限公司(Canotti)。这些企业正采取多种策略来加强其全球影响力并保持竞争优势。领先的製造商正在投资先进的冷冻技术,例如节能压缩机、智慧感测器和即时监控系统,以改善温度控制并降低能耗。与物流供应商和食品生产商的策略合作与伙伴关係正在拓展分销网络并优化供应链。持续的研发投入专注于开发环保冷媒和永续设计,以满足全球环境标准。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 产业影响因素

- 成长驱动因素

- 对温度敏感产品的需求不断增长

- 生鲜电商和线上食品配送业务成长

- 永续性和绿色物流

- 产业陷阱与挑战

- 温度控制故障

- 高昂的营运和能源成本

- 机会

- 技术创新

- 模组化和移动式冷藏解决方案

- 成长驱动因素

- 成长潜力分析

- 未来市场趋势

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 依设备类型

- 监管环境

- 标准和合规要求

- 区域监理框架

- 认证标准

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依设备类型划分,2021-2034年

- 主要趋势

- 冷藏货柜和运输设备

- 标准冷藏货柜(10英尺、20英尺、40英尺)

- 冷藏卡车和拖车

- 专业海上货柜(DNV认证)

- 移动式製冷机组

- 冷库基础设施

- 模组化冷藏室

- 温控仓库

- 速冻设备

- 步入式冷藏室和冷冻室

- 监控系统

- 支援物联网的感测器

- 数据记录器和记录仪

- SCADA监控系统

- 区块链溯源平台

- 冷冻设备

- 中央冷冻系统

- 冷凝机组

- 压缩机和蒸发器

- 热交换器

第六章:市场估算与预测:依温度范围划分,2021-2034年

- 主要趋势

- 冷冻储存(-25°C 至 -18°C)

- 冷藏(0°C 至 +8°C)

- 冷藏(+8°C 至 +15°C)

- 环境温度加(+15°C 至 +25°C)

- 超低温(-70°C 至 -40°C)

第七章:市场估算与预测:依服务类型划分,2021-2034年

- 主要趋势

- 储存服务

- 交通运输服务

- 加值服务

- 速冻

- 标籤和包装

- 库存管理

- 品质管制

第八章:市场估算与预测:依应用领域划分,2021-2034年

- 主要趋势

- 餐饮

- 新鲜农产品(水果、蔬菜)

- 乳製品

- 肉类和海鲜

- 冷冻食品

- 加工食品

- 医药与医疗保健

- 疫苗和生物製剂

- 对温度敏感的药物

- 血液製品

- 医疗器材

- 化学品和工业

- 特种化学品

- 工业材料

- 电子元件

第九章:市场估算与预测:依最终用途划分,2021-2034年

- 主要趋势

- 物流和第三方物流供应商

- 食品製造商

- 製药公司

- 零售连锁店

- 电子商务平台

- 政府和医疗机构

第十章:市场估价与预测:依配销通路划分,2021-2034年

- 主要趋势

- 直接的

- 间接

第十一章:市场估计与预测:按地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十二章:公司简介

- Bureida Trading & Refrigeration

- Carrier Transicold (United Technologies)

- China International Marine Containers

- Coldstores Group of Saudi Arabia (CGS)

- Daikin Industries

- DANA Steel

- Danfoss

- Emerson Electric (Copeland)

- Johnson Controls

- ORBCOMM

- Rivacold

- Thermo King (Trane Technologies)

- Thermodynamics

- TSSC

- Zanotti spa

- Zhengzhou Kaixue Cold Chain

The Global Cold Chain Logistics Equipment Market was valued at USD 89.5 Billion in 2024 and is estimated to grow at a CAGR of 7.4% to reach USD 179.8 Billion by 2034.

Market growth is fueled by the increasing global demand for temperature-sensitive products such as pharmaceuticals, biologics, vaccines, fresh produce, seafood, dairy, and frozen foods. The pharmaceutical industry relies heavily on ultra-low-temperature storage and transport systems to preserve biologics and mRNA-based therapies, creating strong demand for advanced refrigerated logistics equipment. Similarly, the rising consumption of fresh and organic food products has prompted investments in refrigerated storage and transportation systems to ensure product safety and quality throughout the supply chain. With globalization extending the reach of perishable goods across continents, logistics providers are increasingly adopting temperature-controlled solutions to preserve product integrity and reduce spoilage. Growing awareness about food safety and sustainability is also accelerating the transition toward advanced cold chain systems designed to maintain consistent temperature conditions from production to final delivery.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $89.5 Billion |

| Forecast Value | $179.8 Billion |

| CAGR | 7.4% |

In 2024, the reefer containers and transport equipment segment generated USD 39 Billion. These refrigerated containers are vital for international logistics, offering efficient temperature control during multimodal transportation spanning sea, rail, and road, ensuring perishable goods maintain quality during long-distance shipment. Their adaptability and reliability make them indispensable for global cold chain operations.

The food & beverage sector held a 66% share in 2024, driven by rising consumer preference for fresh, natural, and ready-to-eat products. The need for precise temperature regulation to prevent spoilage and contamination has led producers, retailers, and distributors to invest heavily in advanced refrigeration infrastructure, including cold storage units, temperature-sensing systems, and refrigerated transport vehicles. These investments support seamless product movement from farms to retail outlets while maintaining high safety and freshness standards.

U.S. Cold Chain Logistics Equipment Market held 78.2% share and generated USD 24.9 Billion in 2024. The country's well-established infrastructure, strict regulatory environment, and strong demand for temperature-sensitive goods make it a major global hub for cold chain operations. Continuous investments in smart monitoring technologies, cold storage expansion, and efficient transportation systems are further strengthening the country's dominance. The growth is also supported by the thriving e-commerce, food delivery, and pharmaceutical industries, which rely heavily on reliable cold chain systems.

Key players in the Global Cold Chain Logistics Equipment Market include Carrier Transicold (United Technologies), Emerson Electric (Copeland), Johnson Controls, Rivacold, Danfoss, ORBCOMM, DANA Steel, Daikin Industries, Thermo King (Trane Technologies), Bureida Trading & Refrigeration, TSSC, Thermodynamics, China International Marine Containers, Zanotti Spa, Zhengzhou Kaixue Cold Chain, and Coldstores Group of Saudi Arabia (CGS). Companies in the Cold Chain Logistics Equipment Market are adopting multiple strategies to strengthen their global presence and maintain a competitive advantage. Leading manufacturers are investing in advanced refrigeration technologies, such as energy-efficient compressors, smart sensors, and real-time monitoring systems, to improve temperature control and reduce energy consumption. Strategic collaborations and partnerships with logistics providers and food producers are expanding distribution networks and optimizing supply chains. Continuous R&D efforts are focused on developing eco-friendly refrigerants and sustainable designs to meet global environmental standards.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment type

- 2.2.3 Temperature range

- 2.2.4 Service type

- 2.2.5 Application

- 2.2.6 End use industry

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for temperature-sensitive products

- 3.2.1.2 Growth in e-grocery and online food delivery

- 3.2.1.3 Sustainability and green logistics

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Temperature control failures

- 3.2.2.2 High operational and energy costs

- 3.2.3 Opportunities

- 3.2.3.1 Technological innovation

- 3.2.3.2 Modular and mobile cold storage solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By equipment type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Equipment Type, 2021 - 2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Reefer containers and transport equipment

- 5.2.1 Standard reefer containers (10ft, 20ft, 40ft)

- 5.2.2 Refrigerated trucks and trailers

- 5.2.3 Specialized offshore containers (DNV certified)

- 5.2.4 Mobile refrigeration units

- 5.3 Cold storage infrastructure

- 5.3.1 Modular cold rooms

- 5.3.2 Temperature-controlled warehouses

- 5.3.3 Blast freezing equipment

- 5.3.4 Walk-in coolers and freezers

- 5.4 Monitoring and control systems

- 5.4.1 IoT-enabled sensors

- 5.4.2 Data loggers and recorders

- 5.4.3 SCADA monitoring systems

- 5.4.4 Blockchain traceability platforms

- 5.5 Refrigeration equipment

- 5.5.1 Centralized refrigeration systems

- 5.5.2 Condensing units

- 5.5.3 Compressors and evaporators

- 5.5.4 Heat exchangers

Chapter 6 Market Estimates and Forecast, By Temperature Range, 2021 - 2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Frozen storage (-25°C to -18°C)

- 6.3 Chilled storage (0°C to +8°C)

- 6.4 Cool storage (+8°C to +15°C)

- 6.5 Ambient plus (+15°C to +25°C)

- 6.6 Ultra-low temperature (-70°C to -40°C)

Chapter 7 Market Estimates and Forecast, By Service Type, 2021 - 2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Storage services

- 7.3 Transportation services

- 7.4 Value-added services

- 7.4.1 Blast freezing

- 7.4.2 Labeling and packaging

- 7.4.3 Inventory management

- 7.4.4 Quality control

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Food & beverage

- 8.2.1 Fresh produce (fruits, vegetables)

- 8.2.2 Dairy products

- 8.2.3 Meat and seafood

- 8.2.4 Frozen foods

- 8.2.5 Processed foods

- 8.3 Pharmaceuticals & healthcare

- 8.3.1 Vaccines and biologics

- 8.3.2 Temperature-sensitive medicines

- 8.3.3 Blood products

- 8.3.4 Medical devices

- 8.4 Chemicals & industrial

- 8.4.1 Specialty chemicals

- 8.4.2 Industrial materials

- 8.4.3 Electronics components

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Logistics & 3PL providers

- 9.3 Food manufacturers

- 9.4 Pharmaceutical companies

- 9.5 Retail chains

- 9.6 E-commerce platforms

- 9.7 Government & healthcare institutions

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Direct

- 10.3 Indirect

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Bureida Trading & Refrigeration

- 12.2 Carrier Transicold (United Technologies)

- 12.3 China International Marine Containers

- 12.4 Coldstores Group of Saudi Arabia (CGS)

- 12.5 Daikin Industries

- 12.6 DANA Steel

- 12.7 Danfoss

- 12.8 Emerson Electric (Copeland)

- 12.9 Johnson Controls

- 12.10 ORBCOMM

- 12.11 Rivacold

- 12.12 Thermo King (Trane Technologies)

- 12.13 Thermodynamics

- 12.14 TSSC

- 12.15 Zanotti spa

- 12.16 Zhengzhou Kaixue Cold Chain

农产品低温运输物流市场预测至2032年:按组件、温度范围、运输方式、储存基础设施、技术、最终用户和地区分類的全球分析

农产品低温运输物流市场预测至2032年:按组件、温度范围、运输方式、储存基础设施、技术、最终用户和地区分類的全球分析 全球冷链物流市场:依技术、温度类型、解决方案、产业和地区划分-市场规模、产业趋势、机会分析和预测(2025-2033 年)

全球冷链物流市场:依技术、温度类型、解决方案、产业和地区划分-市场规模、产业趋势、机会分析和预测(2025-2033 年) 北美低温运输市场规模、份额和趋势分析报告:按类型、包装、设备、应用、国家和细分市场预测(2025-2033 年)

北美低温运输市场规模、份额和趋势分析报告:按类型、包装、设备、应用、国家和细分市场预测(2025-2033 年) 低温运输市场按温度范围、设备类型、服务模式、最终用户和分销管道划分-2025-2032 年全球预测低温运输物流市场(按服务类型、温度范围和最终用途)-全球预测,2025-2032全球低温运输物流自动化市场:2032 年预测 - 按组件、温度范围、应用、最终用户和地区分析

低温运输市场按温度范围、设备类型、服务模式、最终用户和分销管道划分-2025-2032 年全球预测低温运输物流市场(按服务类型、温度范围和最终用途)-全球预测,2025-2032全球低温运输物流自动化市场:2032 年预测 - 按组件、温度范围、应用、最终用户和地区分析 电动车、电气化与冷链运输:机会在哪里?

电动车、电气化与冷链运输:机会在哪里? 2025年低温运输全球市场报告2032 年低温运输物流市场预测:按类型、温度类型、应用和地区进行的全球分析2032 年水产品和生鲜产品农产品低温运输市场预测:按组件、温度类型、技术、应用、最终用户和地区进行的全球分析

2025年低温运输全球市场报告2032 年低温运输物流市场预测:按类型、温度类型、应用和地区进行的全球分析2032 年水产品和生鲜产品农产品低温运输市场预测:按组件、温度类型、技术、应用、最终用户和地区进行的全球分析