|

市场调查报告书

商品编码

1876533

汽车雷射焊接系统市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Automotive Laser Welding System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

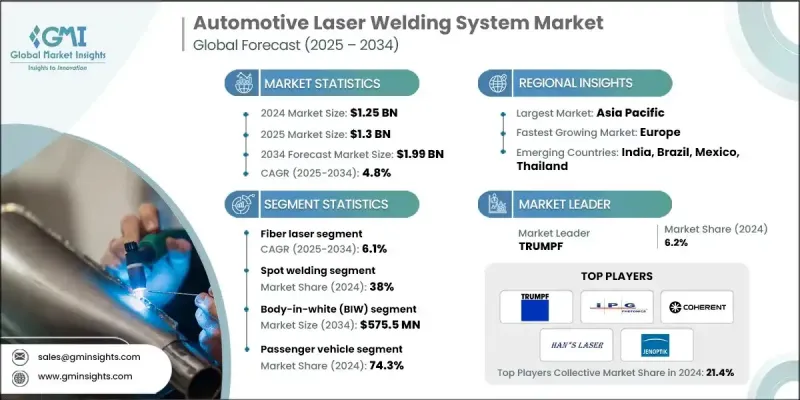

2024 年全球汽车雷射焊接系统市场价值为 12.5 亿美元,预计到 2034 年将以 4.8% 的复合年增长率增长至 19.9 亿美元。

在汽车产量不断增长和发展中经济体需求日益旺盛的推动下,汽车行业的稳步扩张为先进製造解决方案创造了强劲的发展机会。汽车製造商正积极投资雷射焊接技术,以期在满足不断演进的生产标准的同时,实现更高的精度、生产效率和更稳定的品质。高性能、轻量化汽车(尤其是采用铝合金和混合合金製造的汽车)的日益普及,进一步提升了对雷射焊接系统的需求。雷射焊接具有卓越的精度、极小的热变形和优异的强度保持率,使其成为连接薄型或异种材料的理想选择,且不会影响结构完整性。光束控制、自适应感测器和自动化监控技术的持续创新,提高了可靠性并减少了製造缺陷。这些进步不仅提高了生产效率,还确保了大规模生产环境中品质的一致性和可重复性,从而凸显了雷射焊接在现代汽车製造流程中的重要性。汽车生产中对自动化、数位化和永续性的日益重视,正在塑造市场的发展趋势。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 12.5亿美元 |

| 预测值 | 19.9亿美元 |

| 复合年增长率 | 4.8% |

预计2025年至2034年间,光纤雷射器市场将以6.1%的复合年增长率成长。光纤雷射具有卓越的光束精度、高能效以及焊接轻质和混合材料的能力,因此在汽车行业备受青睐。其焊接速度快、运行成本低等性能优势,正推动其在电动车製造和先进车身结构领域的应用。随着汽车製造商日益重视精度、耐用性和成本效益,光纤雷射系统正成为下一代生产设施的关键组成部分。

到2024年,点焊市占率将达到38%。雷射点焊仍然是车身组装的关键工艺,能够实现快速、牢固且精准的焊接。将机器人自动化和高功率光纤雷射整合到点焊製程中,可提高生产效率,最大限度地减少材料浪费,并确保焊接品质的稳定性。这项技术进步与汽车产业日益重视轻量化设计、加速生产週期和减少生产停机时间的趋势相契合。

2024年,美国汽车雷射焊接系统市占率达85.4%。美国在采用先进雷射焊接技术方面持续保持领先地位,尤其是在精度和可靠性要求极高的应用领域。电动车的日益普及、强劲的研发投入以及产业界与研究机构之间的紧密合作,共同推动了美国雷射焊接市场的创新发展。製造商们正着力提升生产品质和自动化水平,进一步推动了全国各地汽车工厂的技术整合。

全球汽车雷射焊接系统市场的主要企业包括TRUMPF、IPG Photonics、Coherent、Jenoptik、Han's Laser Technology、FANUC、Amada Weld Tech、Laserline、Golden Laser和Baison Laser。这些领导企业正透过技术创新、产能扩张和策略合作来巩固其市场地位。他们大力投资研发,以开发先进的雷射光源、即时监控解决方案和节能係统,从而满足不断变化的製造需求。与汽车OEM厂商和工业自动化供应商的合作,协助他们打造针对电动车和轻量化材料最佳化的客製化焊接平台。此外,各企业也不断扩大其业务版图和生产规模,以满足日益增长的全球需求。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基准估算和计算

- 基准年计算

- 市场估算的关键趋势

- 初步研究和验证

- 原始资料

- 预报

- 研究假设和局限性

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 原物料供应商

- 零件製造商

- 系统整合商

- OEM

- 最终用途

- 供应商格局

- 产业影响因素

- 成长驱动因素

- 汽车产能扩张

- 对高精度和轻质材料的需求

- 转向节能型製造工艺

- 雷射光束控制和监测系统的进展

- 电动车和混合动力车的普及率不断提高

- 产业陷阱与挑战

- 初始投资成本高

- 熟练的雷射焊接操作人员数量有限。

- 市场机会

- 电动和混合动力汽车领域的成长

- 电池模组和动力总成焊接应用领域的拓展

- 工业4.0和智慧製造的日益普及

- 多材料焊接解决方案的技术进步

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 目前技术

- 新兴技术

- 专利分析

- 价格趋势分析

- 按组件

- 按地区

- 成本分解分析

- 生产统计

- 生产中心

- 消费中心

- 进出口

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 未来趋势

- 汽车技术路线图与创新轨迹

- 新兴应用及市场拓展机会

- 自动驾驶车辆的影响及组件要求

- 永续製造与绿色技术融合

- 数位转型与智慧製造集成

- 汽车产业客户需求及产业优先事项

- 汽车品质对精度和重复性有很高的要求

- 机器人与自动化整合要求

- 电动车电池焊接规范与标准

- 符合 AWS D8.10 M 和 AIAG CQI-15 标准

- 汽车的能源效率和总拥有成本

- 本地服务网路和技术支援预期

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 重要新闻和倡议

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:雷射市场估算与预测:2021-2034年

- 主要趋势

- 光纤雷射

- 二氧化碳雷射

- 固态雷射

- 二极体雷射

第六章:市场估算与预测:依焊接产业划分,2021-2034年

- 主要趋势

- 点焊

- 缝焊

- 混合焊接

- 远端焊接

第七章:市场估计与预测:依应用领域划分,2021-2034年

- 主要趋势

- 白车身(BIW)

- 动力总成部件

- 电池製造(电动车)

- 排气系统

- 底盘和结构件

第八章:市场估算与预测:依车辆类型划分,2021-2034年

- 主要趋势

- 搭乘用车

- SUV

- 掀背车

- 轿车

- 商用车辆

- 低容量性状

- MCV

- C型肝炎

第九章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧

- 荷兰

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳新银行

- 新加坡

- 泰国

- 越南

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- 全球参与者

- Bystronic Laser

- Coherent

- FANUC

- Han's Laser Technology

- IPG Photonics

- Jenoptik

- TRUMPF

- 区域玩家

- Amada Weld Tech

- HGTECH

- Laser Photonics

- Laserax

- Precitec

- Prima Power

- Sino-Galvo Technology

- Emerson Electric (Branson Ultrasonics)

- 新兴参与者和颠覆者

- ALPHA LASER

- Baison Laser

- Control Laser

- Golden Laser

- KEYENCE

- Laserline

- LaserStar Technologies

- Miyachi Unitek

- Perfect Laser

- Sahajanand Laser Technology

The Global Automotive Laser Welding System Market was valued at USD 1.25 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 1.99 billion by 2034.

The steady expansion of the automotive sector, driven by rising vehicle production and growing demand in developing economies, is creating strong opportunities for advanced manufacturing solutions. Automakers are actively investing in laser welding technologies to achieve higher precision, productivity, and consistent quality while meeting evolving production standards. The increasing shift toward high-performance, lightweight vehicles made from aluminum and hybrid alloys is further amplifying the demand for laser-based welding systems. Laser welding offers exceptional accuracy, minimal thermal distortion, and superior strength retention, making it ideal for joining thin or dissimilar materials without compromising structural integrity. Continued innovation in beam control, adaptive sensors, and automated monitoring technologies enhances reliability and reduces manufacturing defects. These advancements not only improve production efficiency but also ensure uniform quality and repeatability across mass-production environments, reinforcing the importance of laser welding in modern automotive manufacturing processes. The market's evolution is being shaped by a growing focus on automation, digitalization, and sustainability in vehicle production.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.25 Billion |

| Forecast Value | $1.99 Billion |

| CAGR | 4.8% |

The fiber laser segment is anticipated to register a CAGR of 6.1% between 2025 and 2034. Its superior beam precision, energy efficiency, and ability to weld lightweight and mixed materials make fiber lasers highly favored in the automotive industry. Their performance benefits, including high welding speed and lower operating costs, are driving adoption in electric vehicle manufacturing and advanced body structures. As automakers emphasize precision, durability, and cost-effectiveness, fiber laser systems are becoming essential components of next-generation production facilities.

The spot welding segment accounted for a 38% share in 2024. Laser spot welding remains a critical process in vehicle body assembly, offering rapid, strong, and accurate welds. The integration of robotic automation and high-powered fiber lasers in spot welding enhances productivity, minimizes material waste, and ensures consistent weld quality. This technological progress aligns with the automotive industry's increasing focus on lightweight design, faster production cycles, and reduced downtime in manufacturing operations.

U.S. Automotive Laser Welding System Market held a share of 85.4% in 2024. The country continues to lead in adopting advanced laser welding technologies for applications demanding maximum precision and reliability. The growing commercialization of electric vehicles, robust R&D investments, and strong collaboration between industry and research institutions are sustaining innovation in laser welding within the U.S. market. Manufacturers are emphasizing high-quality production and automation, further driving technological integration in automotive plants nationwide.

Key companies operating in the Global Automotive Laser Welding System Market include TRUMPF, IPG Photonics, Coherent, Jenoptik, Han's Laser Technology, FANUC, Amada Weld Tech, Laserline, Golden Laser, and Baison Laser. Leading companies in the Automotive Laser Welding System Market are strengthening their market position through technological innovation, capacity expansion, and strategic partnerships. They are investing extensively in R&D to develop advanced laser sources, real-time monitoring solutions, and energy-efficient systems that meet evolving manufacturing needs. Collaborations with automotive OEMs and industrial automation providers are enabling the creation of customized welding platforms optimized for electric vehicles and lightweight materials. Companies are also expanding their geographic presence and production facilities to meet increasing global demand.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Laser

- 2.2.2 Welding

- 2.2.3 Application

- 2.2.4 Vehicle

- 2.2.5 Region

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material suppliers

- 3.1.1.2 Component manufacturers

- 3.1.1.3 System integrators

- 3.1.1.4 OEM

- 3.1.1.5 End use

- 3.1.1 Supplier landscape

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of automotive production capacity

- 3.2.1.2 Demand for high precision and lightweight materials

- 3.2.1.3 Shift toward energy-efficient manufacturing processes

- 3.2.1.4 Advancements in laser beam control and monitoring systems

- 3.2.1.5 Growing adoption of electric and hybrid vehicles

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment cost

- 3.2.2.2 Limited availability of skilled laser welding operators

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of electric and hybrid vehicle segment

- 3.2.3.2 Expansion in battery module and powertrain welding applications

- 3.2.3.3 Rising adoption of Industry 4.0 and smart manufacturing

- 3.2.3.4 Technological advancements in multi-material welding solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle east and Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technology

- 3.7.2 Emerging technology

- 3.8 Patent analysis

- 3.9 Price Trends Analysis

- 3.9.1 By component

- 3.9.2 By region

- 3.10 Cost Breakdown Analysis

- 3.11 Production statistics

- 3.11.1 Production hubs

- 3.11.2 Consumption hubs

- 3.11.3 Export and import

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

- 3.14 Future trends

- 3.14.1 Technology roadmap & innovation trajectory in automotive

- 3.14.2 Emerging applications & market expansion opportunities

- 3.14.3 Autonomous vehicle impact & component requirements

- 3.14.4 Sustainable manufacturing & green technology integration

- 3.14.5 Digital transformation & smart manufacturing integration

- 3.15 Automotive client requirements & industry priorities

- 3.15.1 High precision & repeatability demands for automotive quality

- 3.15.2 Robotics & automation integration requirements

- 3.15.3 Ev battery welding specifications & standards

- 3.15.4. Compliance with AWS D8.10 M:2021 & AIAG CQI-15 standards

- 3.15.5 Energy efficiency & total cost of ownership in automotive

- 3.15.6 Local service network & technical support expectations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key news and initiatives

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Laser, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Fiber laser

- 5.3 CO2 laser

- 5.4 Solid-state laser

- 5.5 Diode laser

Chapter 6 Market Estimates & Forecast, By Welding, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Spot welding

- 6.3 Seam welding

- 6.4 Hybrid welding

- 6.5 Remote welding

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Body-in-White (BIW)

- 7.3 Powertrain components

- 7.4 Battery manufacturing (EVs)

- 7.5 Exhaust systems

- 7.6 Chassis & structural parts

Chapter 8 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Passenger Vehicle

- 8.2.1 SUV

- 8.2.2 Hatchback

- 8.2.3 Sedan

- 8.3 Commercial Vehicle

- 8.3.1 LCV

- 8.3.2 MCV

- 8.3.3 HCV

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Netherlands

- 9.3.8 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 ANZ

- 9.4.5 Singapore

- 9.4.6 Thailand

- 9.4.7 Vietnam

- 9.4.8 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Bystronic Laser

- 10.1.2 Coherent

- 10.1.3 FANUC

- 10.1.4 Han's Laser Technology

- 10.1.5 IPG Photonics

- 10.1.6 Jenoptik

- 10.1.7 TRUMPF

- 10.2 Regional Players

- 10.2.1 Amada Weld Tech

- 10.2.2 HGTECH

- 10.2.3 Laser Photonics

- 10.2.4 Laserax

- 10.2.5 Precitec

- 10.2.6 Prima Power

- 10.2.7 Sino-Galvo Technology

- 10.2.8 Emerson Electric (Branson Ultrasonics)

- 10.3 Emerging Players and Disruptors

- 10.3.1 ALPHA LASER

- 10.3.2 Baison Laser

- 10.3.3 Control Laser

- 10.3.4 Golden Laser

- 10.3.5 KEYENCE

- 10.3.6 Laserline

- 10.3.7 LaserStar Technologies

- 10.3.8 Miyachi Unitek

- 10.3.9 Perfect Laser

- 10.3.10 Sahajanand Laser Technology

汽车机器人驱动装置市场分析与预测(至2035年):按类型、产品、服务、技术、组件、应用、流程、部署方式、最终用户和功能划分

汽车机器人驱动装置市场分析与预测(至2035年):按类型、产品、服务、技术、组件、应用、流程、部署方式、最终用户和功能划分 2026年全球自主充电机器人市场报告

2026年全球自主充电机器人市场报告 汽车机器人市场:2026-2032年全球市场预测(按机器人类型、组件、有效载荷能力、自主等级、应用和部署状态划分)

汽车机器人市场:2026-2032年全球市场预测(按机器人类型、组件、有效载荷能力、自主等级、应用和部署状态划分) 汽车机器人市场-策略洞察与预测(2026-2031年)汽车机器人市场规模、份额、成长率和全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测

汽车机器人市场-策略洞察与预测(2026-2031年)汽车机器人市场规模、份额、成长率和全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测 汽车机器人市场:按类型、应用、组件、技术、最终用户、国家和地区划分-全球产业分析、市场规模、市场份额及2025年至2032年预测

汽车机器人市场:按类型、应用、组件、技术、最终用户、国家和地区划分-全球产业分析、市场规模、市场份额及2025年至2032年预测 汽车机器人市场-全球产业规模、份额、趋势、机会及预测(依产品类型、组件、应用、地区及竞争格局划分,2021-2031年)

汽车机器人市场-全球产业规模、份额、趋势、机会及预测(依产品类型、组件、应用、地区及竞争格局划分,2021-2031年) 汽车喷涂机器人系统市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)汽车超音波焊接设备市场机会、成长动力、产业趋势分析及2025-2034年预测

汽车喷涂机器人系统市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)汽车超音波焊接设备市场机会、成长动力、产业趋势分析及2025-2034年预测 汽车和机器人工学的VLA大规模模式的应用(2025年)

汽车和机器人工学的VLA大规模模式的应用(2025年)