|

市场调查报告书

商品编码

1885876

植物-动物混合蛋白系统市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Hybrid Plant-Animal Protein System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

2024 年全球植物-动物混合蛋白系统市场价值为 10 亿美元,预计到 2034 年将以 17.9% 的复合年增长率增长至 53 亿美元。

这个市场的核心是混合蛋白系统,它将植物蛋白与动物性成分结合,旨在为未来的食品供应需求创造营养均衡、环境友善且可扩展的蛋白质来源。全球人口的成长和日益严峻的粮食安全压力持续推动着人们对混合蛋白形式的兴趣。世界各国政府都在推广更环保的食品生产方式,以推动气候目标,这进一步强化了对创新蛋白质解决方案的需求。消费者越来越倾向于灵活的饮食模式,减少肉类摄入,同时仍食用动物性产品,这使得混合蛋白成为颇具吸引力的折衷方案。目前,北美凭藉其先进的製造能力和监管支持,在混合蛋白的推广应用方面处于领先地位;而亚太地区则在收入增长、城市生活方式转变以及对可持续发展挑战日益增强的意识的推动下,正经历着快速增长。消费者对兼具营养、感官享受和环境效益的食品的日益增长的需求,正引导着製造商致力于开发能够提高效率、减少资源依赖并保持消费者熟悉度的混合蛋白创新产品。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 10亿美元 |

| 预测值 | 53亿美元 |

| 复合年增长率 | 17.9% |

2024年,植物-动物杂交产品市场规模预计将达到5.618亿美元。该市场占据强劲地位,因为杂交产品配方灵活,能够满足消费者对永续性的需求,同时又不牺牲产品原有风味和口感。研发和加工技术的显着进步正在提升杂交蛋白产品的感官和营养价值,使其在各类食品领域中广泛应用。

到了2024年,共挤出和组织化流程占48.7%的市场。这些加工方法之所以引领市场,是因为它们能够生产出纤维状、类似肉类的质地,并能高度还原传统蛋白质的结构。它们能够将植物性蛋白质和动物性蛋白质整合到具有凝聚力的高品质混合产品中,从而提升产品的感官表现。这些工艺的可扩展性以及对多成分配方的适用性,使其成为大规模生产商的首选技术。

预计2025年至2034年间,北美混合植物-动物蛋白系统市场将以17.9%的复合年增长率成长。消费者对可持续采购、透明度和符合道德规范的食品生产的日益关注,推动了对兼具动物蛋白营养密度和植物蛋白环境优势的混合产品的需求增长。弹性素食主义的兴起以及消费者对天然、清洁标籤产品的偏好,促使企业不断改进混合配方,以提升产品的风味、口感和功能性。

混合植物-动物蛋白系统市场的主要参与者包括嘉吉、ITC有限公司、枫叶食品、康尼格拉食品、JBS、泰森食品、Momentum Foods、Vion Food Group、Rugenwalder Muhle、50/50 Foods, Inc.、雀巢和荷美尔食品。各公司正透过扩大研发投入、推动加工技术以及与原料供应商和食品製造商建立策略联盟,来巩固其在混合植物-动物蛋白系统市场的地位。许多公司正在开发新一代的组织化和混合技术,以改善口感、营养均衡并确保产品品质的稳定性。对消费者研究的投入有助于公司根据不同地区的饮食偏好和永续发展需求,调整混合产品。製造商也在拓展产品组合,将混合产品纳入肉类替代品、即食食品和零食等类别。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 全球蛋白质需求不断成长及粮食安全问题

- 消费者转向弹性素食和减量素食

- 永续发展与气候变迁减缓目标

- 产业陷阱与挑战

- 高昂的生产成本与溢价挑战

- 消费者的怀疑与接受障碍

- 市场机会

- 食品製造商的B2B配料系统

- 人工培育的肉类-植物杂交商业化

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 未来市场趋势

- 专利格局

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依产品划分,2021-2034年

- 主要趋势

- 植物-动物杂交产品

- 人工培育的肉类-植物杂交产品

- 真菌蛋白-动物杂交产品

- 昆虫-植物杂交产品

- 微生物发酵-动物杂交产品

- 其他的

第六章:市场估算与预测:依生产流程划分,2021-2034年

- 主要趋势

- 共挤出和纹理化

- 发酵

- 酵素修饰

- 其他的

第七章:市场估计与预测:依应用领域划分,2021-2034年

- 主要趋势

- 全肌肉类似物混合物

- 牛排和菲力牛排的替代品

- 肉排和肉块形式

- 其他的

- 研磨/切碎的混合产品

- 汉堡肉饼

- 香肠和香肠串

- 肉丸和碎屑

- 其他的

- 加工混合产品

- 鸡块和鸡柳

- 成型肉饼和肉排

- 条状和块状

- 其他的

- 成分混合系统

- 蛋白质分离物和浓缩物

- 组织化植物蛋白(TVP)混合物

- 功能性蛋白质成分

- 其他的

- 即食混合餐

- 冷冻食品形式

- 冷藏预製餐

- 常温保存选项

- 餐点套装

- 其他的

- 其他的

第八章:市场估算与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第九章:公司简介

- 50/50 Foods, Inc

- Cargill

- Conagra Brands

- Hormel Foods

- ITC Limited

- JBS

- Maple Leaf Foods

- Momentum Foods

- Nestle SA

- Rugenwalder Muhle

- Tyson Foods

- Vion Food Group

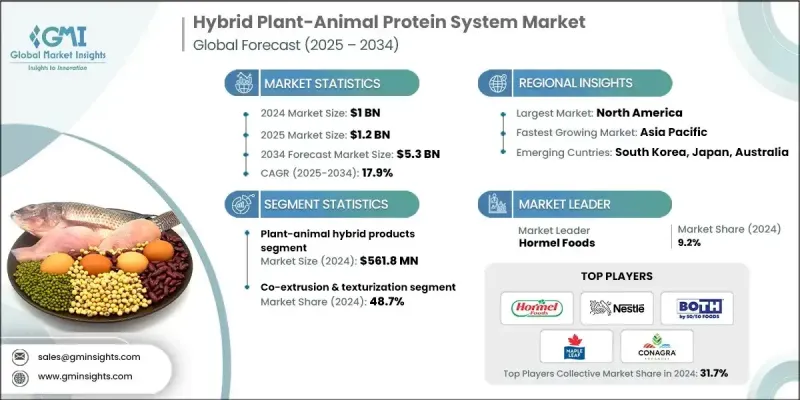

The Global Hybrid Plant-Animal Protein System Market was valued at USD 1 billion in 2024 and is estimated to grow at a CAGR of 17.9% to reach USD 5.3 billion by 2034.

This market centers on blended protein systems that integrate plant proteins with animal-derived components to create nutritionally balanced, environmentally conscious, and scalable protein sources for future food supply needs. Growing global population levels and rising pressure on food security continue to push interest in hybrid protein formats. Governments around the world are promoting greener food production practices to advance climate goals, reinforcing demand for innovative protein solutions. Consumers are increasingly adopting flexible eating patterns that reduce meat intake while still incorporating animal-based products, making hybrid proteins an appealing compromise. North America currently leads adoption due to its advanced manufacturing capabilities and regulatory support, while Asia Pacific is witnessing rapid growth driven by higher incomes, urban lifestyle shifts, and rising awareness of sustainability challenges. This growing openness toward foods that balance nutrition, sensory appeal, and environmental benefits is steering manufacturers toward hybrid protein innovations that improve efficiency, reduce resource dependency, and maintain consumer familiarity.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1 Billion |

| Forecast Value | $5.3 Billion |

| CAGR | 17.9% |

The plant-animal hybrid products segment generated USD 561.8 million in 2024. This segment holds a strong position because hybrid offerings provide adaptable formulations and resonate with consumers who want sustainability without sacrificing recognizable flavors and textures. Substantial advancements in research and processing technologies are enhancing the organoleptic and nutritional attributes of hybrid protein options, allowing them to gain traction across diverse food categories.

The co-extrusion and texturization processes segment accounted for a 48.7% share in 2024. These processing methods lead the market due to their ability to produce fibrous, meat-like textures that closely replicate traditional protein structures. Their capability to integrate plant and animal proteins into cohesive, high-quality hybrid formats supports better sensory performance. The scalability of these processes and suitability for multi-ingredient formulations make them preferred techniques for manufacturers operating at large production volumes.

North America Hybrid Plant-Animal Protein System Market is forecast to grow at a CAGR of 17.9% between 2025 and 2034. Rising consumer interest in sustainable sourcing, transparency, and ethical food production is prompting greater demand for hybrid products that combine the nutritional density of animal proteins with the environmental advantages of plant proteins. Flexitarian dietary habits and increasing preference for natural, clean-label products are encouraging companies to refine hybrid formulations that offer improved flavor, texture, and functional benefits.

Major players in the Hybrid Plant-Animal Protein System Market include Cargill, ITC Limited, Maple Leaf Foods, Conagra Brands, JBS, Tyson Foods, Momentum Foods, Vion Food Group, Rugenwalder Muhle, 50/50 Foods, Inc., Nestle S.A., and Hormel Foods. Companies are strengthening their presence in the Hybrid Plant-Animal Protein System Market by expanding R&D initiatives, advancing processing technologies, and forming strategic alliances with ingredient suppliers and food manufacturers. Many firms are developing next-generation texturization and blending techniques to achieve improved taste, nutritional balance, and consistent product quality. Investments in consumer research help companies tailor hybrid offerings to meet regional dietary preferences and sustainability expectations. Manufacturers are also diversifying their product portfolios to include hybrid options across meat alternatives, ready meals, and snack categories.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product trends

- 2.2.2 Production process trends

- 2.2.3 Application trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global protein demand & food security concerns

- 3.2.1.2 Consumer shift toward flexitarian & reducetarian diets

- 3.2.1.3 Sustainability & climate change mitigation goals

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs & price premium challenges

- 3.2.2.2 Consumer skepticism & acceptance barriers

- 3.2.3 Market opportunities

- 3.2.3.1 B2B ingredient systems for food manufacturers

- 3.2.3.2 Cultivated meat-plant hybrid commercialization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Plant-animal hybrid products

- 5.3 Cultivated meat-plant hybrid products

- 5.4 Mycoprotein-animal hybrid products

- 5.5 Insect-plant hybrid products

- 5.6 Microbial fermentation-animal hybrid products

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Production Process, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Co-extrusion & texturization

- 6.3 Fermentation

- 6.4 Enzymatic modification

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Whole muscle analog hybrids

- 7.2.1 Steak & fillet analogs

- 7.2.2 Cutlet & chop formats

- 7.2.3 Others

- 7.3 Ground / minced hybrid products

- 7.3.1 Burger patties

- 7.3.2 Sausages & links

- 7.3.3 Meatballs & crumbles

- 7.3.4 Others

- 7.4 Processed hybrid products

- 7.4.1 Nuggets & tenders

- 7.4.2 Formed patties & cutlets

- 7.4.3 Strips & bites

- 7.4.4 Others

- 7.5 Ingredient hybrid systems

- 7.5.1 Protein isolates & concentrates

- 7.5.2 Texturized vegetable protein (TVP) blends

- 7.5.3 Functional protein ingredients

- 7.5.4 Others

- 7.6 Ready-to-eat hybrid meals

- 7.6.1 Frozen meal formats

- 7.6.2 Refrigerated prepared meals

- 7.6.3 Shelf-stable options

- 7.6.4 Meal kit

- 7.6.5 Others

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 50/50 Foods, Inc

- 9.2 Cargill

- 9.3 Conagra Brands

- 9.4 Hormel Foods

- 9.5 ITC Limited

- 9.6 JBS

- 9.7 Maple Leaf Foods

- 9.8 Momentum Foods

- 9.9 Nestle S.A.

- 9.10 Rugenwalder Muhle

- 9.11 Tyson Foods

- 9.12 Vion Food Group