|

市场调查报告书

商品编码

1892882

数位货运经纪市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)Digital Freight Brokerage Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

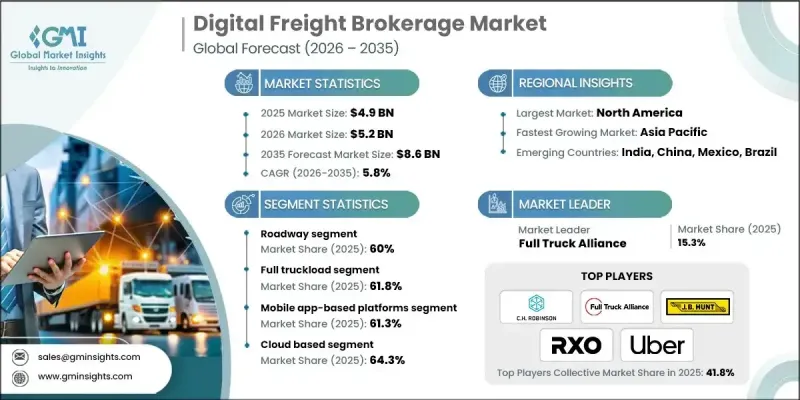

2025 年全球数位货运经纪市场价值 49 亿美元,预计到 2035 年将以 5.8% 的复合年增长率增长至 86 亿美元。

随着托运人越来越依赖自动化货运匹配系统和能够即时获取承运商运力资讯的数位工具,市场成长正在加速。成本效益仍然是主要驱动力,托运人纷纷转向线上平台以简化营运、减少人工流程并降低运输成本。数位经纪平台透过优化装载分配来帮助减少空驶里程,从而提高资产利用率、增加承运商收益并提升整体服务可靠性。国际货运数位化处理的成长以及对更严格合规监管的推动也促进了自动化分配技术的应用。同时,业界正迅速向人工智慧驱动的预测模型转型,以提高定价准确性和线路级绩效可视性。这些预测能力有助于稳定成本并提高服务效率,进一步提升了所有货运类别对数位经纪工具的需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 49亿美元 |

| 预测值 | 86亿美元 |

| 复合年增长率 | 5.8% |

到2025年,基于云端的货运解决方案将占据64.3%的市场份额,这主要得益于货运系统向云端快速转型。目前,相当一部分新型货运管理平台仰赖云端架构,而全球云端投资的持续成长也加速了物流运营的现代化进程。

到 2025 年,基于行动应用程式的平台市占率将达到 61.3%。智慧型手机的广泛普及和司机互动工具将继续推动使用,使用户能够即时存取货运资讯、文件和基于位置的匹配功能。

美国数位货运经纪市场占86.2%的市场份额,预计到2025年市场规模将达到17.6亿美元。强大的数位网路、高公路货运量以及不断增长的末端物流需求支援平台在整个地区的普及应用,都推动了这个市场的发展。独立卡车司机和小型车队越来越多地使用行动端货运通知和远端资讯处理技术来确保稳定的运力。

目录

第一章:方法论

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 电子商务货运量成长

- 向自动化经纪工作流程转变

- 扩展可见性和追踪工具

- 远端资讯处理和车队资料的整合

- 产业陷阱与挑战

- 分散的营运商生态系统

- 对资料隐私和平台依赖的担忧

- 市场机会

- 扩展综合多模式平台

- 采用基于人工智慧的定价和匹配

- 跨境数位走廊的发展

- 成长潜力分析

- 监管环境

- 北美洲

- FMCSA法规

- 加拿大交通局 (CTA) 指南

- 欧洲

- 欧盟运输法规

- 电子货运指令

- 一般资料保护规范(GDPR)

- 英国GDPR

- 数位式行车记录器规则

- 亚太地区

- 公路货运行政措施

- 网路安全法

- 关于提高物流效率的法案

- 2019年机动车辆法

- 运输业务法

- 智慧物流计划

- 拉丁美洲

- 国家陆路运输管理局(ANTT)规章

- 联邦道路运输法

- 美墨加协定规定

- 中东和非洲

- 阿联酋联邦交通法

- 沙乌地阿拉伯运输和物流法规

- 道路交通法

- 北美洲

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 成本細項分析

- 运输成本

- 技术和平台成本

- 营运成本

- 监理和合规成本

- 燃料和能源成本

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 定价分析

- 按地区

- 透过服务

- 用例

- 最佳情况

- 市场进入策略

- 针对特定区域的市场渗透策略

- 新进入者需要考虑的关键监管因素

- 定价、服务和差异化策略

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估算与预测:依运输方式划分,2022-2035年

- 道路

- 航道

- 气道

- 铁路

第六章:市场估算与预测:依服务类型划分,2022-2035年

- 整车运输 (FTL)

- 零担货运 (LTL)

- 多式联运

第七章:市场估计与预测:依平台划分,2022-2035年

- 基于行动应用的平台

- 网路为基础的平台

第八章:市场估算与预测:依部署模式划分,2022-2035年

- 基于云端的

- 本地部署

- 杂交种

第九章:市场估算与预测:依组织规模划分,2022-2035年

- 中小企业

- 大型企业

第十章:市场估计与预测:依应用领域划分,2022-2035年

- 货运管理

- 承运人和托运人匹配

- 价格竞价拍卖

- 即时追踪与分析

- 自动化文件

- 其他的

第十一章:市场估计与预测:依最终用途划分,2022-2035年

- 零售与电子商务

- 汽车

- 製造业

- 消费品

- 卫生保健

- 食品和饮料

- 其他的

第十二章:市场估算与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧

- 荷兰

- 瑞典

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 新加坡

- 泰国

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

- 土耳其

第十三章:公司简介

- 全球参与者

- CH Robinson

- Coyote Logistics

- Echo Global Logistics

- Hub Group

- JB Hunt

- Landstar System

- Total Quality Logistics

- Uber

- Worldwide Express

- XPO

- 区域玩家

- Allen Lund

- ArcBest

- BNSF Logistics

- England Logistics

- GlobalTranz Enterprises

- MATSON Logistics

- Schneider

- Transplace

- Werner Enterprises

- 新兴参与者/颠覆者

- Armstrong Transport Group

- Ascent Global Logistics

- Expeditors International

- NTG Freight

- Trinity Logistics

The Global Digital Freight Brokerage Market was valued at USD 4.9 billion in 2025 and is estimated to grow at a CAGR of 5.8% to reach USD 8.6 billion by 2035.

Market growth is accelerating as shippers increasingly rely on automated freight-matching systems and digital tools that provide real-time access to carrier capacity. Cost efficiency remains a major motivation, with shippers turning to online platforms to streamline operations, minimize manual processes, and lower transportation expenses. Digital brokerage platforms help reduce empty miles by optimizing load assignments, which enhances asset utilization, raises carrier earnings, and improves overall service dependability. The rise in international shipments processed digitally and the push for stronger compliance oversight have also reinforced the adoption of automated allocation technologies. At the same time, the industry is moving rapidly toward AI-driven forecasting models that improve pricing accuracy and lane-level performance visibility. These predictive capabilities help stabilize costs while strengthening service efficiency, further boosting the demand for digital brokerage tools across all freight categories.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.9 Billion |

| Forecast Value | $8.6 Billion |

| CAGR | 5.8% |

The cloud-based category accounted for a 64.3% share in 2025, strengthened by the rapid shift toward cloud-enabled freight systems. A significant portion of new freight management platforms now depend on cloud architecture, supported by global cloud investments that are accelerating the modernization of logistics operations.

The mobile app-based platforms segment held a 61.3% share in 2025. Widespread smartphone adoption and driver engagement tools continue to drive usage, allowing instant access to load postings, documents, and location-based matching capabilities.

U.S. Digital Freight Brokerage Market held 86.2% share and generated USD 1.76 billion in 2025. Strong digital networks, high road freight volumes, and expanding last-mile demand support platform adoption throughout the region. Independent truckers and smaller fleets are increasingly using mobile-enabled load notifications and telematics connectivity to secure consistent capacity.

Key companies in the Global Digital Freight Brokerage Market include C.H. Robinson, Coyote Logistics, Echo Global Logistics, Full Truck Alliance, J.B. Hunt, Landstar System, RXO, Total Quality Logistics (TQL), Uber, and XPO. Market leaders are strengthening their competitive positions by investing in AI-based matching engines, predictive analytics, and automated pricing tools that enhance operational accuracy and provide faster load-to-carrier pairing. Companies are expanding cloud-native platforms to improve scalability and reliability for shippers and carriers. Many are integrating telematics data, real-time tracking, and digital documentation to create seamless end-to-end workflows. Strategic partnerships with carriers, logistics service providers, and supply chain software companies also help expand network density and load availability. Businesses are focusing on mobile-first solutions to support driver engagement and speed up transactions. Continuous enhancements in compliance automation, platform security, and user experience further support market differentiation and long-term customer retention.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Transportation Mode

- 2.2.3 Service

- 2.2.4 Platform

- 2.2.5 Deployment Model

- 2.2.6 Organization Size

- 2.2.7 Application

- 2.2.8 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 Growth in E-commerce freight volumes

- 3.2.1.3 Shift toward automated brokerage workflows

- 3.2.1.4 Expansion of visibility and tracking tools

- 3.2.1.5 Integration of telematics and fleet data

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Fragmented carrier ecosystem

- 3.2.2.2 Concerns about data privacy and platform dependence

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of integrated multimodal platforms

- 3.2.3.2 Adoption of AI based pricing and matching

- 3.2.3.3 Growth of cross border digital corridors

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 FMCSA Regulations

- 3.4.1.2 Canadian Transportation Agency (CTA) Guidelines

- 3.4.2 Europe

- 3.4.2.1 EU transport regulations

- 3.4.2.2 E-freight directive

- 3.4.2.3 General data protection regulation (GDPR)

- 3.4.2.4 UK GDPR

- 3.4.2.5 Digital tachograph rules

- 3.4.3 Asia Pacific

- 3.4.3.1 Administrative measures for road freight

- 3.4.3.2 Cybersecurity law

- 3.4.3.3 Act on Improvement of Logistics Efficiency

- 3.4.3.4 Motor Vehicles Act 2019

- 3.4.3.5 Transport Business Act

- 3.4.3.6 Smart Logistics Initiative

- 3.4.4 Latin America

- 3.4.4.1 National land transport agency (ANTT) regulations

- 3.4.4.2 Federal road transportation law

- 3.4.4.3 Usmca regulations

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE federal transport law

- 3.4.5.2 Saudi transport and logistics regulations

- 3.4.5.3 Road traffic act

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.8.1 Transportation costs

- 3.8.2 Technology & platform costs

- 3.8.3 Operational costs

- 3.8.4 Regulatory & compliance costs

- 3.8.5 Fuel and energy costs

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly Initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Pricing analysis

- 3.11.1 By region

- 3.11.2 By service

- 3.12 Use cases

- 3.13 Best case scenarios

- 3.14 Go-to-Market strategies

- 3.14.1 Region-specific market penetration strategies

- 3.14.2 Key regulatory considerations for new entrants

- 3.14.3 Pricing, service, and differentiation strategies

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Transportation Mode, 2022- 2035 (USD Mn)

- 5.1 Key trends

- 5.2 Roadway

- 5.3 Seaway

- 5.4 Airway

- 5.5 Railway

Chapter 6 Market Estimates & Forecast, By Service, 2022 - 2035 (USD Mn)

- 6.1 Key trends

- 6.2 Full Truckload (FTL)

- 6.3 Less than Truckload (LTL)

- 6.4 Intermodal

Chapter 7 Market Estimates & Forecast, By Platform, 2022 - 2035 (USD Mn)

- 7.1 Key trends

- 7.2 Mobile app-based platforms

- 7.3 Web-based platforms

Chapter 8 Market Estimates & Forecast, By Deployment Model, 2022 - 2035 (USD Mn)

- 8.1 Key trends

- 8.2 Cloud-Based

- 8.3 On-Premises

- 8.4 Hybrid

Chapter 9 Market Estimates & Forecast, By Organization Size, 2022 - 2035 (USD Mn)

- 9.1 Key trends

- 9.2 Small & Medium Enterprises (SMEs)

- 9.3 Large Enterprises

Chapter 10 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Mn)

- 10.1 Key trends

- 10.2 Freight management

- 10.3 Carrier & shipper matching

- 10.4 Price bidding & auction

- 10.5 Real-time tracking & analytics

- 10.6 Automated documentation

- 10.7 Others

Chapter 11 Market Estimates & Forecast, By End Use, 2022 - 2035 (USD Mn)

- 11.1 Key trends

- 11.2 Retail & e-commerce

- 11.3 Automotive

- 11.4 Manufacturing

- 11.5 Consumer goods

- 11.6 Healthcare

- 11.7 Food & beverages

- 11.8 Others

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Mn)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 US

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.3.7 Nordics

- 12.3.8 Netherlands

- 12.3.9 Sweden

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.4.6 Singapore

- 12.4.7 Thailand

- 12.4.8 Indonesia

- 12.4.9 Vietnam

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

- 12.6.4 Turkey

Chapter 13 Company Profiles

- 13.1 Global Players

- 13.1.1 C.H. Robinson

- 13.1.2 Coyote Logistics

- 13.1.3 Echo Global Logistics

- 13.1.4 Hub Group

- 13.1.5 J.B. Hunt

- 13.1.6 Landstar System

- 13.1.7 Total Quality Logistics

- 13.1.8 Uber

- 13.1.9 Worldwide Express

- 13.1.10 XPO

- 13.2 Regional Players

- 13.2.1 Allen Lund

- 13.2.2 ArcBest

- 13.2.3 BNSF Logistics

- 13.2.4 England Logistics

- 13.2.5 GlobalTranz Enterprises

- 13.2.6 MATSON Logistics

- 13.2.7 Schneider

- 13.2.8 Transplace

- 13.2.9 Werner Enterprises

- 13.3 Emerging Players / Disruptors

- 13.3.1 Armstrong Transport Group

- 13.3.2 Ascent Global Logistics

- 13.3.3 Expeditors International

- 13.3.4 NTG Freight

- 13.3.5 Trinity Logistics

货运代理服务市场:依服务类型、运输方式、客户规模、货物类型、技术应用及最终用户产业划分-2026-2032年全球市场预测

货运代理服务市场:依服务类型、运输方式、客户规模、货物类型、技术应用及最终用户产业划分-2026-2032年全球市场预测 美国整车货运经纪市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)

美国整车货运经纪市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年) 全球货运仲介市场规模、份额、趋势和成长分析报告(2026-2034)

全球货运仲介市场规模、份额、趋势和成长分析报告(2026-2034) 2026-2030年全球货运仲介市场

2026-2030年全球货运仲介市场 2026-2030年全球数位货运经纪市场

2026-2030年全球数位货运经纪市场 2032 年数位货运经纪市场预测:按平台类型、运输方式、服务类型、部署模式、最终用户和地区进行的全球分析

2032 年数位货运经纪市场预测:按平台类型、运输方式、服务类型、部署模式、最终用户和地区进行的全球分析 2025年数位货运经纪全球市场报告美国货运经纪:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)全球数位货运经纪市场-以运输方式、垂直产业、区域范围、预测分類的市场规模

2025年数位货运经纪全球市场报告美国货运经纪:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)全球数位货运经纪市场-以运输方式、垂直产业、区域范围、预测分類的市场规模 全球数位货运经纪市场规模、份额、趋势分析报告(依客户类型、运输方式、服务类型、最终用户产业、地区、展望与预测,2025 年至 2032 年)

全球数位货运经纪市场规模、份额、趋势分析报告(依客户类型、运输方式、服务类型、最终用户产业、地区、展望与预测,2025 年至 2032 年)