|

市场调查报告书

商品编码

1913354

车载支付服务市场机会、成长要素、产业趋势分析及2026年至2035年预测In-Vehicle Payment Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球车载支付服务市场预计到 2025 年将达到 16.4 亿美元,到 2035 年将达到 173 亿美元,年复合成长率为 26.9%。

市场发展势头强劲,这主要得益于人们对出行相关活动中无缝、非接触式数位交易日益增长的偏好,促使汽车製造商和出行服务供应商将安全支付功能直接嵌入车辆。联网汽车平台凭藉先进的资讯娱乐和远端资讯处理架构的快速发展,为整合支付功能和即时交易处理奠定了坚实的基础。消费者对数位钱包和无现金支付解决方案的日益依赖,进一步加速了车辆系统与更广泛的金融生态系统之间的兼容性。汽车製造商正积极与金融机构、支付处理商和科技公司合作,以简化开发週期、满足监管要求,并从互联服务中挖掘新的商机。同时,物联网、人工智慧和高速连接等先进技术的集成,正在增强车辆、支付基础设施和服务平台之间的通信,从而提高车载商务解决方案的可扩展性和可靠性。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 16.4亿美元 |

| 预测金额 | 173亿美元 |

| 复合年增长率 | 26.9% |

到 2025 年,近距离场通讯 (NFC) 支付领域将占 45% 的份额,预计到 2035 年将达到 87 亿美元。非接触式支付方式的广泛采用以及与车辆硬体生态系统日益增强的整合正在推动这一领域的发展。

预计到 2025 年,嵌入式远端资讯处理解决方案将占 52% 的市场份额,并创造 8.529 亿美元的收入。这些解决方案的价值在于能够实现安全的本地支付功能,同时还能增强资料所有权、提高系统可靠性和实现长期业务收益。

美国车载支付服务市场预计到 2025 年将达到 6.531 亿美元,并预计到 2035 年将保持强劲成长。市场扩张的驱动力是联网汽车的普及和对便利数位支付体验的强烈需求。

目录

第一章调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率分析

- 成本结构

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 非接触式支付需求不断成长

- 联网汽车渗透率成长

- 扩展数位钱包生态系统

- OEM厂商与金融科技伙伴关係

- 扩大电动车的使用范围并改善充电基础设施

- 产业潜在风险与挑战

- 网路安全和资料隐私问题

- 高昂的系统整合和合规成本

- 市场机会

- 扩大电动车充电支付集成

- 车队和商用车支付自动化发展

- 开发个人化的车用商务服务

- 推出生物识别和语音支付认证

- 成长潜力分析

- 监管环境

- 北美洲

- 美国:车载支付处理安全标准 (PCI DSS)

- 加拿大:《个人资讯保护和电子文件法》(PIPEDA) 规范支付和使用者资料保护。

- 欧洲

- 英国:车上数位支付符合英国GDPR和PCI DSS标准

- 德国:嵌入式支付系统的GDPR和ISO/IEC 27001资讯安全控制

- 法国:PSD2(支付服务指令),旨在保障安全的电子支付和车载支付。

- 义大利:数位和嵌入式付款管道的PSD2和GDPR合规框架

- 西班牙:车载支付资料安全方面的 GDPR 和 PCI DSS 要求

- 亚太地区

- 中国:《个人资讯保护法》规范联网汽车与车载支付数据

- 日本:《汽车支付资料安全个人资讯保护法》(APPI)

- 印度:适用于车载支付服务的印度储备银行数位支付安全指南

- 拉丁美洲

- 巴西:车载和联网支付系统中的通用资料保护法 (LGPD)

- 墨西哥:《个人资料保护法》(LFPDPPP),该法规范汽车数位支付

- 阿根廷:与车载付款管道相关的个人资料保护法(第25326号法律)

- 中东和非洲

- 阿拉伯联合大公国:阿联酋资料保护条例和嵌入式支付服务支付卡产业资料安全标准 (PCI DSS)

- 南非:《个人资讯保护法》(POPIA) 对联网汽车支付资料的影响

- 沙乌地阿拉伯:沙乌地阿拉伯资料与人工智慧管理局 (SDAIA) 车载支付系统资料保护条例

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 成本細項分析

- 开发成本结构

- 研发成本分析

- 行销和销售成本

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 未来市场展望与机会

- OEM货币化与经营模式分析

- 直接交易收入模式(收入分成,基于商家折扣率)

- 基于订阅的车载商务模式

- 平台和生态系统货币化(应用商店、市场)

- 数据驱动的获利机会(使用、行为分析)

- OEM vs. 金融科技 vs. 支付网路 所得所有权

- OEM整合与实施框架

- 生态系动态与策略控制点

第四章 竞争情势

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 企业扩张计画和资金筹措

第五章 依支付方式分類的市场估算与预测,2022-2035年

- 近距离场通讯 (NFC) 支付

- 基于QR码的支付

- 嵌入式钱包

- 其他的

第六章 按技术分類的市场估计与预测,2022-2035年

- 嵌入式车载资讯服务解决方案

- 基于行动应用程式的集成

- 基于云端的付款管道

第七章 依车辆类型分類的市场估计与预测,2022-2035年

- 搭乘用车

- SUV

- 轿车

- 掀背车

- 商用车辆

- 轻型商用车(LCV)

- MCV

- 重型商用车(HCV)

第八章 按应用领域分類的市场估算与预测,2022-2035年

- 加油/电动车充电

- 智慧停车

- 电子收费系统

- 电子商务

- 其他的

第九章 2022-2035年各地区市场估算与预测

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧国家

- 葡萄牙

- 克罗埃西亚

- 比荷卢经济联盟

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 新加坡

- 泰国

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥伦比亚

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

第十章:公司简介

- 世界玩家

- Amazon Web Services

- Ford Motor Company

- Hyundai Motor Company

- IBM

- Mastercard

- PayPal

- Shell

- Visa

- Volkswagen

- BMW

- Jaguar Land Rover Automotive

- ParkMobile

- ZF

- 区域玩家

- General Motors Company

- Honda Motor

- Daimler/Mercedes-Benz

- Toyota Motor

- Telenav

- Parkopedia

- CarPay Diem/Kwalyo

- SiriusXM Connected Vehicle

- Gentex

- Thales

- Emerging/Disruptor Players

- Car IQ Pay

- Cerence

- PayByCar

- Verra Mobility

- Apple

- Samsung Electronics

- Parkwhiz

- Xevo

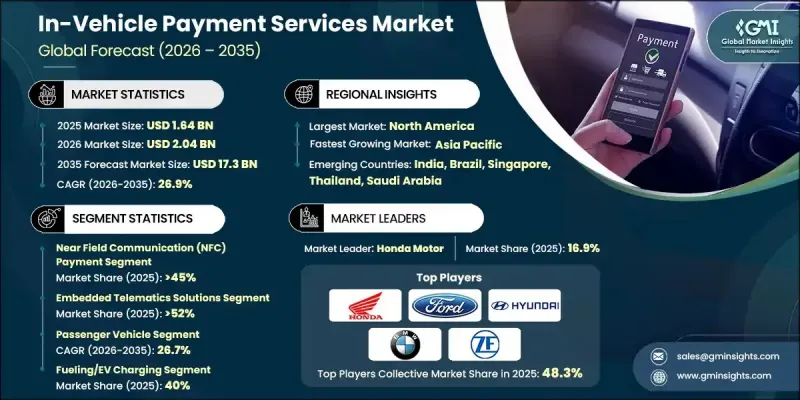

The Global In-Vehicle Payment Services Market was valued at USD 1.64 billion in 2025 and is estimated to grow at a CAGR of 26.9% to reach USD 17.3 billion by 2035.

Market momentum is driven by the growing preference for seamless and contactless digital transactions across mobility-related activities, encouraging automakers and mobility service providers to embed secure payment functionality directly into vehicles. The rapid expansion of connected vehicle platforms equipped with sophisticated infotainment and telematics architectures is creating a robust base for integrated payment capabilities and real-time transaction processing. Increasing consumer reliance on digital wallets and cashless payment solutions is further accelerating compatibility between vehicle systems and broader financial ecosystems. Automakers are actively partnering with financial institutions, payment processors, and technology firms to streamline development cycles, address regulatory requirements, and unlock new revenue opportunities from connected services. In parallel, the integration of advanced technologies such as IoT, AI, and high-speed connectivity is enhancing communication between vehicles, payment infrastructure, and service platforms, reinforcing the scalability and reliability of in-vehicle commerce solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.64 Billion |

| Forecast Value | $17.3 Billion |

| CAGR | 26.9% |

In 2025, the near field communication payment segment held 45% share and is forecast to reach USD 8.7 billion by 2035. Adoption is supported by widespread acceptance of contactless payment methods and increasing integration within vehicle hardware ecosystems.

The embedded telematics solutions segment held 52% share in 2025 and generated USD 852.9 million. These solutions are favored for enabling secure, native payment functionality while improving data ownership, system reliability, and long-term service monetization.

U.S. In-Vehicle Payment Services Market reached USD 653.1 million in 2025 and is expected to record strong growth through 2035. Market expansion is supported by high penetration of connected vehicles and strong demand for convenience-oriented digital payment experiences.

Key companies operating in the Global In-Vehicle Payment Services Market include Volkswagen, PayPal, BMW, ZF, Ford Motor Company, Shell, Hyundai Motor, Jaguar Land Rover Automotive, Honda Motor, and ParkMobile. Companies in the In-Vehicle Payment Services Market are focusing on strategic partnerships to strengthen ecosystem integration and accelerate solution deployment. Collaboration with financial institutions, fintech providers, and mobility service platforms allows players to ensure regulatory compliance while expanding transaction coverage. Many firms are investing in cybersecurity, tokenization, and data encryption to enhance trust and protect user information. Continuous software innovation and over-the-air update capabilities are being leveraged to improve functionality and scalability. Market participants are also prioritizing user-centric interface design to improve adoption and engagement.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Payment mode

- 2.2.3 Technology

- 2.2.4 Vehicle

- 2.2.5 Application

- 2.3 TAM Analysis, 2026-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook & strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 Rising demand for contactless payments

- 3.2.1.3 Growth of connected vehicle penetration

- 3.2.1.4 Expansion of digital wallet ecosystems

- 3.2.1.5 OEM-fintech partnerships

- 3.2.1.6 Increase in EV adoption and charging infrastructures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Cybersecurity and data privacy concerns

- 3.2.2.2 High system integration and compliance costs

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of EV charging payment integration

- 3.2.3.2 Growth of fleet and commercial vehicle payment automation

- 3.2.3.3 Development of personalized in-car commerce services

- 3.2.3.4 Adoption of biometric and voice-enabled payment authentication

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 United States: PCI DSS (Payment Card Industry Data Security Standard) for secure in-vehicle payment processing

- 3.4.1.2 Canada: PIPEDA (Personal Information Protection and Electronic Documents Act) governing payment and user data protection

- 3.4.2 Europe

- 3.4.2.1 United Kingdom: UK GDPR and PCI DSS compliance for in-vehicle digital payments

- 3.4.2.2 Germany: GDPR and ISO/IEC 27001 information security management for embedded payment systems

- 3.4.2.3 France: PSD2 (Revised Payment Services Directive) for secure electronic and in-vehicle payments

- 3.4.2.4 Italy: PSD2 and GDPR compliance framework for digital and embedded payment platforms

- 3.4.2.5 Spain: GDPR and PCI DSS requirements for in-vehicle payment data security

- 3.4.3 Asia Pacific

- 3.4.3.1 China: PIPL (Personal Information Protection Law) regulating connected vehicle and in-vehicle payment data

- 3.4.3.2 Japan: APPI (Act on the Protection of Personal Information) for automotive payment data security

- 3.4.3.3 India: RBI digital payment security guidelines applicable to in-vehicle payment services

- 3.4.4 Latin America

- 3.4.4.1 Brazil: LGPD (Lei Geral de Protecao de Dados) for in-vehicle and connected payment systems

- 3.4.4.2 Mexico: Federal Law on Protection of Personal Data (LFPDPPP) governing automotive digital payments

- 3.4.4.3 Argentina: Personal Data Protection Law (Law No. 25,326) relevant to in-vehicle payment platforms

- 3.4.5 Middle East & Africa

- 3.4.5.1 United Arab Emirates: UAE data protection regulations and PCI DSS for embedded payment services

- 3.4.5.2 South Africa: POPIA (Protection of Personal Information Act) for connected vehicle payment data

- 3.4.5.3 Saudi Arabia: Saudi Data and AI Authority (SDAIA) data protection regulations for in-vehicle payment systems

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.8.1 Development cost structure

- 3.8.2 R&D cost analysis

- 3.8.3 Marketing & sales costs

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly Initiatives

- 3.11 Future market outlook & opportunities

- 3.12 OEM Monetization & Business Model Analysis

- 3.12.1 Direct transaction revenue models (revenue share, MDR-based)

- 3.12.2 Subscription-based in-vehicle commerce models

- 3.12.3 Platform and ecosystem monetization (app stores, marketplaces)

- 3.12.4 Data-driven monetization opportunities (usage, behavioral insights)

- 3.12.5 OEM vs fintech vs payment network revenue ownership

- 3.13 OEM Integration & Deployment Framework

- 3.14 Ecosystem Power Dynamics & Strategic Control Points

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Payment mode, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Near Field Communication (NFC) Payments

- 5.3 QR Code-Based Payments

- 5.4 Embedded Wallets

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Embedded Telematics Solutions

- 6.3 Mobile Application-Based Integration

- 6.4 Cloud-Based Payment Platforms

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Passenger vehicle

- 7.2.1 SUV

- 7.2.2 Sedan

- 7.2.3 Hatchback

- 7.3 Commercial vehicle

- 7.3.1 LCV

- 7.3.2 MCV

- 7.3.3 HCV

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Fueling/EV Charging

- 8.3 Smart Parking

- 8.4 Automated Toll Payments

- 8.5 E-commerce

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.3.8 Portugal

- 9.3.9 Croatia

- 9.3.10 Benelux

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Singapore

- 9.4.7 Thailand

- 9.4.8 Indonesia

- 9.4.9 Vietnam

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Colombia

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Turkey

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Amazon Web Services

- 10.1.2 Ford Motor Company

- 10.1.3 Hyundai Motor Company

- 10.1.4 IBM

- 10.1.5 Mastercard

- 10.1.6 PayPal

- 10.1.7 Shell

- 10.1.8 Visa

- 10.1.9 Volkswagen

- 10.1.10 BMW

- 10.1.11 Jaguar Land Rover Automotive

- 10.1.12 ParkMobile

- 10.1.13 ZF

- 10.2 Regional Players

- 10.2.1 General Motors Company

- 10.2.2 Honda Motor

- 10.2.3 Daimler / Mercedes-Benz

- 10.2.4 Toyota Motor

- 10.2.5 Telenav

- 10.2.6 Parkopedia

- 10.2.7 CarPay Diem / Kwalyo

- 10.2.8 SiriusXM Connected Vehicle

- 10.2.9 Gentex

- 10.2.10 Thales

- 10.3 Emerging / Disruptor Players

- 10.3.1 Car IQ Pay

- 10.3.2 Cerence

- 10.3.3 PayByCar

- 10.3.4 Verra Mobility

- 10.3.5 Apple

- 10.3.6 Samsung Electronics

- 10.3.7 Parkwhiz

- 10.3.8 Xevo

车载支付服务市场:支付方式、连结性、交易类型、应用与车辆类型-2026-2032年全球市场预测

车载支付服务市场:支付方式、连结性、交易类型、应用与车辆类型-2026-2032年全球市场预测 车载支付市场分析及预测(至2035年):依类型、产品、服务、技术、组件、应用、设备、部署类型、最终用户及解决方案划分

车载支付市场分析及预测(至2035年):依类型、产品、服务、技术、组件、应用、设备、部署类型、最终用户及解决方案划分 全球车载支付服务市场规模、份额、趋势和成长分析报告(2026-2034)

全球车载支付服务市场规模、份额、趋势和成长分析报告(2026-2034) 2032年车载支付服务市场预测:按支付方式、车辆类型、应用和地区进行的全球分析

2032年车载支付服务市场预测:按支付方式、车辆类型、应用和地区进行的全球分析 2025年全球车用支付服务市场报告

2025年全球车用支付服务市场报告 全球车用支付服务市场

全球车用支付服务市场 车载付款服务市场:按付款方式、应用程式和地区划分

车载付款服务市场:按付款方式、应用程式和地区划分 车载付款服务市场规模、份额及成长分析(按付款方式、应用和地区)- 产业预测 2025-2032

车载付款服务市场规模、份额及成长分析(按付款方式、应用和地区)- 产业预测 2025-2032 车内付款·ETC的中国市场(2024年)到 2030 年车载付款系统市场预测:按付款类型、车辆类型、技术、应用、最终用户和地区进行全球分析

车内付款·ETC的中国市场(2024年)到 2030 年车载付款系统市场预测:按付款类型、车辆类型、技术、应用、最终用户和地区进行全球分析