|

市场调查报告书

商品编码

1913481

婴儿背带及配件市场机会、成长驱动因素、产业趋势分析及预测(2026-2035)Baby and Toddlers Carriers and Accessories Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

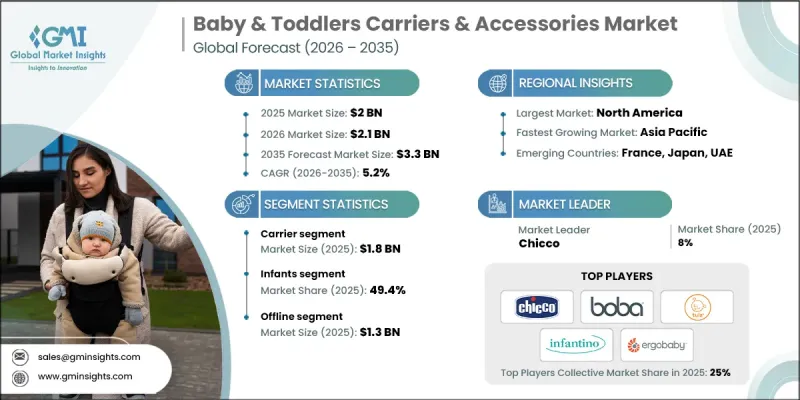

全球婴儿背带及配件市场预计到 2025 年将达到 20 亿美元,到 2035 年将达到 33 亿美元,年复合成长率为 5.2%。

市场成长正受到家庭结构变化的影响,尤其是双薪家庭的增加和持续的都市化。现代父母越来越倾向于选择能够支持积极生活方式、兼顾工作、个人生活和育儿的产品。婴儿背带提供了一个实用的解决方案,既能解放双手,又能与孩子保持亲密的身体连结。在人口密集的都市区,由于背带在拥挤的道路、公共交通工具和狭小的生活空间中更易于使用,因此往往比传统婴儿车更受欢迎。对便携性和效率的关注正在推动产品创新,各大品牌都在设计兼具舒适性、安全性和美观性的背带。现代父母期望产品既能体现现代美学和功能性,又能无缝融入他们的日常生活,这促使製造商不断扩展其多功能、符合人体工学且外观时尚的背带产品线。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始金额 | 20亿美元 |

| 预测金额 | 33亿美元 |

| 复合年增长率 | 5.2% |

预计到2025年,婴儿背带市场规模将达18亿美元。这些产品专为照顾者设计,让他们能够安全地抱起婴幼儿,同时解放双手。婴儿背带款式多样,可满足不同发展阶段、舒适度需求及抱姿偏好。父母依靠婴儿背带增进亲子关係,确保照顾者和孩子都能保持正确的姿势,并在日常活动中保持舒适。

预计到2025年,婴儿用品市占率将达到49.4%。婴儿期,尤其是5个月至2岁这段时期,是身体和认知快速发展的阶段。随着婴儿逐渐能够控制头部、颈部和身体躯干,照顾者会逐渐过渡到使用结构更稳固的背带,这些背带既能提供支撑,又能让孩子观察周围环境并与之互动。在这个尚未学会走路的阶段,背带在维繫照顾者与孩子之间的亲密关係方面发挥着重要作用,同时也能支持孩子日益增长的好奇心以及与环境的感官互动。

预计2025年,美国婴儿背带及配件市场规模将达5亿美元,占78.6%的市占率。高购买力、对安全性和人体工学标准的重视以及以儿童为中心的消费文化,是推动市场持续成长的主要因素。美国父母尤其偏好兼具舒适性、设计感、多功能性和符合健康指南的婴儿背带。实体店和线上平台的广泛产品供应进一步促进了市场成长,并丰富了消费者的选择。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 产业影响因素

- 成长驱动因素

- 越来越多的职业父母和城市生活方式的普及

- 父母对背巾使用婴儿的好处的看法

- 注重人体工学与舒适性

- 产业潜在风险与挑战

- 安全和合规问题

- 品管和仿冒品措施

- 机会

- 配件创新

- 技术整合产品

- 成长驱动因素

- 成长潜力分析

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 依产品类型

- 监管环境

- 标准和合规要求

- 区域法规结构

- 认证标准

- 波特分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 依产品类型分類的市场估算与预测(2022-2035 年)

- 职业

- 软结构类型

- 包装搬运工

- 斜背包

- 背包式背带

- 其他(美泰航空等)

- 配件

- 食物

- 靠背

- 口水垫

- 肩带保护套

- 其他(收纳袋等)

第六章 市场估算与预测:依材料分类(2022-2035 年)

- 棉布

- 尼龙

- 亚麻布

- 聚酯纤维

- 其他(人造毛皮、氯丁橡胶等)

第七章 市场估计与预测:依年龄层划分(2022-2035 年)

- 新生儿(0-5个月)

- 婴儿(5个月至2岁)

- 幼儿(2-4岁)

第八章 市场估算与预测:依持有类型划分(2022-2035 年)

- 积极的

- 向后

- 时髦的

第九章 市场估计与预测:依价格划分(2022-2035 年)

- 低价位

- 中价位

- 高价位范围

第十章 按分销管道分類的市场估计和预测(2022-2035 年)

- 在线的

- 电子商务

- 公司网站

- 离线

- 超级市场/大卖场

- 专卖店

- 其他(个别门市等)

第十一章 各地区市场估计与预测(2022-2035 年)

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十二章:公司简介

- Baby K'tan

- Baby Tula

- Be Lenka

- Boba

- Chicco

- Ergobaby

- Fidella

- Infantino

- Kinderkraft

- Kol Kol Baby Carrier

- LennyLamb

- Mabe

- MaMidea

- Tushbaby

- Wildbird

The Global Baby & Toddlers Carriers & Accessories Market was valued at USD 2 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 3.3 billion by 2035.

Market growth is shaped by changing family dynamics, particularly the rise in dual-income households and continued urbanization. Modern parents increasingly seek products that support active lifestyles while allowing them to manage childcare alongside professional and personal responsibilities. Baby carriers offer a practical solution by enabling hands-free mobility while maintaining close physical connection with children. In dense urban environments, carriers are often favored over traditional strollers due to their ease of use on crowded streets, public transport systems, and in compact living spaces. The emphasis on portability and efficiency has influenced product innovation, leading brands to design carriers that balance comfort, safety, and visual appeal. Today's parents expect products that integrate seamlessly into daily routines while reflecting modern aesthetics and functionality, which has encouraged manufacturers to expand their portfolios with versatile, ergonomic, and visually refined carrier solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2 Billion |

| Forecast Value | $3.3 Billion |

| CAGR | 5.2% |

The carriers segment reached USD 1.8 billion in 2025. These products are designed to be worn by caregivers, allowing infants and toddlers to be carried securely while keeping hands free. Available in a variety of designs, carriers support different developmental stages, comfort needs, and carrying preferences. Parents rely on them to promote closeness, support proper posture for both caregiver and child, and maintain comfort during everyday activities.

The infant category accounted for 49.4% share in 2025. Early childhood is marked by rapid physical and cognitive development, particularly between five months and two years of age. As infants gain better head, neck, and core control, caregivers increasingly transition to structured carriers that provide support while allowing children to observe and engage with their surroundings. During this pre-mobility phase, carriers play a key role in maintaining caregiver bonding while supporting a child's growing curiosity and sensory interaction with the environment.

United States Baby & Toddlers Carriers & Accessories Market held 78.6% share, generating USD 500 million in 2025. Strong purchasing power, high awareness of safety and ergonomic standards, and a well-established culture of child-focused consumer spending support sustained demand. Parents in the U.S. show strong preference for carriers that combine comfort, design appeal, versatility, and compliance with health guidelines. Broad product availability through both physical retail channels and online platforms further strengthens market growth and consumer choice.

Key companies active in the Global Baby & Toddlers Carriers & Accessories Market include Ergobaby, Baby K'tan, Infantino, Chicco, Boba, Tushbaby, LennyLamb, Baby Tula, Kinderkraft, Wildbird, Fidella, Be Lenka, Kol Kol Baby Carrier, MaMidea, and Mabe. Companies in the Global Baby & Toddlers Carriers & Accessories Market are reinforcing their market position through continuous product innovation, brand differentiation, and expanded distribution strategies. Many players focus on ergonomic research to improve comfort and safety for both caregivers and children. Design-led development that blends functionality with modern styling is being used to attract fashion-conscious parents. Brands are also strengthening digital presence through direct-to-consumer platforms and targeted marketing campaigns. Strategic partnerships with retailers and parenting communities help expand reach and build trust.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Material

- 2.2.4 Age

- 2.2.5 Carry positions

- 2.2.6 Price

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in working parents & urban lifestyles

- 3.2.1.2 Parental awareness of babywearing benefits

- 3.2.1.3 Focus on ergonomics & comfort

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Safety and compliance concerns

- 3.2.2.2 Quality control and counterfeit products

- 3.2.3 Opportunities

- 3.2.3.1 Accessory innovation

- 3.2.3.2 Tech-integrated products

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Carrier

- 5.2.1 Soft structured

- 5.2.2 Wrap carriers

- 5.2.3 Sling carriers

- 5.2.4 Backpack carriers

- 5.2.5 Others (Mei-tai carriers etc.)

- 5.3 Accessories

- 5.3.1 Hood

- 5.3.2 Back support

- 5.3.3 Drool pads

- 5.3.4 Shoulder strap protectors

- 5.3.5 Others (storage pouch etc.)

Chapter 6 Market Estimates and Forecast, By Material, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 Cotton

- 6.3 Nylon

- 6.4 Linen

- 6.5 Polyester

- 6.6 Others (faux fur, neoprene etc.)

Chapter 7 Market Estimates and Forecast, By Age, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 Newborns (0m-5m)

- 7.3 Infants (5m-2y)

- 7.4 Toddler (2y-4y)

Chapter 8 Market Estimates and Forecast, By Carry Positions, 2022 - 2035 (USD Billion)

- 8.1 Key trends

- 8.2 Front facing

- 8.3 Back facing

- 8.4 Hip

Chapter 9 Market Estimates and Forecast, By Price, 2022 - 2035 (USD Billion)

- 9.1 Key trends

- 9.2 Low

- 9.3 Medium

- 9.4 High

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion)

- 10.1 Key trends

- 10.2 Online

- 10.2.1 E-commerce

- 10.2.2 Company owned website

- 10.3 Offline

- 10.3.1 Supermarket/hypermarket

- 10.3.2 Specialty stores

- 10.3.3 Others (individual stores, etc.)

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Baby K'tan

- 12.2 Baby Tula

- 12.3 Be Lenka

- 12.4 Boba

- 12.5 Chicco

- 12.6 Ergobaby

- 12.7 Fidella

- 12.8 Infantino

- 12.9 Kinderkraft

- 12.10 Kol Kol Baby Carrier

- 12.11 LennyLamb

- 12.12 Mabe

- 12.13 MaMidea

- 12.14 Tushbaby

- 12.15 Wildbird

婴儿背带市场报告:趋势、预测和竞争分析(至2035年)

婴儿背带市场报告:趋势、预测和竞争分析(至2035年) 婴儿背带市场:依背带类型、销售管道、年龄层及材质划分-2026-2032年全球市场预测

婴儿背带市场:依背带类型、销售管道、年龄层及材质划分-2026-2032年全球市场预测 婴儿背带市场商机、成长要素、产业趋势分析及2026-2035年预测。

婴儿背带市场商机、成长要素、产业趋势分析及2026-2035年预测。 2026-2030年全球婴儿背带市场

2026-2030年全球婴儿背带市场 婴儿背带市场规模、份额和趋势:按产品类型、分销管道和地区划分,并预测至2026-2034年

婴儿背带市场规模、份额和趋势:按产品类型、分销管道和地区划分,并预测至2026-2034年 婴儿背带市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测

婴儿背带市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测 婴儿背带市场 - 全球产业规模、份额、趋势、机会及预测(按类型、价格范围、分销管道、地区和竞争格局划分,2021-2031年)婴幼儿枕头市场:依产品类型、材质类型、尺寸、最终用户和通路划分,全球预测(2026-2032年)

婴儿背带市场 - 全球产业规模、份额、趋势、机会及预测(按类型、价格范围、分销管道、地区和竞争格局划分,2021-2031年)婴幼儿枕头市场:依产品类型、材质类型、尺寸、最终用户和通路划分,全球预测(2026-2032年) 婴儿背带市场规模、份额和成长分析(按类型、分销管道、价格分布和地区)- 2025-2032 年行业预测

婴儿背带市场规模、份额和成长分析(按类型、分销管道、价格分布和地区)- 2025-2032 年行业预测 婴幼儿背带及配件的全球市场

婴幼儿背带及配件的全球市场