|

市场调查报告书

商品编码

1928924

磺基琥珀酸酯市场机会、成长要素、产业趋势分析及2026年至2035年预测Sulfosuccinate Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

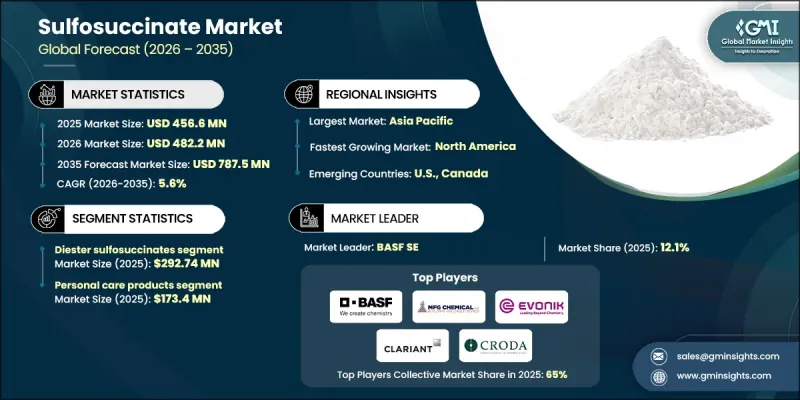

全球磺基琥珀酸酯市场预计到 2025 年将达到 4.566 亿美元,预计到 2035 年将达到 7.875 亿美元,年复合成长率为 5.6%。

市场成长动能主要源自于个人护理、家居和工业产品中对温和、易生物降解界面活性剂日益增长的需求。这种需求的驱动力来自消费者对更温和清洁方案的转变,这些方案即使在严苛条件下也能保持可靠的清洁性能,同时符合环境法规。法规结构和永续性发展政策正日益影响配方选择,推动了安全性高、生物降解性强、毒性低的界面活性剂的使用。个人保健产品消费量的成长迫使品牌重新设计产品体系,使其更加温和,尤其是在敏感肌肤应用方面。同时,亚太地区的经济快速成长和欧洲的监管审查进一步推动了此类产品的普及。工业和机构清洁标准也日趋严格,要求界面活性剂具备有效的润湿性、渗透性和最小残留性。永续性目标和绿色化学原则正在重塑表面活性剂的选择,製造商优先考虑符合严格生物降解性和环境性能标准的材料。这些趋势表明,监管政策和永续性要求正在积极塑造市场需求,而非仅仅是次要因素。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 4.566亿美元 |

| 预测金额 | 7.875亿美元 |

| 复合年增长率 | 5.6% |

二酯磺基琥珀酸酯因其优异的乳化和润湿性能,在高性能配方中占据主导地位。该领域的持续创新主要集中在改善泡沫控制、提高其在各种温度条件下的溶解度以及达到适用于高级应用的高纯度水平。这些改进正在推动其在消费品和工业系统中广泛应用。

2025年,个人护理应用领域占据了相当大的市场份额,这主要得益于对亲肤清洁剂和温和界面活性剂系统的需求。在家用清洁产品中,磺基琥珀酸酯被用于改善泡沫品质和清洁效率,同时确保使用者安全。在工业清洁应用中,磺基琥珀酸酯因其优异的润湿性和低残留性能而备受青睐,这也符合法规环境下的合规要求。此外,其需求来自众多工业领域,包括製药、纺织、农业、食品加工、涂料、石油天然气、造纸、皮革、黏合剂、采矿和金属加工等。

美国磺基琥珀酸酯市场预计在2025年达到1.048亿美元,并在2035年达到1.808亿美元。该地区的成长得益于产品倡议改良、以永续性发展为导向的产品开发,以及来自高规格工业和机构清洁领域的强劲需求。监管机构对更安全化学替代品的激励措施持续推动着销售稳定成长和溢价提升。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 产业潜在风险与挑战

- 市场机会

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特分析

- PESTEL 分析

- 价格趋势

- 按地区

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计(HS编码)(註:仅提供主要国家的贸易统计)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续努力

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

5. 2022-2035年按产品类型分類的炸药市场

- 二酯磺基琥珀酸酯

- 二辛基磺基琥珀酸钠

- 二异十三烷基磺基琥珀酸钠

- 二月桂基磺基琥珀酸钠

- 二十三烷基磺基琥珀酸钠

- 其他的

- 单酯磺基琥珀酸酯

- 月桂基磺基琥珀酸铵

- 月桂基磺基琥珀酸二钠

- 单烷基磺基琥珀酸酯乙氧基化物

- 共单乙醇酰胺磺基琥珀酸酯

- 其他的

第六章 烟火市场:依形式划分,2022-2035年

- 液体配方

- 糊状物製备

- 粉末製剂

第七章 烟火市场:依应用领域划分,2022-2035年

- 清洁剂

- 家用清洁剂和清洁剂

- 清洁剂

- 硬表面清洁剂

- 纤维和纺织品护理

- 其他的

- 工业用清洁剂

- 金属清洗和脱脂

- 商用和工业 (I&I) 清洁

- 汽车清洁剂

- 其他的

- 个人保健产品

- 洗髮精

- 身体保养乳液

- 化妆品

- 护髮产品

- 其他的

- 製药

- 口服泻药

- 片剂配方

- 其他的

- 食品/饮料

- 食品乳化剂

- 饮料加工

- 其他的

- 农业化学品

- 农药乳化剂

- 佐剂

- 其他的

- 纺织加工

- 染色/均匀性

- 纤维上浆剂

- 纺织助剂

- 皮革加工

- 皮革饰面

- 皮革染色

- 纸浆和造纸

- 油漆、涂料和油墨

- 石油和天然气

- 黏合剂和密封剂

- 采矿和矿物加工

- 金属加工/润滑

- 其他(防雾剂、壁纸去除剂、消毒剂)

第八章 2022-2035年各地区市场规模及预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第九章:公司简介

- The Dow Chemical Company

- Huntsman Corporation

- MFG Chemical

- Stepan Company

- Cytec Industries

- Air Products and Chemicals

- Evonik Industries AG

- Clariant AG

- Dupont

- Croda International

- KAO Corporation

- Henkel AG

The Global Sulfosuccinate Market was valued at USD 456.6 million in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 787.5 million by 2035.

Market momentum is driven by the growing preference for mild and readily biodegradable surfactants across personal care, household, and industrial formulations. Demand is supported by the shift toward gentle cleansing solutions that align with environmental compliance while maintaining dependable performance under demanding conditions. Regulatory frameworks and sustainability-driven policies are increasingly influencing formulation choices, encouraging the use of surfactants with verified safety, biodegradability, and low toxicity. Rising consumption of personal care and cosmetic products is pushing brands to reformulate toward gentler systems, particularly for sensitive-use applications, while rapid economic growth in Asia Pacific and regulatory oversight in Europe continue to reinforce adoption. Industrial and institutional cleaning standards are also becoming more stringent, requiring surfactants that deliver effective wetting, penetration, and minimal residue. Sustainability goals and green chemistry principles are reshaping surfactant selection, with manufacturers prioritizing materials that meet strict biodegradability and environmental performance criteria. These trends indicate that regulatory policy and sustainability requirements are actively shaping market demand rather than serving as secondary considerations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $456.6 Million |

| Forecast Value | $787.5 Million |

| CAGR | 5.6% |

The diester sulfosuccinates dominate performance-focused formulations due to their strong emulsification and wetting characteristics. Continuous innovation across this segment is focused on improving foam control, enhancing solubility under varied temperature conditions, and achieving higher purity levels suitable for advanced applications. These improvements are supporting broader adoption across both consumer-facing and industrial systems.

The personal care applications segment held a significant share in 2025, supported by demand for dermatologically compatible cleansing and mild surfactant systems. Household cleaning products utilize sulfosuccinates to improve foam quality and cleaning efficiency while maintaining user safety. Industrial cleaning applications benefit from their effective wetting behavior and low-residue performance, aligning with compliance expectations in regulated environments. Additional demand stems from a wide range of industries, including pharmaceuticals, textiles, agriculture, food processing, coatings, oil and gas, paper, leather, adhesives, mining, and metal processing.

U.S. Sulfosuccinate Market was valued at USD 104.8 million in 2025 and is forecast to reach USD 180.8 million by 2035. Growth in the region is supported by reformulation initiatives, sustainability-driven product development, and strong demand from high-specification industrial and institutional cleaning sectors. Regulatory encouragement toward safer chemical alternatives continues to support steady volume growth and premium-value expansion.

Key companies active in the Global Sulfosuccinate Market include Stepan Company, Croda International, The Dow Chemical Company, Evonik Industries AG, Clariant AG, Huntsman Corporation, DuPont, Henkel AG, KAO Corporation, Air Products and Chemicals, MFG Chemical, and Cytec Industries. Companies operating in the Sulfosuccinate Market are strengthening their market position through targeted strategies focused on sustainability, innovation, and geographic expansion. Manufacturers are investing in research and development to enhance product mildness, biodegradability, and performance consistency. Portfolio optimization toward compliant and environmentally preferred formulations is a core priority. Firms are expanding production capabilities, improving supply chain resilience, and forming strategic partnerships with personal care and industrial formulators.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 Form

- 2.2.3 Application

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Explosives Market, By Product Type, 2022-2035(USD Million, Kilo Tons)

- 5.1 Key trends

- 5.2 Diester sulfosuccinates

- 5.2.1 Dioctyl sodium sulfosuccinate

- 5.2.2 Sodium diisotridecyl sulfosuccinate

- 5.2.3 Dilauryl sodium sulfosuccinate

- 5.2.4 Ditridecyl sodium sulfosuccinate

- 5.2.5 Others

- 5.3 Monoester sulfosuccinates

- 5.3.1 Ammonium lauryl sulfosuccinate

- 5.3.2 Disodium lauryl sulfosuccinate

- 5.3.3 Ethoxylated monoalkyl sulfosuccinates

- 5.3.4 Cocomonoethanolamide sulfosuccinate

- 5.4 Others

Chapter 6 Pyrotechnics Market, By Form, 2022-2035(USD Million, Kilo Tons)

- 6.1 Key trends

- 6.2 Liquid formulations

- 6.3 Paste formulations

- 6.4 Powder formulations

Chapter 7 Pyrotechnics Market, By Application, 2022-2035(USD Million, Kilo Tons)

- 7.1 Key trends

- 7.2 Dishwashing liquid

- 7.3 Household detergents & cleaners

- 7.3.1 Laundry detergents

- 7.3.2 Hard surface cleaners

- 7.3.3 Fabric & textile care

- 7.3.4 Others

- 7.4 Industrial cleaners

- 7.4.1 Metal cleaning & degreasing

- 7.4.2 Institutional & industrial (I&I) cleaning

- 7.4.3 Automotive cleaners

- 7.4.4 Others

- 7.5 Personal care products

- 7.5.1 Shampoos

- 7.5.2 Body care & lotions

- 7.5.3 Cosmetics

- 7.5.4 Hair care products

- 7.5.5 Others

- 7.6 Pharmaceutical

- 7.6.1 Oral laxatives

- 7.6.2 Tablet formulation

- 7.6.3 Others

- 7.7 Food & beverage

- 7.7.1 Food emulsifier

- 7.7.2 Beverage processing

- 7.7.3 Others

- 7.8 Agricultural chemicals

- 7.8.1 Agrochemical emulsifiers

- 7.8.2 Adjuvants

- 7.8.3 Others

- 7.9 Textile processing

- 7.9.1 Dyeing & leveling

- 7.9.2 Textile sizing

- 7.9.3 Textile auxiliaries

- 7.10 Leather processing

- 7.10.1 Leather finishing

- 7.10.2 Leather dyeing

- 7.11 Paper & pulp

- 7.12 Paints, coatings & inks

- 7.13 Oil & gas

- 7.14 Adhesives & sealants

- 7.15 Mining & mineral processing

- 7.16 Metalworking & lubrication

- 7.17 Others (antifog, wallpaper removers, germicidal preparations)

Chapter 8 Market Size and Forecast, By Region, 2022-2035(USD Million, Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 The Dow Chemical Company

- 9.2 Huntsman Corporation

- 9.3 MFG Chemical

- 9.4 Stepan Company

- 9.5 Cytec Industries

- 9.6 Air Products and Chemicals

- 9.7 Evonik Industries AG

- 9.8 Clariant AG

- 9.9 Dupont

- 9.10 Croda International

- 9.11 KAO Corporation

- 9.12 Henkel AG

全球聚丁二酸丁二醇酯市场规模、份额、趋势和成长分析报告(2026-2034年)琥珀酸全球市场规模、份额、趋势和成长分析报告(2026-2034)

全球聚丁二酸丁二醇酯市场规模、份额、趋势和成长分析报告(2026-2034年)琥珀酸全球市场规模、份额、趋势和成长分析报告(2026-2034) 2026-2030年全球琥珀酸市场

2026-2030年全球琥珀酸市场 琥珀酸市场规模、份额及成长分析(按类型、应用、终端用户产业和地区划分)-产业预测(2026-2033)

琥珀酸市场规模、份额及成长分析(按类型、应用、终端用户产业和地区划分)-产业预测(2026-2033) 生物琥珀酸衍生聚酯多元醇市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测(2025-2033 年)

生物琥珀酸衍生聚酯多元醇市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测(2025-2033 年) Polybutylene Succinate的全球市场

Polybutylene Succinate的全球市场 琥珀酸:市场占有率分析、产业趋势、统计数据、成长预测(2025-2030)生物基琥珀酸:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)琥珀酸市场规模(按类型、最终用途行业、地区和预测)

琥珀酸:市场占有率分析、产业趋势、统计数据、成长预测(2025-2030)生物基琥珀酸:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)琥珀酸市场规模(按类型、最终用途行业、地区和预测) 2030 年琥珀酸市场预测:按类型、应用程式、最终用户和地区分類的全球分析

2030 年琥珀酸市场预测:按类型、应用程式、最终用户和地区分類的全球分析