|

市场调查报告书

商品编码

1959293

植物来源调质剂市场机会、成长要素、产业趋势分析及2026年至2035年预测。Plant Based Texturizers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

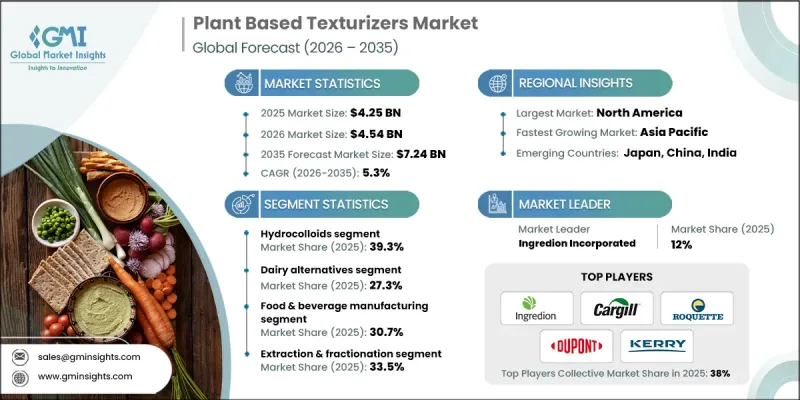

2025 年全球植物来源调质剂市值为 42.5 亿美元,预计到 2035 年将达到 72.4 亿美元,年复合成长率为 5.3%。

在食品、营养补充品、个人护理和工业应用等现代产品设计中,质地、稳定性和均匀性是至关重要的性能特征,而植物性成分在此类产品中扮演着举足轻重的角色。植物来源成分的应用范围已不再局限于特定的领域,如今已成为主流产品开发不可或缺的一部分。这一转变反映了消费者对天然来源、透明且来源可靠的成分的强劲需求。加工方法、成分精炼和生物优化技术的不断进步,使得植物来源调质剂能够实现更高的功能性、更强的耐热性、更优异的分散性和与复杂配方更佳的相容性。这些改进使製造商能够在满足监管要求和永续性目标的同时,取代传统的合成材料。企业致力于建立更具环保意识的供应链并减少对石油化学成分的依赖,进一步推动了市场成长,并将植物来源调质剂定位为面向未来的配方策略的基础要素。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 42.5亿美元 |

| 预测金额 | 72.4亿美元 |

| 复合年增长率 | 5.3% |

预计到2025年,亲水胶体市占率将达到39.3%,并在2035年之前以4.7%的复合年增长率成长。这些原材料为黏度控制、水分保持和整体产品稳定性提供了至关重要的结构支撑,广泛应用于各个终端应用产业。其适应性使混配商能够微调质地和口感,因此对于成熟产品线和新兴的植物来源产品而言,它们都必不可少,因为这些产品需要可靠且天然的性能特征。

预计到2025年,替代乳製品应用领域将占据27.3%的市场份额,并在2026年至2035年间以6.9%的复合年增长率增长。植物来源调质剂对于实现非乳製品配方所需的理想奶油质感、顺滑质地和稳定乳化至关重要。这些成分有助于在整个生产、储存和分销过程中保持产品品质的一致性,维持产品的感官吸引力和结构完整性,同时满足洁净标示的要求。

预计2025年,北美植物来源调质剂市占率将达37%。该地区受益于先进的加工技术、创新製造商以及积极支持永续和植物来源趋势的成熟消费群。健全的法规结构和对研发的大力投入进一步巩固了北美在该市场的主导地位。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 消费者对植物来源食品的需求日益增长

- 洁净标示和天然成分的发展趋势

- 对植物来源替代品的监管支持

- 产业潜在风险与挑战

- 与传统调质剂相比,生产成本更高

- 与感官特性和风味相关的问题(异味、苦味)

- 市场机会

- 新兴蛋白质来源(藻类、真菌、新型豆科植物)

- 功能性配方和客製化调质剂系统

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 价格趋势

- 按地区

- 依产品类型

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计(HS编码)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 具有环保意识的倡议

- 考虑碳足迹

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 公司矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估算与预测:依产品类型划分,2022-2035年

- 水溶性多醣

- 植物性蛋白质(组织化)

- 淀粉

- 纤维素衍生物

- 其他植物来源的调质剂

第六章 市场估计与预测:依应用领域划分,2022-2035年

- 乳製品替代品

- 麵包糖果甜点

- 肉类替代品/肉类替代品

- 饮料

- 酱汁、调味料和佐料

- 零食和速食

- 冷冻食品/加工食品

第七章 市场估计与预测:依最终用户划分,2022-2035年

- 食品饮料製造业

- 谷物和油籽加工

- 乳製品替代品生产商

- 麵包和糖果甜点

- 适用于餐饮服务业及设施

- 零售和消费品

第八章 市场估计与预测:依技术划分,2022-2035年

- 挤出技术

- 基于发酵的生产

- 萃取和分馏

- 新型纹理技术

- 化学和物理改性

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第十章:公司简介

- Ingredion Incorporated

- Cargill, Incorporated

- Roquette Freres

- ICL Food Specialties(ICL Group)

- DuPont Nutrition &Biosciences

- Kerry Group plc

- Ashland Global Holdings Inc.

- PURIS Holdings LLC

- Marine Hydrocolloids

- TIC Gums

- Palsgaard A/S

- Fiberstar Inc

- CP Kelco

- Socius Ingredients

- Burcon NutraScience Corporation

The Global Plant Based Texturizers Market was valued at USD 4.25 billion in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 7.24 billion by 2035.

The market plays a critical role in modern formulation across food, nutraceutical, personal care, and industrial applications, where texture, stability, and consistency are essential performance attributes. Ingredients derived from plant sources have moved beyond limited or specialized use and are now integral to mainstream product development. This shift reflects strong consumer demand for natural, transparent, and responsibly sourced ingredients. Ongoing advancements in processing methods, ingredient refinement, and biological optimization are enabling plant-based texturizers to deliver higher functionality, improved thermal resistance, better dispersibility, and greater compatibility with complex formulations. These improvements enable manufacturers to replace conventional synthetic materials while meeting regulatory requirements and sustainability objectives. Corporate commitments to greener supply chains and reduced dependence on petrochemical inputs are further reinforcing market growth, positioning plant-based texturizers as a foundational component of future-oriented formulation strategies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.25 Billion |

| Forecast Value | $7.24 Billion |

| CAGR | 5.3% |

The hydrocolloids segment held a share of 39.3% in 2025 and is expected to grow at a CAGR of 4.7% through 2035. These ingredients provide critical structural support by managing viscosity, moisture retention, and overall product stability across multiple end-use industries. Their adaptability allows formulators to fine-tune texture and mouthfeel, making them indispensable for both established product lines and emerging plant-forward innovations that require reliable, naturally sourced performance characteristics.

The dairy alternatives application segment accounted for 27.3% share in 2025 and is forecast to grow at a CAGR of 6.9% from 2026 to 2035. Plant-based texturizers are essential in delivering the desired creaminess, smooth consistency, and stable emulsification required in non-dairy formulations. These ingredients support consistent quality throughout manufacturing, storage, and distribution, ensuring products maintain their sensory appeal and structural integrity while aligning with clean-label expectations.

North America Plant Based Texturizers Market held a 37% share in 2025. The region benefits from advanced processing capabilities, innovation-driven manufacturers, and a well-established consumer base that actively supports sustainable and plant-focused formulation trends. Robust regulatory frameworks and strong investment in research and development further reinforce North America's leadership position in this market.

Key companies operating in the Global Plant Based Texturizers Market include Cargill, Incorporated, Ingredion Incorporated, Kerry Group plc, Roquette Freres, CP Kelco, DuPont Nutrition & Biosciences, Ashland Global Holdings Inc., ICL Food Specialties (ICL Group), Palsgaard A/S, TIC Gums, Fiberstar Inc, PURIS Holdings LLC, Marine Hydrocolloids, Burcon NutraScience Corporation, and Socius Ingredients. Companies in the plant based texturizers market are strengthening their competitive position by focusing on innovation, sustainability, and application-specific solutions. Many players are investing heavily in research to enhance ingredient performance, improve functionality, and expand use across diverse formulation systems. Strategic partnerships with food and personal care manufacturers are being used to accelerate product adoption and co-develop tailored solutions. Firms are also expanding production capacity and sourcing capabilities to ensure supply chain reliability and traceability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Application

- 2.2.4 End-User

- 2.2.5 Technology Method

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer demand for plant-based foods

- 3.2.1.2 Clean label & natural ingredient trends

- 3.2.1.3 Regulatory support for plant-based alternatives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs vs conventional texturizers

- 3.2.2.2 Sensory & flavor challenges (off-notes, bitterness)

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging protein sources (algae, fungi, novel legumes)

- 3.2.3.2 Functional blends & customized texturizer systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Hydrocolloids

- 5.3 Plant proteins (texturized)

- 5.4 Starches

- 5.5 Cellulose derivatives

- 5.6 Other plant-based texturizers

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Dairy Alternatives

- 6.3 Bakery & Confectionery

- 6.4 Meat Alternatives & Analogs

- 6.5 Beverages

- 6.6 Sauces, Dressings & Condiments

- 6.7 Snacks & Convenience Foods

- 6.8 Frozen & Processed Foods

Chapter 7 Market Estimates and Forecast, By End-User, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverage manufacturing

- 7.3 Grain & oilseed processing

- 7.4 Dairy alternative manufacturers

- 7.5 Bakery & confectionery

- 7.6 Foodservice & institutional

- 7.7 Retail & consumer packaged goods

Chapter 8 Market Estimates and Forecast, By Technology Method, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Extrusion technology

- 8.3 Fermentation-based production

- 8.4 Extraction & fractionation

- 8.5 Novel texturization technologies

- 8.6 Chemical/physical modification

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Ingredion Incorporated

- 10.2 Cargill, Incorporated

- 10.3 Roquette Freres

- 10.4 ICL Food Specialties (ICL Group)

- 10.5 DuPont Nutrition & Biosciences

- 10.6 Kerry Group plc

- 10.7 Ashland Global Holdings Inc.

- 10.8 PURIS Holdings LLC

- 10.9 Marine Hydrocolloids

- 10.10 TIC Gums

- 10.11 Palsgaard A/S

- 10.12 Fiberstar Inc

- 10.13 CP Kelco

- 10.14 Socius Ingredients

- 10.15 Burcon NutraScience Corporation

全球植物来源食品市场规模、份额、趋势和成长分析报告(2026-2034)

全球植物来源食品市场规模、份额、趋势和成长分析报告(2026-2034) 植物基食品市场趋势预测至2032年:按类型、成分、形式、分销管道、应用和地区分類的全球分析

植物基食品市场趋势预测至2032年:按类型、成分、形式、分销管道、应用和地区分類的全球分析 植物来源食品市场规模、份额和成长分析(按类型、通路、性质、成分和地区划分)—产业预测(2026-2033 年)2032年植物性食品质地增强市场预测:按产品类型、性质、质地形态、应用和地区分類的全球分析

植物来源食品市场规模、份额和成长分析(按类型、通路、性质、成分和地区划分)—产业预测(2026-2033 年)2032年植物性食品质地增强市场预测:按产品类型、性质、质地形态、应用和地区分類的全球分析 全球植物性零食市场Aquafaba 的全球市场全球植物性食品市场

全球植物性零食市场Aquafaba 的全球市场全球植物性食品市场 美国的植物性食品市场评估:各产品类型,各来源,各最终用途,各流通管道,各地区,机会,预测,2018年~2032年到 2030 年植物性食品市场预测:按产品、原材料、分销管道、最终用户和地区进行的全球分析

美国的植物性食品市场评估:各产品类型,各来源,各最终用途,各流通管道,各地区,机会,预测,2018年~2032年到 2030 年植物性食品市场预测:按产品、原材料、分销管道、最终用户和地区进行的全球分析 植物性食品市场报告:2030 年趋势、预测与竞争分析

植物性食品市场报告:2030 年趋势、预测与竞争分析