|

市场调查报告书

商品编码

1998799

冷冻烘焙食品市场机会、成长要素、产业趋势分析及2026-2035年预测Frozen Bakery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

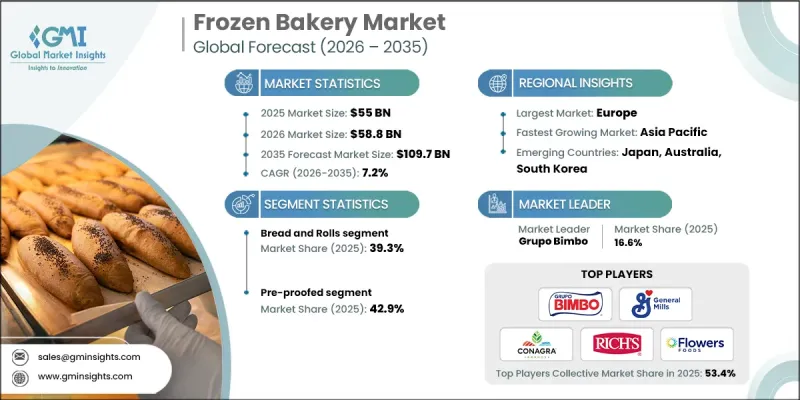

全球冷冻烘焙食品市场预计到 2025 年将达到 550 亿美元,预计到 2035 年将以 7.2% 的复合年增长率增长至 1,097 亿美元。

随着传统麵包製作方法与现代食品加工技术的日益融合,冷冻烘焙市场正经历显着的变化。曾经被视为纯粹以便利性为导向的品类,如今已成为餐饮服务、零售分销和商用供应体系中不可或缺的一部分。行业相关人员正日益重视自动化和先进的生产技术,以提高营运效率并应对劳动力短缺问题。永续性也变得越发重要,企业致力于减少废弃物、优化能源利用并改善包装策略,以符合环保要求。遵守有关食品安全和原材料透明度的监管标准已成为市场准入的基本要求。产品多元化也在重塑市场格局,製造商正在开发各种各样的冷冻烘焙产品,以满足消费者多样化的偏好和营运需求。冷冻烘焙产品能够适应各种烹饪方法和烘焙工艺,因此为製造商和餐饮服务供应商提供了柔软性。此外,新的分销模式有助于在企业发展扩张和保持营运灵活性之间取得平衡。物流能力的提升和筹资策略的改进也增强了整个冷冻烘焙行业供应链的韧性。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 550亿美元 |

| 预测金额 | 1097亿美元 |

| 复合年增长率 | 7.2% |

预计到2025年,预发酵产品将占据42.9%的市场。该市场涵盖多种生产和加工方法,使製造商能够提供满足不同营运需求的客製化烘焙产品。预发酵冷冻烘焙产品在冷冻前会进行发酵,以便在现场完成最终的发酵和烘焙。这项工艺能够使产品在香气、质地和整体品质方面都接近新鲜烘焙产品。另一种常见的生产方法是在冷冻前对产品进行部分烘焙,这既能缩短最终烘焙时间,又能维持产品品质。这些工艺使企业能够在保持产品一致性的同时,减少烘焙时间和操作复杂性,使冷冻烘焙产品能够很好地适应各种餐饮服务和零售环境。

受消费者生活方式改变和对便利食品需求成长的推动,预计到2025年,北美冷冻烘焙食品市场规模将达到147亿美元。消费者越来越青睐易于烹饪且品质优良的烘焙产品。冷冻烘焙产品在零售和餐饮通路的广泛供应进一步巩固了其市场地位。为满足餐饮服务商和零售经销商日益增长的需求,製造商正在扩大产品线和产能。大型零售商店和商用餐饮机构对冷冻烘焙产品的日益青睐,也持续推动该地区市场的稳定成长。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 对简便食品的需求不断增长

- 新兴市场零售通路的发展

- 冷冻烘焙点心的优良特性

- 产业潜在风险与挑战

- 传统新鲜烘焙产品的市场需求成熟

- 解冻后保存期限短

- 市场机会

- 都市化和生活方式的改变

- 现代零售通路与电子商务的扩张

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 价格趋势

- 按地区

- 依产品类型

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利趋势

- 贸易统计(HS编码)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 环保意识的倡议

- 考虑碳足迹

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估算与预测:依产品类型划分,2022-2035年

- 麵包和捲饼

- 特色麵包

- 三明治麵包卷

- 汉堡麵包

- 其他的

- 披萨饼皮

- 传统披萨饼皮

- 薄布料

- 特製饼皮

- 酥皮点心和可颂麵包

- 丹麦酥皮

- 酥皮点心

- 咸味酥皮点心

- 甜点烘焙点心

- 油炸圈饼

- 甜麵包卷

- 鬆饼

- 速成麵包

- 其他的

- 特色手工麵包

- 有机的

- 纯素/植物来源

第六章 市场估算与预测:依製造方法划分,2022-2035年

- 预发酵

- 部分发酵

- 完全的

- 准备射击

第七章 市场估算与预测:依最终使用者管道划分,2022-2035年

- 店内烘焙坊

- 超级市场和大卖场里的麵包房

- 便利商店麵包店

- 百货公司美食广场

- 速食店

- 速食连锁店

- 速食餐厅

- 咖啡店和咖啡馆

- 饭店和餐饮

- 饭店食品服务

- 餐饮和活动服务

- 机构食品服务

- 独立麵包店

- 新兴管道

- 幽灵厨房

- 云厨房

- 餐车和流动摊贩

- 线上到线下(O2O)模式

第八章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 波兰

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 泰国

- 印尼

- 马来西亚

- 澳洲

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第九章:公司简介

- Accion Alimenticia

- Aryzta AG

- BredenMaster SA

- Canada Bread Company

- Conagra Brands, Inc.

- Dr. Oetker

- Europastry

- Flowers Foods

- General Mills

- Grupo Bimbo

- Lantmannen Unibake

- Navona Kitchen LLP(Pizzo &Crozzo)

- Rhodes Bake-N-Serv

- Rich Products Corporation

- Vandemoortele

The Global Frozen Bakery Market was valued at USD 55 billion in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 109.7 billion by 2035.

The frozen bakery market is undergoing a notable evolution as traditional baking practices are increasingly combined with modern food processing technologies. What was once considered a purely convenience-oriented category is now becoming an essential component of foodservice operations, retail distribution, and institutional supply systems. Industry participants are increasingly prioritizing automation and advanced production technologies to improve operational efficiency and manage workforce challenges. Sustainability considerations are also gaining importance, prompting companies to focus on waste reduction, energy optimization, and improved packaging strategies that align with environmental expectations. Compliance with regulatory standards related to food safety and ingredient transparency has become a fundamental requirement for market participation. Product diversification is also shaping the market, with manufacturers developing a wide range of frozen bakery items to meet varying consumer preferences and operational needs. Frozen bakery products provide flexibility for both manufacturers and foodservice operators by supporting different preparation methods and baking processes. In addition, emerging distribution models are helping businesses expand their reach while maintaining operational adaptability. Improved logistics capabilities and more efficient sourcing strategies are also strengthening supply chain resilience across the frozen bakery industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $55 Billion |

| Forecast Value | $109.7 Billion |

| CAGR | 7.2% |

The pre-proofed segment accounted for 42.9% share in 2025. The market includes several production and preparation approaches that allow manufacturers to supply bakery products tailored to diverse operational requirements. Pre-proofed frozen bakery items undergo fermentation prior to freezing, which allows final proofing and baking to be completed at the point of preparation. This process helps deliver freshly baked characteristics in terms of aroma, texture, and overall product quality. Another common production approach involves partially baking products before freezing them, which preserves product quality while allowing for faster preparation during final baking. These processes enable businesses to maintain product consistency while reducing preparation time and operational complexity, making frozen bakery products highly adaptable for a wide range of foodservice and retail environments.

North America Frozen Bakery Market was valued at USD 14.7 billion in 2025, supported by evolving consumer lifestyles and the increasing demand for convenient food options. Consumers are increasingly drawn to bakery products that offer easy preparation while maintaining high product quality. The availability of frozen bakery products across multiple retail and foodservice channels has further strengthened their market presence. Growing demand from foodservice operators and retail distributors is encouraging manufacturers to expand their product offerings and production capabilities. The widespread presence of frozen bakery products across large-scale retail outlets and commercial foodservice establishments continues to support steady market growth in the region.

Key companies operating in the Global Frozen Bakery Market include Grupo Bimbo, Aryzta AG, Europastry, Vandemoortele, Conagra Brands, Inc., General Mills, Flowers Foods, Rich Products Corporation, Dr. Oetker, Lantmannen Unibake, Canada Bread Company, Rhodes Bake-N-Serv, Accion Alimenticia, BredenMaster S.A., and Navona Kitchen LLP (Pizzo & Crozzo). Companies operating in the Frozen Bakery Market are implementing a variety of strategic initiatives to strengthen their competitive positions and expand their market presence. A major focus remains on product innovation, with manufacturers developing new frozen bakery formulations that align with evolving consumer preferences and foodservice requirements. Many companies are investing in advanced production technologies and automation to enhance efficiency, maintain consistent product quality, and address labor challenges within manufacturing operations. Strategic partnerships with foodservice providers, distributors, and retail chains are helping companies broaden their distribution networks and improve market reach. In addition, businesses are expanding production facilities and strengthening supply chain capabilities to meet rising global demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Baking process

- 2.2.4 End-user channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for convenience food

- 3.2.1.2 Developing retail channels in emerging nations

- 3.2.1.3 Superior properties of frozen baked products

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Mature conventional fresh baked products market demand

- 3.2.2.2 Short shelf life after thawing

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing urbanization and changing lifestyles

- 3.2.3.2 Expansion of modern retail channels and e-commerce

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Bread and rolls

- 5.2.1 Specialty breads

- 5.2.2 Sandwich rolls

- 5.2.3 Burger buns

- 5.2.4 Others

- 5.3 Pizza crusts

- 5.3.1 Traditional pizza crusts

- 5.3.2 Thin crust

- 5.3.3 Specialty crust

- 5.4 Pastries and croissants

- 5.4.1 Danish pastries

- 5.4.2 Sweet pastries

- 5.4.3 Savory pastry

- 5.5 Sweet baked goods

- 5.5.1 Donuts

- 5.5.2 Sweet rolls

- 5.5.3 Muffins

- 5.5.4 Quick breads

- 5.5.5 Others

- 5.6 Specialty and artisanal products

- 5.6.1 Organic

- 5.6.2 Vegan/plant based

Chapter 6 Market Estimates and Forecast, By Baking Process, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Pre-proofed

- 6.3 Partially

- 6.4 Fully

- 6.5 Ready-to-bake

Chapter 7 Market Estimates and Forecast, By End-User Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 In-store bakeries

- 7.2.1 Supermarket and hypermarket bakeries

- 7.2.2 Convenience store bakeries

- 7.2.3 Department store food courts

- 7.3 Quick service restaurants

- 7.3.1 Fast food chains

- 7.3.2 Fast casual restaurants

- 7.3.3 Coffee shops and cafes

- 7.4 Hotels and catering

- 7.4.1 Hotel food service

- 7.4.2 Catering and event services

- 7.4.3 Institutional foodservice

- 7.5 Independent bakeries

- 7.6 Emerging channel

- 7.6.1 Ghost kitchens

- 7.6.2 Cloud kitchens

- 7.6.3 Food trucks and mobile vendors

- 7.6.4 Online-to-offline (O2O) models

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Poland

- 8.3.7 Russia

- 8.3.8 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Thailand

- 8.4.5 Indonesia

- 8.4.6 Malaysia

- 8.4.7 Australia

- 8.4.8 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Accion Alimenticia

- 9.2 Aryzta AG

- 9.3 BredenMaster S.A.

- 9.4 Canada Bread Company

- 9.5 Conagra Brands, Inc.

- 9.6 Dr. Oetker

- 9.7 Europastry

- 9.8 Flowers Foods

- 9.9 General Mills

- 9.10 Grupo Bimbo

- 9.11 Lantmannen Unibake

- 9.12 Navona Kitchen LLP (Pizzo & Crozzo)

- 9.13 Rhodes Bake-N-Serv

- 9.14 Rich Products Corporation

- 9.15 Vandemoortele

全球冷冻烘焙产品市场规模、份额、趋势和成长分析报告(2026-2034年)全球冷冻烘焙添加剂市场规模、份额、趋势和成长分析报告(2026-2034年)

全球冷冻烘焙产品市场规模、份额、趋势和成长分析报告(2026-2034年)全球冷冻烘焙添加剂市场规模、份额、趋势和成长分析报告(2026-2034年) 全球冷冻烘焙产品市场:按特色类型、最终用户、分销管道、消费模式、类型和地区划分-预测至2030年

全球冷冻烘焙产品市场:按特色类型、最终用户、分销管道、消费模式、类型和地区划分-预测至2030年 冷冻烘焙产品市场-全球产业规模、份额、趋势、机会及预测(按类型、消费类型、销售管道、地区和竞争格局划分,2021-2031年)

冷冻烘焙产品市场-全球产业规模、份额、趋势、机会及预测(按类型、消费类型、销售管道、地区和竞争格局划分,2021-2031年) 冷冻烘焙产品市场规模、份额及成长分析(按类型、分销通路、消费类型、特色及地区划分)-产业预测(2026-2033 年)

冷冻烘焙产品市场规模、份额及成长分析(按类型、分销通路、消费类型、特色及地区划分)-产业预测(2026-2033 年) 冷冻烘焙食品市场规模、份额及成长分析(按类型、消费类型、特色、通路管道及地区划分)-2026-2033年产业预测冷冻烘焙产品市场-2025-2030年预测

冷冻烘焙食品市场规模、份额及成长分析(按类型、消费类型、特色、通路管道及地区划分)-2026-2033年产业预测冷冻烘焙产品市场-2025-2030年预测 冷冻烘焙产品:全球市占率及排名、总收入及需求预测(2025-2031年)

冷冻烘焙产品:全球市占率及排名、总收入及需求预测(2025-2031年) 拉丁美洲冷冻烘焙产品市场规模及预测(2021-2031年)、区域份额、趋势和成长机会分析报告涵盖范围:按产品类型划分,包括饼干和糕点

拉丁美洲冷冻烘焙产品市场规模及预测(2021-2031年)、区域份额、趋势和成长机会分析报告涵盖范围:按产品类型划分,包括饼干和糕点 全球冷冻烘焙添加剂市场

全球冷冻烘焙添加剂市场