|

市场调查报告书

商品编码

1413835

农业生物防治剂市场:按产品类型、品种、作物类型、应用、最终用户 - 全球预测 2024-2030Agricultural Biological Control Agents Market by Product Type (Bacteria, Fungi, Parasitoids), Type (Biopesticides, Semiochemicals), Crop Type, Application, End-User - Global Forecast 2024-2030 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

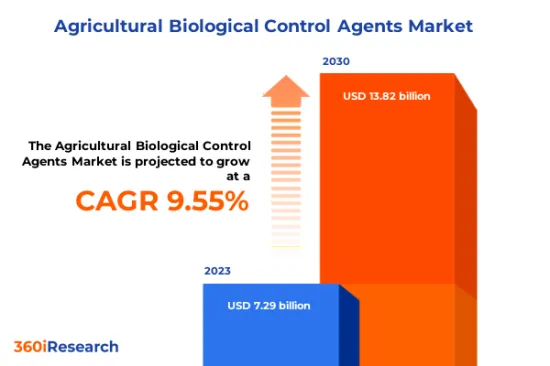

预计2023年农业生物防治剂市场规模为72.9亿美元,预计2024年将达79.5亿美元,2030年将达到138.2亿美元,复合年增长率为9.55%。

农业生物防治剂的全球市场

| 主要市场统计 | |

|---|---|

| 基准年[2023] | 72.9亿美元 |

| 预测年份 [2024] | 79.5亿美元 |

| 预测年份 [2030] | 138.2亿美元 |

| 复合年增长率(%) | 9.55% |

生物防治剂主要应用于园艺、大田耕作和温室栽培等农业领域的害虫综合管理(IPM)策略。最终用户包括商业规模的农民和专注于永续农业实践的个人生产者。该市场也针对促进环保农业实践的研究机构和政府机构。由于对环保和永续害虫管理解决方案的需求不断增加,农业生物防治剂市场正在显着成长。随着监管机构推广环境安全的替代品以及消费者对有机产品的需求增加,寄生虫、掠食者、病原体和竞争者等天然生物的使用正在获得动力。这些药剂主要由大型和个体生产者在园艺、田间耕作和温室栽培等不同农业环境中的综合害虫管理 (IPM) 计划中使用。推动这一市场发展的是生物技术的进步,提高了生物药品的效率,以及人们普遍认识到化学农药对人类健康和生态系统的负面影响。随着市场的扩大和专注于精准应用技术和新型生物防治剂发现的合作机会的出现,公司透过投资创新来实现成长。然而,必须解决药物保质期有限、环境因素导致的疗效变化以及监管复杂性等挑战。对配方技术、标靶输送系统、基因改良和综合 IPM 策略的投资对于克服这些障碍和促进市场扩张至关重要。此外,教育农民了解生物防治方法的部署和好处对于该行业的发展至关重要。

区域洞察

在美洲,特别是在美国和加拿大,化学农药监管压力的增加以及对永续农业实践的认识的提高导致生物防治剂的采用增加。消费者趋势显示出向有机食品消费的转变,刺激了对生物控制解决方案的需求。两国对研发的投资导致了创新且有效的生物防治剂的引进。该地区的最新专利通常围绕着新的生物农药配方和基因改造生物来有效防治害虫。主要措施包括美国农业部 (USDA) 推广纳入生物防治的综合害虫管理 (IPM) 策略。欧盟有严格的环保法规,导致对环保生物防治剂的需求很高。该地区的消费者对农业对环境的影响高度敏感,促使製造商专注于永续的生物防治产品。该地区的研究通常得到政府机构的资助,促进天然害虫防治剂的创新。欧盟的研究和技术开发架构计画对于资助旨在优化生物防治剂使用的计划至关重要。此外,欧盟通用农业政策支持使用生物控制方法作为绿色指令的一部分。亚太地区,特别是中国、日本和印度,农业生物防治剂市场正在快速成长。这是由于该地区的大规模农业活动、对环境的日益关注以及在不损害生态系统的情况下提高产量的需要。合作伙伴关係和研究计划在亚太地区很常见,政府支持计划正在促进生物控制产品的开发和引进。在中东和非洲,生物防治方法的引入受到气候条件以及水资源短缺和其他环境问题下永续农场管理实践需求的影响。粮农组织和地方政府等国际组织的发展措施旨在教育农民了解生物製药在害虫防治方面的益处。

FPNV定位矩阵

FPNV定位矩阵对于评估农业生防剂市场至关重要。我们检视与业务策略和产品满意度相关的关键指标,以对供应商进行全面评估。这种深入的分析使用户能够根据自己的要求做出明智的决策。根据评估,供应商被分为四个成功程度不同的像限:前沿(F)、探路者(P)、利基(N)和重要(V)。

市场占有率分析

市场占有率分析是一种综合工具,可以对农业生物防治剂市场供应商的现状进行深入而详细的研究。全面比较和分析供应商在整体收益、基本客群和其他关键指标方面的贡献,以便更好地了解公司的绩效及其在争夺市场占有率时面临的挑战。此外,该分析还提供了对该行业竞争特征的宝贵考察,包括在研究基准年观察到的累积、分散主导地位和合併特征等因素。这种详细程度的提高使供应商能够做出更明智的决策并制定有效的策略,从而在市场上获得竞争优势。

本报告在以下方面提供了宝贵的见解:

1-市场渗透率:提供有关主要企业所服务的市场的全面资讯。

2-市场开拓:我们深入研究利润丰厚的新兴市场,并分析它们在成熟细分市场中的渗透率。

3- 市场多元化:提供有关新产品发布、开拓地区、最新发展和投资的详细资讯。

4-竞争力评估与资讯:对主要企业的市场占有率、策略、产品、认证、监管状况、专利状况、製造能力等进行全面评估。

5- 产品开发与创新:提供对未来技术、研发活动和突破性产品开发的见解。

本报告解决了以下关键问题:

1-农业生防剂市场规模与预测是多少?

2-在农业生物防治剂市场的预测期间内,有哪些产品、细分市场、应用和领域需要考虑投资?

3-农业生物防治剂市场的技术趋势和法律规范是什么?

4-农业生物防治剂市场主要供应商的市场占有率为何?

5-进入农业生防剂市场合适的型态和策略手段是什么?

目录

第一章 前言

第二章调查方法

第三章执行摘要

第四章市场概况

第五章市场洞察

- 市场动态

- 促进因素

- 人们越来越关注农药使用对环境的影响

- 政府努力改善害虫管理并促进采用生物防治剂

- 有机农产品方向

- 抑制因素

- 对生物防治剂的效率和有效性的担忧

- 机会

- 持续研发高效能农业生防剂

- 生物防治剂的监管核准和上市

- 任务

- 对抗药性控制和品管的担忧

- 促进因素

- 市场区隔分析

- 产品:基于细菌的药剂是农业系统中的首选,可最大限度地减少对环境的影响并促进永续的杂草管理。

- 类型:生物杀虫剂是首选,因为它们具有广泛的作用,可影响多种害虫。

- 作物类型:不同作物的广泛和特殊需求的永续农业实践趋势将影响所开发的生物控制类型。

- 应用:种子处理应用适用于保护植物免受发育早期阶段的影响。

- 市场趋势分析

- 高通膨的累积效应

- 波特五力分析

- 价值炼和关键路径分析

- 法律规范

第六章农业生物防治剂市场:依产品类型

- 细菌

- 菌类

- 寄生虫

- 掠食者

- 除草剂

第七章农业生物防治剂市场:依类型

- 生物农药

- 生物杀菌剂

- 生物除草剂

- 生物杀虫剂

- 除生物剂

- 资讯化学

- 种间化学交感物质

- 信息素

第八章农业生物防治剂市场:依作物类型

- 粮食

- 玉米

- 米

- 小麦

- 水果和蔬菜

- 莓果

- 柑橘类水果

- 绿叶蔬菜

- 仁果

- 根茎类蔬菜

- 油籽和豆类

- 大豆

- 向日葵

第九章农业生物防治剂市场:依应用分类

- 叶面喷布喷施

- 种子处理

- 土壤处理

第十章农业生物防治剂市场:依最终用户分类

- 商业规模农业

- 个人种植者

第十一章美洲农业生物防治剂市场

- 阿根廷

- 巴西

- 加拿大

- 墨西哥

- 美国

第十二章亚太地区农业生物防治剂市场

- 澳洲

- 中国

- 印度

- 印尼

- 日本

- 马来西亚

- 菲律宾

- 新加坡

- 韩国

- 台湾

- 泰国

- 越南

第十三章欧洲、中东和非洲农业生防剂市场

- 丹麦

- 埃及

- 芬兰

- 法国

- 德国

- 以色列

- 义大利

- 荷兰

- 奈及利亚

- 挪威

- 波兰

- 卡达

- 俄罗斯

- 沙乌地阿拉伯

- 南非

- 西班牙

- 瑞典

- 瑞士

- 土耳其

- 阿拉伯聯合大公国

- 英国

第14章竞争形势

- FPNV定位矩阵

- 市场占有率分析:按主要企业划分

- 主要企业竞争情境分析

- 新产品发布和功能增强

- 投资、资金筹措

第15章竞争产品组合

- 主要公司简介

- AgBiTech Pty. Ltd.

- Andermatt Group AG

- BASF SE

- Bayer AG

- Biocontrol Technologies SL

- Bioline AgroSciences Ltd.

- BioWorks, Inc. by Biobest Group NV

- Cearitis

- Certis Biologicals by Mitsui & Co., Ltd.

- Corteva Agriscience

- Dora Agri-Tech

- Eco Bugs India Private Limited

- FMC Corporation

- IPL Biologicals Limited

- Isagro SpA

- Koppert Biological Systems

- Manidharma Biotech Private Limited

- Marrone Bio Innovations, Inc. by Bioceres Crop Solutions Corp.

- Novozymes A/S

- Prakriti Biotech

- Russell IPM Ltd.

- Shin-Etsu Chemical Co. Ltd.

- STK Bio-Ag Technologies

- Suterra LLC by The Wonderful Company LLC

- Syngenta Crop Protection AG

- UPL Limited

- Valent Biosciences LLC by Sumitomo Chemical Co., Ltd.

- Vegalab SA

- 主要产品系列

第十六章附录

- 讨论指南

- 关于许可证和定价

[191 Pages Report] The Agricultural Biological Control Agents Market size was estimated at USD 7.29 billion in 2023 and expected to reach USD 7.95 billion in 2024, at a CAGR 9.55% to reach USD 13.82 billion by 2030.

Global Agricultural Biological Control Agents Market

| KEY MARKET STATISTICS | |

|---|---|

| Base Year [2023] | USD 7.29 billion |

| Estimated Year [2024] | USD 7.95 billion |

| Forecast Year [2030] | USD 13.82 billion |

| CAGR (%) | 9.55% |

Biological control agents are primarily applied in integrated pest management (IPM) strategies across various agricultural segments such as horticulture, field crops, and greenhouse farming. End-users include both commercial-scale farm operations and individual growers focused on sustainable and organic farming practices. The scope of the market also extends to research institutions and government bodies promoting eco-friendly farming initiatives. The market for agricultural biological control agents is experiencing significant growth due to the increasing need for eco-friendly and sustainable pest management solutions. As regulatory bodies push for environment-safe alternatives and consumer demand for organic produce rises, the use of natural organisms such as parasites, predators, pathogens, and competitors has gained momentum. These agents are primarily utilized in integrated pest management (IPM) programs across diverse agricultural settings, including horticulture, field crops, and greenhouse farming, by both large-scale and individual growers. Fueling this market are technological advancements in biotechnology that enhance the efficiency of biological agents and the widespread acknowledgment of the negative impacts of chemical pesticides on human health and ecosystems. As opportunities emerge for market expansion and partnerships focusing on precision application technologies and novel biocontrol discoveries, companies are poised for growth by investing in innovation. However, challenges like the limited shelf life of agents, effectiveness variability due to environmental factors, and regulatory complexities must be addressed. To overcome these barriers and foster market expansion, investments in formulation technologies, targeted delivery systems, genetic improvements, and comprehensive IPM strategies are crucial. Moreover, educating farmers on the deployment and advantages of biological control methodologies is paramount for industry advancement.

Regional Insights

In the Americas, especially in the United States and Canada, there is a growing adoption of biological control agents due to increased regulatory pressures on chemical pesticides and rising awareness regarding sustainable agricultural practices. Consumer behavior trends indicate a shift towards organic food consumption, stimulating the demand for biocontrol solutions. Investments in R&D in both countries have led to the introduction of innovative and effective biological control agents. The latest patents in this region often revolve around novel biopesticide formulations and genetically modified organisms to combat pests effectively. Major initiatives include the United States Department of Agriculture's (USDA) efforts to promote integrated pest management (IPM) strategies, which incorporate biological controls. In the EU, environmental conservation regulations are stringent, leading to significant demand for eco-friendly biological control agents. Consumers in this region are highly sensitive to the environmental impact of agriculture, prompting manufacturers to emphasize sustainable biocontrol products. Research in this region is often subsidized by governmental bodies, fostering innovation in natural pest control treatments. EU's Framework Programmes for Research and Technological Development have been pivotal in financing projects that aim to optimize the use of biocontrol agents. Additionally, the EU's Common Agricultural Policy supports the use of biocontrol methods as part of its green directives. The Asia Pacific region, particularly China, Japan, and India, is experiencing rapid growth in the agricultural biocontrol market. This can be attributed to the region's large-scale agricultural activities, growing environmental concerns, and a need to increase yield without harming ecosystems. Partnerships and research initiatives are common in the Asia Pacific, with government-backed programs facilitating the development and adoption of biocontrol products. In the Middle East and Africa, the uptake of biological control methods is influenced by climate conditions and the need for sustainable farm management practices amidst water scarcity and other environmental concerns. Development initiatives by international organizations, such as the FAO and regional governments, aim to educate farmers on the benefits of biological agents in pest management.

FPNV Positioning Matrix

The FPNV Positioning Matrix is pivotal in evaluating the Agricultural Biological Control Agents Market. It offers a comprehensive assessment of vendors, examining key metrics related to Business Strategy and Product Satisfaction. This in-depth analysis empowers users to make well-informed decisions aligned with their requirements. Based on the evaluation, the vendors are then categorized into four distinct quadrants representing varying levels of success: Forefront (F), Pathfinder (P), Niche (N), or Vital (V).

Market Share Analysis

The Market Share Analysis is a comprehensive tool that provides an insightful and in-depth examination of the current state of vendors in the Agricultural Biological Control Agents Market. By meticulously comparing and analyzing vendor contributions in terms of overall revenue, customer base, and other key metrics, we can offer companies a greater understanding of their performance and the challenges they face when competing for market share. Additionally, this analysis provides valuable insights into the competitive nature of the sector, including factors such as accumulation, fragmentation dominance, and amalgamation traits observed over the base year period studied. With this expanded level of detail, vendors can make more informed decisions and devise effective strategies to gain a competitive edge in the market.

Key Company Profiles

The report delves into recent significant developments in the Agricultural Biological Control Agents Market, highlighting leading vendors and their innovative profiles. These include AgBiTech Pty. Ltd., Andermatt Group AG, BASF SE, Bayer AG, Biocontrol Technologies SL, Bioline AgroSciences Ltd., BioWorks, Inc. by Biobest Group NV, Cearitis, Certis Biologicals by Mitsui & Co., Ltd., Corteva Agriscience, Dora Agri-Tech, Eco Bugs India Private Limited, FMC Corporation, IPL Biologicals Limited, Isagro S.p.A., Koppert Biological Systems, Manidharma Biotech Private Limited, Marrone Bio Innovations, Inc. by Bioceres Crop Solutions Corp., Novozymes A/S, Prakriti Biotech, Russell IPM Ltd., Shin-Etsu Chemical Co. Ltd., STK Bio-Ag Technologies, Suterra LLC by The Wonderful Company LLC, Syngenta Crop Protection AG, UPL Limited, Valent Biosciences LLC by Sumitomo Chemical Co., Ltd., and Vegalab SA.

Market Segmentation & Coverage

This research report categorizes the Agricultural Biological Control Agents Market to forecast the revenues and analyze trends in each of the following sub-markets:

- Product Type

- Bacteria

- Fungi

- Parasitoids

- Predators

- Weed Killers

- Type

- Biopesticides

- Biofungicides

- Bioherbicides

- Bioinsecticides

- Bionematicides

- Semiochemicals

- Allelochemicals

- Pheromones

- Biopesticides

- Crop Type

- Cereal & Grains

- Corn

- Rice

- Wheat

- Fruits & Vegetables

- Berries

- Citrus Fruits

- Leafy Vegetables

- Pome Fruits

- Root & Tuber Vegetables

- Oilseeds & Pulses

- Soybean

- Sunflower

- Cereal & Grains

- Application

- Foliar Spray

- Seed Treatment

- Soil Treatment

- End-User

- Commercial Scale Farming

- Individual Grower

- Region

- Americas

- Argentina

- Brazil

- Canada

- Mexico

- United States

- California

- Florida

- Illinois

- New York

- Ohio

- Pennsylvania

- Texas

- Asia-Pacific

- Australia

- China

- India

- Indonesia

- Japan

- Malaysia

- Philippines

- Singapore

- South Korea

- Taiwan

- Thailand

- Vietnam

- Europe, Middle East & Africa

- Denmark

- Egypt

- Finland

- France

- Germany

- Israel

- Italy

- Netherlands

- Nigeria

- Norway

- Poland

- Qatar

- Russia

- Saudi Arabia

- South Africa

- Spain

- Sweden

- Switzerland

- Turkey

- United Arab Emirates

- United Kingdom

- Americas

The report offers valuable insights on the following aspects:

1. Market Penetration: It presents comprehensive information on the market provided by key players.

2. Market Development: It delves deep into lucrative emerging markets and analyzes the penetration across mature market segments.

3. Market Diversification: It provides detailed information on new product launches, untapped geographic regions, recent developments, and investments.

4. Competitive Assessment & Intelligence: It conducts an exhaustive assessment of market shares, strategies, products, certifications, regulatory approvals, patent landscape, and manufacturing capabilities of the leading players.

5. Product Development & Innovation: It offers intelligent insights on future technologies, R&D activities, and breakthrough product developments.

The report addresses key questions such as:

1. What is the market size and forecast of the Agricultural Biological Control Agents Market?

2. Which products, segments, applications, and areas should one consider investing in over the forecast period in the Agricultural Biological Control Agents Market?

3. What are the technology trends and regulatory frameworks in the Agricultural Biological Control Agents Market?

4. What is the market share of the leading vendors in the Agricultural Biological Control Agents Market?

5. Which modes and strategic moves are suitable for entering the Agricultural Biological Control Agents Market?

Table of Contents

1. Preface

- 1.1. Objectives of the Study

- 1.2. Market Segmentation & Coverage

- 1.3. Years Considered for the Study

- 1.4. Currency & Pricing

- 1.5. Language

- 1.6. Limitations

- 1.7. Assumptions

- 1.8. Stakeholders

2. Research Methodology

- 2.1. Define: Research Objective

- 2.2. Determine: Research Design

- 2.3. Prepare: Research Instrument

- 2.4. Collect: Data Source

- 2.5. Analyze: Data Interpretation

- 2.6. Formulate: Data Verification

- 2.7. Publish: Research Report

- 2.8. Repeat: Report Update

3. Executive Summary

4. Market Overview

- 4.1. Introduction

- 4.2. Agricultural Biological Control Agents Market, by Region

5. Market Insights

- 5.1. Market Dynamics

- 5.1.1. Drivers

- 5.1.1.1. Growing concerns regarding the environmental impact associated with pesticide use

- 5.1.1.2. Government initiatives to improve pest management and promote adoption of biological control agents

- 5.1.1.3. Inclination towards organic agricultural commodities

- 5.1.2. Restraints

- 5.1.2.1. Concerns regarding the efficiency and effectiveness of biological control agents

- 5.1.3. Opportunities

- 5.1.3.1. Ongoing R&D for the development of efficient agricultural biological control agents

- 5.1.3.2. Regulatory approvals and release of biological control agents

- 5.1.4. Challenges

- 5.1.4.1. Concerns associated with resistance management and quality control

- 5.1.1. Drivers

- 5.2. Market Segmentation Analysis

- 5.2.1. Product: Bacteria-based agents are preferred in agricultural systems to minimizing environmental impact and promoting sustainable weed management

- 5.2.2. Type: Biopesticides are preferred choice due to their broader spectrum of action affecting a variety of pests

- 5.2.3. Crop Type: Inclination trend towards sustainable agriculture practices in broad-spectrum and specialized needs of varied crops, influences the kind of biological controls developed

- 5.2.4. Application: Seed treatments application is more suitable to protect plant from early stage of development

- 5.3. Market Trend Analysis

- 5.4. Cumulative Impact of High Inflation

- 5.5. Porter's Five Forces Analysis

- 5.5.1. Threat of New Entrants

- 5.5.2. Threat of Substitutes

- 5.5.3. Bargaining Power of Customers

- 5.5.4. Bargaining Power of Suppliers

- 5.5.5. Industry Rivalry

- 5.6. Value Chain & Critical Path Analysis

- 5.7. Regulatory Framework

6. Agricultural Biological Control Agents Market, by Product Type

- 6.1. Introduction

- 6.2. Bacteria

- 6.3. Fungi

- 6.4. Parasitoids

- 6.5. Predators

- 6.6. Weed Killers

7. Agricultural Biological Control Agents Market, by Type

- 7.1. Introduction

- 7.2. Biopesticides

- 7.3.1. Biofungicides

- 7.3.2. Bioherbicides

- 7.3.3. Bioinsecticides

- 7.3.4. Bionematicides

- 7.3. Semiochemicals

- 7.4.1. Allelochemicals

- 7.4.2. Pheromones

8. Agricultural Biological Control Agents Market, by Crop Type

- 8.1. Introduction

- 8.2. Cereal & Grains

- 8.3.1. Corn

- 8.3.2. Rice

- 8.3.3. Wheat

- 8.3. Fruits & Vegetables

- 8.4.1. Berries

- 8.4.2. Citrus Fruits

- 8.4.3. Leafy Vegetables

- 8.4.4. Pome Fruits

- 8.4.5. Root & Tuber Vegetables

- 8.4. Oilseeds & Pulses

- 8.5.1. Soybean

- 8.5.2. Sunflower

9. Agricultural Biological Control Agents Market, by Application

- 9.1. Introduction

- 9.2. Foliar Spray

- 9.3. Seed Treatment

- 9.4. Soil Treatment

10. Agricultural Biological Control Agents Market, by End-User

- 10.1. Introduction

- 10.2. Commercial Scale Farming

- 10.3. Individual Grower

11. Americas Agricultural Biological Control Agents Market

- 11.1. Introduction

- 11.2. Argentina

- 11.3. Brazil

- 11.4. Canada

- 11.5. Mexico

- 11.6. United States

12. Asia-Pacific Agricultural Biological Control Agents Market

- 12.1. Introduction

- 12.2. Australia

- 12.3. China

- 12.4. India

- 12.5. Indonesia

- 12.6. Japan

- 12.7. Malaysia

- 12.8. Philippines

- 12.9. Singapore

- 12.10. South Korea

- 12.11. Taiwan

- 12.12. Thailand

- 12.13. Vietnam

13. Europe, Middle East & Africa Agricultural Biological Control Agents Market

- 13.1. Introduction

- 13.2. Denmark

- 13.3. Egypt

- 13.4. Finland

- 13.5. France

- 13.6. Germany

- 13.7. Israel

- 13.8. Italy

- 13.9. Netherlands

- 13.10. Nigeria

- 13.11. Norway

- 13.12. Poland

- 13.13. Qatar

- 13.14. Russia

- 13.15. Saudi Arabia

- 13.16. South Africa

- 13.17. Spain

- 13.18. Sweden

- 13.19. Switzerland

- 13.20. Turkey

- 13.21. United Arab Emirates

- 13.22. United Kingdom

14. Competitive Landscape

- 14.1. FPNV Positioning Matrix

- 14.2. Market Share Analysis, By Key Player

- 14.3. Competitive Scenario Analysis, By Key Player

- 14.3.1. New Product Launch & Enhancement

- 14.3.1.1. Syngenta Launches A New Biopesticide CERTANO in Brazil for Sugarcane

- 14.3.1.2. Croda's First Product Launch Specifically Focusing On The Biopesticide Market

- 14.3.2. Investment & Funding

- 14.3.2.1. Innatrix Raising Funds With Goal of Launching Its First Biopesticide in 2026

- 14.3.1. New Product Launch & Enhancement

15. Competitive Portfolio

- 15.1. Key Company Profiles

- 15.1.1. AgBiTech Pty. Ltd.

- 15.1.2. Andermatt Group AG

- 15.1.3. BASF SE

- 15.1.4. Bayer AG

- 15.1.5. Biocontrol Technologies SL

- 15.1.6. Bioline AgroSciences Ltd.

- 15.1.7. BioWorks, Inc. by Biobest Group NV

- 15.1.8. Cearitis

- 15.1.9. Certis Biologicals by Mitsui & Co., Ltd.

- 15.1.10. Corteva Agriscience

- 15.1.11. Dora Agri-Tech

- 15.1.12. Eco Bugs India Private Limited

- 15.1.13. FMC Corporation

- 15.1.14. IPL Biologicals Limited

- 15.1.15. Isagro S.p.A.

- 15.1.16. Koppert Biological Systems

- 15.1.17. Manidharma Biotech Private Limited

- 15.1.18. Marrone Bio Innovations, Inc. by Bioceres Crop Solutions Corp.

- 15.1.19. Novozymes A/S

- 15.1.20. Prakriti Biotech

- 15.1.21. Russell IPM Ltd.

- 15.1.22. Shin-Etsu Chemical Co. Ltd.

- 15.1.23. STK Bio-Ag Technologies

- 15.1.24. Suterra LLC by The Wonderful Company LLC

- 15.1.25. Syngenta Crop Protection AG

- 15.1.26. UPL Limited

- 15.1.27. Valent Biosciences LLC by Sumitomo Chemical Co., Ltd.

- 15.1.28. Vegalab SA

- 15.2. Key Product Portfolio

16. Appendix

- 16.1. Discussion Guide

- 16.2. License & Pricing

LIST OF FIGURES

- FIGURE 1. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET RESEARCH PROCESS

- FIGURE 2. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, 2023 VS 2030

- FIGURE 3. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, 2018-2030 (USD MILLION)

- FIGURE 4. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY REGION, 2023 VS 2030 (%)

- FIGURE 5. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY REGION, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 6. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET DYNAMICS

- FIGURE 7. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PRODUCT TYPE, 2023 VS 2030 (%)

- FIGURE 8. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PRODUCT TYPE, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 9. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY TYPE, 2023 VS 2030 (%)

- FIGURE 10. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY TYPE, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 11. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CROP TYPE, 2023 VS 2030 (%)

- FIGURE 12. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CROP TYPE, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 13. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY APPLICATION, 2023 VS 2030 (%)

- FIGURE 14. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY APPLICATION, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 15. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY END-USER, 2023 VS 2030 (%)

- FIGURE 16. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY END-USER, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 17. AMERICAS AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY COUNTRY, 2023 VS 2030 (%)

- FIGURE 18. AMERICAS AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY COUNTRY, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 19. UNITED STATES AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY STATE, 2023 VS 2030 (%)

- FIGURE 20. UNITED STATES AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY STATE, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 21. ASIA-PACIFIC AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY COUNTRY, 2023 VS 2030 (%)

- FIGURE 22. ASIA-PACIFIC AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY COUNTRY, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 23. EUROPE, MIDDLE EAST & AFRICA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY COUNTRY, 2023 VS 2030 (%)

- FIGURE 24. EUROPE, MIDDLE EAST & AFRICA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY COUNTRY, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 25. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET, FPNV POSITIONING MATRIX, 2023

- FIGURE 26. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SHARE, BY KEY PLAYER, 2023

LIST OF TABLES

- TABLE 1. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SEGMENTATION & COVERAGE

- TABLE 2. UNITED STATES DOLLAR EXCHANGE RATE, 2018-2023

- TABLE 3. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, 2018-2030 (USD MILLION)

- TABLE 4. GLOBAL AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY REGION, 2018-2030 (USD MILLION)

- TABLE 5. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PRODUCT TYPE, 2018-2030 (USD MILLION)

- TABLE 6. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BACTERIA, BY REGION, 2018-2030 (USD MILLION)

- TABLE 7. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY FUNGI, BY REGION, 2018-2030 (USD MILLION)

- TABLE 8. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PARASITOIDS, BY REGION, 2018-2030 (USD MILLION)

- TABLE 9. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PREDATORS, BY REGION, 2018-2030 (USD MILLION)

- TABLE 10. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY WEED KILLERS, BY REGION, 2018-2030 (USD MILLION)

- TABLE 11. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 12. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOPESTICIDES, BY REGION, 2018-2030 (USD MILLION)

- TABLE 13. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOPESTICIDES, 2018-2030 (USD MILLION)

- TABLE 14. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOFUNGICIDES, BY REGION, 2018-2030 (USD MILLION)

- TABLE 15. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOHERBICIDES, BY REGION, 2018-2030 (USD MILLION)

- TABLE 16. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOINSECTICIDES, BY REGION, 2018-2030 (USD MILLION)

- TABLE 17. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIONEMATICIDES, BY REGION, 2018-2030 (USD MILLION)

- TABLE 18. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SEMIOCHEMICALS, BY REGION, 2018-2030 (USD MILLION)

- TABLE 19. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SEMIOCHEMICALS, 2018-2030 (USD MILLION)

- TABLE 20. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY ALLELOCHEMICALS, BY REGION, 2018-2030 (USD MILLION)

- TABLE 21. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PHEROMONES, BY REGION, 2018-2030 (USD MILLION)

- TABLE 22. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CROP TYPE, 2018-2030 (USD MILLION)

- TABLE 23. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CEREAL & GRAINS, BY REGION, 2018-2030 (USD MILLION)

- TABLE 24. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CEREAL & GRAINS, 2018-2030 (USD MILLION)

- TABLE 25. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CORN, BY REGION, 2018-2030 (USD MILLION)

- TABLE 26. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY RICE, BY REGION, 2018-2030 (USD MILLION)

- TABLE 27. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY WHEAT, BY REGION, 2018-2030 (USD MILLION)

- TABLE 28. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY FRUITS & VEGETABLES, BY REGION, 2018-2030 (USD MILLION)

- TABLE 29. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY FRUITS & VEGETABLES, 2018-2030 (USD MILLION)

- TABLE 30. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BERRIES, BY REGION, 2018-2030 (USD MILLION)

- TABLE 31. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CITRUS FRUITS, BY REGION, 2018-2030 (USD MILLION)

- TABLE 32. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY LEAFY VEGETABLES, BY REGION, 2018-2030 (USD MILLION)

- TABLE 33. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY POME FRUITS, BY REGION, 2018-2030 (USD MILLION)

- TABLE 34. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY ROOT & TUBER VEGETABLES, BY REGION, 2018-2030 (USD MILLION)

- TABLE 35. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY OILSEEDS & PULSES, BY REGION, 2018-2030 (USD MILLION)

- TABLE 36. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY OILSEEDS & PULSES, 2018-2030 (USD MILLION)

- TABLE 37. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SOYBEAN, BY REGION, 2018-2030 (USD MILLION)

- TABLE 38. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SUNFLOWER, BY REGION, 2018-2030 (USD MILLION)

- TABLE 39. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 40. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY FOLIAR SPRAY, BY REGION, 2018-2030 (USD MILLION)

- TABLE 41. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SEED TREATMENT, BY REGION, 2018-2030 (USD MILLION)

- TABLE 42. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SOIL TREATMENT, BY REGION, 2018-2030 (USD MILLION)

- TABLE 43. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 44. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY COMMERCIAL SCALE FARMING, BY REGION, 2018-2030 (USD MILLION)

- TABLE 45. AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY INDIVIDUAL GROWER, BY REGION, 2018-2030 (USD MILLION)

- TABLE 46. AMERICAS AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PRODUCT TYPE, 2018-2030 (USD MILLION)

- TABLE 47. AMERICAS AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 48. AMERICAS AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOPESTICIDES, 2018-2030 (USD MILLION)

- TABLE 49. AMERICAS AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SEMIOCHEMICALS, 2018-2030 (USD MILLION)

- TABLE 50. AMERICAS AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CROP TYPE, 2018-2030 (USD MILLION)

- TABLE 51. AMERICAS AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CEREAL & GRAINS, 2018-2030 (USD MILLION)

- TABLE 52. AMERICAS AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY FRUITS & VEGETABLES, 2018-2030 (USD MILLION)

- TABLE 53. AMERICAS AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY OILSEEDS & PULSES, 2018-2030 (USD MILLION)

- TABLE 54. AMERICAS AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 55. AMERICAS AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 56. AMERICAS AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY COUNTRY, 2018-2030 (USD MILLION)

- TABLE 57. ARGENTINA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PRODUCT TYPE, 2018-2030 (USD MILLION)

- TABLE 58. ARGENTINA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 59. ARGENTINA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOPESTICIDES, 2018-2030 (USD MILLION)

- TABLE 60. ARGENTINA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SEMIOCHEMICALS, 2018-2030 (USD MILLION)

- TABLE 61. ARGENTINA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CROP TYPE, 2018-2030 (USD MILLION)

- TABLE 62. ARGENTINA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CEREAL & GRAINS, 2018-2030 (USD MILLION)

- TABLE 63. ARGENTINA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY FRUITS & VEGETABLES, 2018-2030 (USD MILLION)

- TABLE 64. ARGENTINA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY OILSEEDS & PULSES, 2018-2030 (USD MILLION)

- TABLE 65. ARGENTINA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 66. ARGENTINA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 67. BRAZIL AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PRODUCT TYPE, 2018-2030 (USD MILLION)

- TABLE 68. BRAZIL AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 69. BRAZIL AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOPESTICIDES, 2018-2030 (USD MILLION)

- TABLE 70. BRAZIL AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SEMIOCHEMICALS, 2018-2030 (USD MILLION)

- TABLE 71. BRAZIL AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CROP TYPE, 2018-2030 (USD MILLION)

- TABLE 72. BRAZIL AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CEREAL & GRAINS, 2018-2030 (USD MILLION)

- TABLE 73. BRAZIL AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY FRUITS & VEGETABLES, 2018-2030 (USD MILLION)

- TABLE 74. BRAZIL AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY OILSEEDS & PULSES, 2018-2030 (USD MILLION)

- TABLE 75. BRAZIL AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 76. BRAZIL AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 77. CANADA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PRODUCT TYPE, 2018-2030 (USD MILLION)

- TABLE 78. CANADA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 79. CANADA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOPESTICIDES, 2018-2030 (USD MILLION)

- TABLE 80. CANADA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SEMIOCHEMICALS, 2018-2030 (USD MILLION)

- TABLE 81. CANADA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CROP TYPE, 2018-2030 (USD MILLION)

- TABLE 82. CANADA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CEREAL & GRAINS, 2018-2030 (USD MILLION)

- TABLE 83. CANADA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY FRUITS & VEGETABLES, 2018-2030 (USD MILLION)

- TABLE 84. CANADA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY OILSEEDS & PULSES, 2018-2030 (USD MILLION)

- TABLE 85. CANADA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 86. CANADA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 87. MEXICO AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PRODUCT TYPE, 2018-2030 (USD MILLION)

- TABLE 88. MEXICO AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 89. MEXICO AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOPESTICIDES, 2018-2030 (USD MILLION)

- TABLE 90. MEXICO AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SEMIOCHEMICALS, 2018-2030 (USD MILLION)

- TABLE 91. MEXICO AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CROP TYPE, 2018-2030 (USD MILLION)

- TABLE 92. MEXICO AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CEREAL & GRAINS, 2018-2030 (USD MILLION)

- TABLE 93. MEXICO AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY FRUITS & VEGETABLES, 2018-2030 (USD MILLION)

- TABLE 94. MEXICO AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY OILSEEDS & PULSES, 2018-2030 (USD MILLION)

- TABLE 95. MEXICO AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 96. MEXICO AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 97. UNITED STATES AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PRODUCT TYPE, 2018-2030 (USD MILLION)

- TABLE 98. UNITED STATES AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 99. UNITED STATES AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOPESTICIDES, 2018-2030 (USD MILLION)

- TABLE 100. UNITED STATES AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SEMIOCHEMICALS, 2018-2030 (USD MILLION)

- TABLE 101. UNITED STATES AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CROP TYPE, 2018-2030 (USD MILLION)

- TABLE 102. UNITED STATES AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CEREAL & GRAINS, 2018-2030 (USD MILLION)

- TABLE 103. UNITED STATES AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY FRUITS & VEGETABLES, 2018-2030 (USD MILLION)

- TABLE 104. UNITED STATES AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY OILSEEDS & PULSES, 2018-2030 (USD MILLION)

- TABLE 105. UNITED STATES AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 106. UNITED STATES AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 107. UNITED STATES AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY STATE, 2018-2030 (USD MILLION)

- TABLE 108. ASIA-PACIFIC AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PRODUCT TYPE, 2018-2030 (USD MILLION)

- TABLE 109. ASIA-PACIFIC AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 110. ASIA-PACIFIC AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOPESTICIDES, 2018-2030 (USD MILLION)

- TABLE 111. ASIA-PACIFIC AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SEMIOCHEMICALS, 2018-2030 (USD MILLION)

- TABLE 112. ASIA-PACIFIC AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CROP TYPE, 2018-2030 (USD MILLION)

- TABLE 113. ASIA-PACIFIC AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CEREAL & GRAINS, 2018-2030 (USD MILLION)

- TABLE 114. ASIA-PACIFIC AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY FRUITS & VEGETABLES, 2018-2030 (USD MILLION)

- TABLE 115. ASIA-PACIFIC AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY OILSEEDS & PULSES, 2018-2030 (USD MILLION)

- TABLE 116. ASIA-PACIFIC AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 117. ASIA-PACIFIC AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 118. ASIA-PACIFIC AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY COUNTRY, 2018-2030 (USD MILLION)

- TABLE 119. AUSTRALIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PRODUCT TYPE, 2018-2030 (USD MILLION)

- TABLE 120. AUSTRALIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 121. AUSTRALIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOPESTICIDES, 2018-2030 (USD MILLION)

- TABLE 122. AUSTRALIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SEMIOCHEMICALS, 2018-2030 (USD MILLION)

- TABLE 123. AUSTRALIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CROP TYPE, 2018-2030 (USD MILLION)

- TABLE 124. AUSTRALIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CEREAL & GRAINS, 2018-2030 (USD MILLION)

- TABLE 125. AUSTRALIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY FRUITS & VEGETABLES, 2018-2030 (USD MILLION)

- TABLE 126. AUSTRALIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY OILSEEDS & PULSES, 2018-2030 (USD MILLION)

- TABLE 127. AUSTRALIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 128. AUSTRALIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 129. CHINA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PRODUCT TYPE, 2018-2030 (USD MILLION)

- TABLE 130. CHINA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 131. CHINA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOPESTICIDES, 2018-2030 (USD MILLION)

- TABLE 132. CHINA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SEMIOCHEMICALS, 2018-2030 (USD MILLION)

- TABLE 133. CHINA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CROP TYPE, 2018-2030 (USD MILLION)

- TABLE 134. CHINA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CEREAL & GRAINS, 2018-2030 (USD MILLION)

- TABLE 135. CHINA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY FRUITS & VEGETABLES, 2018-2030 (USD MILLION)

- TABLE 136. CHINA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY OILSEEDS & PULSES, 2018-2030 (USD MILLION)

- TABLE 137. CHINA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 138. CHINA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 139. INDIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PRODUCT TYPE, 2018-2030 (USD MILLION)

- TABLE 140. INDIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 141. INDIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOPESTICIDES, 2018-2030 (USD MILLION)

- TABLE 142. INDIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SEMIOCHEMICALS, 2018-2030 (USD MILLION)

- TABLE 143. INDIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CROP TYPE, 2018-2030 (USD MILLION)

- TABLE 144. INDIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CEREAL & GRAINS, 2018-2030 (USD MILLION)

- TABLE 145. INDIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY FRUITS & VEGETABLES, 2018-2030 (USD MILLION)

- TABLE 146. INDIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY OILSEEDS & PULSES, 2018-2030 (USD MILLION)

- TABLE 147. INDIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 148. INDIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 149. INDONESIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PRODUCT TYPE, 2018-2030 (USD MILLION)

- TABLE 150. INDONESIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 151. INDONESIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOPESTICIDES, 2018-2030 (USD MILLION)

- TABLE 152. INDONESIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SEMIOCHEMICALS, 2018-2030 (USD MILLION)

- TABLE 153. INDONESIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CROP TYPE, 2018-2030 (USD MILLION)

- TABLE 154. INDONESIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CEREAL & GRAINS, 2018-2030 (USD MILLION)

- TABLE 155. INDONESIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY FRUITS & VEGETABLES, 2018-2030 (USD MILLION)

- TABLE 156. INDONESIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY OILSEEDS & PULSES, 2018-2030 (USD MILLION)

- TABLE 157. INDONESIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 158. INDONESIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 159. JAPAN AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PRODUCT TYPE, 2018-2030 (USD MILLION)

- TABLE 160. JAPAN AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 161. JAPAN AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOPESTICIDES, 2018-2030 (USD MILLION)

- TABLE 162. JAPAN AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SEMIOCHEMICALS, 2018-2030 (USD MILLION)

- TABLE 163. JAPAN AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CROP TYPE, 2018-2030 (USD MILLION)

- TABLE 164. JAPAN AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CEREAL & GRAINS, 2018-2030 (USD MILLION)

- TABLE 165. JAPAN AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY FRUITS & VEGETABLES, 2018-2030 (USD MILLION)

- TABLE 166. JAPAN AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY OILSEEDS & PULSES, 2018-2030 (USD MILLION)

- TABLE 167. JAPAN AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 168. JAPAN AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 169. MALAYSIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PRODUCT TYPE, 2018-2030 (USD MILLION)

- TABLE 170. MALAYSIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 171. MALAYSIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOPESTICIDES, 2018-2030 (USD MILLION)

- TABLE 172. MALAYSIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SEMIOCHEMICALS, 2018-2030 (USD MILLION)

- TABLE 173. MALAYSIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CROP TYPE, 2018-2030 (USD MILLION)

- TABLE 174. MALAYSIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CEREAL & GRAINS, 2018-2030 (USD MILLION)

- TABLE 175. MALAYSIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY FRUITS & VEGETABLES, 2018-2030 (USD MILLION)

- TABLE 176. MALAYSIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY OILSEEDS & PULSES, 2018-2030 (USD MILLION)

- TABLE 177. MALAYSIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 178. MALAYSIA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 179. PHILIPPINES AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PRODUCT TYPE, 2018-2030 (USD MILLION)

- TABLE 180. PHILIPPINES AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 181. PHILIPPINES AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOPESTICIDES, 2018-2030 (USD MILLION)

- TABLE 182. PHILIPPINES AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SEMIOCHEMICALS, 2018-2030 (USD MILLION)

- TABLE 183. PHILIPPINES AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CROP TYPE, 2018-2030 (USD MILLION)

- TABLE 184. PHILIPPINES AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CEREAL & GRAINS, 2018-2030 (USD MILLION)

- TABLE 185. PHILIPPINES AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY FRUITS & VEGETABLES, 2018-2030 (USD MILLION)

- TABLE 186. PHILIPPINES AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY OILSEEDS & PULSES, 2018-2030 (USD MILLION)

- TABLE 187. PHILIPPINES AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 188. PHILIPPINES AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 189. SINGAPORE AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PRODUCT TYPE, 2018-2030 (USD MILLION)

- TABLE 190. SINGAPORE AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 191. SINGAPORE AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOPESTICIDES, 2018-2030 (USD MILLION)

- TABLE 192. SINGAPORE AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SEMIOCHEMICALS, 2018-2030 (USD MILLION)

- TABLE 193. SINGAPORE AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CROP TYPE, 2018-2030 (USD MILLION)

- TABLE 194. SINGAPORE AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CEREAL & GRAINS, 2018-2030 (USD MILLION)

- TABLE 195. SINGAPORE AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY FRUITS & VEGETABLES, 2018-2030 (USD MILLION)

- TABLE 196. SINGAPORE AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY OILSEEDS & PULSES, 2018-2030 (USD MILLION)

- TABLE 197. SINGAPORE AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 198. SINGAPORE AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 199. SOUTH KOREA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PRODUCT TYPE, 2018-2030 (USD MILLION)

- TABLE 200. SOUTH KOREA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 201. SOUTH KOREA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOPESTICIDES, 2018-2030 (USD MILLION)

- TABLE 202. SOUTH KOREA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SEMIOCHEMICALS, 2018-2030 (USD MILLION)

- TABLE 203. SOUTH KOREA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CROP TYPE, 2018-2030 (USD MILLION)

- TABLE 204. SOUTH KOREA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CEREAL & GRAINS, 2018-2030 (USD MILLION)

- TABLE 205. SOUTH KOREA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY FRUITS & VEGETABLES, 2018-2030 (USD MILLION)

- TABLE 206. SOUTH KOREA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY OILSEEDS & PULSES, 2018-2030 (USD MILLION)

- TABLE 207. SOUTH KOREA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 208. SOUTH KOREA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 209. TAIWAN AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PRODUCT TYPE, 2018-2030 (USD MILLION)

- TABLE 210. TAIWAN AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 211. TAIWAN AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOPESTICIDES, 2018-2030 (USD MILLION)

- TABLE 212. TAIWAN AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SEMIOCHEMICALS, 2018-2030 (USD MILLION)

- TABLE 213. TAIWAN AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CROP TYPE, 2018-2030 (USD MILLION)

- TABLE 214. TAIWAN AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CEREAL & GRAINS, 2018-2030 (USD MILLION)

- TABLE 215. TAIWAN AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY FRUITS & VEGETABLES, 2018-2030 (USD MILLION)

- TABLE 216. TAIWAN AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY OILSEEDS & PULSES, 2018-2030 (USD MILLION)

- TABLE 217. TAIWAN AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 218. TAIWAN AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 219. THAILAND AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PRODUCT TYPE, 2018-2030 (USD MILLION)

- TABLE 220. THAILAND AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 221. THAILAND AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOPESTICIDES, 2018-2030 (USD MILLION)

- TABLE 222. THAILAND AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SEMIOCHEMICALS, 2018-2030 (USD MILLION)

- TABLE 223. THAILAND AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CROP TYPE, 2018-2030 (USD MILLION)

- TABLE 224. THAILAND AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CEREAL & GRAINS, 2018-2030 (USD MILLION)

- TABLE 225. THAILAND AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY FRUITS & VEGETABLES, 2018-2030 (USD MILLION)

- TABLE 226. THAILAND AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY OILSEEDS & PULSES, 2018-2030 (USD MILLION)

- TABLE 227. THAILAND AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 228. THAILAND AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 229. VIETNAM AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PRODUCT TYPE, 2018-2030 (USD MILLION)

- TABLE 230. VIETNAM AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 231. VIETNAM AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOPESTICIDES, 2018-2030 (USD MILLION)

- TABLE 232. VIETNAM AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SEMIOCHEMICALS, 2018-2030 (USD MILLION)

- TABLE 233. VIETNAM AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CROP TYPE, 2018-2030 (USD MILLION)

- TABLE 234. VIETNAM AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CEREAL & GRAINS, 2018-2030 (USD MILLION)

- TABLE 235. VIETNAM AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY FRUITS & VEGETABLES, 2018-2030 (USD MILLION)

- TABLE 236. VIETNAM AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY OILSEEDS & PULSES, 2018-2030 (USD MILLION)

- TABLE 237. VIETNAM AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 238. VIETNAM AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 239. EUROPE, MIDDLE EAST & AFRICA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PRODUCT TYPE, 2018-2030 (USD MILLION)

- TABLE 240. EUROPE, MIDDLE EAST & AFRICA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 241. EUROPE, MIDDLE EAST & AFRICA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOPESTICIDES, 2018-2030 (USD MILLION)

- TABLE 242. EUROPE, MIDDLE EAST & AFRICA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SEMIOCHEMICALS, 2018-2030 (USD MILLION)

- TABLE 243. EUROPE, MIDDLE EAST & AFRICA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CROP TYPE, 2018-2030 (USD MILLION)

- TABLE 244. EUROPE, MIDDLE EAST & AFRICA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CEREAL & GRAINS, 2018-2030 (USD MILLION)

- TABLE 245. EUROPE, MIDDLE EAST & AFRICA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY FRUITS & VEGETABLES, 2018-2030 (USD MILLION)

- TABLE 246. EUROPE, MIDDLE EAST & AFRICA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY OILSEEDS & PULSES, 2018-2030 (USD MILLION)

- TABLE 247. EUROPE, MIDDLE EAST & AFRICA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 248. EUROPE, MIDDLE EAST & AFRICA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 249. EUROPE, MIDDLE EAST & AFRICA AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY COUNTRY, 2018-2030 (USD MILLION)

- TABLE 250. DENMARK AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PRODUCT TYPE, 2018-2030 (USD MILLION)

- TABLE 251. DENMARK AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 252. DENMARK AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOPESTICIDES, 2018-2030 (USD MILLION)

- TABLE 253. DENMARK AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SEMIOCHEMICALS, 2018-2030 (USD MILLION)

- TABLE 254. DENMARK AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CROP TYPE, 2018-2030 (USD MILLION)

- TABLE 255. DENMARK AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CEREAL & GRAINS, 2018-2030 (USD MILLION)

- TABLE 256. DENMARK AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY FRUITS & VEGETABLES, 2018-2030 (USD MILLION)

- TABLE 257. DENMARK AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY OILSEEDS & PULSES, 2018-2030 (USD MILLION)

- TABLE 258. DENMARK AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 259. DENMARK AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 260. EGYPT AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PRODUCT TYPE, 2018-2030 (USD MILLION)

- TABLE 261. EGYPT AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 262. EGYPT AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOPESTICIDES, 2018-2030 (USD MILLION)

- TABLE 263. EGYPT AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SEMIOCHEMICALS, 2018-2030 (USD MILLION)

- TABLE 264. EGYPT AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CROP TYPE, 2018-2030 (USD MILLION)

- TABLE 265. EGYPT AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CEREAL & GRAINS, 2018-2030 (USD MILLION)

- TABLE 266. EGYPT AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY FRUITS & VEGETABLES, 2018-2030 (USD MILLION)

- TABLE 267. EGYPT AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY OILSEEDS & PULSES, 2018-2030 (USD MILLION)

- TABLE 268. EGYPT AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 269. EGYPT AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 270. FINLAND AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PRODUCT TYPE, 2018-2030 (USD MILLION)

- TABLE 271. FINLAND AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 272. FINLAND AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOPESTICIDES, 2018-2030 (USD MILLION)

- TABLE 273. FINLAND AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SEMIOCHEMICALS, 2018-2030 (USD MILLION)

- TABLE 274. FINLAND AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CROP TYPE, 2018-2030 (USD MILLION)

- TABLE 275. FINLAND AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CEREAL & GRAINS, 2018-2030 (USD MILLION)

- TABLE 276. FINLAND AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY FRUITS & VEGETABLES, 2018-2030 (USD MILLION)

- TABLE 277. FINLAND AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY OILSEEDS & PULSES, 2018-2030 (USD MILLION)

- TABLE 278. FINLAND AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 279. FINLAND AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 280. FRANCE AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PRODUCT TYPE, 2018-2030 (USD MILLION)

- TABLE 281. FRANCE AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 282. FRANCE AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY BIOPESTICIDES, 2018-2030 (USD MILLION)

- TABLE 283. FRANCE AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY SEMIOCHEMICALS, 2018-2030 (USD MILLION)

- TABLE 284. FRANCE AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CROP TYPE, 2018-2030 (USD MILLION)

- TABLE 285. FRANCE AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY CEREAL & GRAINS, 2018-2030 (USD MILLION)

- TABLE 286. FRANCE AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY FRUITS & VEGETABLES, 2018-2030 (USD MILLION)

- TABLE 287. FRANCE AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY OILSEEDS & PULSES, 2018-2030 (USD MILLION)

- TABLE 288. FRANCE AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 289. FRANCE AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY END-USER, 2018-2030 (USD MILLION)

- TABLE 290. GERMANY AGRICULTURAL BIOLOGICAL CONTROL AGENTS MARKET SIZE, BY PRODUCT TYPE, 2018-2030 (USD MILLION)

- TABLE 291. GERMANY AGRICULTURAL BIOLOGICAL CON

生物防治市场,按来源、按作物类型、按类型、按应用、按最终用户、按国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

生物防治市场,按来源、按作物类型、按类型、按应用、按最终用户、按国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测 生物作物保护 (生物农药) 的全球市场:市场占有率及排行榜·整体销售额及需求预测 (2024-2030年)

生物作物保护 (生物农药) 的全球市场:市场占有率及排行榜·整体销售额及需求预测 (2024-2030年) 2024-2032 年生物农药市场报告(依产品、配方、来源、应用方式、作物类型和地区)

2024-2032 年生物农药市场报告(依产品、配方、来源、应用方式、作物类型和地区) 2023-2030 年全球生物农药市场规模研究与预测(按配方、类型、来源、作物类型、应用和区域分析)

2023-2030 年全球生物农药市场规模研究与预测(按配方、类型、来源、作物类型、应用和区域分析) 生物农药:市场占有率分析、产业趋势与统计、成长预测(2024-2029)

生物农药:市场占有率分析、产业趋势与统计、成长预测(2024-2029) 生物防治 - 市场占有率分析、产业趋势与统计、成长预测(2024 - 2029)

生物防治 - 市场占有率分析、产业趋势与统计、成长预测(2024 - 2029) 全球生物杀虫剂市场 - 2023-20230

全球生物杀虫剂市场 - 2023-20230 生物农药市场报告:2030 年趋势、预测与竞争分析

生物农药市场报告:2030 年趋势、预测与竞争分析 2024 年生物防治全球市场报告

2024 年生物防治全球市场报告 生物防治剂市场:依活性物质、作物类型、害虫防治目标、应用划分 - 2024-2030 年全球预测

生物防治剂市场:依活性物质、作物类型、害虫防治目标、应用划分 - 2024-2030 年全球预测