|

市场调查报告书

商品编码

1881237

全球电动两轮车市场(至2032年):按车辆类型(电动Scooter/电动轻型轻型机踏车/电动机车)、电压、马达类型(轮毂马达/中置马达)、电池(锂离子电池/铅酸电池)、马达功率、技术(电池供电/插电式)、车辆等级、应用和地区划分Electric Two Wheeler Market by Vehicle (E-Scooter/Moped, E-Motorcycle), Voltage Type, Motor Type (Hub, Mid-drive), Battery (Li-ion, lead acid), Motor Power, Technology (Battery, Plug-in), Vehicle Class, Usage, Region - Global Forecast to 2032 |

||||||

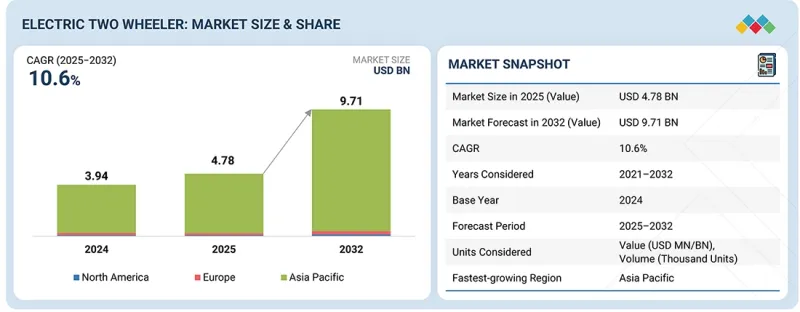

预计电动摩托车市场将从 2025 年的 47.8 亿美元成长到 2032 年的 97.1 亿美元,复合年增长率为 10.6%。

在印度和东南亚,大众市场的Scooter正在使用本地生产的电池组组装和电芯到电池包 (CTP) 设计来提高每千瓦时的成本效率。

| 调查范围 | |

|---|---|

| 调查期 | 2021-2032 |

| 基准年 | 2024 |

| 预测期 | 2025-2032 |

| 单元 | 数量(单位)和金额(美元) |

| 部分 | 车辆类型、马达功率、马达类型、电池、应用、技术、电压、里程、车辆等级、地区 |

| 目标区域 | 亚太地区、欧洲、北美 |

共享旅游和配送业者正在向原始设备製造商 (OEM) 提供即时使用数据,从而影响下一代车辆的设计,使其更加重视耐用性、耐热性和易于维护。电动两轮车的设计如今着重于持续动力输出,而非短时加速,这体现了向持续性能优化的转变。因此,竞争差异化正从机械硬体转向智慧系统,例如骑乘模式、牵引力控制演算法和能量管理软体。

“预计在预测期内,轮毂式马达将主导市场。”

由于其设计简单、维护成本低,轮毂式马达有望主导电动摩托车市场。轮毂马达直接整合在轮毂内,无需链条、皮带和变速箱,从而降低了机械复杂性、重量和维护成本。其紧凑的设计使得车辆更轻、更符合人体工学——这对都市区通勤者和配送车队而言是一项关键优势。轮毂式马达还提供高效的能量回收煞车和更高的能量利用率,从而提升续航里程和整体驾驶效率。电池价格的下降和能量密度的提高使得配备轮毂式马达的车辆生产成本更低,也更容易实现大规模量产。共享出行和车队营运日益重要,进一步推动了轮轮毂式马达的普及,因为可靠性和低维护成本比追求极致性能更为重要。顺应全球城市电气化的趋势,轮毂式马达架构为原始设备製造商 (OEM) 提供了成本、简易性和扩充性之间的最佳平衡。 2025 年 8 月,Ola Electric(印度)推出了一款自主研发的轮毂式马达,该电机采用铁氧体(不含稀土元素)磁铁,从而降低了对进口稀土元素材料的依赖,并增强了其本地製造能力。

“预计在预测期内,商业领域的成长率将最高。”

电动Scooter和电动机车的商业用途,包括送货车辆、共享出行服务和最后一公里物流,预计将迎来最高的成长率,因为营运商正致力于降低生命週期成本、提高营运效率并确保车辆快速週转。与内燃机车型相比,电动摩托车在燃料和维护成本方面可显着节省,使其成为高运转率车队的理想选择。随着电子商务和外送配送的快速发展,许多公司正在将其整个车队电气化,以实现永续性目标并遵守更严格的都市区排放法规。这些商业营运已建立了可预测的路线和使用模式,使得电动车的大规模部署和资金筹措更加便利。为此,原始设备製造商 (OEM) 正在开发具备载货能力的重型电动Scooter和摩托车,并配备电池更换系统和专为车队营运设计的专用充电网路。

“亚太地区将主要由印度驱动”

印度庞大的两轮车市场,在强劲的更换需求和快速的都市化进程的推动下,为亚太地区Scooter和摩托车行业的电动化提供了极其有利的环境。政府的各项倡议,例如FAME II计划、邦级补贴以及到2030年实现30%电动车普及率的国家目标,都显着降低了前期成本,加速了电动两轮车的普及。锂离子电池价格的持续下降,进一步提升了电动两轮车相对于内燃机车型的成本竞争力。包括Ola Electric、Ather Energy和Hero MotoCorp在内的主要本土汽车製造商以及新兴企业,正在积极拓展其电动车产品线,同时加强在地化生产、分销和服务网路。印度拥挤的城市交通、较短的通勤时间和高昂的燃油价格,也使得电动两轮车从整体拥有成本的角度来看极具吸引力。这项向电动化的转型符合印度的环境和能源安全目标,并受到市场趋势、政策方向和消费者需求的共同驱动。受此发展势头推动,预计到 2024 财年,印度电动两轮车的销量将达到约 115 万辆。基础建设也在稳步推进,例如 Ather Energy 等公司计划在 2026 年 3 月将其零售店数量翻一番,达到全国 700 家。

本报告调查了全球电动摩托车市场,并提供了市场概况、影响市场成长的各种因素分析、技术和专利趋势、法律制度、案例研究、市场规模趋势和预测、按各个细分市场、地区/主要国家进行的详细分析、竞争格局以及主要企业的概况。

目录

第一章 引言

第二章调查方法

第三章执行摘要

第四章重要考察

第五章 市场概览

- 市场动态

- 司机

- 抑制因素

- 机会

- 任务

- 未满足的需求和閒置频段

- 与相关市场和不同产业相关的跨领域机会

- 一级/二级/三级公司的策略性倡议

- 专利分析

- 生成式人工智慧将如何影响电动摩托车市场

- 电动摩托车声学车辆警示系统(AVAS)

- 电动摩托车市场的新经营模式

- 关键新兴技术

- 互补技术

- 技术/产品蓝图

- 材料清单

- 总拥有成本

- OEM分析

- 电动摩托车生态系中的未来应用

- 总体经济指标

- 影响您业务的趋势/颠覆性因素

- 定价分析

- 生态系分析

- 供应链分析

- 案例研究分析

- 投资和资金筹措方案

- 贸易分析

- 2025-2026 年重要会议与活动

- 决策流程

- 相关利益者和采购标准

- 招募障碍和内部挑战

- 监管状况和合规性

- 对永续性的承诺

第六章 依车辆类型分類的电动摩托车市场

- 电动Scooter/轻型机踏车

- 电动机车

- 关键见解

第七章 按车辆类型分類的电动摩托车市场

- 经济

- 奢华

- 关键见解

第八章 按电压类型分類的电动摩托车市场

- 36V

- 48V

- 60V

- 72V

- 超过72伏

- 关键见解

第九章 电池驱动的电动摩托车市场

- 密闭式铅酸电池

- 锂离子

- 镍氢化物(NIMH)

- 钠离子

- 关键见解

第十章 按里程分類的电动摩托车市场

- 不到75英里

- 75至100英里

- 超过100英里

- 关键见解

第十一章 电动摩托车市场:依应用领域划分

- 个人

- 商业的

- 关键见解

第十二章 电动摩托车市场:依技术划分

- 外挂

- 电池

- 关键见解

第十三章 依电机类型分類的电动摩托车市场

- 中置马达

- 轮毂式马达

- 其他的

- 关键见解

第十四章 以马达输出功率分類的电动摩托车市场

- 小于1.5千瓦

- 1.5~3kW

- 3千瓦或以上

- 关键见解

第十五章 各地区的电动摩托车市场

- 亚太地区

- 宏观经济展望

- 中国

- 日本

- 印度

- 韩国

- 台湾

- 泰国

- 印尼

- 马来西亚

- 菲律宾

- 越南

- 欧洲

- 宏观经济展望

- 法国

- 德国

- 西班牙

- 奥地利

- 英国

- 义大利

- 比利时

- 荷兰

- 波兰

- 丹麦

- 北美洲

- 宏观经济展望

- 美国

- 加拿大

第十六章 竞争格局

- 概述

- 主要参与企业的策略/优势

- 电动摩托车供应商市场份额分析

- 收入分析

- 估值和财务指标

- 产品对比

- 企业估值矩阵

- Start-Ups/中小企业评估矩阵

- 竞争场景

第十七章:公司简介

- 主要企业

- OLA ELECTRIC

- BAJAJ AUTO LTD.

- TVS MOTOR COMPANY

- ATHER ENERGY

- YADEA TECHNOLOGY GROUP CO., LTD.

- HERO ELECTRIC

- GOGORO

- VMOTO LIMITED

- NIU INTERNATIONAL

- JIANGSU XINRI E-VEHICLE CO., LTD.

- IDEANOMICS, INC.

- ASKOLL EVA SPA

- 其他公司

- ULTRAVIOLETTE AUTOMOTIVE

- REVOLT INTELLICORP PRIVATE LIMITED(REVOLT MOTORS)

- Z ELECTRIC VEHICLE

- CAKE

- LIGHTNING MOTORCYCLES

- JOHAMMER E-MOBILITY GMBH

- PIAGGIO GROUP

- KTM AG

- HARLEY DAVIDSON

- BMW GROUP

- AIMA TECHNOLOGY GROUP CO., LTD.

- HONDA MOTOR CO., LTD.

- GREAVES ELECTRIC MOBILITY PRIVATE LIMITED(AMPERE VEHICLES)

- DONGGUAN TAILING ELECTRIC VEHICLE CO., LTD.

- CEZETA

- TERRA MOTORS CORPORATION

- NEXZU MOBILITY LTD.(AVAN MOTORS INDIA)

- EMFLUX MOTORS

- MAHINDRA & MAHINDRA LTD.

- DAMON MOTORS INC.

- VIAR MOTOR INDONESIA

- SELIS

- GESITS

- UNITED E-MOTOR

- SMOOT ELEKTRIK

- PT VOLTA INDONESIA SEMESTA(VOLTA)

- ALVA

- NUSA MOTORS

- BF GOODRICH

第十八章附录

The electric two wheeler market is projected to grow from USD 4.78 billion in 2025 to USD 9.71 billion by 2032 at a CAGR of 10.6%. In India and Southeast Asia, localized battery pack assembly and cell-to-pack (CTP) designs are being adopted to improve the cost-per-kWh efficiency of mass-market scooters.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Units Considered | Volume (Thousand Units) and Value (USD Million) |

| Segments | Vehicle type, Motor Power, Motor type, Battery Type, Usage, Technology Type, Voltage Type, Distance Covered, Vehicle Class, and Region |

| Regions covered | Asia Pacific, Europe, and North America |

Shared mobility and delivery operators are providing real-time usage data to OEMs, influencing next-generation vehicle designs focused on durability, thermal endurance, and ease of maintenance. Electric motorcycles are now being engineered for sustained power delivery rather than short bursts, reflecting a shift toward continuous performance optimization. As a result, competitive differentiation is moving from mechanical hardware to intelligent systems, including ride modes, traction control algorithms, and energy management software.

Hub motors are expected to dominate the electric two wheeler market during the forecast period.

Hub motors are expected to dominate the electric two wheeler market due to their simple construction and low maintenance requirements. Integrated directly into the wheel hub, they eliminate chains, belts, and gearboxes, reducing mechanical complexity, weight, and service costs. Their compact design enables lighter and more ergonomic vehicles to be an essential advantage for urban commuters and delivery fleets. Hub motors also provide efficient regenerative braking and improved energy utilization, enhancing range and overall ride efficiency. With battery prices declining and energy density improving, hub motor-based vehicles are becoming more cost-effective to produce and easier to scale for mass markets. The growing importance of shared mobility and fleet operations further supports hub motor adoption, as reliability and low upkeep outweigh the need for peak performance. Aligning with the global shift toward urban electrification, hub motor architecture offers OEMs an optimal balance of cost, simplicity, and scalability. In August 2025, Ola Electric (India) introduced an in-house hub motor utilizing ferrite (rare-earth-free) magnets, thereby reducing its dependence on imported rare-earth materials and strengthening local manufacturing capabilities.

The commercial usage segment is expected to grow at the fastest rate in the electric two wheeler market during the forecast period.

The commercial usage of electric scooters and motorcycles, including delivery fleets, ride-share services, and last-mile logistics, is expected to grow at the fastest rate in the electric two wheeler market as operators focus on lowering lifecycle costs, improving operational efficiency, and ensuring rapid fleet turnover. Electric two-wheelers deliver substantial savings in fuel and maintenance compared to internal combustion models, making them ideal for high-utilization fleets. With the rapid growth of e-commerce and food delivery, many companies are transitioning their entire fleets to electric models to meet sustainability goals and comply with stricter urban emission norms. These commercial operations also benefit from predictable routes and usage patterns, enabling easier deployment and financing of electric vehicles at scale. In response, OEMs are developing rugged, cargo-capable electric scooters and motorcycles, supported by battery swapping and dedicated charging networks tailored for fleet operations. For instance, in May 2025, Komaki launched the CAT 2.0 Eco, an electric scooter designed for last-mile delivery and utility applications. It features a lithium-ion battery offering a range of 110-120 km per charge and is powered by a BLDC motor capable of reaching a top speed of 55 km/h. Once commercial adoption reaches scale, the resulting cost efficiencies and infrastructure development are likely to extend into the consumer market, driving broader industry growth.

"The Asia Pacific electric two wheeler market is mainly driven by India."

India's vast two-wheeler market, driven by strong replacement demand and rapid urbanization, presents a highly favorable environment for electrification in the scooter & motorcycle sector in the Asia Pacific region. Government initiatives such as the FAME II scheme, state-level subsidies, and the national target of achieving 30% EV penetration by 2030 have significantly lowered upfront costs and accelerated adoption. The steady decline in lithium-ion battery prices is further enhancing the cost competitiveness of electric two-wheelers compared to ICE models. Leading domestic OEMs and startups, including Ola Electric, Ather Energy, and Hero MotoCorp, are actively expanding their electric portfolios while strengthening local manufacturing, distribution, and service networks. India's dense urban traffic, short daily commutes, and high fuel prices make electric two-wheelers particularly attractive from a total cost-of-ownership perspective. The shift toward electrification is also supported by the country's environmental and energy-security goals, aligning market forces, policy direction, and consumer demand. Reflecting this momentum, electric two-wheeler sales in India reached approximately 1.15 million units in FY24. Infrastructure development is keeping pace, with players such as Ather Energy planning to double their retail presence to 700 outlets nationwide by March 2026.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various key organizations operating in this market.

- By Company Type: OEMs - 30%, Tier I - 30%, and Tier II - 40%

- By Designation: CXOs - 35%, Directors - 20%, and Others - 45%

- By Region: North America - 15%, Europe - 15%, Asia Pacific - 70%

The electric two wheeler market is dominated by major players, including Ola Electric (India), Bajaj Auto Ltd. (India), TVS Motor Company (India), Ather Energy (India), and Yadea Technology Group Co., Ltd. (China). These companies have adopted a mix of organic and inorganic growth strategies, such as product launches, strategic partnerships, joint ventures, mergers & acquisitions, and expansion of production facilities, to strengthen their international footprint and capture a larger market share. Through these strategies, they have expanded across regions by offering a diverse portfolio of electric two-wheelers tailored to local market needs, featuring advanced battery technologies, connected mobility solutions, and competitive pricing to attract a wider customer base.

Research Coverage:

This research report categorizes the electric two wheeler market by vehicle type (E-scooter/moped, e-motorcycle), voltage type (36V, 48V, 60V, 72V, above 72V), motor type (hub and mid-drive), battery (Li-ion and lead acid), motor power, distance covered, technology, vehicle class, usage, and region. It covers the competitive landscape and profiles of the major players of the electric two wheeler market.

The study also includes an in-depth competitive analysis of the key market players, along with their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report:

- The report will help market leaders/new entrants with information on the closest approximations of revenue numbers for the overall electric two wheeler market and its subsegments.

- This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies.

- The report will also help stakeholders understand the market pulse and provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insight into the following pointers:

- Analysis of key drivers (fleet electrification for urban and commercial mobility, partnerships with fleet operators, and technological evolution in battery systems) restraints (charging infrastructure gaps and range performance constraints, and battery heating problems and long charging times), opportunities (lightweight design and shared vehicle architecture innovation, transition to modular and swappable energy platforms, and software ecosystem development and digital value chain expansion), and challenges (reliability of thermal and power electronics in urban operating conditions, and lack of standardization in battery communication and swapping protocols)

- Product Development/Innovation: Detailed insights into upcoming technologies and research & development activities in the electric two wheeler market

- Market Development: Comprehensive information about lucrative markets (the report analyzes the electric two wheeler market across varied regions)

- Market Diversification: Exhaustive information about untapped geographies, recent developments, and investments in the electric two wheeler market

- Competitive Assessment: In-depth assessment of market share, growth strategies, and product offerings of leading players such as Ola Electric (India), Bajaj Auto Ltd. (India), TVS Motor Company (India), Ather Energy (India), and Yadea Technology Group Co., Ltd. (China) in the electric two wheeler market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 List of secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Primary participants

- 2.1.2.2 Key industry insights and breakdown of primary interviews

- 2.1.2.3 Breakdown of primary interviews

- 2.1.2.4 List of primary interview participants

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.3 DATA TRIANGULATION

- 2.4 FACTOR ANALYSIS

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

- 2.7 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

- 3.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 3.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 3.3 DISRUPTIVE TRENDS SHAPING MARKET

- 3.4 HIGH-GROWTH SEGMENTS AND EMERGING FRONTIERS

- 3.5 GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN ELECTRIC TWO WHEELER MARKET

- 4.2 ELECTRIC TWO WHEELER MARKET, BY REGION

- 4.3 ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE

- 4.4 ELECTRIC TWO WHEELER MARKET, BY BATTERY TYPE

- 4.5 ELECTRIC TWO WHEELER MARKET, BY DISTANCE COVERED

- 4.6 ELECTRIC TWO WHEELER MARKET, BY MOTOR TYPE

- 4.7 ELECTRIC TWO WHEELER MARKET, BY USAGE

- 4.8 ELECTRIC TWO WHEELER MARKET, BY VEHICLE CLASS

- 4.9 ELECTRIC TWO WHEELER MARKET, BY TECHNOLOGY TYPE

- 4.10 ELECTRIC TWO WHEELER MARKET, BY MOTOR POWER

- 4.11 ELECTRIC TWO WHEELER MARKET, BY VOLTAGE TYPE

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Fleet electrification for urban and commercial mobility

- 5.2.1.2 Advancements in battery systems

- 5.2.1.3 Collaborations between OEMs, electric two wheeler manufacturers, and fleet operators

- 5.2.2 RESTRAINTS

- 5.2.2.1 Charging infrastructure gaps in many emerging economies and range performance issues

- 5.2.2.2 Battery heating problems and long charging times

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Lightweight design and shared vehicle architecture innovation

- 5.2.3.2 Transition to modular and swappable energy platforms

- 5.2.3.3 Software ecosystem development and digital value chain expansion

- 5.2.4 CHALLENGES

- 5.2.4.1 Reliability of thermal and power electronics in urban operating conditions

- 5.2.4.2 Lack of standardization in battery communication and swapping protocols

- 5.2.1 DRIVERS

- 5.3 UNMET NEEDS AND WHITE SPACES

- 5.3.1 UNMET NEEDS IN ELECTRIC TWO WHEELER MARKET

- 5.3.2 WHITE SPACE OPPORTUNITIES

- 5.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 5.4.1 INTERCONNECTED MARKETS

- 5.4.2 CROSS-SECTOR OPPORTUNITIES

- 5.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 5.5.1 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 5.6 PATENT ANALYSIS

- 5.7 IMPACT OF GENERATIVE AI ON ELECTRIC TWO WHEELER MARKET

- 5.7.1 PRODUCT DESIGN AND DEVELOPMENT OPTIMIZATION

- 5.7.2 INTELLIGENT MANUFACTURING AND SUPPLY CHAIN EFFICIENCY

- 5.7.3 PERSONALIZATION AND USER EXPERIENCE ENHANCEMENT

- 5.7.4 ADVANCED BATTERY MANAGEMENT AND ENERGY OPTIMIZATION

- 5.8 ACOUSTIC VEHICLE ALERTING SYSTEM (AVAS) IN ELECTRIC 2-WHEELERS

- 5.8.1 REGULATORY FRAMEWORK AND MANDATES

- 5.8.2 AVAS INTEGRATION IN ELECTRIC TWO WHEELERS

- 5.8.3 COMPONENT ARCHITECTURE AND DESIGN TRENDS

- 5.8.3.1 Typical setup

- 5.8.3.2 Design trends

- 5.8.4 FUTURE ADVANCEMENTS IN SOUND SIGNATURE AND SMART AVAS

- 5.8.4.1 Dynamic sound profiles

- 5.8.4.2 Psychoacoustic tuning

- 5.9 EMERGING BUSINESS MODELS IN ELECTRIC TWO WHEELER MARKET

- 5.9.1 SUBSCRIPTION-BASED AND LEASING MODELS

- 5.9.2 BATTERY SWAPPING AND ENERGY-AS-A-SERVICE (EAAS)

- 5.9.3 SHARED MOBILITY AND FLEET ELECTRIFICATION

- 5.9.4 BATTERY-AS-A-SERVICE (BAAS)

- 5.9.5 DIGITAL SERVICE MONETIZATION

- 5.10 KEY EMERGING TECHNOLOGIES

- 5.10.1 INTEGRATED POWERTRAIN MODULES

- 5.10.2 SOLID-STATE BATTERY (SSB)

- 5.10.3 SMART CHARGING SYSTEMS

- 5.11 COMPLEMENTARY TECHNOLOGIES

- 5.11.1 BATTERY SWAPPING IN ELECTRIC SCOOTERS

- 5.11.2 INTERNET OF THINGS IN ELECTRIC TWO WHEELERS

- 5.11.3 SHARED MOBILITY

- 5.11.4 BATTERY-RELATED SERVICES

- 5.11.5 VEHICLE INTELLIGENCE & CONNECTIVITY STACK

- 5.12 TECHNOLOGY/PRODUCT ROADMAP

- 5.12.1 SHORT-TERM (2025-2027) | FOUNDATION AND EARLY COMMERCIALIZATION

- 5.12.2 MID-TERM (2028-2030) | EXPANSION AND STANDARDIZATION

- 5.12.3 LONG-TERM (2031-2035+) | MASS COMMERCIALIZATION & DISRUPTION

- 5.13 BILL OF MATERIALS

- 5.14 TOTAL COST OF OWNERSHIP

- 5.15 OEM ANALYSIS

- 5.15.1 PRODUCTION CAPACITY OF KEY OEMS

- 5.15.2 TECHNOLOGICAL DEVELOPMENTS

- 5.15.2.1 Honda

- 5.15.2.2 Yamaha

- 5.15.2.3 BMW Motorrad

- 5.15.2.4 Piaggio Group (Vespa/Piaggio)

- 5.15.2.5 Ather Energy

- 5.15.2.6 Ola Electric

- 5.15.2.7 NIU (China/Global)

- 5.15.3 COMPARATIVE ANALYSIS OF MOTOR POWER AND VEHICLE RANGE ACROSS VOLTAGE LEVEL

- 5.16 FUTURE APPLICATIONS IN ELECTRIC TWO WHEELER ECOSYSTEM

- 5.16.1 BATTERY INNOVATIONS AND ENERGY STORAGE SYSTEMS

- 5.16.1.1 Solid-state and semi-solid batteries

- 5.16.1.2 Fast charging and smart charging infrastructure

- 5.16.1.3 Battery management systems

- 5.16.1.4 Second-life & recycling

- 5.16.2 SMART/ADAPTIVE RIDE MODES AND AI

- 5.16.2.1 Personalized ride modes

- 5.16.2.2 Terrain and traffic adaptation

- 5.16.3 ADVANCED RIDER/VEHICLE SAFETY SYSTEMS

- 5.16.3.1 AI-based collision avoidance

- 5.16.3.2 Connected helmets & wearables

- 5.16.3.3 Blind-spot monitoring & alerts

- 5.16.4 ADVANCED RIDER/VEHICLE SAFETY SYSTEMS

- 5.16.4.1 Valet parking & remote summon

- 5.16.4.2 Self-balancing & self-righting concepts

- 5.16.4.3 Convoy/Ride-following modes

- 5.16.1 BATTERY INNOVATIONS AND ENERGY STORAGE SYSTEMS

- 5.17 MACROECONOMICS INDICATORS

- 5.17.1 INTRODUCTION

- 5.17.2 GDP TRENDS AND FORECAST

- 5.17.3 TRENDS IN GLOBAL TWO WHEELER INDUSTRY (INTERNAL COMBUSTION ENGINE AND ELECTRIC VEHICLES)

- 5.17.4 TRENDS IN GLOBAL AUTOMOTIVE & TRANSPORTATION INDUSTRY

- 5.18 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.19 PRICING ANALYSIS

- 5.19.1 AVERAGE SELLING PRICE TREND, BY VEHICLE TYPE, 2022-2024

- 5.19.2 AVERAGE SELLING PRICE FOR VEHICLE TYPES BY KEY PLAYERS, 2024

- 5.19.3 AVERAGE SELLING PRICE TREND, BY REGION, 2022-2024

- 5.20 ECOSYSTEM ANALYSIS

- 5.20.1 RAW MATERIAL SUPPLIERS

- 5.20.2 COMPONENT SUPPLIERS

- 5.20.3 BATTERY PACK MANUFACTURERS/SUPPLIERS

- 5.20.4 CHARGING INFRASTRUCTURE PROVIDERS

- 5.20.5 ELECTRIC SCOOTER AND MOTORCYCLE MANUFACTURERS

- 5.21 SUPPLY CHAIN ANALYSIS

- 5.22 CASE STUDY ANALYSIS

- 5.22.1 GENZE PARTNERED WITH LEEWAYHERTZ FOR INTEGRATION OF ELECTRIC SCOOTER WITH MOBILE APP

- 5.22.2 HERO ELECTRIC PARTNERED WITH EBIKEGO TO TRANSFORM LAST-MILE DELIVERIES

- 5.22.3 ZYPP ELECTRIC TO USE HERO ELECTRIC BIKES TO ELECTRIFY 100% LAST-MILE DELIVERY BY 2025

- 5.23 INVESTMENT AND FUNDING SCENARIO

- 5.24 TRADE ANALYSIS

- 5.24.1 IMPORT SCENARIO (HS CODE 871190)

- 5.24.2 EXPORT SCENARIO (HS CODE 871190)

- 5.25 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.26 DECISION-MAKING PROCESS

- 5.27 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 5.27.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.27.2 BUYING CRITERIA

- 5.28 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 5.29 REGULATORY LANDSCAPE AND COMPLIANCE

- 5.29.1 INDUSTRY STANDARDS

- 5.29.1.1 India

- 5.29.1.2 Thailand

- 5.29.1.3 Vietnam

- 5.29.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.29.1 INDUSTRY STANDARDS

- 5.30 SUSTAINABILITY INITIATIVES

- 5.30.1 CARBON FOOTPRINT REDUCTION THROUGH GREEN MANUFACTURING

- 5.30.1.1 Renewable energy in factories

- 5.30.1.2 Materials and efficiency

- 5.30.1.3 Certifications and targets

- 5.30.2 ECO-APPLICATIONS AND ENVIRONMENTAL BENEFITS OF ELECTRIFICATION

- 5.30.3 LIFE-CYCLE ASSESSMENT (LCA) OF ELECTRIC TWO WHEELERS

- 5.30.3.1 Energy and emissions by phase

- 5.30.3.2 Battery production impact

- 5.30.1 CARBON FOOTPRINT REDUCTION THROUGH GREEN MANUFACTURING

6 ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE

- 6.1 INTRODUCTION

- 6.1.1 OPERATIONAL DATA

- 6.2 E-SCOOTER/MOPED

- 6.2.1 GROWING FOCUS ON REDUCED EMISSIONS AND SUSTAINABLE MODELS TO DRIVE MARKET

- 6.3 E-MOTORCYCLE

- 6.3.1 RISING DEMAND FOR HIGH-PERFORMANCE AND LOW-MAINTENANCE MODELS TO DRIVE MARKET

- 6.4 KEY PRIMARY INSIGHTS

7 ELECTRIC TWO WHEELER MARKET, BY VEHICLE CLASS

- 7.1 INTRODUCTION

- 7.1.1 OPERATIONAL DATA

- 7.2 ECONOMY

- 7.2.1 AVAILABILITY OF BUDGET-FRIENDLY FINANCING AND LEASING OPTIONS TO DRIVE MARKET

- 7.3 LUXURY

- 7.3.1 DEMAND FOR PREMIUM FEATURES AND TECHNOLOGY IN ELECTRIC TWO WHEELERS TO DRIVE MARKET

- 7.4 PRIMARY INSIGHTS

8 ELECTRIC TWO WHEELER MARKET, BY VOLTAGE TYPE

- 8.1 INTRODUCTION

- 8.1.1 OPERATIONAL DATA

- 8.2 36 V

- 8.2.1 INCREASING DEMAND FOR SHORT COMMUTES TO DRIVE GROWTH

- 8.3 48 V

- 8.3.1 NEED FOR ADEQUATE POWER AND RANGE FOR URBAN AND SUBURBAN COMMUTING TO DRIVE GROWTH

- 8.4 60 V

- 8.4.1 EMERGING DEMAND FOR HIGH-PERFORMANCE ELECTRIC SCOOTERS TO DRIVE GROWTH

- 8.5 72 V

- 8.5.1 IMPROVED BATTERY TECHNOLOGY AND CHARGING INFRASTRUCTURE TO DRIVE GROWTH

- 8.6 ABOVE 72 V

- 8.6.1 INCREASED RANGE POTENTIAL AND HIGH-PERFORMANCE NEEDS TO DRIVE GROWTH

- 8.7 KEY PRIMARY INSIGHTS

9 ELECTRIC TWO WHEELER MARKET, BY BATTERY TYPE

- 9.1 INTRODUCTION

- 9.1.1 OPERATIONAL DATA

- 9.2 SEALED LEAD-ACID

- 9.2.1 LOW RANGE AND PERFORMANCE TO DECREASE DEMAND

- 9.3 LITHIUM-ION

- 9.3.1 ADVANCEMENTS IN BATTERY TECHNOLOGY TO DRIVE MARKET

- 9.4 NICKEL METAL HYDRIDE (NIMH)

- 9.5 SODIUM-ION

- 9.6 PRIMARY INSIGHTS

10 ELECTRIC TWO WHEELER MARKET, BY DISTANCE COVERED

- 10.1 INTRODUCTION

- 10.1.1 OPERATIONAL DATA

- 10.2 BELOW 75 MILES

- 10.2.1 DOMINANT USE IN CITIES FOR SHORT COMMUTES TO DRIVE MARKET

- 10.3 75-100 MILES

- 10.3.1 VERSATILITY AND RANGE ANXIETY REDUCTION TO DRIVE MARKET

- 10.4 ABOVE 100 MILES

- 10.4.1 DEVELOPMENTS IN BATTERY TECHNOLOGY TO DRIVE MARKET

- 10.5 PRIMARY INSIGHTS

11 ELECTRIC TWO WHEELER MARKET, BY USAGE

- 11.1 INTRODUCTION

- 11.1.1 OPERATIONAL DATA

- 11.2 PRIVATE

- 11.2.1 NEW RANGE OF PRODUCTS WITH REDUCED PRICES TO DRIVE MARKET

- 11.3 COMMERCIAL

- 11.3.1 OPERATIONAL AND COST EFFICIENCY TO DRIVE MARKET

- 11.4 PRIMARY INSIGHTS

12 ELECTRIC TWO WHEELER MARKET, BY TECHNOLOGY TYPE

- 12.1 INTRODUCTION

- 12.1.1 OPERATIONAL DATA

- 12.2 PLUG-IN

- 12.2.1 INCREASING NUMBER OF PUBLIC FAST CHARGING STATIONS FOR ELECTRIC TWO WHEELERS TO DRIVE MARKET

- 12.3 BATTERY

- 12.3.1 ENABLES QUICK REFUELING BY EXCHANGING DEPLETED BATTERIES FOR FULLY CHARGED ONES AT DESIGNATED STATIONS

- 12.4 PRIMARY INSIGHTS

13 ELECTRIC SCOOTER MARKET, BY MOTOR TYPE

- 13.1 INTRODUCTION

- 13.1.1 OPERATIONAL DATA

- 13.2 MID-DRIVE MOTOR

- 13.2.1 HIGH TORQUE ADVANTAGE TO DRIVE MARKET

- 13.3 HUB MOTOR

- 13.3.1 INCREASING PRODUCTION OF VEHICLES WITH IN-WHEEL ELECTRIC MOTORS TO DRIVE MARKET

- 13.4 OTHERS

- 13.5 PRIMARY INSIGHTS

14 ELECTRIC TWO WHEELER MARKET, BY MOTOR POWER

- 14.1 INTRODUCTION

- 14.1.1 OPERATIONAL DATA

- 14.2 LESS THAN 1.5 KW

- 14.2.1 LOWER PRICE TAG THAN HIGHER-POWERED MODELS TO DRIVE MARKET

- 14.3 1.5-3 KW

- 14.3.1 IMPROVED PERFORMANCE COMPARED TO LOWER-POWERED MODELS TO DRIVE MARKET

- 14.4 ABOVE 3 KW

- 14.4.1 DEMAND FOR HIGH SPEED AND ACCELERATION WITH LONGER RANGE TO DRIVE MARKET

- 14.5 KEY PRIMARY INSIGHTS

15 ELECTRIC TWO WHEELER MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 ASIA PACIFIC

- 15.2.1 MACROECONOMIC OUTLOOK

- 15.2.2 CHINA

- 15.2.2.1 Increasing demand for electric scooters/mopeds in metropolitan cities to drive market

- 15.2.3 JAPAN

- 15.2.3.1 Investment in charging infrastructure and battery swapping technologies to drive market

- 15.2.4 INDIA

- 15.2.4.1 Introduction of Battery-as-a-Service model to drive market

- 15.2.5 SOUTH KOREA

- 15.2.5.1 Launch of innovative models by domestic OEMs to drive market

- 15.2.6 TAIWAN

- 15.2.6.1 Focus on advanced electric two wheeler technologies that are energy-efficient and environmentally friendly to drive market

- 15.2.7 THAILAND

- 15.2.7.1 Strong government support for electric vehicle adoption to drive market

- 15.2.8 INDONESIA

- 15.2.8.1 Growth of online sales of electric vehicles and domestic manufacturing to drive market

- 15.2.9 MALAYSIA

- 15.2.9.1 Introduction of battery swapping points to drive market

- 15.2.10 PHILIPPINES

- 15.2.10.1 Growing EV ecosystem to support market growth

- 15.2.11 VIETNAM

- 15.2.11.1 Shift toward sustainable transportation to drive market

- 15.3 EUROPE

- 15.3.1 MACROECONOMIC OUTLOOK

- 15.3.2 FRANCE

- 15.3.2.1 Government incentive programs to fuel market

- 15.3.3 GERMANY

- 15.3.3.1 Growing demand for energy-efficient commuting modes to drive market

- 15.3.4 SPAIN

- 15.3.4.1 NECP's plan for five million electric vehicles on road by 2030 to drive market

- 15.3.5 AUSTRIA

- 15.3.5.1 Subsidies and tax exemptions for electric two wheelers to drive market

- 15.3.6 UK

- 15.3.6.1 Increasing concerns regarding two wheeler carbon emissions to drive market

- 15.3.7 ITALY

- 15.3.7.1 Increasing presence of key players to support market growth

- 15.3.8 BELGIUM

- 15.3.8.1 Strong government support to promote electric two wheelers to drive market

- 15.3.9 NETHERLANDS

- 15.3.9.1 Development of charging infrastructure to drive market

- 15.3.10 POLAND

- 15.3.10.1 Growing focus on emission reduction to drive market

- 15.3.11 DENMARK

- 15.3.11.1 Government support to develop charging infrastructure to drive market

- 15.4 NORTH AMERICA

- 15.4.1 MACROECONOMIC OUTLOOK

- 15.4.2 US

- 15.4.2.1 R&D of new EV-related technologies to drive market

- 15.4.3 CANADA

- 15.4.3.1 High demand for electric scooters among young population to drive market

16 COMPETITIVE LANDSCAPE

- 16.1 OVERVIEW

- 16.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- 16.3 MARKET SHARE ANALYSIS OF ELECTRIC TWO WHEELER PROVIDERS, 2024

- 16.4 REVENUE ANALYSIS, 2020-2024

- 16.5 COMPANY VALUATION AND FINANCIAL METRICS

- 16.5.1 COMPANY VALUATION

- 16.5.2 FINANCIAL METRICS

- 16.6 PRODUCT COMPARISON

- 16.7 COMPANY EVALUATION MATRIX

- 16.7.1 STARS

- 16.7.2 EMERGING LEADERS

- 16.7.3 PERVASIVE PLAYERS

- 16.7.4 PARTICIPANTS

- 16.7.5 COMPANY FOOTPRINT

- 16.8 STARTUP/SME EVALUATION MATRIX

- 16.8.1 PROGRESSIVE COMPANIES

- 16.8.2 RESPONSIVE COMPANIES

- 16.8.3 DYNAMIC COMPANIES

- 16.8.4 STARTING BLOCKS

- 16.8.5 COMPETITIVE BENCHMARKING

- 16.8.5.1 Key startups/SMEs

- 16.8.5.2 Competitive benchmarking of key startups/SMEs

- 16.9 COMPETITIVE SCENARIO

- 16.9.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 16.9.2 DEALS

- 16.9.3 EXPANSIONS

- 16.9.4 OTHER DEVELOPMENTS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 OLA ELECTRIC

- 17.1.1.1 Business overview

- 17.1.1.2 Products offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Product launches/developments

- 17.1.1.3.2 Expansions

- 17.1.1.3.3 Others

- 17.1.1.4 MnM view

- 17.1.1.4.1 Key strengths

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses and competitive threats

- 17.1.2 BAJAJ AUTO LTD.

- 17.1.2.1 Business overview

- 17.1.2.2 Products offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Product launches/developments

- 17.1.2.4 MnM view

- 17.1.2.4.1 Key strengths

- 17.1.2.4.2 Strategic choices

- 17.1.2.4.3 Weaknesses and competitive threats

- 17.1.3 TVS MOTOR COMPANY

- 17.1.3.1 Business overview

- 17.1.3.2 Products offered

- 17.1.3.3 Recent developments

- 17.1.3.3.1 Product launches/upgrades

- 17.1.3.3.2 Deals

- 17.1.3.3.3 Others

- 17.1.3.4 MnM view

- 17.1.3.4.1 Key strengths

- 17.1.3.4.2 Strategic choices

- 17.1.3.4.3 Weaknesses and competitive threats

- 17.1.4 ATHER ENERGY

- 17.1.4.1 Business overview

- 17.1.4.2 Products offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Product launches/developments

- 17.1.4.3.2 Deals

- 17.1.4.4 MnM view

- 17.1.4.4.1 Key strengths

- 17.1.4.4.2 Strategic choices

- 17.1.4.4.3 Weaknesses and competitive threats

- 17.1.5 YADEA TECHNOLOGY GROUP CO., LTD.

- 17.1.5.1 Business overview

- 17.1.5.2 Products offered

- 17.1.5.3 Recent developments

- 17.1.5.3.1 Product launches/developments

- 17.1.5.3.2 Deals

- 17.1.5.3.3 Expansions

- 17.1.5.3.4 Others

- 17.1.5.4 MnM view

- 17.1.5.4.1 Key strengths

- 17.1.5.4.2 Strategic choices

- 17.1.5.4.3 Weaknesses and competitive threats

- 17.1.6 HERO ELECTRIC

- 17.1.6.1 Business overview

- 17.1.6.2 Products offered

- 17.1.6.3 Recent developments

- 17.1.6.3.1 Product launches/developments

- 17.1.6.3.2 Deals

- 17.1.6.3.3 Expansions

- 17.1.7 GOGORO

- 17.1.7.1 Business overview

- 17.1.7.2 Products offered

- 17.1.7.3 Recent developments

- 17.1.7.3.1 Product/technology launches

- 17.1.7.3.2 Deals

- 17.1.8 VMOTO LIMITED

- 17.1.8.1 Business overview

- 17.1.8.2 Products offered

- 17.1.8.3 Recent developments

- 17.1.8.3.1 Product launches/developments

- 17.1.8.3.2 Deals

- 17.1.8.3.3 Expansions

- 17.1.8.3.4 Others

- 17.1.9 NIU INTERNATIONAL

- 17.1.9.1 Business overview

- 17.1.9.2 Products offered

- 17.1.9.3 Recent developments

- 17.1.9.3.1 Product launches/developments

- 17.1.9.3.2 Deals

- 17.1.10 JIANGSU XINRI E-VEHICLE CO., LTD.

- 17.1.10.1 Business overview

- 17.1.10.2 Products offered

- 17.1.10.3 Recent developments

- 17.1.10.3.1 Product launches/developments

- 17.1.10.3.2 Deals

- 17.1.10.3.3 Expansions

- 17.1.11 IDEANOMICS, INC.

- 17.1.11.1 Business overview

- 17.1.11.2 Products offered

- 17.1.11.3 Recent developments

- 17.1.11.3.1 Product launches/developments

- 17.1.11.3.2 Deals

- 17.1.11.3.3 Expansions

- 17.1.12 ASKOLL EVA S.P.A.

- 17.1.12.1 Business overview

- 17.1.12.2 Products offered

- 17.1.12.3 Recent developments

- 17.1.12.3.1 Deals

- 17.1.12.3.2 Others

- 17.1.1 OLA ELECTRIC

- 17.2 OTHER PLAYERS

- 17.2.1 ULTRAVIOLETTE AUTOMOTIVE

- 17.2.2 REVOLT INTELLICORP PRIVATE LIMITED (REVOLT MOTORS)

- 17.2.3 Z ELECTRIC VEHICLE

- 17.2.4 CAKE

- 17.2.5 LIGHTNING MOTORCYCLES

- 17.2.6 JOHAMMER E-MOBILITY GMBH

- 17.2.7 PIAGGIO GROUP

- 17.2.8 KTM AG

- 17.2.9 HARLEY DAVIDSON

- 17.2.10 BMW GROUP

- 17.2.11 AIMA TECHNOLOGY GROUP CO., LTD.

- 17.2.12 HONDA MOTOR CO., LTD.

- 17.2.13 GREAVES ELECTRIC MOBILITY PRIVATE LIMITED (AMPERE VEHICLES)

- 17.2.14 DONGGUAN TAILING ELECTRIC VEHICLE CO., LTD.

- 17.2.15 CEZETA

- 17.2.16 TERRA MOTORS CORPORATION

- 17.2.17 NEXZU MOBILITY LTD. (AVAN MOTORS INDIA)

- 17.2.18 EMFLUX MOTORS

- 17.2.19 MAHINDRA & MAHINDRA LTD.

- 17.2.20 DAMON MOTORS INC.

- 17.2.21 VIAR MOTOR INDONESIA

- 17.2.22 SELIS

- 17.2.23 GESITS

- 17.2.24 UNITED E-MOTOR

- 17.2.25 SMOOT ELEKTRIK

- 17.2.26 PT VOLTA INDONESIA SEMESTA (VOLTA)

- 17.2.27 ALVA

- 17.2.28 NUSA MOTORS

- 17.2.29 BF GOODRICH

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.3.1 ELECTRIC SCOOTER MARKET, BY BATTERY TYPE AT COUNTRY LEVEL (FOR COUNTRIES COVERED IN THE REPORT)

- 18.3.2 PROFILING OF ADDITIONAL MARKET PLAYERS (UP TO 5)

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS

List of Tables

- TABLE 1 ELECTRIC TWO WHEELER MARKET DEFINITION, BY VEHICLE TYPE

- TABLE 2 ELECTRIC TWO WHEELER MARKET DEFINITION, BY BATTERY TYPE

- TABLE 3 ELECTRIC TWO WHEELER MARKET DEFINITION, BY TECHNOLOGY TYPE

- TABLE 4 ELECTRIC TWO WHEELER MARKET DEFINITION, BY VEHICLE CLASS

- TABLE 5 ELECTRIC TWO WHEELER MARKET DEFINITION, BY USAGE

- TABLE 6 ELECTRIC TWO WHEELER MARKET DEFINITION, BY MOTOR TYPE

- TABLE 7 ELECTRIC TWO WHEELER MARKET DEFINITION, BY MOTOR POWER

- TABLE 8 ELECTRIC TWO WHEELER MARKET DEFINITION, BY DISTANCE COVERED

- TABLE 9 ELECTRIC TWO WHEELER MARKET DEFINITION, BY VOLTAGE TYPE

- TABLE 10 ELECTRIC TWO WHEELER MARKET: INCLUSIONS AND EXCLUSIONS

- TABLE 11 USD EXCHANGE RATES

- TABLE 12 ELECTRIFICATION TARGETS OF KEY COUNTRIES IN ASIA PACIFIC

- TABLE 13 ELECTRIC VEHICLE CHARGING POINTS, BY EMERGING ECONOMIES, 2024

- TABLE 14 MODEL-WISE DRIVING RANGE OF ELECTRIC SCOOTERS AND MOTORCYCLES

- TABLE 15 TIME REQUIRED TO CHARGE ELECTRIC SCOOTERS AND MOTORCYCLES

- TABLE 16 IMPACT OF MARKET DYNAMICS

- TABLE 17 PATENT ANALYSIS

- TABLE 18 OEMS WITH SUBSCRIPTION-BASED AND LEASING MODELS

- TABLE 19 OEMS ADOPTING BATTERY SWAPPING AND ENERGY-AS-A-SERVICE BUSINESS MODELS

- TABLE 20 COMPANIES ADOPTING SHARED MOBILITY AND FLEET ELECTRIFICATION BUSINESS MODELS

- TABLE 21 OEMS OFFERING BAAS IN ELECTRIC TWO WHEELERS

- TABLE 22 BILL OF MATERIALS FOR ELECTRIC SCOOTERS IN 2025

- TABLE 23 BILL OF MATERIALS FOR ICE SCOOTERS IN 2025

- TABLE 24 BILL OF MATERIALS FOR ELECTRIC MOTORCYCLES IN 2025

- TABLE 25 BILL OF MATERIALS FOR ICE MOTORCYCLES IN 2025

- TABLE 26 TCO COMPARISON: ELECTRIC VS. ICE SCOOTERS

- TABLE 27 PRODUCTION CAPACITY OF KEY OEMS

- TABLE 28 ANALYSIS OF MOTOR POWER AND VEHICLE RANGE ACROSS VOLTAGE LEVEL

- TABLE 29 GDP PERCENTAGE CHANGE, BY KEY COUNTRY, 2021-2030

- TABLE 30 AVERAGE SELLING PRICE TREND, BY VEHICLE TYPE, 2022-2024 (USD)

- TABLE 31 AVERAGE SELLING PRICE OF ELECTRIC SCOOTERS BY KEY PLAYERS, 2024 (USD)

- TABLE 32 AVERAGE SELLING PRICE OF ELECTRIC MOTORCYCLES BY KEY PLAYERS, 2024 (USD)

- TABLE 33 AVERAGE SELLING PRICE TREND FOR ELECTRIC SCOOTERS, BY REGION, 2022-2024 (USD/UNIT)

- TABLE 34 AVERAGE SELLING PRICE TREND FOR ELECTRIC MOTORCYCLES, BY REGION, 2022-2024 (USD/UNIT)

- TABLE 35 ELECTRIC TWO WHEELER MARKET: ROLE OF COMPANIES IN ECOSYSTEM

- TABLE 36 IMPORT DATA FOR HS CODE 871190, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 37 EXPORT DATA FOR HS CODE 871190, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 38 ELECTRIC TWO WHEELER MARKET: KEY CONFERENCES AND EVENTS, 2025-2026

- TABLE 39 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR ELECTRIC TWO WHEELERS (%)

- TABLE 40 KEY BUYING CRITERIA

- TABLE 41 SUBSIDY UNDER FAME II, BY VEHICLE TYPE

- TABLE 42 CENTRAL AND STATE TAXES AND FEES FOR SELECT VEHICLES IN INDIA

- TABLE 43 INDIA: GOVERNMENT INCENTIVES, BY STATE

- TABLE 44 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 45 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 46 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 47 STRATEGIC GREEN MANUFACTURING ACTIONS BY OEMS

- TABLE 48 CONVENTIONAL VS. BATTERY ELECTRIC SCOOTER/MOPED AND MOTORCYCLE

- TABLE 49 ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 50 ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 51 ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 52 ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 53 POPULAR E-SCOOTER/MOPED AND E-MOTORCYCLE MODELS WORLDWIDE

- TABLE 54 E-SCOOTER/MOPED: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 55 E-SCOOTER/MOPED: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 56 E-SCOOTER/MOPED: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 57 E-SCOOTER/MOPED: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 58 E-MOTORCYCLE: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 59 E-MOTORCYCLE: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 60 E-MOTORCYCLE: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 61 E-MOTORCYCLE: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 62 ELECTRIC TWO WHEELER MARKET, BY VEHICLE CLASS, 2021-2024 (THOUSAND UNITS)

- TABLE 63 ELECTRIC TWO WHEELER MARKET, BY VEHICLE CLASS, 2025-2032 (THOUSAND UNITS)

- TABLE 64 ELECTRIC TWO WHEELER MARKET, BY VEHICLE CLASS, 2021-2024 (USD MILLION)

- TABLE 65 ELECTRIC TWO WHEELER MARKET, BY VEHICLE CLASS, 2025-2032 (USD MILLION)

- TABLE 66 E-SCOOTER/MOPED AND E-MOTORCYCLE MODELS WORLDWIDE

- TABLE 67 ECONOMY: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 68 ECONOMY: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 69 ECONOMY: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 70 ECONOMY: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 71 LUXURY: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 72 LUXURY: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 73 LUXURY: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 74 LUXURY: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 75 ELECTRIC SCOOTERS OFFERED BY OEMS, BY VOLTAGE TYPE

- TABLE 76 ELECTRIC TWO WHEELER MARKET, BY VOLTAGE TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 77 ELECTRIC TWO WHEELER MARKET, BY VOLTAGE TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 78 ELECTRIC TWO WHEELER MARKET, BY VOLTAGE TYPE, 2021-2024 (USD MILLION)

- TABLE 79 ELECTRIC TWO WHEELER MARKET, BY VOLTAGE TYPE, 2025-2032 (USD MILLION)

- TABLE 80 POPULAR E-SCOOTER/MOPED AND E-MOTORCYCLE MODELS AND THEIR BATTERY VOLTAGE

- TABLE 81 36 V: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 82 36 V: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 83 36 V: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 84 36 V: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 85 48 V: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 86 48 V: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 87 48 V: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 88 48 V: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 89 60 V: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 90 60 V: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 91 60 V: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 92 60 V: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 93 72 V: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 94 72 V: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 95 72 V: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 96 72 V: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 97 ABOVE 72 V: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 98 ABOVE 72 V: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 99 ABOVE 72 V: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 100 ABOVE 72 V: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 101 LITHIUM-ION VS. LEAD-ACID BATTERIES

- TABLE 102 ELECTRIC TWO WHEELER MARKET, BY BATTERY TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 103 ELECTRIC TWO WHEELER MARKET, BY BATTERY TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 104 ELECTRIC TWO WHEELER MARKET, BY BATTERY TYPE, 2021-2024 (USD MILLION)

- TABLE 105 ELECTRIC TWO WHEELER MARKET, BY BATTERY TYPE, 2025-2032 (USD MILLION)

- TABLE 106 POPULAR ELECTRIC SCOOTERS, BY BATTERY TYPE

- TABLE 107 SEALED LEAD-ACID: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 108 SEALED LEAD-ACID: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 109 SEALED LEAD-ACID: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 110 SEALED LEAD-ACID: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 111 COMPARATIVE EVALUATION OF ELECTRIC VEHICLES USING LITHIUM-ION BATTERIES

- TABLE 112 LITHIUM-ION: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 113 LITHIUM-ION: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 114 LITHIUM-ION: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 115 LITHIUM-ION: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 116 ELECTRIC TWO WHEELER MARKET, BY DISTANCE COVERED, 2021-2024 (THOUSAND UNITS)

- TABLE 117 ELECTRIC TWO WHEELER MARKET, BY DISTANCE COVERED 2025-2032 (THOUSAND UNITS)

- TABLE 118 ELECTRIC TWO WHEELER MARKET, BY DISTANCE COVERED, 2021-2024 (USD MILLION)

- TABLE 119 ELECTRIC TWO WHEELER MARKET, BY DISTANCE COVERED, 2025-2032 (USD MILLION)

- TABLE 120 POPULAR ELECTRIC SCOOTERS/MOPEDS AND MOTORCYCLES WITH RANGE

- TABLE 121 BELOW 75 MILES: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 122 BELOW 75 MILES: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 123 BELOW 75 MILES: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 124 BELOW 75 MILES: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 125 75-100 MILES: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 126 75-100 MILES: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 127 75-100 MILES: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 128 75-100 MILES: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 129 ABOVE 100 MILES: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 130 ABOVE 100 MILES: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 131 ABOVE 100 MILES: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 132 ABOVE 100 MILES: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 133 ELECTRIC TWO WHEELER MARKET, BY USAGE, 2021-2024 (THOUSAND UNITS)

- TABLE 134 ELECTRIC TWO WHEELER MARKET, BY USAGE, 2025-2032 (THOUSAND UNITS)

- TABLE 135 ELECTRIC TWO WHEELER MARKET, BY USAGE, 2021-2024 (USD MILLION)

- TABLE 136 ELECTRIC TWO WHEELER MARKET, BY USAGE, 2025-2032 (USD MILLION)

- TABLE 137 E-SCOOTER/MOPED AND E-MOTORCYCLE MODELS BY USAGE

- TABLE 138 PRIVATE: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 139 PRIVATE: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 140 PRIVATE: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 141 PRIVATE: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 142 COMMERCIAL: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 143 COMMERCIAL: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 144 COMMERCIAL: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 145 COMMERCIAL: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 146 ELECTRIC TWO WHEELER MARKET, BY TECHNOLOGY TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 147 ELECTRIC TWO WHEELER MARKET, BY TECHNOLOGY TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 148 ELECTRIC TWO WHEELER MARKET, BY TECHNOLOGY TYPE, 2021-2024 (USD MILLION)

- TABLE 149 ELECTRIC TWO WHEELER MARKET, BY TECHNOLOGY TYPE, 2025-2032 (USD MILLION)

- TABLE 150 E-SCOOTER/MOPED AND E-MOTORCYCLE MODELS WITH DIFFERENT CHARGING TECHNOLOGIES

- TABLE 151 PLUG-IN CHARGING VS. BATTERY CHARGING

- TABLE 152 PLUG-IN: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 153 PLUG-IN: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 154 PLUG-IN: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 155 PLUG-IN: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 156 BATTERY: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 157 BATTERY: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 158 BATTERY: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 159 BATTERY: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 160 ELECTRIC TWO WHEELER MARKET, BY MOTOR TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 161 ELECTRIC TWO WHEELER MARKET, BY MOTOR TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 162 ELECTRIC TWO WHEELER MARKET, BY MOTOR TYPE, 2021-2024 (USD MILLION)

- TABLE 163 ELECTRIC TWO WHEELER MARKET, BY MOTOR TYPE, 2025-2032 (USD MILLION)

- TABLE 164 POPULAR E-SCOOTER/MOPED AND E-MOTORCYCLE MODELS, BY MOTOR TYPE

- TABLE 165 MID-DRIVE MOTOR: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 166 MID-DRIVE MOTOR: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 167 MID-DRIVE MOTOR: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 168 MID-DRIVE MOTOR: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 169 HUB MOTOR: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 170 HUB MOTOR: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 171 HUB MOTOR: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 172 HUB MOTOR: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 173 ELECTRIC TWO WHEELER MARKET, BY MOTOR POWER, 2021-2024 (THOUSAND UNITS)

- TABLE 174 ELECTRIC TWO WHEELER MARKET, BY MOTOR POWER, 2025-2032 (THOUSAND UNITS)

- TABLE 175 ELECTRIC TWO WHEELER MARKET, BY MOTOR POWER, 2021-2024 (USD MILLION)

- TABLE 176 ELECTRIC TWO WHEELER MARKET, BY MOTOR POWER, 2025-2032 (USD MILLION)

- TABLE 177 POPULAR E-SCOOTER/MOPED AND E-MOTORCYCLE MODELS, BY MOTOR POWER

- TABLE 178 LESS THAN 1.5 KW: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 179 LESS THAN 1.5 KW: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 180 LESS THAN 1.5 KW: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 181 LESS THAN 1.5 KW: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 182 1.5-3 KW: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 183 1.5-3 KW: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 184 1.5-3 KW: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 185 1.5-3 KW: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 186 ABOVE 3 KW: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 187 ABOVE 3 KW: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 188 ABOVE 3 KW: ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 189 ABOVE 3 KW: ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 190 ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 191 ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 192 ELECTRIC TWO WHEELER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 193 ELECTRIC TWO WHEELER MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 194 ASIA PACIFIC: ELECTRIC TWO WHEELER MARKET, BY COUNTRY, 2021-2024 (THOUSAND UNITS)

- TABLE 195 ASIA PACIFIC: ELECTRIC TWO WHEELER MARKET, BY COUNTRY, 2025-2032 (THOUSAND UNITS)

- TABLE 196 ASIA PACIFIC: ELECTRIC TWO WHEELER MARKET, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 197 ASIA PACIFIC: ELECTRIC TWO WHEELER MARKET, BY COUNTRY, 2025-2032 (USD MILLION)

- TABLE 198 CHINA: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (UNITS)

- TABLE 199 CHINA: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (UNITS)

- TABLE 200 CHINA: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 201 CHINA: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 202 JAPAN: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (UNITS)

- TABLE 203 JAPAN: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (UNITS)

- TABLE 204 JAPAN: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 205 JAPAN: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 206 INDIA: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (UNITS)

- TABLE 207 INDIA: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (UNITS)

- TABLE 208 INDIA: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 209 INDIA: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 210 SOUTH KOREA: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (UNITS)

- TABLE 211 SOUTH KOREA: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (UNITS)

- TABLE 212 SOUTH KOREA: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 213 SOUTH KOREA: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 214 TAIWAN: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (UNITS)

- TABLE 215 TAIWAN: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (UNITS)

- TABLE 216 TAIWAN: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 217 TAIWAN: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 218 THAILAND: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (UNITS)

- TABLE 219 THAILAND: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (UNITS)

- TABLE 220 THAILAND: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 221 THAILAND: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 222 INDONESIA: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (UNITS)

- TABLE 223 INDONESIA: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (UNITS)

- TABLE 224 INDONESIA: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 225 INDONESIA: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 226 MALAYSIA: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (UNITS)

- TABLE 227 MALAYSIA: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (UNITS)

- TABLE 228 MALAYSIA: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 229 MALAYSIA: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 230 PHILIPPINES: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (UNITS)

- TABLE 231 PHILIPPINES: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (UNITS)

- TABLE 232 PHILIPPINES: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 233 PHILIPPINES: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 234 VIETNAM: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (UNITS)

- TABLE 235 VIETNAM: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (UNITS)

- TABLE 236 VIETNAM: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 237 VIETNAM: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 238 EUROPE: ELECTRIC TWO WHEELER MARKET, BY COUNTRY, 2021-2024 (THOUSAND UNITS)

- TABLE 239 EUROPE: ELECTRIC TWO WHEELER MARKET, BY COUNTRY, 2025-2032 (THOUSAND UNITS)

- TABLE 240 EUROPE: ELECTRIC TWO WHEELER MARKET, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 241 EUROPE: ELECTRIC TWO WHEELER MARKET, BY COUNTRY, 2025-2032 (USD MILLION)

- TABLE 242 FRANCE: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (UNITS)

- TABLE 243 FRANCE: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (UNITS)

- TABLE 244 FRANCE: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 245 FRANCE: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 246 GERMANY: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (UNITS)

- TABLE 247 GERMANY: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (UNITS)

- TABLE 248 GERMANY: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 249 GERMANY: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 250 SPAIN: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (UNITS)

- TABLE 251 SPAIN: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (UNITS)

- TABLE 252 SPAIN: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 253 SPAIN: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 254 AUSTRIA: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (UNITS)

- TABLE 255 AUSTRIA: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (UNITS)

- TABLE 256 AUSTRIA: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 257 AUSTRIA: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 258 UK: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (UNITS)

- TABLE 259 UK: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (UNITS)

- TABLE 260 UK: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 261 UK: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 262 ITALY: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (UNITS)

- TABLE 263 ITALY: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (UNITS)

- TABLE 264 ITALY: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 265 ITALY: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 266 BELGIUM: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (UNITS)

- TABLE 267 BELGIUM: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (UNITS)

- TABLE 268 BELGIUM: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 269 BELGIUM: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 270 NETHERLANDS: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (UNITS)

- TABLE 271 NETHERLANDS: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (UNITS)

- TABLE 272 NETHERLANDS: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 273 NETHERLANDS: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 274 POLAND: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (UNITS)

- TABLE 275 POLAND: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (UNITS)

- TABLE 276 POLAND: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 277 POLAND: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 278 DENMARK: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (UNITS)

- TABLE 279 DENMARK: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (UNITS)

- TABLE 280 DENMARK: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 281 DENMARK: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 282 NORTH AMERICA: ELECTRIC TWO WHEELER MARKET, BY COUNTRY, 2021-2024 (THOUSAND UNITS)

- TABLE 283 NORTH AMERICA: ELECTRIC TWO WHEELER MARKET, BY COUNTRY, 2025-2032 (THOUSAND UNITS)

- TABLE 284 NORTH AMERICA: ELECTRIC TWO WHEELER MARKET, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 285 NORTH AMERICA: ELECTRIC TWO WHEELER MARKET, BY COUNTRY, 2025-2032 (USD MILLION)

- TABLE 286 US: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (UNITS)

- TABLE 287 US: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (UNITS)

- TABLE 288 US: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 289 US: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 290 CANADA: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (UNITS)

- TABLE 291 CANADA: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (UNITS)

- TABLE 292 CANADA: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 293 CANADA: ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 294 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- TABLE 295 DEGREE OF COMPETITION, 2024

- TABLE 296 ELECTRIC TWO WHEELER MARKET: PRODUCT COMPARISON (KEY SCOOTER MODELS)

- TABLE 297 ELECTRIC TWO WHEELER MARKET: PRODUCT COMPARISON (KEY MOTORCYCLE MODELS)

- TABLE 298 ELECTRIC TWO WHEELER MARKET: REGION FOOTPRINT

- TABLE 299 ELECTRIC TWO WHEELER MARKET: VEHICLE TYPE FOOTPRINT

- TABLE 300 ELECTRIC TWO WHEELER MARKET: BATTERY TYPE FOOTPRINT

- TABLE 301 ELECTRIC TWO WHEELER MARKET, TECHNOLOGY TYPE FOOTPRINT

- TABLE 302 ELECTRIC TWO WHEELER MARKET: KEY STARTUPS/SMES

- TABLE 303 ELECTRIC TWO WHEELER MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 304 ELECTRIC TWO WHEELER MARKET: PRODUCT LAUNCHES/DEVELOPMENTS, JANUARY 2021-OCTOBER 2025

- TABLE 305 ELECTRIC TWO WHEELER MARKET: DEALS, JANUARY 2021- OCTOBER 2025

- TABLE 306 ELECTRIC TWO WHEELER MARKET: EXPANSIONS, JANUARY 2021- OCTOBER 2025

- TABLE 307 ELECTRIC TWO WHEELER MARKET: OTHER DEVELOPMENTS, JANUARY 2021- OCTOBER 2025

- TABLE 308 OLA ELECTRIC: COMPANY OVERVIEW

- TABLE 309 OLA ELECTRIC: PRODUCTS OFFERED

- TABLE 310 OLA ELECTRIC: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 311 OLA ELECTRIC: EXPANSIONS

- TABLE 312 OLA ELECTRIC: OTHERS

- TABLE 313 BAJAJ AUTO LTD.: COMPANY OVERVIEW

- TABLE 314 BAJAJ AUTO LTD.: PRODUCTS OFFERED

- TABLE 315 BAJAJ AUTO LTD.: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 316 TVS MOTOR COMPANY: COMPANY OVERVIEW

- TABLE 317 TVS MOTOR COMPANY: PRODUCTS OFFERED

- TABLE 318 TVS MOTOR COMPANY.: PRODUCT LAUNCHES/UPGRADES

- TABLE 319 TVS MOTOR COMPANY: DEALS

- TABLE 320 TVS MOTOR COMPANY: OTHERS

- TABLE 321 ATHER ENERGY: COMPANY OVERVIEW

- TABLE 322 ATHER ENERGY: PRODUCTS OFFERED

- TABLE 323 ATHER ENERGY: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 324 ATHER ENERGY: DEALS

- TABLE 325 YADEA TECHNOLOGY GROUP CO., LTD.: COMPANY OVERVIEW

- TABLE 326 YADEA TECHNOLOGY GROUP CO., LTD.: PRODUCTS OFFERED

- TABLE 327 YADEA TECHNOLOGY GROUP CO., LTD.: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 328 YADEA TECHNOLOGY GROUP CO., LTD.: DEALS

- TABLE 329 YADEA TECHNOLOGY GROUP CO., LTD.: EXPANSIONS

- TABLE 330 YADEA TECHNOLOGY GROUP CO., LTD.: OTHERS

- TABLE 331 HERO ELECTRIC: COMPANY OVERVIEW

- TABLE 332 HERO ELECTRIC: PRODUCTS OFFERED

- TABLE 333 HERO ELECTRIC: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 334 HERO ELECTRIC: DEALS

- TABLE 335 HERO ELECTRIC: EXPANSIONS

- TABLE 336 GOGORO: COMPANY OVERVIEW

- TABLE 337 GOGORO: PRODUCTS OFFERED

- TABLE 338 GOGORO: PRODUCT/TECHNOLOGY LAUNCHES

- TABLE 339 GOGORO: DEALS

- TABLE 340 VMOTO LIMITED: COMPANY OVERVIEW

- TABLE 341 VMOTO LIMITED: PRODUCTS OFFERED

- TABLE 342 VMOTO LIMITED: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 343 VMOTO LIMITED: DEALS

- TABLE 344 VMOTO LIMITED: EXPANSIONS

- TABLE 345 VMOTO LIMITED: OTHERS

- TABLE 346 NIU INTERNATIONAL: COMPANY OVERVIEW

- TABLE 347 NIU INTERNATIONAL: PRODUCTS OFFERED

- TABLE 348 NIU INTERNATIONAL: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 349 NIU INTERNATIONAL: DEALS

- TABLE 350 JIANGSU XINRI E-VEHICLE CO., LTD.: COMPANY OVERVIEW

- TABLE 351 JIANGSU XINRI E-VEHICLE CO., LTD.: PRODUCTS OFFERED

- TABLE 352 JIANGSU XINRI E-VEHICLE CO., LTD.: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 353 JIANGSU XINRI E-VEHICLE CO., LTD.: DEALS

- TABLE 354 JIANGSU XINRI E-VEHICLE CO., LTD.: EXPANSIONS

- TABLE 355 IDEANOMICS, INC.: COMPANY OVERVIEW

- TABLE 356 IDEANOMICS, INC.: PRODUCTS OFFERED

- TABLE 357 IDEANOMICS, INC.: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 358 IDEANOMICS, INC.: DEALS

- TABLE 359 IDEANOMICS, INC.: EXPANSIONS

- TABLE 360 ASKOLL EVA S.P.A.: COMPANY OVERVIEW

- TABLE 361 ASKOLL EVA S.P.A.: PRODUCTS OFFERED

- TABLE 362 ASKOLL EVA S.P.A.: DEALS

- TABLE 363 ASKOLL EVA S.P.A.: OTHERS

- TABLE 364 ULTRAVIOLETTE AUTOMOTIVE: COMPANY OVERVIEW

- TABLE 365 REVOLT INTELLICORP PRIVATE LIMITED (REVOLT MOTORS): COMPANY OVERVIEW

- TABLE 366 Z ELECTRIC VEHICLE: COMPANY OVERVIEW

- TABLE 367 CAKE: COMPANY OVERVIEW

- TABLE 368 LIGHTNING MOTORCYCLES: COMPANY OVERVIEW

- TABLE 369 JOHAMMER E-MOBILITY GMBH: COMPANY OVERVIEW

- TABLE 370 PIAGGIO GROUP: COMPANY OVERVIEW

- TABLE 371 KTM AG: COMPANY OVERVIEW

- TABLE 372 HARLEY DAVIDSON: COMPANY OVERVIEW

- TABLE 373 BMW GROUP: COMPANY OVERVIEW

- TABLE 374 AIMA TECHNOLOGY GROUP CO., LTD.: COMPANY OVERVIEW

- TABLE 375 HONDA MOTOR CO., LTD.: COMPANY OVERVIEW

- TABLE 376 GREAVES ELECTRIC MOBILITY PRIVATE LIMITED (AMPERE VEHICLES): COMPANY OVERVIEW

- TABLE 377 DONGGUAN TAILING ELECTRIC VEHICLE CO., LTD.: COMPANY OVERVIEW

- TABLE 378 CEZETA: COMPANY OVERVIEW

- TABLE 379 TERRA MOTORS CORPORATION: COMPANY OVERVIEW

- TABLE 380 NEXZU MOBILITY LTD. (AVAN MOTORS INDIA): COMPANY OVERVIEW

- TABLE 381 EMFLUX MOTORS: COMPANY OVERVIEW

- TABLE 382 MAHINDRA & MAHINDRA LTD.: COMPANY OVERVIEW

- TABLE 383 DAMON MOTORS INC.: COMPANY OVERVIEW

- TABLE 384 VIAR MOTOR INDONESIA: COMPANY OVERVIEW

- TABLE 385 SELIS: COMPANY OVERVIEW

- TABLE 386 GESITS: COMPANY OVERVIEW

- TABLE 387 UNITED E-MOTOR: COMPANY OVERVIEW

- TABLE 388 SMOOT ELEKTRIK: COMPANY OVERVIEW

- TABLE 389 PT VOLTA INDONESIA SEMESTA (VOLTA): COMPANY OVERVIEW

- TABLE 390 ALVA: COMPANY OVERVIEW

- TABLE 391 NUSA MOTORS: COMPANY OVERVIEW

- TABLE 392 BF GOODRICH: COMPANY OVERVIEW

List of Figures

- FIGURE 1 ELECTRIC TWO WHEELER MARKET SEGMENTATION & REGIONAL SCOPE

- FIGURE 2 ELECTRIC TWO WHEELER MARKET: RESEARCH DESIGN

- FIGURE 3 RESEARCH DESIGN MODEL

- FIGURE 4 KEY INSIGHTS FROM INDUSTRY EXPERTS

- FIGURE 5 RESEARCH METHODOLOGY: HYPOTHESIS BUILDING

- FIGURE 6 ELECTRIC TWO WHEELER MARKET: BOTTOM-UP APPROACH

- FIGURE 7 ELECTRIC TWO WHEELER MARKET: TOP-DOWN APPROACH

- FIGURE 8 DATA TRIANGULATION

- FIGURE 9 GROWTH PROJECTIONS FROM DEMAND-SIDE DRIVERS

- FIGURE 10 DEMAND- AND SUPPLY-SIDE FACTOR ANALYSIS

- FIGURE 11 KEY INSIGHTS AND MARKET HIGHLIGHTS

- FIGURE 12 STRATEGIES ADOPTED BY KEY PLAYERS IN ELECTRIC TWO WHEELER MARKET

- FIGURE 13 TRENDS AND DISRUPTIONS IMPACTING GROWTH OF ELECTRIC TWO WHEELER MARKET

- FIGURE 14 E-SCOOTER/MOPED SEGMENT TO HOLD LARGEST SHARE IN 2025

- FIGURE 15 ASIA PACIFIC TO BE LEADING REGIONAL MARKET DURING FORECAST PERIOD

- FIGURE 16 ADVANCEMENTS IN BATTERY TECHNOLOGY TO DRIVE MARKET

- FIGURE 17 ASIA PACIFIC TO ACCOUNT FOR DOMINANT MARKET SHARE IN 2025

- FIGURE 18 E-SCOOTER/MOPED SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 19 LITHIUM-ION SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 20 BELOW 75 MILES TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 21 HUB MOTOR SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 22 COMMERCIAL SEGMENT TO REGISTER HIGHER CAGR THAN PRIVATE SEGMENT DURING FORECAST PERIOD

- FIGURE 23 ECONOMY SEGMENT TO HOLD LARGER MARKET SIZE THAN LUXURY SEGMENT DURING FORECAST PERIOD

- FIGURE 24 PLUG-IN SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 25 ABOVE 3 KW SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 26 72 V SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 27 ELECTRIC TWO WHEELER MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 28 EVOLUTION OF BATTERY TECHNOLOGIES

- FIGURE 29 TECHNOLOGICAL BARRIERS FOR ELECTRIC TWO WHEELERS

- FIGURE 30 ELECTRIC TWO WHEELER MARKET: PATENT ANALYSIS, JANUARY 2015-OCTOBER 2025

- FIGURE 31 LEGAL STATUS OF PATENTS, 2015-2025

- FIGURE 32 SMART ELECTRIC VEHICLE CHARGING SYSTEM

- FIGURE 33 TCO OF ICE VS. BATTERY SWAPPING POWERED VEHICLES

- FIGURE 34 SMART IOT SOLUTION FOR ELECTRIC TWO WHEELER MANUFACTURERS

- FIGURE 35 TOTAL COST OF OWNERSHIP OF ELECTRIC VS. ICE SCOOTERS

- FIGURE 36 ELECTRIC TWO WHEELER MARKET: TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 37 AVERAGE SELLING PRICE TREND, BY VEHICLE TYPE, 2022-2024 (USD)

- FIGURE 38 AVERAGE SELLING PRICE TREND FOR ELECTRIC SCOOTERS, BY REGION, 2022-2024

- FIGURE 39 AVERAGE SELLING PRICE TREND FOR ELECTRIC MOTORCYCLES, BY REGION, 2022-2024

- FIGURE 40 ELECTRIC TWO WHEELER MARKET: ECOSYSTEM ANALYSIS

- FIGURE 41 ELECTRIC TWO WHEELER MARKET: SUPPLY CHAIN ANALYSIS

- FIGURE 42 INVESTMENT AND FUNDING SCENARIO, 2020-2024

- FIGURE 43 IMPORT DATA FOR HS CODE 871190, BY COUNTRY, 2021-2024 (USD MILLION)

- FIGURE 44 EXPORT DATA FOR HS CODE 871190, BY COUNTRY, 2021-2024 (USD MILLION)

- FIGURE 45 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR ELECTRIC TWO WHEELERS

- FIGURE 46 KEY BUYING CRITERIA

- FIGURE 47 ELECTRIC TWO WHEELER MARKET, BY VEHICLE TYPE, 2025 VS. 2032 (USD MILLION)

- FIGURE 48 ELECTRIC TWO WHEELER MARKET, BY VEHICLE CLASS, 2025 VS. 2032 (USD MILLION)

- FIGURE 49 ELECTRIC TWO WHEELER MARKET, BY VOLTAGE TYPE, 2025 VS. 2032 (USD MILLION)

- FIGURE 50 ELECTRIC TWO WHEELER MARKET, BY BATTERY TYPE, 2025 VS. 2032 (USD MILLION)

- FIGURE 51 ELECTRIC TWO WHEELER MARKET, BY DISTANCE COVERED, 2025 VS. 2032 (USD MILLION)

- FIGURE 52 ELECTRIC TWO WHEELER MARKET, BY USAGE, 2025 VS. 2032 (USD MILLION)

- FIGURE 53 ELECTRIC TWO WHEELER MARKET, BY TECHNOLOGY TYPE, 2025 VS. 2032 (USD MILLION)

- FIGURE 54 ELECTRIC TWO WHEELER MARKET, BY MOTOR TYPE, 2025 VS. 2032 (USD MILLION)

- FIGURE 55 ELECTRIC TWO WHEELER MARKET, BY MOTOR POWER, 2025 VS. 2032 (USD MILLION)

- FIGURE 56 ELECTRIC TWO WHEELER MARKET, BY REGION, 2025 VS. 2032

- FIGURE 57 ASIA PACIFIC: REAL GDP GROWTH RATE, BY COUNTRY, 2024-2026

- FIGURE 58 ASIA PACIFIC: GDP PER CAPITA, BY COUNTRY, 2024-2026

- FIGURE 59 ASIA PACIFIC: INFLATION RATE AVERAGE CONSUMER PRICES, BY COUNTRY, 2024-2026

- FIGURE 60 ASIA PACIFIC: MANUFACTURING INDUSTRY'S CONTRIBUTION TO GDP, 2024

- FIGURE 61 ASIA PACIFIC: ELECTRIC TWO WHEELER MARKET SNAPSHOT

- FIGURE 62 INDONESIA: ROADMAP FOR ELECTRIC MOTORCYCLE CHARGING INFRASTRUCTURE

- FIGURE 63 EUROPE: REAL GDP GROWTH RATE, BY COUNTRY, 2024-2026

- FIGURE 64 EUROPE: GDP PER CAPITA, BY COUNTRY, 2024-2026

- FIGURE 65 EUROPE: INFLATION RATE AVERAGE CONSUMER PRICES, BY COUNTRY, 2024-2026

- FIGURE 66 EUROPE: MANUFACTURING INDUSTRY'S CONTRIBUTION TO GDP, 2024

- FIGURE 67 EUROPE: ELECTRIC TWO WHEELER MARKET, BY COUNTRY, 2025 VS. 2032 (USD MILLION)

- FIGURE 68 NORTH AMERICA: REAL GDP GROWTH RATE, BY COUNTRY, 2024-2026

- FIGURE 69 NORTH AMERICA: GDP PER CAPITA, BY COUNTRY, 2024-2026

- FIGURE 70 NORTH AMERICA: CPI INFLATION RATE, BY COUNTRY, 2024-2026

- FIGURE 71 NORTH AMERICA: MANUFACTURING INDUSTRY'S CONTRIBUTION TO GDP, 2024

- FIGURE 72 NORTH AMERICA: ELECTRIC TWO WHEELER MARKET SNAPSHOT

- FIGURE 73 MARKET SHARE ANALYSIS OF ELECTRIC TWO WHEELER PROVIDERS, 2024

- FIGURE 74 REVENUE ANALYSIS OF TOP 5 PLAYERS, 2020-2024

- FIGURE 75 COMPANY VALUATION OF KEY PLAYERS, 2024

- FIGURE 76 FINANCIAL METRICS OF KEY PLAYERS, 2024

- FIGURE 77 ELECTRIC TWO WHEELER MARKET: COMPANY EVALUATION MATRIX, 2024

- FIGURE 78 ELECTRIC TWO WHEELER MARKET: COMPANY FOOTPRINT

- FIGURE 79 ELECTRIC TWO WHEELER MARKET: STARTUP/SME EVALUATION MATRIX, 2024

- FIGURE 80 OLA ELECTRIC: COMPANY SNAPSHOT

- FIGURE 81 OLA ELECTRIC: PRODUCT ROADMAP

- FIGURE 82 OLA ELECTRIC: MOVE OS FOR E2W

- FIGURE 83 BAJAJ AUTO LTD.: COMPANY SNAPSHOT

- FIGURE 84 TVS MOTOR COMPANY: COMPANY SNAPSHOT

- FIGURE 85 ATHER ENERGY: COMPANY SNAPSHOT

- FIGURE 86 ATHER ENERGY: PATENTS FILED ACROSS ELECTRIC TWO WHEELER DEVELOPMENT

- FIGURE 87 ATHER ENERGY: PRODUCT LAUNCH ROADMAP

- FIGURE 88 YADEA TECHNOLOGY GROUP CO., LTD.: COMPANY SNAPSHOT

- FIGURE 89 GOGORO: COMPANY SNAPSHOT

- FIGURE 90 VMOTO LIMITED: COMPANY SNAPSHOT

- FIGURE 91 NIU INTERNATIONAL: COMPANY SNAPSHOT

- FIGURE 92 NIU INTERNATIONAL: ORGANIZATIONAL STRUCTURE

- FIGURE 93 JIANGSU XINRI E-VEHICLE CO., LTD.: COMPANY SNAPSHOT

- FIGURE 94 ASKOLL EVA S.P.A.: COMPANY SNAPSHOT

全球电动两轮和三轮车市场:预测至2032年-按车辆类型、电池类型、马达类型、功率输出、充电基础设施、所有权模式、最终用户和地区进行分析

全球电动两轮和三轮车市场:预测至2032年-按车辆类型、电池类型、马达类型、功率输出、充电基础设施、所有权模式、最终用户和地区进行分析 电动机车市场按车辆类型、马达类型、最终用户和应用划分-2025-2032年全球预测

电动机车市场按车辆类型、马达类型、最终用户和应用划分-2025-2032年全球预测 全球摩托车车把市场2032 年亚太地区电动两轮车市场预测:按车辆类型、推进类型、电池类型、电压容量、电池容量、技术、最终用户和地区进行的全球分析全球电动两轮车市场全球电动两轮车零件市场

全球摩托车车把市场2032 年亚太地区电动两轮车市场预测:按车辆类型、推进类型、电池类型、电压容量、电池容量、技术、最终用户和地区进行的全球分析全球电动两轮车市场全球电动两轮车零件市场 电动两轮车市场规模、份额及成长分析(按车型、共享系统、电池、最终用途、经营模式和地区)-2025 年至 2032 年产业预测

电动两轮车市场规模、份额及成长分析(按车型、共享系统、电池、最终用途、经营模式和地区)-2025 年至 2032 年产业预测 日本电动两轮车市场规模、份额、趋势及预测(按车型、电池类型、电压类型、峰值功率、电池技术、马达布局和地区),2025 年至 2033 年电动两轮车共享市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

日本电动两轮车市场规模、份额、趋势及预测(按车型、电池类型、电压类型、峰值功率、电池技术、马达布局和地区),2025 年至 2033 年电动两轮车共享市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 亚太地区电动两轮车市场:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

亚太地区电动两轮车市场:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)