|

市场调查报告书

商品编码

1405081

Apron Bus:市场占有率分析、产业趋势/统计、成长预测,2024-2029Apron Bus - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

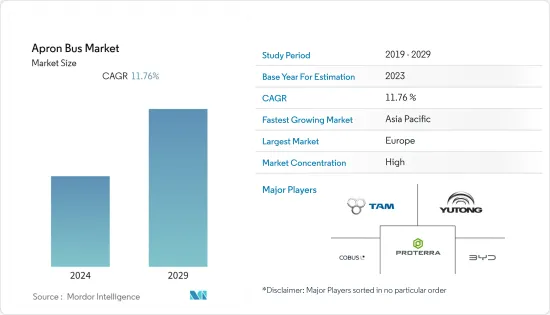

2024年,停机坪巴士市场价值为4.9797亿美元,预计到2029年将达到8.6836亿美元,预测期内复合年增长率为11.76%。

登机是飞机週转时间的关键流程之一,直接影响航空公司成本。停机坪巴士市场的主要成长要素之一是快速登机流程。停机坪巴士是将乘客从飞机运送到航站楼的绝佳选择,反之亦然,具体取决于机场。随着航空公司不断努力提高乘客满意度,他们需要加快办理登机手续的流程。旅客数量的增加以及航空公司持有的相应增加是市场成长的主要驱动力。另外,由于机场缺乏登机桥,有必要引进停机坪巴士。此外,它对加快登机过程和改善所有乘客舒适体验的贡献应该引起客户的注意。此外,越来越多的航空公司正在采用配备 Anaba 马达的电动巴士,以减少老化柴油引擎的排放。

为了主导市场,客车製造商正在转向全电动客车。预计新机场的建设将在预测期内进一步增加对停机坪巴士的需求。

停机坪巴士市场趋势

预计电动领域在预测期内将出现显着成长

预计在预测期内,电动市场将出现显着成长。这一增长是由旅客数量的增加和加强机场基础设施支出的增加所推动的。机场和航空公司正在努力透过采用先进的技术和系统来减少碳排放。在航站楼和飞机之间运送乘客的拖船、拖拉机和公共汽车等地面支援车辆也对机场总排放做出了重大贡献。航空公司和机场正在用新型电动巴士取代老化的柴油巴士,以实现碳中和。电动公车的优点是易于操作、维护成本低,最重要的是零排放。

过去十年,欧洲多个机场成功实现或减少了碳排放。随着世界各地的机场寻求在未来 30 年内将全球航空排放减少约一半,电动巴士产业将在未来几年加速成长。国际航空运输 CORSIA 二氧化碳抵销和减排计画旨在透过要求航空公司从 2020 年起减少未来排放的增加来稳定排放水准。根据预期参与情况,在 2021 年至 2035 年期间,该计划预计将抵消 2020 年水平以上排放的约 80%。第一阶段的参与是自愿的,但航空活动较少的国家除外。例如,Aviator Airport Alliance AB 设定了 2030 年达到净零排放的目标。该公司计划将永续燃料纳入其营运中,并将其地勤支援设备(GSE) 机群转变为电力。

欧洲占最高市场份额

欧洲在市场上占有最高份额,并将在预测期内继续占据主导地位。这一增长是由于机场建设计划的增加以及空中交通量增加对新停机坪巴士的需求增加所致。近年来,一些欧洲机场已用无排放电动巴士取代了柴油或燃气引擎的停机坪巴士,以减少碳排放。

提供 Apronbus 服务的欧洲机场包括慕尼黑、比萨、法兰克福、马德里、伦敦卢顿和阿姆斯特丹史基浦机场。例如,2021 年 9 月,英国布里斯托机场启用了电动停机坪巴士,以减少机场营运的排放。这辆电动巴士在航站楼和飞机之间运行,最多可运送 110 名乘客,由 COBUS Industries GmbH(德国)提供。这款全电动车配备了尖端功能,可最大限度地提高安全性和舒适性。机场将利用这次试运行来研究公车的营运效益,并将其与现有车队进行比较。同样,2023 年 6 月,Go-Ahead Group 投资 3,800 万美元建造氢巴士车队和加氢站,为伦敦盖特威克机场及其周边地区提供服务。

停机坪巴士产业概况

停机坪巴士市场因其性质而受到整合,因为它由少数现有公司主导。市场上的知名企业包括 COBUS Industries GmbH、宇通客车、比亚迪有限公司、Proterra Inc. 和 TAM-EUROPE。建造新机场或更新老化巴士为玩家提供了新的机会。客车製造商正在透过推出具有先进功能的新型客车来扩大产品系列,以赢得新合约。在全球范围内,随着航空公司寻求减少碳足迹,巴士製造商也在转向电动停机坪巴士,为乘客和行李提供更多空间。

例如,Quantron(德国)是「电动交通」领域的专家,提供各种类型的电动卡车和运输车,包括巴士。对于机场市场,我们提供多种用于餐饮、飞机供应/服务或道路清洁的车款。 2022 年 12 月,SpeediShuttle(美国美国)获得了一份航站楼间合同,在 Daniel K. Inouye 机场(美国美国)运营 Wiki Wiki Shuttle 服务。该服务是前往机场内行李提取区或其他航站楼的快速交通方式。 SpeediShuttle 计划推出管理系统,通知用户到达时间。此外,阿姆斯特丹史基浦机场计划于2023年3月进行自动驾驶巴士的试运行。该计划将由皇家史基浦集团与 NLMTD 和 TNW (The Next Web) 合作实施,以进一步加速机场的创新。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场概况

- 市场驱动因素

- 市场抑制因素

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家/消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

第五章市场区隔

- 类型

- 电动的

- 柴油引擎

- 地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 俄罗斯

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 其他亚太地区

- 拉丁美洲

- 巴西

- 墨西哥

- 其他拉丁美洲

- 中东/非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 埃及

- 南非

- 其他中东/非洲

- 北美洲

第六章竞争形势

- 供应商市场占有率

- 公司简介

- Yutong Bus Co., Ltd.

- COBUS Industries GmbH

- TAM-EUROPE

- BYD Company Ltd

- Xinfa Airport Equipment Ltd

- Proterra Inc.

- Xiamen King Long International Trading Co.,Ltd.

- Solaris Bus & Coach sp. z oo

- AB Volvo

- Ashok Leyland

- Mallaghan(GA)Inc

第七章 市场机会及未来趋势

The Apron Bus Market is valued at USD 497.97 million in 2024 and is expected to reach USD 868.36 million by 2029, registering a CAGR of 11.76% during the forecast period.

Boarding is one of the major processes of aircraft turnaround time with a direct influence on airline companies' costs. One of the main growth factors in the market for apron buses is the quicker boarding process. Apron buses are the best option at some airports to transport passengers from the plane to the terminal or vice versa. As airlines continuously strive for better passenger satisfaction, they must speed up the boarding process. The increasing air passenger traffic and the corresponding growth in airline fleets are the main drivers for the market growth. Also, the lack of available boarding bridges at airports is causing the need to introduce apron buses. In addition, the faster boarding process and its contribution to improving a comfortable experience for all passengers should attract customer attention. In addition, in order to limit emissions caused by the aging diesel engines on buses, a number of airlines are adopting an electrical bus equipped with Anaba's electronic motors.

In order to dominate the market, bus manufacturers are shifting toward all-electric buses. The construction of new airports is expected to further generate the demand for apron buses during the forecast period.

Apron Bus Market Trends

Electric Segment is Expected to Show Significant Growth During the Forecast Period

The electric segment is anticipated to show significant growth in the market during the forecast period. The growth is due to the increasing number of air passengers and growing spending on enhancing airport infrastructure. Airports and airlines are striving to reduce their carbon footprint by adopting advanced technologies and systems. Of the total emissions at airports, ground support vehicles, like tugs, tractors, and buses ferrying passengers between the terminals and the aircraft are also contributing significantly. Airlines and airports, in order to achieve carbon neutrality, are replacing aging diesel engine-powered buses with new electric buses. Electric buses offer advantages like ease of operation, low maintenance, and, most importantly, zero-emission.

Several airports across Europe were successful, over the past decade, in achieving or reducing their carbon footprint. As airports across the world are trying to reduce their global aviation emissions by about half over the next three decades, the electric bus segment will experience accelerated growth in the coming years. The CORSIA CO2 offset and reduction scheme for international air transport aims to stabilize emission levels by requiring airlines to mitigate the future growth of emissions after 2020. During the period 2021-2035, and based on expected participation, the scheme is estimated to offset around 80% of the emissions above 2020 levels. Participation of states in the first phase is voluntary, and there are exceptions for those with low aviation activity. For instance, Aviator Airport Alliance AB set itself a goal of becoming net zero by 2030. The authority plans to incorporate sustainable fuel into operations and transition its Ground Support Equipment (GSE) fleet to electric power. The company can confidently accomplish this objective.

Europe Holds Highest Shares in the Market

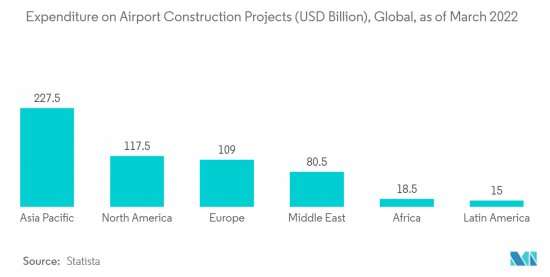

Europe holds the highest shares in the market and continue its domination during the forecast period. The growth is due to the increasing number of airport construction projects and rising demand for new apron buses due to increased air traffic. Several airports in Europe, in order to reduce their carbon footprint, replaced their diesel or gas-powered apron buses with emission-free electric buses in the past few years.

Some of the European airports that operate apron buses are Munich, Pisa, Frankfurt, Madrid, London Luton, and Amsterdam Schiphol, among others. For instance, in September 2021, Bristol Airport (UK) ordered an electric airside bus in a bid to reduce airport operating emissions. The electric bus, capable of transporting up to 110 passengers and operating between the terminal building and an aircraft, is supplied by COBUS Industries GmbH (Germany). The fully electric vehicle includes state-of-the-art features to maximize safety and comfort. The airport will use the trial to study the operating benefits of the bus and compare it to its existing fleet. Similarly, in June 2023, the Go-Ahead Group invested USD 38 million in a hydrogen bus fleet and refueling station for services in and around London Gatwick Airport.

Apron Bus Industry Overview

The apron bus market is consolidated in nature as a few established players dominate it. Some of the prominent players in the market are COBUS Industries GmbH, YUTONG, BYD Company Ltd, Proterra Inc., and TAM - EUROPE. The construction of new airports and the replacement of aging buses will offer new opportunities to the players. Bus manufacturers, in order to gain new contracts, are expanding their product portfolios by introducing new buses with advanced features. Globally, as the airlines look forward to reducing their carbon footprint, bus manufacturers are also shifting toward electric apron buses with increased space for passengers and their baggage.

For instance, Quantron (Germany) is a specialist in 'e-mobility,' offering electric trucks and transporters of various kinds, including buses. For the airport market, it provides a number of vehicle models for catering applications and aircraft supply/service or surface sweepers. In December 2022, SpeediShuttle (Hawaii, US) was awarded the interterminal contract to operate the Wiki Wiki Shuttle service within the Daniel K. Inouye Airport (Hawaii, US). Flyers use the service as a speedy way to get across the airport to baggage claim or a different terminal. SpeediShuttle will be implementing a management system that gives riders arrival times. Moreover, in March 2023, Amsterdam Schiphol Airport plans the trials of self-driving buses. The trials are a result of the Royal Schiphol Group teaming up with nlmtd and TNW (The Next Web) to further accelerate innovation at the airport.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Electric

- 5.1.2 Diesel

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 Germany

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Russia

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Australia

- 5.2.3.6 Rest of Asia-Pacific

- 5.2.4 Latin America

- 5.2.4.1 Brazil

- 5.2.4.2 Mexico

- 5.2.4.3 Rest of Latin America

- 5.2.5 Middle East & Africa

- 5.2.5.1 United Arab Emirates

- 5.2.5.2 Saudi Arabia

- 5.2.5.3 Egypt

- 5.2.5.4 South Africa

- 5.2.5.5 Rest of Middle East & Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share**

- 6.2 Company Profiles

- 6.2.1 Yutong Bus Co., Ltd.

- 6.2.2 COBUS Industries GmbH

- 6.2.3 TAM - EUROPE

- 6.2.4 BYD Company Ltd

- 6.2.5 Xinfa Airport Equipment Ltd

- 6.2.6 Proterra Inc.

- 6.2.7 Xiamen King Long International Trading Co.,Ltd.

- 6.2.8 Solaris Bus & Coach sp. z o.o.

- 6.2.9 AB Volvo

- 6.2.10 Ashok Leyland

- 6.2.11 Mallaghan (G.A.) Inc

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

按动力类型、巴士类型、容量、应用和销售管道分類的停机坪巴士市场 - 全球预测 2025-2032

按动力类型、巴士类型、容量、应用和销售管道分類的停机坪巴士市场 - 全球预测 2025-2032 全球月台巴士市场

全球月台巴士市场 空中停机坪巴士市场规模、份额、成长分析(按类型、按推进类型、按巴士尺寸、按自动化程度、按应用、按最终用途、按地区)- 产业预测 2025-2032

空中停机坪巴士市场规模、份额、成长分析(按类型、按推进类型、按巴士尺寸、按自动化程度、按应用、按最终用途、按地区)- 产业预测 2025-2032 站坪巴士市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

站坪巴士市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 停机坪巴士市场报告:至2030年的趋势、预测与竞争分析

停机坪巴士市场报告:至2030年的趋势、预测与竞争分析 停机坪巴士的全球市场预测(截至 2030 年):按巴士类型、设计、座位数、用途、最终用户和地区进行分析

停机坪巴士的全球市场预测(截至 2030 年):按巴士类型、设计、座位数、用途、最终用户和地区进行分析 停机坪巴士市场:现况分析与预测(2024-2032)

停机坪巴士市场:现况分析与预测(2024-2032) 全球停机坪巴士市场 2024-20312030 年停机坪巴士市场预测:按类型、运能、最终用户和地区分類的全球分析

全球停机坪巴士市场 2024-20312030 年停机坪巴士市场预测:按类型、运能、最终用户和地区分類的全球分析