|

市场调查报告书

商品编码

1406581

咨询服务:市场占有率分析、产业趋势/统计、成长预测,2024-2029Consulting Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

咨询服务市场规模预计将从2024年的3,238.8亿美元成长到2029年的4,318.9亿美元,预测期间(2024-2029年)复合年增长率为4.96%。

主要亮点

- 管理顾问公司提供帮助组织提高效率的服务。这些公司分析其业务并了解现有的组织效率低下的情况,从原材料成本到组织的人力资源政策。

- 由于欧洲市场经济的强劲成长、金融部门的监管改革、后端业务外包给低成本经济体以及公共投资,对管理咨询服务的需求不断增加。经济成长加速、数位咨询的兴起和全球化的兴起预计将在预测期内推动进一步成长。

- 许多公司不断寻求降低成本并提高效率,以便将成本节省惠及客户并在面临的激烈竞争中生存。因此,对业务流程改进和与业务效率相关的咨询的需求不断增加。英国脱欧和欧盟通用资料保护规范 (GDPR) 等监管变化正在推动主要服务领域的咨询需求。跨国公司寻求高价值的建议以遵守法规,从而推动了对管理咨询服务的需求。

- 计划日益复杂是咨询业面临的主要挑战。计划管理是咨询服务的核心,顾问公司依赖结构化的计划团队和强大的管理流程。导致计划复杂性的关键因素之一是保持成本和付加要素透明度的压力越来越大。

- COVID-19 的疫情促使全国各地的组织采取一切必要措施,确保员工和社区的安全。由于远距工作的增加和公司数位转型的扩大,COVID-19 的爆发使市场受益。公司希望业务流程无缝、高效且可从任何地方存取。

- 此外,许多公司已经完成了数位转型,并决定保持完全远端或混合模式运作。随着远距工作模式的扩展,企业正在增加向云端和人工智慧技术转型的投资,预计这将推动营运咨询服务市场的发展。

咨询服务市场趋势

生命科学和医疗保健增速最高

- 医疗保健咨询公司的角色是优化效率、产生收入和结构改进。这个角色有型态,从而催生了医疗保健咨询领域的各种专业化。在某些情况下,大型医疗机构选择咨询公司作为聘用者,并接受持续的评估和咨询服务,以提高长期绩效。对于有财力聘请多种咨询服务(包括业务、策略和技术咨询服务)的大型医疗保健组织来说尤其如此。

- 随着现代医疗基础设施、患者照护单位的开拓、政府投资以及医疗保健行业数位工具的集成,医疗保健行业的竞争逐渐变得更加激烈,从而产生了市场对战略咨询服务的需求。

- 医疗机构必须遵守营运法律准则,但仅获得一次许可证是不够的,因为法律法规不断变化。因此,在医疗保健领域,对法律咨询和咨询服务的需求不断增长,以加强日常业务、患者资讯管理和治疗合同,为普华永道和安永等供应商创造了商机。

- 此外,GE Healthcare 和Siemens Healthineers 等医疗技术和设备公司正在实施数位化策略,以提高工厂效率,为咨询服务创造机会。例如,2023年8月,塔塔咨询服务公司(TCS)赢得了GE医疗科技公司的合同,透过咨询和工程专业知识帮助医疗保健公司转变其IT营运模式,这表明市场对医疗保健领域技术咨询服务的需求。

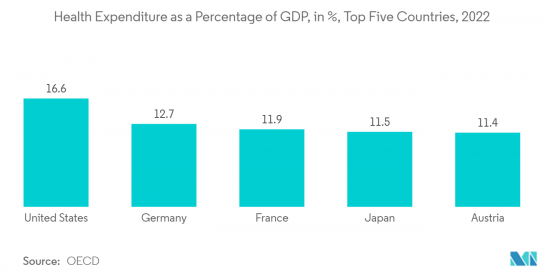

- 该市场拥有支持其成长的合作伙伴关係和收购。这是因为该市场的供应商正在与分析公司合作,以增强他们在医疗保健领域的咨询和咨询服务的能力。此外,美国和德国等国家将其GDP的10%以上用于医疗保健,这表明他们正在优先考虑医疗保健产业的未来成长。

北美市场占有率最大

- 美国是世界上最大的咨询服务市场,因为它是为广泛的最终用户行业提供服务的全球顶级咨询公司的所在地。此外,美国经济市场的高度波动,加上政府监管的持续改革,导致企业转向管理咨询提供者寻求其国内财务业务的协助。

- 美国也是市场先驱,在将技术进步推向全球市场方面发挥着重要作用。麦肯锡公司、科尔尼公司、波士顿顾问公司和贝恩公司等美国咨询服务提供者是美国市场上的顶级供应商。

- 该国的高创新率和先进技术的采用也支持了对技术咨询的需求。此外,该国的顾问公司正致力于建立合作伙伴关係,提供特定行业的咨询服务,这正在迅速推动市场发展。

- 加拿大也是全球咨询服务提供者的重要市场。该国越来越多地采用数位服务以及许多美国咨询公司的存在也激励许多本地供应商扩大其业务。

- 自疫情爆发以来,数位转型已成为各行业的首要任务,大多数最终用户供应商都在寻找新的方法来利用技术来获得竞争优势。由于政府投资和对数位化效率计画的承诺,医疗保健製药和生技领域的咨询服务市场也呈现成长。

- 此外,国内咨询服务公司正在加强技术和IT咨询服务,以有效挖掘业务数位转型的机会。预计这将在预测期内为该国的技术咨询服务创造重大成长机会。

咨询服务业概况

咨询服务市场的特点是适度分散,国内外参与者都拥有数十年的产业经验。这些供应商利用其专业知识并在广告工作中投入大量资源,采用强而有力的竞争策略。影响赢得新契约的主要因素包括品质认证、服务内容、成本和技术力。总而言之,该市场竞争对手之间的竞争非常激烈,预计这种趋势将在整个预测期内持续下去。市场上的知名参与者包括德勤Tohmatsu、Accenture公司、普华永道会计师事务所、安永国际有限公司和Capgemini SA公司。

2023 年 5 月,贝恩公司发布了与 Ashling Partners(专注于自动化的咨询和实施服务提供者)建立合作伙伴关係的策略公告。此外,贝恩将直接投资 Ashling Partners,加强贝恩 Vector Digital 业务内部的合作。此次扩大的合作伙伴关係旨在帮助客户更有效、更快速地开发、建立和扩展其自动化程序,从而充分发挥其潜力和价值。

2023 年 1 月,麦肯锡宣布收购人工智慧和机器学习专家 Iguagio。这项收购不仅让麦肯锡获得了 Iguagio 的技术,还增加了一支由 70 多名资料和人工智慧专家组成的团队。因此,麦肯锡将能够显着加速和扩大人工智慧的采用,为我们的客户带来更大的影响。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- 评估 COVID-19 对产业的影响

- 产业生态系统分析

- 区域重点热点

- 工业4.0和数位转型对咨询服务市场的影响

- 数位化在咨询服务市场中的作用分析

- 管理顾问领域常见的经营模式

第五章市场动态

- 市场驱动因素

- 扩大对新兴技术的投资

- 市场挑战

- 计划复杂性不断增加,咨询市场不断变化

第六章市场区隔

- 按服务类型

- 营运咨询

- 策略咨询

- 财务咨询

- 技术咨询

- 其他的

- 按最终用户产业

- 金融服务

- 生命科学/医疗保健

- 资讯科技/通讯

- 政府机关

- 活力

- 其他最终用户产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国(包括爱尔兰)

- 德国

- 法国

- 义大利

- 比荷卢经济联盟

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 其他亚太地区

- 中东/非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 卡达

- 南非

- 拉丁美洲

- 北美洲

第七章 竞争形势

- 公司简介

- Deloitte Touche Tohmatsu Limited

- Accenture PLC

- Pricewaterhousecoopers LLP

- Ernst & Young Global Limited

- Capgemini SE

- KPMG International

- Boston Consulting Group Inc.

- AT Kearney Inc(Kearney)

- Mckinsey & Company

- Bain & Company Inc.

- Roland Berger Holding Gmbh & Co. KGAA

- Simon-Kucher & Partners

- Oc&c Strategy Consultants LLP

第八章投资分析

第9章市场的未来

The consulting services market size is expected to grow from USD 323.88 billion in 2024 to USD 431.89 billion by 2029, at a CAGR of 4.96% during the forecast period (2024-2029).

Key Highlights

- Management consulting firms provide services that help organizations improve their efficiency. These firms analyze the operations and understand the existing organizational inefficiencies, ranging from the cost of raw materials to the HR policies in the organization.

- There is a growing need for management consulting services, owing to the strong economic growth in the European markets, the regulatory reforms in the financial sector, the outsourcing of back-end operations to low-cost economies, and public investments. Over the forecast period, faster economic growth, the emergence of digital consulting, and the rise of globalization are expected to drive further growth.

- Many companies are constantly trying to reduce costs and increase their efficiency to transfer the costs saved to the customer and withstand the intense competition they face. This leads to increased demand for business process improvisations and consulting related to operational efficiency. Regulatory changes, such as Brexit and the EU General Data Protection Regulation (GDPR), have increased demand for consulting across all major service lines. Multinational organizations seek high-value advice to comply with regulations, boosting the demand for management consulting services.

- The growing complexity of projects presents a significant challenge in the consulting industry. Project management is the core of consulting services, with consulting firms relying on well-organized project teams and robust management processes. One key factor contributing to project complexity is the mounting pressure to maintain transparency regarding costs and value-added components.

- The outbreak of COVID-19 prompted organizations across the country to undertake all the necessary steps to ensure the safety of their employees and the community. The COVID-19 pandemic benefited the market, owing to the rise in remote working and the expanding digital transformation of enterprises. Businesses are looking for business processes that are seamless, efficient, and accessible from any location.

- Furthermore, many businesses have completed their digital transformation, and many have decided to remain fully remote or operate on a digital and in-office hybrid model. With the growing remote working model, companies are increasing investments in the shift to cloud and AI-powered technologies, which is expected to boost the operations consulting services market.

Consulting Service Market Trends

Life Sciences and Healthcare to Witness the Highest Growth Rate

- The role of a healthcare consulting firm is to optimize efficiency, revenue generation, and structural improvements. This can take many forms, with various specializations emerging within the healthcare consulting sector. Some larger healthcare organizations could have a consulting firm on retainer and continuously receive evaluation and advisory services to improve performance over a longer period. This is especially the case with large healthcare organizations with the financial power to employ many types of consulting services, such as operational, strategy, and technology advisory services.

- The healthcare sector has been gradually becoming competitive with the development of modern healthcare infrastructure, patient care units, governmental investments, and the integration of digital tools in the healthcare sector, which would create a demand for strategy consultancy services in the market because, with diverse business knowledge and a deep understanding of, these service provider can guide healthcare facilities to target audience's pain points.

- Healthcare organizations should comply with legal guidelines to be operational, and getting a license once is not enough because the laws and regulations constantly change, which fuels the need for legal advisory consulting services in the healthcare sector which can enable the businesses to enhance their day-to-day operations, patient information management, treatment contracts, and would create an opportunity for the market vendors, including PWC, E&Y, among others.

- Additionally, healthcare technology and equipment firms, such as GE Healthcare and Siemens Healthineers, are implementing digital strategies in their operations to increase their plants' efficiency, which is creating opportunities for consulting services. For instance, in August 2023, Tata Consultancy Services (TCS) gained a contract from GE HealthCare Technologies Inc. to support the healthcare company in transforming its IT operating model through its consulting and engineering expertise, which shows the demand for technology consulting services in the healthcare sector in the market.

- The market has been witnessing partnerships and acquisitions, which are supporting growth because market vendors are partnering with analytical firms to increase their consulting and advisory services capabilities in the healthcare sectors. Additionally, countries such as the United States and Germany are spending more than 10% of their GDP on healthcare, which shows the priority on the future healthcare segment's growth, fueling the need for consulting services in the healthcare sector.

North America Holds Largest Market Share

- The United States is the world's largest revenue-generating consulting service market, owing to being the home of top global consultancy firms catering across a broad range of end-user verticals. Furthermore, the highly volatile marketplace across the US economy, along with the sustained reforms in government regulation, is driving companies to turn to management consulting providers for acquiring assistance in their financial operations across the country.

- The United States is also a pioneer in the market and plays a significant role in bringing technological advancement to the global market. The US-based consulting services providers, like McKinsey & Company, A. T. KEARNEY INC, the Boston Consulting Group, and Bain & Company, among others, are some of the top market vendors globally.

- The country's high rate of innovation and adoption of advanced technologies have also fueled the demand for technology consulting. In addition, consulting firms in the country are focusing on partnerships to offer industry-specialized consulting services, which drives the market rapidly.

- Canada is also a significant market for global consultancy service providers. The country's growing adoption of digital services and the presence of many US-based consultancy companies also motivated many local vendors to expand their presence.

- Since the pandemic, digital transformation has become a top priority across sectors, as most of the end-user vendors are finding new ways to use technology to gain a competitive edge. The consulting services market also witnessed growth in the healthcare pharma and biotech segments, which also benefited from government investment and commitment to digitized efficiency programs.

- Further, consulting service companies in the country are enhancing their technology and IT consulting services to capitalize on the opportunity of digital transformation of businesses effectively. This, in turn, is expected to create substantial growth opportunities for Technology consulting services in the country over the forecast period.

Consulting Service Industry Overview

The consulting services market is characterized by a moderate degree of fragmentation, featuring both local and international players boasting decades of industry experience. These vendors employ a potent competitive strategy by harnessing their expertise and allocating significant resources to advertising efforts. Key factors influencing their ability to attract new contracts include quality certification, service offerings, costs, and technical capabilities. In sum, the competitive rivalry in this market is notably intense, and this trend is expected to persist throughout the forecast period. Among the prominent players in the market are Deloitte Touche Tohmatsu Limited, Accenture PLC, PricewaterhouseCoopers LLP, Ernst & Young Global Limited, and Capgemini SE.

In May 2023, Bain & Company made a strategic announcement regarding their partnership with Ashling Partners, a consulting and implementation services provider specializing in automation. Additionally, Bain is making a direct investment in Ashling Partners to strengthen their collaboration within Bain's Vector digital practices. This expanded partnership aims to assist clients in more effectively and rapidly developing, building, and scaling their automation programs to unlock their full potential and value.

In January 2023, McKinsey & Company disclosed its acquisition of Iguazio, a company specializing in AI and machine learning. This acquisition not only grants McKinsey access to Iguazio's technology but also brings onboard a team of over 70 data and AI experts. As a result, McKinsey can significantly accelerate and scale its AI deployments, thereby driving greater impact for its clients

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Industry

- 4.4 Industry Ecosystem Analysis

- 4.5 Key Regional Hotspots

- 4.6 Impact of Industry 4.0 and Digital transformation -Related Practices on the Consulting Services Market

- 4.7 Analysis of the Role of Digitization in the Consulting Services Market

- 4.8 Prevalent Business Models in the Management Consulting Domain

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Investment in Emerging Technologies

- 5.2 Market Challenges

- 5.2.1 Project Complexities and Shift in Consulting Marketplace

6 MARKET SEGMENTATION

- 6.1 By Service Type

- 6.1.1 Operations Consulting

- 6.1.2 Strategy Consulting

- 6.1.3 Financial Advisory

- 6.1.4 Technology Advisory

- 6.1.5 Other Service Types

- 6.2 By End-user Industry

- 6.2.1 Financial Services

- 6.2.2 Life Sciences and Healthcare

- 6.2.3 IT and Telecommunication

- 6.2.4 Government

- 6.2.5 Energy

- 6.2.6 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom (Including Ireland)

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Italy

- 6.3.2.5 Benelux

- 6.3.2.6 Rest of Europe

- 6.3.3 Asia Pacific

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 Japan

- 6.3.3.4 Rest of Asia Pacific

- 6.3.4 Middle East & Africa

- 6.3.4.1 Saudi Arabia

- 6.3.4.2 United Arab Emirates

- 6.3.4.3 Qatar

- 6.3.4.4 South Africa

- 6.3.5 Latin America

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Deloitte Touche Tohmatsu Limited

- 7.1.2 Accenture PLC

- 7.1.3 Pricewaterhousecoopers LLP

- 7.1.4 Ernst & Young Global Limited

- 7.1.5 Capgemini SE

- 7.1.6 KPMG International

- 7.1.7 Boston Consulting Group Inc.

- 7.1.8 A. T. Kearney Inc (Kearney)

- 7.1.9 Mckinsey & Company

- 7.1.10 Bain & Company Inc.

- 7.1.11 Roland Berger Holding Gmbh & Co. KGAA

- 7.1.12 Simon-Kucher & Partners

- 7.1.13 Oc&c Strategy Consultants LLP

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

拉丁美洲供应链咨询服务:市场占有率分析、行业趋势和成长预测(2025-2030 年)

拉丁美洲供应链咨询服务:市场占有率分析、行业趋势和成长预测(2025-2030 年) 零售咨询市场按服务类型、应用、零售类型和公司规模划分 - 2025-2030 年全球预测

零售咨询市场按服务类型、应用、零售类型和公司规模划分 - 2025-2030 年全球预测 2025年全球企业敏捷转型服务市场报告2025年全球IT咨询市场报告

2025年全球企业敏捷转型服务市场报告2025年全球IT咨询市场报告 全球行销咨询市场 2025-2029欧洲策略咨询服务:市场占有率分析、产业趋势与成长预测(2025-2030 年)2025-2033 年企业敏捷转型服务市场(依方法、服务类型、组织规模、垂直产业和地区划分)亚太地区策略咨询服务:市场占有率分析、产业趋势与成长预测(2025-2030)北美策略咨询:市场占有率分析、产业趋势与成长预测(2025-2030)咨询服务技术市场 - 全球产业规模、份额、趋势、机会和预测,按服务类型、应用、地区和竞争细分,2019-2029F

全球行销咨询市场 2025-2029欧洲策略咨询服务:市场占有率分析、产业趋势与成长预测(2025-2030 年)2025-2033 年企业敏捷转型服务市场(依方法、服务类型、组织规模、垂直产业和地区划分)亚太地区策略咨询服务:市场占有率分析、产业趋势与成长预测(2025-2030)北美策略咨询:市场占有率分析、产业趋势与成长预测(2025-2030)咨询服务技术市场 - 全球产业规模、份额、趋势、机会和预测,按服务类型、应用、地区和竞争细分,2019-2029F