|

市场调查报告书

商品编码

1408442

6G -市场占有率分析、产业趋势与统计、2024年至2029年成长预测6G - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

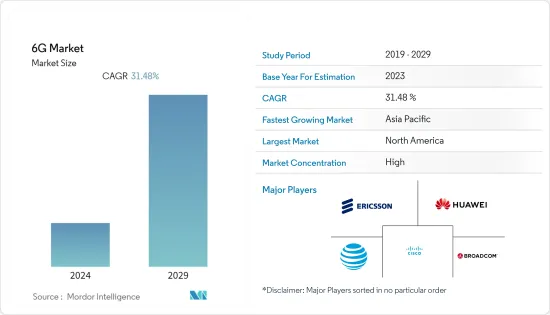

预计6G市场在预测期内的复合年增长率将达到31.48%。

主要亮点

- 6G 预计将在 2030 年代推出,其基础是 5G 高端功能在社交、消费者和工业用例中实现行动连接的突破。透过整合数位世界和物理世界,6G 将透过多感官扩增实境、精准医疗、智慧农业协作机器人和智慧型自主系统等新应用,打造一个更创新、永续和高效的社会,预计将做出贡献。

- 物联网和加密货币等新兴技术对连接的重视以及对 6G通讯的需求不断增加,是促进该行业成长的关键因素。高速互联网和远端连接是6G技术的基本特征,其采用将促进这些通讯技术的商业化。

- 快速都市化和通讯现已成为人类营养的基本权利,并可能在塑造市场方面发挥重要作用。大量人口已经迁移到大城市,以寻求更多机会和更好的生活。通讯和连接将在这一转变中发挥关键作用。此外,6G技术的采用也将受到智慧城市扩张和支持都市区人口成长的努力的严重影响。

- 6G 可能会建立在 5G 初步成功的基础上,以确保物联网设备和网路的可靠性。此外,6G的到来将伴随着自动化和智慧型设备水准的显着提高,例如生产现场的仓库机器人,因为与5G相比,6G具有更低的延迟和更高的资料负载。

- 此外,为了促进 5G 生态系统的发展并支持欧洲的 6G 研究,智慧网路服务营业单位选择了 35 个研发和试点计划的初始组合。其目标是在先进5G系统领域打造一流的欧洲供应链,并建立欧洲6G技术能力。这些投资显着提高了市场成长率。

6G市场趋势

对资料的需求增加

- 分析了由于多种数位技术和行动装置的引入而产生大量资料而导致的资料需求的增加,从而为6G市场创造了巨大的需求。

- 此外,随着行动资料消耗的增加,6G基础设施的部署和扩展对于支援不断增长的资料流量和提供增强的行动连线变得至关重要。例如,根据爱立信的报告,截至年终,不包括固定无线存取(FWA)流量的全球行动资料总流量达到每月93EB。到 2028 年,该流量预计将成长 3.5 倍,达到每月 329EB。预期的流量大幅成长凸显了对强大且先进的基础设施(例如 6G 网路)的需求,以满足对行动资料服务不断增长的需求。

- 预测期内流量成长的预测是基于 AR、VR 和混合实境(MR) 等 XR 类服务将在预测期结束时首先推出的假设。此外,云端处理服务的采用正在各行业中迅速扩大。云端基础的应用程式需要高速连接来存取和处理储存在远端位置的资料。

- 此外,物联网领域的成长是资料需求的关键驱动因素之一。例如,增加网路容量将加速MassiveIoT技术的成长,使其能够透过频谱共享与4G和5G共用,以及频谱分割频宽duplexFDD,甚至与6G一起实现更快的速度成为可能。

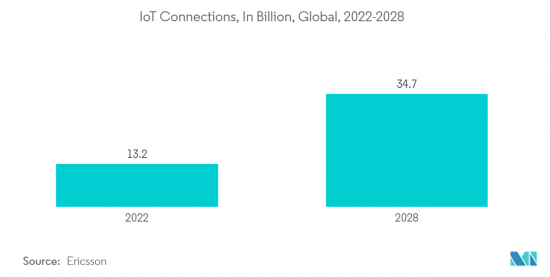

- 此外,爱立信预计,到 2030 年,连网装置数量将超过 500 亿台。透过解决所有连接问题,6G 有望释放物联网的潜力并为智慧城市提供动力。

分析显示北美占最大市场份额

- 在北美,美国是5G和6G市场的主要创新者和投资者之一。该国的通讯业占全球5G技术消耗的大部分。

- 美国在地区5G市场的投资、部署和应用方面也占据主导地位。包括AT&T、Verizon和T-Mobile在内的美国通讯业者已与爱立信、三星、诺基亚、华为和中兴通讯等网路设备供应商签署了10亿美元的协议,建设美国的5G和6G网路基础设施。我在这里。

- 此外,2023年4月,美国商务部长正式推出了15亿美元的公共无线供应链创新基金,用于建立开放和互通性的网路。透过展示新的无线网路开放架构方法的可行性,第一轮资金筹措确保 5G 和下一代无线技术的未来将由美国及其全球盟友和合作伙伴共同建造。我认为这将有助于确保那。创新基金是日本和美国立法努力的成果,旨在开发开放、可互通的无线网络,以加强安全、竞争和永续的全球供应链。

- 2023 年 4 月,白宫与商界领袖、技术代表和学术专家进行了磋商,制定了未来 6G 网路的策略。儘管 6G 技术仍处于起步阶段,距离广泛普及可能还需要数年时间,但预计其速度将明显快于目前的 5G 网络,并大幅提高全球的高速互联网接入。

- 此外,投资的增加也拉动了市场的成长速度。例如,2022 年 12 月,高级无线研究平台 (PAWR)计划办公室宣布获得美国国家科学基金会(NSF) 的 280 万美元投资,用于加速 5G、6G 及更高技术的无线创新。 。这项新资源反映了世界各地的研究人员对无线研究设施日益增长的兴趣,并强调了增加对先进和动态测试环境的访问的计划的需求。

6G产业概况

6G 技术市场预计将显着成长,迫使企业合作并制定有凝聚力的策略,以在这个竞争激烈的领域保持竞争力。这些公司经常建立合资企业(称为合资计划),以共用产品系列併寻求额外资源来实现其目标。这些努力将促进资源共用并加速进展。值得注意的是,6G 市场由大公司主导,这些公司正在大力投资开发,并着眼于未来的商业部署。

2022 年 11 月,NTT DoCoMo 与韩国 SK Telecom (SKT) 宣布建立战略合作伙伴关係,旨在推进 5G 和 6G 蜂窝技术。两家公司之间的合作也扩展到开放和虚拟无线接取网路(RAN)技术的开发。此举符合不断变化的全球形势,因为各个地区都在为部署下一代蜂窝技术做好准备。

2022年11月,爱立信承诺在该国建立一个新的研究团队,作为数百万英镑投资的一部分,共同努力加强英国的无线通讯能力。未来 10 年,爱立信将向英国的一项致力于 6G 研究和突破性创新的计画投入 1000 万英镑。这项倡议凸显了 6G 技术在全球范围内日益增长的重要性。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 买方议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

- 产业价值链分析

- 影响市场的宏观经济因素

第五章市场动态

- 市场驱动因素

- 对资料的需求增加

- 边缘运算

- 市场抑制因素

- 由于网路架构模型部署和频谱挑战,初始资本投资较高

第六章市场区隔

- 按设备

- 行动装置

- 物联网和边缘运算设备

- 其他设备

- 按行业分类

- 农业

- 车

- 医疗保健

- 政府机关

- 製造业

- 按行业分類的其他最终用户

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 其他的

第七章 竞争形势

- 公司简介

- AT&T

- Broadcom

- Cisco

- Ericsson

- Huawei

- Nokia

- NTT Docomo

- Orange

- NEC Corporation

第八章投资分析

第九章 市场机会及未来趋势

The 6G market is expected to register a CAGR of 31.48% during the forecast period.

Key Highlights

- 6G is anticipated to become available in the 2030s, building on societal, consumer, and industry use-case mobile connectivity breakthroughs enabled by the high-end capabilities of 5G. It is expected that 6G will contribute to a more innovative, more sustainable, and more efficient society with new uses for multisensory extended realities, precision health care, smart agricultural cobot, and intelligent autonomous systems by merging the digital and physical worlds.

- The increasing emphasis on connectivity and demand for 6G communication in newly developing technologies, e.g., the Internet of Things or cryptocurrencies, are significant factors contributing to the industry's growth. The introduction of high-speed Internet and remote connectivity, which are fundamental to the characteristics of 6G technologies, will be conducive to commercializing such communication technologies.

- Rapid urbanization and communication, now a fundamental right for human nutrition, will also play an essential role in shaping the market. A large population has already moved to the big cities for increased opportunities and better living. The critical role of communication and connectivity in this transition has been played. Moreover, the adoption of 6G technology will be significantly influenced by growing efforts toward supporting smarter cities and population growth in urban areas.

- In order to ensure the reliability of Internet of Things devices and networks, 6G will likely draw on the original success of 5G. Moreover, the emergence of 6G will coincide with a much larger level of automation and intelligent devices, such as warehouse robots at production sites, in view of its lower latency and higher data load compared to 5G.

- Further, to enable the development of 5G ecosystems and to support 6G research in Europe, the Smart Networks and Services Joint Undertaking selected its first portfolio of 35 R&I and trial projects. The objective is to create a first-class European supply chain in the field of advanced 5G systems as well as build Europe's capacity for 6G technology. These investments are significantly driving the market growth rate.

6G Market Trends

Increasing Data Demand

- The increasing data demand with the growing generation of high-volume data with the adoption of several digital technologies and mobile devices is analyzed to create significant demand for the 6G market.

- Further, as mobile data consumption grows, the deployment and expansion of 6G infrastructure become essential to support the increasing data traffic and deliver enhanced mobile connectivity. For instance, according to the Ericsson report, at the end of 2022, total global mobile data traffic, excluding traffic from fixed wireless access (FWA), reached 93 EB per month. By 2028, it is anticipated that this traffic will have increased by a factor of 3.5 to reach 329 EB per month. The anticipation of such significant traffic growth emphasizes the need for robust and advanced infrastructure, like 6G networks, to accommodate the rising demand for mobile data services.

- The estimation of the expected growth in traffic over the period is accompanied by an assumption that, at the end of the forecast period, there will be a first uptake of XR-type services such as AR, VR, and Mixed RealityMR. In addition, the adoption of cloud computing services is expanding rapidly across industries. Cloud-based applications require high-speed connectivity to access and process data stored remotely.

- Further, the growing IoT sector is one of the major contributors to the data demand. For instance, Adding network capacity will enhance the growth of MassiveIoT technologies and enable it to coexist with 4G and 5G in a spectrum division band duplexFDD as well as by sharing spectrum, and 6G could further enhance the speed.

- Furthermore, according to an Ericsson estimate, by 2030, there will be more than 50 billion linked devices. By addressing and resolving all connectivity concerns, 6G is anticipated to liberate the IoT's potential and serve as the driving force for the smart city.

North America is Analyzed to Hold Largest Share in the Market

- In North America, the US is one of the major innovators and investors in the 5G and 6G markets, owing to a high investment rate for advanced technological deployments. The telecom industry in the country accounts for a significant portion of the global consumption of 5G technology.

- Also, the US dominates the regional 5G market regarding investment, adoption, and applications. Telecom operators in the country, such as AT&T, Verizon, and T-Mobile, have made billion-dollar deals with network equipment vendors, such as Ericsson, Samsung, Nokia, Huawei, and ZTE, to build up their US 5G and 6G network infrastructure.

- Moreover, In April 2023, The US Secretary of Commerce officially launched a USD 1.5 billion public wireless supply chain innovation fund, which will be used to build Open and Interoperability networks. By demonstrating the viability of new, open-architecture approaches to wireless networks, this initial round of funding will help to ensure that the future of 5G and next-gen wireless technology is built by the US and its global allies and partners. The Innovation Fund is a result of the legislative efforts undertaken by both sides to develop Open and Interoperable Wireless Networks, which aim to enhance security, competitiveness, and sustainable worldwide supply chains.

- In April 2023, The White House consulted with business leaders, technology representatives, and experts in academia about developing strategies for the future 6G networks. Although 6G technologies are still in the early phases and likely years away from widespread use by the public, they are expected to become significantly faster than current 5G networks, as well as exponentially increasing high-speed internet access throughout the world.

- Moreover, the growing investments are also bolstering the market growth rate. For instance, in December 2022, The Platforms for Advanced Wireless Research (PAWR) Project Office announced an investment of USD 2.8 million from the US National Science Foundation (NSF) to accelerate wireless innovation in 5G, 6G, and beyond. The new resources reflect the growing interest of researchers around the world in wireless research facilities and highlight the need for programs to increase their access to advanced and dynamic testing environments.

6G Industry Overview

The 6G technology market is poised for significant growth, prompting companies to collaborate and devise cohesive strategies to stay competitive in this fiercely contested arena. Such enterprises, sharing a product portfolio and seeking additional resources to meet their goals, often engage in collaborative ventures, known as Joint Venture Programmes. These initiatives facilitate resource sharing and accelerate progress. Notably, the 6G market is dominated by major players making substantial investments in development, with an eye on future commercial deployment.

In November 2022, NTT DoCoMo and South Korea's SK Telecom (SKT) announced a strategic partnership aimed at advancing both 5G and 6G cellular technologies. Their collaborative efforts extend to the development of open and virtualized radio access network (RAN) technology. This move aligns with the evolving global landscape as various regions position themselves for the rollout of next-generation cellular technologies.

In November 2022, in a concerted effort to bolster the United Kingdom's wireless communications capabilities, Ericsson committed to establishing a new research team in the country as part of a multi-million-pound investment. Over the next decade, Ericsson plans to inject GBP 10 million into a UK-based program dedicated to 6G research and groundbreaking innovations. This initiative underscores the growing importance of 6G technology on a global scale.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Macro Economic Factors Impacting the market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Data Demand

- 5.1.2 Edge Computing

- 5.2 Market Restraints

- 5.2.1 High Initial Capital Expenditure due to Deployment of Network Architecture Model and Spectrum Challenges

6 MARKET SEGMENTATION

- 6.1 By Devices

- 6.1.1 Mobile Devices

- 6.1.2 IoT and Edge Computing Devices

- 6.1.3 Other Devices

- 6.2 By End-user Vertical

- 6.2.1 Agriculture

- 6.2.2 Automotive

- 6.2.3 Healthcare

- 6.2.4 Government

- 6.2.5 Manufacturing

- 6.2.6 Other End-user Verticals

- 6.3 By Region

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 AT&T

- 7.1.2 Broadcom

- 7.1.3 Cisco

- 7.1.4 Ericsson

- 7.1.5 Google

- 7.1.6 Huawei

- 7.1.7 Nokia

- 7.1.8 NTT Docomo

- 7.1.9 Orange

- 7.1.10 NEC Corporation

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

6G的全球市场(2026年~2046年)

6G的全球市场(2026年~2046年) 6G发展及商业化市场预测至2032年:全球应用情境、商业化战略、技术、应用、最终用户及区域分析

6G发展及商业化市场预测至2032年:全球应用情境、商业化战略、技术、应用、最终用户及区域分析 6G通讯的光和光电的机会:市场·技术 (2026-2046年)

6G通讯的光和光电的机会:市场·技术 (2026-2046年) 全球 6G 市场:依企业用途、使用情境和地区划分(至 2036 年)

全球 6G 市场:依企业用途、使用情境和地区划分(至 2036 年) 6G通讯的有希望材料·硬体设备·系统:市场·技术机会 (2026-2046年)

6G通讯的有希望材料·硬体设备·系统:市场·技术机会 (2026-2046年) 2025年6G全球市场报告

2025年6G全球市场报告 6G通讯:RIS (可重构智慧表面) 材料及硬体设备的市场与技术 (2026~2046年)2025年太空船自主全球市场报告

6G通讯:RIS (可重构智慧表面) 材料及硬体设备的市场与技术 (2026~2046年)2025年太空船自主全球市场报告 6G 技术市场(按组件、技术、通讯基础设施、应用和最终用户产业划分)—2025-2030 年全球预测

6G 技术市场(按组件、技术、通讯基础设施、应用和最终用户产业划分)—2025-2030 年全球预测 6G及其社会影响

6G及其社会影响