|

市场调查报告书

商品编码

1440304

包装:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

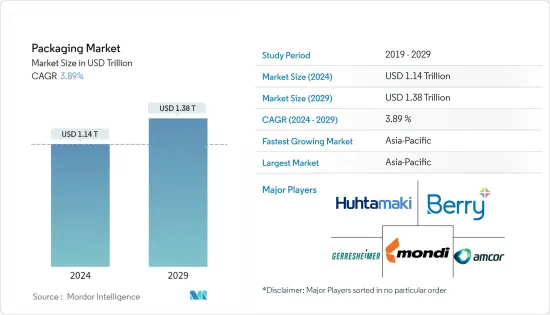

2024年包装市场规模预计为1.14兆美元,预计到2029年将达到1.38兆美元,在预测期内(2024-2029年)复合年增长率为3.89%增长。

由于基材选择的变化、新市场的扩张以及所有权关係的变化,全球包装业务在过去十年中经历了持续成长。传统包装可能会继续被软包装和高阻隔薄膜所取代,而立式杀菌袋有潜力与金属罐和玻璃瓶等硬包装形式竞争,适用于各种食品。

主要亮点

- 随着糖果零食和糖果零食产品消费量的增加,一些软质塑胶包装供应商正在提供专门满足这项需求的包装解决方案,进一步提高销售额和收益。例如,根据美国人口普查局的数据,到 2023 财年,美国糖果零食业收益预计将达到 108.9 亿美元。

- 根据软质包装协会统计,软质包装主要用于食品,占整个市场的60%以上。由于能够针对各种包装问题采用新的解决方案,软包装产业正在稳步成长。此外,根据 IBEF 的数据,印度的食品和杂货市场是全球第六大市场,零售额占销售额的 70%。印度食品加工业是该国最重要的产业之一,占全国食品市场总量的32%,在产量、消费和出口方面排名第五。

- 永续性趋势,包括 PET 的回收和生物分解性型态的使用,预计在预测期内将会增加。在某些方面,其生产的性质意味着它将始终面临永续性问题。然而,回收流和发展可以帮助解决此类永续性问题。例如,可口可乐的欧洲合作伙伴承诺到 2025 年在西欧收集 100% 的包装,并在宝特瓶使用 50% 的再生塑胶。百事可乐的目标是到 2025 年在欧洲生产的瓶子中使用 50% 的再生塑胶。 2030年,中期目标是到2025年约45%。各大食品製造商也面临来自活动人士和消费者的压力,现在他们的使命是重新思考塑胶包装并转向循环经济。例如,雀巢和亿滋最近签署了欧洲塑胶协议。该倡议的目标是到 2025 年使包装材料 100% 可回收或可重复使用,并减少原生塑胶的使用。

- 不同的公司都专注于产品创新,以便在所研究的市场中占有重要地位。例如,2021年2月,ConstantiaFlexibles推出了新产品Perpetua,这是一种用于药品的可回收阻隔性聚合物单材料包装解决方案。该公司表示,该解决方案与广泛的药品包装应用相容,目前在全球范围内销售。

- 许多供应商都致力于透过建造新的纸包装生产设施来扩大其市场份额。例如,2021年12月,罗马尼亚工业包装公司Promateris宣布将在该国建造生产设施,并于2022年进入纸包装领域。该计划预计将于2023年完工。此外,该公司计划于 2022 年开始生产以玉米粉为基础的生物分解性和可堆肥原料,成为东欧第一家这样做的公司。

- 然而,另一方面,不可回收和不可生物分解性的塑胶包装解决方案的整体使用正在增加,导致环境中的碳排放增加。这可能是限制市场成长的因素。因此,亚马逊、谷歌和利乐等许多大公司都以净零碳排放为目标,预计将转化为资本支出。

- 在COVID-19的影响下,无接触配送也成为新趋势。 Garcon Wines 等永续包装先驱有潜力适应这些新标准。 Garcon Wines 顺利供应信箱和平底酒瓶,需求量大。此外,COVID-19感染疾病的快速生产也增加了对玻璃容器和管瓶储存的需求。德国着名玻璃公司 Schott AG 到 2021 年 3 月已生产足够 10 亿剂 COVID-19感染疾病的管瓶,并且预计将生产超过 20 亿剂。该公司表示,大约 90% 的批准疫苗使用其硼硅酸管瓶,因为它们能够抵抗衝击和极端温度。

包装市场趋势

纸和纸板包装产品将经历最高成长

- 包装中越来越多地使用环保材料推动了市场的发展。环保包装可回收、生物分解性降解、可重复使用、无毒且对环境影响较小。纸袋、小袋和纸箱等纸包装产品是成长最快的永续包装材料。在线零售和有关非生物分解和不可回收包装解决方案的环境法规的日益增长的趋势正在逐渐创造对环保纸包装解决方案的巨大需求。

- 2021 年 2 月,可口可乐使用纸瓶测试了第一个试点,该纸瓶由非常坚固的纸壳和薄塑胶内衬组成。我们对 2,000 个瓶子进行了初步测试,看看它的耐用性。该公司的目标是製造 100% 可回收的无塑胶瓶,以防止气体从碳酸饮料中逸出。

- 此外,Smarties 等公司正在全球糖果零食业为糖果零食产品部署可回收纸包装。这意味着 Smarties 系列已完成 90% 的迁移。 10% 已采用可回收纸包装。此外,实现雀巢宏伟目标的重要一步是到 2025 年所有包装均采用纸质且可回收或可重复使用,从而将原始塑胶的使用量在同一时期减少三分之一。

- 纸包装市场的公司越来越重视永续包装解决方案,以满足消费者的需求。例如,芬兰食品包装专家 Huhtamaki Oyj 开发了 Huhtamaki Blue Loop,这是一个新平台,合作伙伴可以在该平台上进行协作并集思广益,讨论永续纸质包装。此类创新平台的引入正在导致市场扩张。

- 此外,各供应商正在采用并创新使用纸质包装材料的新包装,以减少包装对环境的影响并发起多项回收措施。例如,2021 年 2 月,利乐宣布与吉达穆罕默德迪亚区模型中心合作在吉达实施一项新措施。收集并回收用过的纸盒,以支持永续的消费习惯。

亚太包装市场显着扩张

- 塑胶包装在亚洲已被广泛使用,印度和中国等国家透过其食品和饮料市场做出了巨大贡献。中国的包装产业深受人口变数的影响,例如人均收入的增加、社会氛围的变化以及旨在最大限度地减少塑胶排放的禁塑措施。这对包装业务有重大影响。

- 中国在2021-2025年「五年计画」中宣布增加塑胶回收和焚烧能力,推广「绿色」塑胶产品,打击包装和农业领域的塑胶滥用。新的五年计画要求商店和快递公司减少「不合理」的塑胶包装,到2025年将都市区焚烧的垃圾量减少到每天80万吨左右(去年为58万吨)。数量增加。这些发展预计将增加国内对可回收软质塑胶包装的需求。阿里巴巴等电子商务巨头的崛起预计将在预测期内刺激包装市场。例如,在持续10天的阿里巴巴双11购物活动期间,中国消费者收到了约19亿件包裹。

- 包装是印度第五大产业,也是印度成长最快的产业之一。近年来,包装产业已成为该国技术和创新的主要推动力,为包括农业和日常消费品(日常消费品)产业在内的各个製造业领域创造价值。

- 印度包装研究所(IIP)的数据显示,过去十年,印度的包装消费量激增了200%,从2010年的每人每年4.3公斤pppa(pppa)增加到2020年的8.6公斤pppa。儘管过去十年快速成长,但与世界其他已开发地区相比,该行业仍存在巨大的成长空间。

- 日本是各种行业纸质产品的主要用户,包括报纸、包装、印刷和通讯、卫生产品以及各种其他应用。此外,由于消费者对永续包装的认识、对森林砍伐的担忧以及原材料的可用性,包装行业最近已转向使用纸张。

包装行业概况

主导全球包装市场的关键因素是透过创新实现的永续竞争优势、市场渗透水平、退出障碍、竞争策略广告支出的力量以及公司的集中度。这个市场的参与者透过创新拥有竞争优势。包装材料,特别是塑胶包装,规格不同,产品差异化的可能性很高。

- 2022 年 7 月 - Mondi 和 Fiorini International 合作,为义大利优质义式麵食产品製造商 Antico Pastificio Umbro 创建新的纸质包装解决方案。新包装完全可回收,在所有义式麵食产品中推广后,每年可节省多达 20 吨塑胶。

- 2022 年 6 月 - Coveris 扩大库夫施泰因工厂的产能。新的挤压设备最近全面运作,继续推进工厂的现代化工作,并显着提高青贮饲料包拉伸膜的生产率。

- 2022 年 6 月 - Ardagh Metal Packaging 宣布计划透过位于法国拉西约塔的新工厂扩大产能。该支出将得到 Sud Attractivite 和 Bpifrance 的支持,并将满足中东非洲 (MEA) 和西南部现有客户和新客户对长期合作伙伴关係不断增长的需求。

- 2022 年 4 月 - Sealed Air 推出数位包装品牌 PRISTIQ,提供设计服务、数位印刷和智慧包装解决方案组合,旨在消除浪费和过度包装,同时增强产品和客户参与。Masu。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章 简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 竞争对手之间存在敌对威胁

- 替代品的威胁

- 产业价值链分析

- 市场驱动因素(纸张和玻璃)

- 市场挑战(塑胶)

- 评估 COVID-19 对包装产业的感染疾病

- 全球主要国家人均包装消费量覆盖率

- 市场机会

第五章市场区隔

- 按包装类型

- 塑胶包装

- 单独的硬质塑胶包装

- 依材料类型- (PE-HDPE &LDPE, PP, PET, PVC, PS, EPS)

- 按产品类型 - (瓶子和罐子(容器)、瓶盖和盖子、散装级产品 - IBC、板条箱和托盘、其他)

- 按最终用户行业 -(食品、饮料、工业和建筑、汽车、化妆品和个人护理、其他最终用户行业)

- 独立软质塑胶包装

- 依材料类型-(PE、BOPP、CPP 等)

- 依产品类型 -(袋、袋、薄膜、包装纸)

- 按最终用户行业 -(食品、饮料、药品、化妆品、个人护理)

- 按地区 -(北美、欧洲、亚太地区、中东和非洲(海湾合作委员会、阿拉伯联合大公国、沙乌地阿拉伯、海湾合作委员会其他地区、中东其他地区)、拉丁美洲)

- 纸和纸板

- 依产品类型 -(折迭纸盒、瓦楞纸箱、免洗纸产品(袋子、杯子等))

- 依最终使用者(食品、饮料、工业和电子、化妆品和个人护理、医疗保健、其他(家庭用品、汽车零件、机械等的运输))

- 按地区 -(北美、欧洲、亚太地区、中东和非洲(海湾合作委员会、阿拉伯联合大公国、沙乌地阿拉伯、海湾合作委员会其他地区、中东其他地区)、拉丁美洲)

- 金属包装

- 依产品类型 -(罐头(食品、饮料、气雾剂、其他)、瓶盖和盖子、其他产品类型)

- 按地区 -(北美、欧洲、亚太地区、中东和非洲(海湾合作委员会、阿拉伯联合大公国、沙乌地阿拉伯、海湾合作委员会其他地区、中东其他地区)、拉丁美洲)

- 容器玻璃

- 按最终用户 -(食品、饮料(酒精、非酒精)、个人护理和化妆品、药品)

- 按地区 -(北美、欧洲、亚太地区、中东和非洲(海湾合作委员会、阿拉伯联合大公国、沙乌地阿拉伯、海湾合作委员会其他地区、中东其他地区)、拉丁美洲)

- 塑胶包装

第六章 竞争形势

- 公司简介-主要纸包装厂商分析

- International Paper Company

- Mondi Group

- Smurfit Kappa Group

- DS Smith PLC

- WestRock Company

- 公司简介-主要软质塑胶包装厂商分析

- UFlex Limited

- Huhtamaki OYJ

- Amcor PLC

- Coveris Holding SA

- Sealed Air Corporation

- 公司简介-主要硬质塑胶包装厂商分析

- Greif, Inc.

- Sonoco Products Company

- Aptar Group Inc.

- Berry Global Inc.

- Alpla Group

- 公司简介-主要容器玻璃製造商分析

- Owens-illinois, Inc.

- Vidrala, SA

- Verallia SA

- Gerresheimer AG

- Vitro, SAB De CV

- 公司简介-主要金属包装厂商分析

- Ball Corporation

- Crown Holdings, Inc.

- Ardagh Group SA

- Can Pack SA

- Silgan Holdings Inc.

第七章 投资分析

第八章 市场未来展望

The Packaging Market size is estimated at USD 1.14 trillion in 2024, and is expected to reach USD 1.38 trillion by 2029, growing at a CAGR of 3.89% during the forecast period (2024-2029).

The global packaging business has experienced consistent growth over the last decade due to substrate choice changes, expansion of new markets, and changing ownership dynamics. Traditional packaging may continue to be replaced by flexible packaging, high-barrier films, and stand-up retort pouches may challenge rigid pack formats like metal tins and glass jars for a wide range of food products.

Key Highlights

- With the rising consumption of sweets and confectionery, several flexible plastic packaging providers are offering packaging solutions, specifically catering to this demand, and are further driving their sales and revenues. For instance, according to the US Census Bureau, confectionery manufacturing industry revenue in the United States is expected to reach USD 10.89 billion by FY 2023.

- According to the Flexible Packaging Association, flexible packaging is mainly used for food, which accounts for more than 60% of the total market. Since it could incorporate new solutions for various packaging issues, the flexible packaging industry is experiencing robust growth. In addition, the Indian food and grocery market is the world's sixth-largest, according to IBEF, with retail accounting for 70% of sales. The Indian food processing industry, which contributes to 32% of the country's overall food market, ranks fifth in production, consumption, and export and is one of the country's most important industries.

- The sustainability trends, including recycling and using bio-degradable forms of PET, are expected to rise over the forecast period. In some regards, it will always face sustainability issues due to the nature of its production. However, the recycling streams and development will help neutralize such sustainability issues. For instance, the Coca-Cola European partners pledged to collect 100% of the packaging and use 50% recycled plastic in plastic PET bottles in Western Europe by 2025. PepsiCo aims to use 50% of recycled plastic in its bottles across the European region by 2030, with an interim target of around 45% by 2025. Also, various large food manufacturers are under pressure from campaigners and consumers and are currently on a mission to rethink their plastic packaging and move towards a circular economy. For instance, Nestle and Mondelez recently signed the European Plastics Pact. This initiative is committed to making 100% of packaging recyclable or reusable and reducing virgin plastic usage by 2025.

- Various companies focus on product innovations to hold a significant position in the studied market. For instance, in February 2021, Constantia Flexibles announced its new product, Perpetua, a recyclable, high-barrier, polymeric mono-material packaging solution for pharmaceutical products. According to the company, the solution has a wide range of pharmaceutical packaging applications and is now available worldwide.

- Various vendors have been focusing on expanding their market presence by constructing new production facilities for paper packaging. For instance, in December 2021, Promateris, a Romanian industrial packaging company, announced entering the paper packaging area in 2022 by building a production facility in the country. This project will be completed in 2023. Furthermore, in 2022, the firm expects to begin producing biodegradable and compostable raw materials based on corn starch, making it the first company to do so in Eastern Europe.

- However, on the other hand, the overall usage of non-recyclable, non-biodegradable plastic packaging solutions is expanding, resulting in increased carbon emissions in the environment. This might be a factor that could restrain the market growth. As a result, numerous large firms such as Amazon, Google, and Tetrapak, among others, are aiming toward net-zero carbon emissions, which is predicted to be their capital expenditure.

- During COVID-19, contactless delivery has also emerged as a new trend. Pioneers in sustainable packaging could adjust to these new standards, such as Garcon Wines, whose frictionless supply of letterbox- and climate-friendly flat wine bottles has witnessed a great demand. In addition, the rapid production of COVID-19 vaccines has also increased the need for glass containers or vials for storage purposes. By March 2021, Schott AG, a prominent German glass company, had produced enough vials for one billion COVID-19 vaccine doses, and it is on schedule to produce over two billion doses. According to the company, their borosilicate glass vials are used in roughly 90% of licensed vaccinations because they are resistant to shocks and temperature extremes.

Packaging Market Trends

Paper and Paperboard Packaging Products to Witness the Highest Growth

- The market is driven by the increased usage of environmentally friendly materials in packaging. Eco-friendly packaging is recyclable, biodegradable, reused, and non-toxic, with a low environmental impact. Paper packaging products, such as paper bags, pouches, and cartons, are the fastest-growing sustainable packaging materials. The increasing trend of online retail and environmental regulations on non-biodegradable and non-recyclable packaging solutions is progressively creating a massive demand for eco-friendly paper packaging solutions.

- In February 2021, Coca-Cola tested its first test run on paper bottles from an extra-strong paper shell containing a thin plastic liner. It ran its first test with 2,000 bottles to see how it held up. The company aims to create a 100% recyclable, plastic-free bottle to prevent gas from escaping from carbonated drinks.

- Moreover, companies such as Smarties have rolled out recyclable paper packaging for confectionery products worldwide in the confectionaries category. This would represent a transition of 90% of the Smarties range, as 10% was already packed in recyclable paper packaging. Further, Nestle's major step toward its ambition is to make all of its packaging paper-based and recyclable or reusable by 2025 and reduce the usage of virgin plastics by one-third in the same period.

- Companies in the paper packaging market are increasing their focus on sustainable packaging solutions that meet consumer demands. For instance, Huhtamaki Oyj, a Finland-based food packaging specialist, developed the Huhtamaki blue loop, a novel platform where partners can collaborate to brainstorm sustainable paper packaging. The introduction of such innovative platforms is leading to market expansion.

- Moreover, various vendors are adapting and innovating new packaging with paper packaging material to reduce the environmental impact of packaging and launch multiple recycling initiatives. For instance, in February 2021, TetraPak announced a new initiative in Jeddah in partnership with the District Model Center of Muhammadiyah in Jeddah. It will collect used carton packages and recycles them to support sustainable consumption practices.

Asia Pacific Packaging Market to Expand Significantly

- Plastic packaging has observed wide-scale utilization in Asia, with countries like India and China contributing significantly through their food and beverages market. The Chinese packaging sector is heavily influenced by variables such as rising per capita income, changing social atmosphere, and demographics, including ban enforcement on plastics to minimize its plastic footprint. This results in significant impacts on the packaging business.

- In a 2021-2025 "five-year plan," China announced it would improve its plastic recycling and incineration capacities, promote "green" plastic products, and combat the misuse of plastic in packaging and agriculture. The new five-year plan would push merchants and delivery companies to reduce "unreasonable" plastic wrapping and increase garbage incineration rates in cities to about 800,000 tons per day by 2025, up from 580,000 tons last year. Such developments are expected to increase the country's demand for recyclable flexible plastic packaging. Over the projection period, the rise of e-commerce giants like Alibaba is expected to fuel the packaging market. For example, Chinese shoppers received approximately 1.9 billion shipments during Alibaba's Double 11 shopping event, which lasted 10 days.

- Packaging is India's fifth-largest industry and one of the country's fastest-growing sectors. Over the last few years, the packaging industry has been a key driver of technology and innovation in the country, contributing value to various manufacturing sectors, including agriculture and the fast-moving consumer goods (FMCG) segments.

- According to the Indian Institute of Packaging (IIP), packaging consumption in India has surged by 200% over the last decade, from 4.3 kilograms per person per annum (pppa) in FY10 to 8.6 kg pppa in FY20. Despite the sharp increase over the last decade, there remains tremendous space for growth in this industry compared to other developed regions throughout the world.

- Japan is a major user of paper-based products in various industries, including newspaper, packaging, printing and communication, sanitary products, and other miscellaneous uses. Moreover, due to consumer awareness about sustainable packaging, worries about deforestation, and raw material availability, there has been a recent movement in the packaging sector to utilize paper.

Packaging Industry Overview

The significant factors governing the Global Packaging Market are sustainable competitive advantages through innovation, levels of market penetration, barriers to exit, advertising expense power of competitive strategy, and firm concentration ratio. The players in this market possess a competitive advantage through innovation. The specification of the packaging material is different, mostly in plastic packaging, leaving a high possibility of product differentiation.

- July 2022 - Mondi and Fiorini International teamed up to create a new paper packaging solution for Italian premium pasta product manufacturer Antico Pastificio Umbro. The new packaging is fully recyclable and, when rolled out across all pasta products, it could save up to 20 tons of plastic each year.

- June 2022 - Coveris expanded capacity at its Kufstein site. The new extrusion facility, which was recently put into full operation, continues the modernization efforts at the plant and significantly increases the production speed of stretch film for silage bales.

- June 2022- Ardagh Metal Packaging announced plans to expand its production capacity through a new facility at La Ciotat, France. The expenditure will be supported by Sud Attractivite and Bpifrance, catering to the increasing demands from existing and new customers for long-term partnerships in Middle East Africa (MEA) and Southwestern Europe.

- April 2022 - Sealed Air introduced PRISTIQ, a digital packaging brand with a portfolio of solutions for design services, digital printing, and smart packaging, eliminating waste and excess packaging while enhancing products and customer engagement.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Competitive Rivalry

- 4.2.5 Threat of Substitutes

- 4.3 Industry Value Chain Analysis

- 4.4 Market Drivers (Paper and Glass)

- 4.5 Market Challenges (Plastic)

- 4.6 Assessment of the Impact of COVID-19 on the Packaging Industry

- 4.7 Coverage of Per Capita Packaging Consumption in Major Countries Across the World

- 4.8 Market Opportunities

5 MARKET SEGMENTATION

- 5.1 By Packaging Type

- 5.1.1 Plastic Packaging

- 5.1.1.1 By Rigid Plastic Packaging

- 5.1.1.1.1 By Material Type - (PE - HDPE & LDPE, PP, PET, PVC, PS and EPS)

- 5.1.1.1.2 By Product Type - (Bottles and Jars (Containers), Caps and Closures, Bulk-Grade Products - IBC, Crates & Pallets, Others)

- 5.1.1.1.3 By End-User Industry - (Food, Beverage, Industrial and Construction, Automotive, Cosmetics and Personal Care, Other End-user Industries)

- 5.1.1.2 By Flexible Plastic Packaging

- 5.1.1.2.1 By Material Type - (PE, BOPP, CPP, Others)

- 5.1.1.2.2 By Product Type - (Pouches, Bags, Films and Wraps)

- 5.1.1.2.3 By End User Industry - (Food, Beverage, Pharmaceutical, Cosmetics and Personal Care)

- 5.1.1.3 By Region - (North America, Europe, Asia Pacific, Middle East and Africa (GCC, United Arab Emirates, KSA, Rest of GCC, Rest of Middle East and Africa), Latin America)

- 5.1.2 Paper and Paperboard

- 5.1.2.1 By Product Type - (Folding Carton, Corrugated Boxes, Single-use Paper Products (Bags, Cups, Others))

- 5.1.2.2 By End-user (Food, Beverage, Industrial & Electronic, Cosmetics & Personal Care, Healthcare, Others (Household Care, Transit (Transportation of Automobile Components, Machinery, etc.))

- 5.1.2.3 By Region - (North America, Europe, Asia Pacific, Middle East and Africa (GCC, United Arab Emirates, KSA, Rest of GCC, Rest of Middle East and Africa), Latin America)

- 5.1.3 Metal Packaging

- 5.1.3.1 By Product Type - (Cans (Food, Beverage, Aerosols, Others), Caps and Closures, Other Product Types)

- 5.1.3.2 By Region - (North America, Europe, Asia Pacific, Middle East and Africa (GCC, United Arab Emirates, KSA, Rest of GCC, Rest of Middle East and Africa), Latin America)

- 5.1.4 Container Glass

- 5.1.4.1 By End-user - (Food, Beverage (Alcoholic, Non-Alcoholic), Personal Care and Cosmetics, Pharmaceuticals)

- 5.1.4.2 By Region - (North America, Europe, Asia Pacific, Middle East and Africa (GCC, United Arab Emirates, KSA, Rest of GCC, Rest of Middle East and Africa), Latin America)

- 5.1.1 Plastic Packaging

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles - Analysis of the Major Paper Packaging Manufacturers

- 6.1.1 International Paper Company

- 6.1.2 Mondi Group

- 6.1.3 Smurfit Kappa Group

- 6.1.4 DS Smith PLC

- 6.1.5 WestRock Company

- 6.2 Company Profiles - Analysis of the Major Flexible Plastic Packaging Manufacturers

- 6.2.1 UFlex Limited

- 6.2.2 Huhtamaki OYJ

- 6.2.3 Amcor PLC

- 6.2.4 Coveris Holding SA

- 6.2.5 Sealed Air Corporation

- 6.3 Company Profiles - Analysis of the Major Rigid Plastic Packaging Manufacturers

- 6.3.1 Greif, Inc.

- 6.3.2 Sonoco Products Company

- 6.3.3 Aptar Group Inc.

- 6.3.4 Berry Global Inc.

- 6.3.5 Alpla Group

- 6.4 Company Profiles - Analysis of the Major Container Glass Manufacturers

- 6.4.1 Owens-illinois, Inc.

- 6.4.2 Vidrala, S.A.

- 6.4.3 Verallia SA

- 6.4.4 Gerresheimer AG

- 6.4.5 Vitro, S.A.B. De C.V.

- 6.5 Company Profiles - Analysis of the Major Metal Packaging Manufacturers

- 6.5.1 Ball Corporation

- 6.5.2 Crown Holdings, Inc.

- 6.5.3 Ardagh Group S.A.

- 6.5.4 Can Pack SA

- 6.5.5 Silgan Holdings Inc.

7 INVESTMENT ANALYSIS

8 FUTURE OUTLOOK OF THE MARKET

2024-2028 年全球快速消费品 (CPG) 市场

2024-2028 年全球快速消费品 (CPG) 市场 2030 年微波包装市场预测:按产品类型、材料、应用、最终用户和地区分類的全球分析

2030 年微波包装市场预测:按产品类型、材料、应用、最终用户和地区分類的全球分析 2024-2032 年糖果和麵包店包装市场报告(按类型(纸包装、玻璃包装、塑胶包装等)、应用(糖果、麵包店)和地区)

2024-2032 年糖果和麵包店包装市场报告(按类型(纸包装、玻璃包装、塑胶包装等)、应用(糖果、麵包店)和地区) 2024 年包装产品全球市场报告

2024 年包装产品全球市场报告 2024 年转换设备世界市场报告

2024 年转换设备世界市场报告 2030 年消失包装市场预测:按原料、最终用户和地区进行的全球分析

2030 年消失包装市场预测:按原料、最终用户和地区进行的全球分析 全球快速消费品 (CPG) 市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势与预测

全球快速消费品 (CPG) 市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势与预测 礼品包装市场:预测(2024-2029)

礼品包装市场:预测(2024-2029) 全球健康与卫生包装市场(~2028):产品类型(薄膜和片材、层压板、袋子和小袋、瓶子和罐子、香袋、标籤、管材、盒子和纸箱)、型态、出货型态、结构、最终用途(按行业) /地区

全球健康与卫生包装市场(~2028):产品类型(薄膜和片材、层压板、袋子和小袋、瓶子和罐子、香袋、标籤、管材、盒子和纸箱)、型态、出货型态、结构、最终用途(按行业) /地区 先进封装专利监测服务

先进封装专利监测服务