|

市场调查报告书

商品编码

1536892

界面活性剂:市场占有率分析、产业趋势/统计、成长预测(2024-2029)Surfactants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

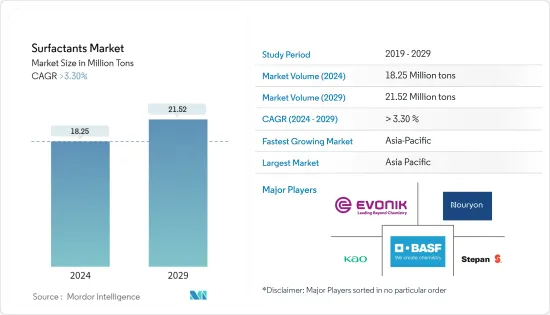

预计2024年全球界面活性剂市场规模将达到1825万吨,2024-2029年复合年增长率将超过3.30%,2029年将达到2152万吨。

主要亮点

- 短期内,个人护理和化妆品行业的崛起以及清洁剂和清洁剂製造中用量的增加预计将推动表面活性剂市场的成长。

- 然而,人们对使用界面活性剂的环保意识不断增强,预计将阻碍市场成长。

- 表面活性剂领域的新发明和生物基表面活性剂的引入可能会创造更多机会。

- 亚太地区在市场上占据主导地位,预计在预测期内仍将保持最高的复合年增长率。

表面活性剂市场趋势

阴离子界面活性剂可望主导市场

- 阴离子界面活性剂属于一类界面活性试剂,其中界面活性剂聚合物的头部保持带负电荷。这使其能够与悬浮在液体中的杂质和颗粒结合。

- 阴离子界面活性剂约占整个界面活性剂市场份额的一半。由于对环境法规的兴趣增加,预计对阴离子界面活性剂的需求将会增加。

- 阴离子界面活性剂广泛应用于工业及家庭清洗及农药配方。在阴离子界面活性剂中,生物分解性的直链烷基苯磺酸盐(LAS) 是最常见的,存在于污水系统和河水中。

- 阴离子界面活性剂最适合去除污垢、黏土和一些油性污渍。阴离子界面活性剂透过电离作用发挥作用。当添加到水中时,阴离子界面活性剂会电离并带有负电荷。带负电的界面活性剂与带正电的颗粒(例如黏土)结合。阴离子界面活性剂可有效去除颗粒污垢。

- 最常用的阴离子界面活性剂包括磺酸盐、醇硫酸盐、磷酸酯、烷基苯磺酸盐和羧酸盐。

- 阴离子界面活性剂因其优异的起泡、清洗、增稠、增溶、乳化、抗菌、渗透增强等特殊功效,在个人护理应用的护肤护髮产品中广受欢迎,化妆品的需求量日益增加。预计将提振需求。

- 目前,市场对环保替代品的需求正在推动对生物基阴离子界面活性剂的需求。

亚太地区预计将主导市场

- 在亚太地区,中国预计将主导市场。化妆品和个人护理品是中国成长最快的行业之一。人口持续增长也是推动该国个人护理、肥皂和清洁剂需求的一个因素,从而扩大了表面活性剂市场。

- 中国化学工业的产品对于肥皂、清洁剂和化妆品等多种产品至关重要。日本有60多家清洗剂、护理剂、清洁剂的製造商。然而,该市场由BASF公司和赢创工业公司等跨国公司主导。中国也是最大的肥皂和清洁剂产品出口国之一。

- 此外,印度也是世界上最大的肥皂生产国之一。印度人均香皂和沐浴皂消费量为800公克。印度约65%的人口居住在农村地区,可支配收入的增加和农村市场的成长正在推动消费者转向奢侈品。预计这一转变将推动印度表面活性剂市场的发展。

- 据印度品牌资产基金会称,到 2025 年,美容、化妆品和美容市场预计将达到 200 亿美元。

- 根据日本经济产业省统计,2022年国内生产总值为46,090吨,与前一年同期比较增加3%以上。

- 韩国的油漆和涂料市场是亚太地区第四大市场。 KCC、Samhwa Paints、Kangnam Jevisco(原 Kunsul Chemical Industrial Company,俗称 KCI)、Noroo Paints 和 Chokwang Paints 是主要的油漆和涂料製造商。他们主导着韩国涂料市场。

- 总体而言,预计该地区的表面活性剂市场在预测期内将稳定成长。

表面活性剂产业概况

界面活性剂市场高度分散,排名前五的公司占比重微乎其微。市场主要企业(排名不分先后)包括Nouryon、Evonik Industries AG、Kao Corporation、 BASF SE、Stepan Company等。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章 简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场驱动因素

- 个人护理和化妆品行业的全球需求不断增长

- 增加在清洁剂和清洁剂製造的使用

- 市场限制因素

- 环境问题和法规

- 其他阻碍因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 价格分析

第五章市场区隔(市场规模:数量)

- 按类型

- 阴离子界面活性剂

- 直链烷基苯磺酸盐(LAS 或 LABS)

- 醇乙氧基硫酸盐 (AES)

- α-烯烃磺酸盐(AOS)

- 二次性磺酸盐(SAS)

- 磺酸甲酯(MES)

- 磺基琥珀酸

- 其他阴离子界面活性剂

- 阳离子界面活性剂

- 季铵化合物

- 其他阳离子界面活性剂类型

- 非离子界面活性剂

- 醇乙氧基化物

- 乙氧基化烷基酚

- 脂肪酸酯

- 其他非离子表面活性剂

- 两性界面活性剂

- 硅胶表面活性剂

- 阴离子界面活性剂

- 按用途

- 家用肥皂和清洁剂

- 个人护理

- 润滑油/燃油添加剂

- 工业和设施清洗

- 食品加工

- 油田化学品

- 农业化学品

- 纤维加工

- 乳液聚合

- 其他用途

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 其他中东/非洲

- 亚太地区

第六章 竞争状况

- 併购、合资、联盟和协议

- 市场排名分析

- 主要企业策略

- 公司简介

- 3M

- Arkema

- Ashland

- BASF SE

- Bayer AG

- Cepsa

- Clariant

- Croda International PLC

- Dow Inc.

- Emery Oleochemicals

- Evonik Industries AG

- Galaxy Surfactants

- Geo Speciality Chemicals

- Godrej Industries Limited

- Huntsman International LLC

- Innospec

- Kao Corporation

- KLK Oleo

- Lankem

- Lonza

- Nouryon

- Oxiteno

- P&G Chemicals

- Reliance Industries Ltd

- Sanyo Chemical Industries Ltd

- Sasol

- Sinopec(China Petrochemical Corporation)

- Solvay

- Stepan Company

- Sulfatrade SA

- Sumitomo Chemical Co. Ltd

- Taiwan NJC Corporation Ltd

- TENSAC

- YPF SA

第七章 市场机会及未来趋势

- 扩大生物基界面活性剂的应用基础

- 特种表面活性剂应用的创新可能性

简介目录

Product Code: 56859

The Surfactants Market size is estimated at 18.25 Million tons in 2024, and is expected to reach 21.52 Million tons by 2029, growing at a CAGR of greater than 3.30% during the forecast period (2024-2029).

Key Highlights

- Over the short term, the rising personal care and cosmetic industry and the growing usage in the manufacturing of detergents and cleaners are expected to drive the growth of the surfactant market.

- However, the increasing environmental awareness against the use of surfactants is expected to hinder the growth of the market.

- New inventions in the field of surfactants and the introduction of bio-based surfactants are likely to create more opportunities.

- Asia-Pacific is expected to dominate the market, and it is likely to witness the highest CAGR during the forecast period.

Surfactants Market Trends

Anionic Surfactants are Expected to Dominate the Market

- Anionic surfactants belong to the class of surface-active reagents, in which the head of the surfactant macromolecule remains negatively charged. This allows it to bind to impurities and particles suspended in the liquid.

- Anionic surfactants account for approximately half of the total share of the surfactants market. A growing focus on environmental regulations is expected to increase the demand for anionic surfactants.

- Anionic surfactants are widely used for industrial and household cleaning and for pesticide formulations. Of the anionic surfactants, biodegradable linear alkylbenzene sulfonates (LAS) are the most common and can be found in wastewater systems and river water.

- Anionic surfactants work best to remove dirt, clay, and some oily stains. They work through ionization. When added to water, the anionic surfactants ionize and take a negative charge. The negatively charged surfactants bind to positively charged particles like clay. Anionic surfactants are effective in removing particulate soils.

- Some of the most used anionic surfactants are sulfonic acid salts, alcohol sulfates, phosphoric acid esters, alkylbenzene sulfonates, and carboxylic acid salts.

- The increasing demand for anionic surfactants in cosmetic products, such as skincare and hair care products in personal care applications, owing to their superior characteristics, such as foaming, cleansing, thickening, solubilizing, emulsifying, antimicrobial effects, penetration enhancement, and other special effects, is expected to boost the demand.

- The current market demand for environment-friendly alternatives has led to a boost in demand for bio-based anionic surfactants.

Asia-Pacific is Expected to Dominate the Market

- In Asia-Pacific, China is likely to dominate the market studied. In China, cosmetics and personal care are among the fastest-growing sectors. Continuous growth in population is another factor fuelling the demand for personal care, soaps, and detergents in the country, which augments the surfactants market.

- The output from the Chinese chemical industry is essential in various products, including soaps, detergents, cosmetics, etc. There are more than 60 manufacturers of washing, care, and cleaning agents in the country. However, the market studied is dominated by global players like BASF SE and Evonik Industries AG. China is also one of the largest exporters of soaps and detergent products.

- Moreover, India is one of the largest producers of soaps in the world. The per capita consumption of toilet/bathing soaps in the country is around 800 grams. Around 65% of the Indian population resides in rural areas, and the increasing disposable incomes and growth in rural markets make consumers shift to premium products. This shift is expected to drive the Indian surfactants market.

- According to the India Brand Equity Foundation, the beauty, cosmetic, and grooming market is expected to reach USD 20 billion by 2025.

- According to the Ministry of Economy, Trade and Industry (METI), Japan, in 2022, the total production of cationic surfactants in the country stood at 46.09 thousand metric tons, registering an increase of more than 3% compared to the previous year.

- The South Korean paint and coating market is the fourth-largest Asia-Pacific region. KCC, Samhwa Paints, Kangnam Jevisco (formerly Kunsul Chemical Industrial Company, popularly called KCI), Noroo Paints, and Chokwang Paints are the major paint and coating producers. They dominate the South Korean paint and coating market.

- Overall, the market for surfactants in the region is expected to witness steady growth during the forecast period.

Surfactants Industry Overview

The surfactants market is highly fragmented, with the top five companies accounting for a minimal share of the market. Some major players in the market (in no particular order) include Nouryon, Evonik Industries AG, Kao Corporation, BASF SE, and Stepan Company, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Growing Demand from the Personal Care and Cosmetics Industry Globally

- 4.1.2 Increasing Usage in Manufacturing of Detergents and cleaners

- 4.2 Market Restraints

- 4.2.1 Environmental Concerns and Regulations

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Price Analysis

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 By Type

- 5.1.1 Anionic Surfactants

- 5.1.1.1 Linear Alkylbenzene Sulfonate (LAS or LABS)

- 5.1.1.2 Alcohol Ethoxy Sulfates (AES)

- 5.1.1.3 Alpha Olefin Sulfonates (AOS)

- 5.1.1.4 Secondary Alkane Sulfonate (SAS)

- 5.1.1.5 Methyl Ester Sulfonates (MES)

- 5.1.1.6 Sulfosuccinates

- 5.1.1.7 Other Types of Anionic Surfactants

- 5.1.2 Cationic Surfactants

- 5.1.2.1 Quaternary Ammonium Compounds

- 5.1.2.2 Other Types of Cationic Surfactants

- 5.1.3 Non-ionic Surfactants

- 5.1.3.1 Alcohol Ethoxylates

- 5.1.3.2 Ethoxylated Alkyl-phenols

- 5.1.3.3 Fatty Acid Esters

- 5.1.3.4 Other Non-ionic Surfactants

- 5.1.4 Amphoteric Surfactants

- 5.1.5 Silicone Surfactants

- 5.1.1 Anionic Surfactants

- 5.2 By Application

- 5.2.1 Household Soaps and Detergents

- 5.2.2 Personal Care

- 5.2.3 Lubricants and Fuel Additives

- 5.2.4 Industry and Institutional Cleaning

- 5.2.5 Food Processing

- 5.2.6 Oilfield Chemicals

- 5.2.7 Agricultural Chemicals

- 5.2.8 Textile Processing

- 5.2.9 Emulsion Polymerization

- 5.2.10 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Ashland

- 6.4.4 BASF SE

- 6.4.5 Bayer AG

- 6.4.6 Cepsa

- 6.4.7 Clariant

- 6.4.8 Croda International PLC

- 6.4.9 Dow Inc.

- 6.4.10 Emery Oleochemicals

- 6.4.11 Evonik Industries AG

- 6.4.12 Galaxy Surfactants

- 6.4.13 Geo Speciality Chemicals

- 6.4.14 Godrej Industries Limited

- 6.4.15 Huntsman International LLC

- 6.4.16 Innospec

- 6.4.17 Kao Corporation

- 6.4.18 KLK Oleo

- 6.4.19 Lankem

- 6.4.20 Lonza

- 6.4.21 Nouryon

- 6.4.22 Oxiteno

- 6.4.23 P&G Chemicals

- 6.4.24 Reliance Industries Ltd

- 6.4.25 Sanyo Chemical Industries Ltd

- 6.4.26 Sasol

- 6.4.27 Sinopec (China Petrochemical Corporation)

- 6.4.28 Solvay

- 6.4.29 Stepan Company

- 6.4.30 Sulfatrade SA

- 6.4.31 Sumitomo Chemical Co. Ltd

- 6.4.32 Taiwan NJC Corporation Ltd

- 6.4.33 TENSAC

- 6.4.34 YPF SA

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Expansion of Application Base For Bio-based Surfactants

- 7.2 Possible Innovations in the Application of Specialty Surfactants

02-2729-4219

+886-2-2729-4219

胺基酸界面活性剂市场(按类型、形式和应用)-全球预测 2025-2030

胺基酸界面活性剂市场(按类型、形式和应用)-全球预测 2025-2030 全球胺基酸界面活性剂市场研究报告-产业分析、规模、份额、成长、趋势和预测 2025 年至 2033 年

全球胺基酸界面活性剂市场研究报告-产业分析、规模、份额、成长、趋势和预测 2025 年至 2033 年 2025 年全球糖基界面活性剂市场报告两性界面活性剂全球市场报告 2025特种界面活性剂市场 - 全球产业规模、份额、趋势、机会和预测,按类型、应用、地区和竞争细分,2020-2030 年预测

2025 年全球糖基界面活性剂市场报告两性界面活性剂全球市场报告 2025特种界面活性剂市场 - 全球产业规模、份额、趋势、机会和预测,按类型、应用、地区和竞争细分,2020-2030 年预测 全球酯基季铵盐市场:产业分析、规模、占有率、成长、趋势与预测(2025-2032 年)

全球酯基季铵盐市场:产业分析、规模、占有率、成长、趋势与预测(2025-2032 年) 北美界面活性剂:市场占有率分析、产业趋势与统计、成长预测(2025-2030)特种界面活性剂:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

北美界面活性剂:市场占有率分析、产业趋势与统计、成长预测(2025-2030)特种界面活性剂:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年) 酯基季铵盐市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测界面活性剂 EOR 市场:按类型、产地、类别、应用分类 - 2025-2030 年全球预测

酯基季铵盐市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测界面活性剂 EOR 市场:按类型、产地、类别、应用分类 - 2025-2030 年全球预测

▼