|

市场调查报告书

商品编码

1549845

可重复使用食品服务包装的全球市场:市场占有率分析、产业趋势/统计、成长预测(2024-2029)Reusable Foodservice Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

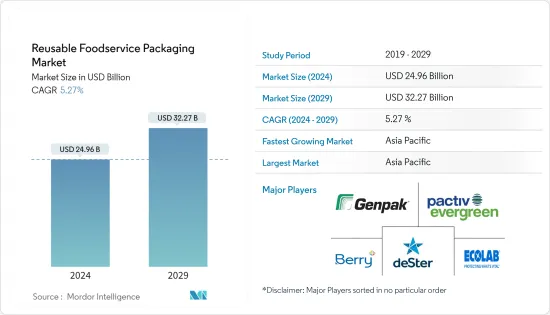

全球可重复使用食品服务包装市场规模预计到 2024 年为 249.6 亿美元,到 2029 年达到 322.7 亿美元,在预测期内(2024-2029 年)复合年增长率为 5.27%。

由于对耐用和永续物料输送解决方案的需求不断增长,全球可重复使用包装市场有望显着成长。可回收包装在永续性中发挥着至关重要的作用,并透过减少通常最终进入垃圾掩埋场的包装废弃物量而脱颖而出。

主要亮点

- 多样化的城市景观正在推动该国对方便、便携和轻质食品的需求。近年来,即食食品和方便食品已发展成为全球食品服务中最多样化的领域之一。随着环境问题的增加和垃圾掩埋场的掩埋废物迅速增加,饭店、全方位服务餐厅 (FSR) 和快餐餐厅 (QSR) 正在使用可重复使用的食品服务包装。

- 世界各地的多个政府机构对跨行业使用可重复使用包装制定了严格的指导方针。例如,SUP指令要求欧盟成员国积极减少一次性塑胶废弃物,并在地方和国家层级设定具体的减少目标。除了监管之外,这些国家还提倡使用可重复使用的食品包装来实现这些目标。

- 在法国,最近的立法要求店内的所有餐点和轻食都采用可重复使用的包装和餐具。

- 过去几年,线上食品订购和餐厅外送产业成长了 20%。随着线上食品配送系统变得越来越流行,对永续食品服务包装的需求也迅速增加。根据中国互联网络资讯中心2024年3月公布的数据显示,中国线上外送用户数量将从2020年的41883万增加到2023年的54454万。这种成长促使製造商将注意力转向环保、可重复使用的包装解决方案。

- 然而,工业食品应用中塑胶包装从一次性到可重复使用模式的转变可能会带来不可预见的挑战,特别是在卫生和感知方面。重复使用塑胶包装会带来增加化学污染和食品中存在微塑胶颗粒的风险。此外,包装产品的卫生标准和感知一致性可能会受到影响。

- 在全球范围内,大公司正在摆脱传统的「捕获、包装、丢弃」模式,转向零废弃物的生活方式。我们透过使其可重复使用来永续延长食品服务包装的生命週期来实现这一目标。这种转变不仅降低了与包装相关的营运成本,而且还消除了不断购买新包装的需要。

可重复使用食品服务包装的市场趋势

对快餐店 (QSR) 的需求不断增长推动市场发展

- 快餐店 (QSR) 注重服务速度并提供低成本的餐饮选择。它们与传统餐厅的不同之处在于,它们将餐桌服务降至最低限度并强调自助服务。在 QSR,您在享用食物和饮料之前先付款。在过去的十年中,多家国际快餐连锁店以及提供各种美食以满足不断变化的消费者偏好的本土品牌不断发展,特别是在这些国家的区域食品服务市场。

- 随着环境永续性意识的不断增强,一些主要的快餐连锁店越来越关注可回收性、可堆肥性和可重复使用的包装。汉堡王、麦当劳和温蒂等知名公司都宣布了对可重复使用包装的承诺。

- 例如,法国的麦当劳为用餐的顾客提供了21种可重复使用的容器。其中包括装炸薯条的红色塑胶容器、透明塑胶饮水杯和装鸡块的白色塑胶杯。

- 专利权模式对于快餐连锁店的崛起至关重要,预计将推动全球未来市场的成长。国际专利权协会公布的资料显示,截至 2024 年 4 月,美国快餐店数量在过去几年中稳步增长,在 COVID-19 大流行期间略有下降后,2020 年门市数量有所增加。人增至2023 年195,510 人。值得注意的是,估计表明,在预测期内,美国各地的快餐店数量预计将进一步增加。

- 此外,由于人们越来越偏好外出用餐,导致食品成本不断上涨,这推动了对快餐的需求,并推动了对可重复使用的食品服务包装的需求。根据英国国家统计局的数据,在疫情后时期,英国餐厅和咖啡馆的消费者支出激增至 1,328.9 亿英镑(1,695 亿美元)。预计支出的增加将对市场产生正面影响。

- 千禧世代,尤其是 Z 世代现在正在积极寻找与其核心价值产生共鸣的品牌和场所。整体而言,速食店可以透过积极宣传消费者的价值观来满足消费者对透明度和信任的需求。这可以透过筹款活动和促销活动等以永续来源的成分和可回收和可重复使用的包装为特色的倡议来实现。

预计亚太地区在预测期内将占据主要市场占有率

- 亚太地区是中国和印度等人口稠密的新兴经济体的所在地,这些国家对食品服务的需求正在迅速增长。市场受到对便利性需求激增的推动,转向更健康的饮食选择,导致永续包装的采用显着增加,预计在预测期内将达到顶峰。这些趋势有望将该地区转变为技术创新和业务成长的中心。

- 该地区对行动食品服务站的需求正在迅速增长。这一增长的主要驱动力是都市化的加速、生活方式的日益忙碌以及人们对外出就餐的渴望不断增长。

- 例如,2023 年 6 月,香港一家由学生主导的食品服务新兴企业推出了可重复使用碗的环保租赁服务。 11 家餐厅和 300 名註册用户参与了这项创新倡议。这些区域性运动预计将提高餐饮业对可重复使用产品包装的认识。

- 亚太地区塑胶污染的迅速上升正促使该地区各国政府实施旨在减少塑胶废弃物和推广永续包装解决方案的政策。 2022年,印度政府在包括食品服务业在内的多个行业禁止使用一次性塑料,加速了全国对多用途包装产品的需求。

- 此外,随着劳动力的成长和忙碌的生活方式,日本、中国、印度和印尼等国家的消费者外出用餐支出正在增加。例如,根据内务部/统计局 2024 年 2 月发布的报告,日本家庭每年平均外出用餐支出将从 2021 年的 8,110 日圆(51 美元)增加到 2023 年,仅用三年时间几年来,它迅速上涨至11,110 日圆(70 美元)。

可重复使用的食品服务包装产业概述

研究的市场是分散的,大型供应商控制着大部分市场占有率。市场上许多公司的存在会影响服务的定价,并且是一个直接的竞争因素,特别是对于较小的供应商。受调查的市场中的供应商可能会专注于提供一站式服务,以获得竞争优势。该市场的主要参与者包括 Berry Global Inc.、Ecolab Services、Genpak LLC 和 Enpak Enterprise。

- 2024 年 2 月:Berry Global 推出一系列可重复使用的餐具,以满足食品服务业对永续包装不断增长的需求。这项措施出台之际,立法和消费者需求正在推动该产业转向更环保的包装解决方案。根据该公司食品服务副总裁介绍,新系列可重复使用餐具旨在减少废弃物、减少对新资源的依赖,并在满足法律标准的同时确保功能性和耐用性。

- 2024 年 5 月:服务用品和食品包装开发商 deSter 与特种材料公司 Eastman 合作,向航空公司推出可重复使用的机上饮料器具。包装采用 Tritan Renew,这是一种由回收分子共聚酯製成的特殊塑胶。该材料在部署过程中将塑胶废弃物分解为其基本化学成分,从而实现多次回收循环。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 替代品的威胁

- 新进入者的威胁

- 竞争公司之间的敌对关係

- 产业价值链分析

- 评估近期地缘政治情境对产业的影响

- 在当前场景下可重复使用和一次性使用的安全解决方案

第五章市场动态

- 市场驱动因素

- 对线上食品宅配服务的需求不断增长

- 人们对环境永续性的认识不断增强,对一次性塑胶包装的严格规定

- 市场限制因素

- 重复使用塑胶包装的意外后果和健康问题

第六章 市场细分

- 依材料类型

- 金属

- 塑胶

- 玻璃

- 其他材料类型

- 依产品类型

- 纸板和纸箱

- 瓶子和玻璃

- 托盘、盘子、食品容器、碗

- 杯子和盖子

- 翻盖式

- 其他产品类型

- 按最终用户产业

- 速食店 (QSR)

- 全方位服务餐厅 (FSR)

- 机构

- 款待

- 其他最终用户产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲/纽西兰

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 中东/非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 北美洲

第七章 竞争格局

- 公司简介

- Berry Global Inc.

- Ecolab services

- deSter Corporation

- Genpak LLC

- Pactiv Evergreen Inc.

- Limepack

- Re:Dish Co.

- Verive

- Evergreen Packaging

- Enpak Enterprise Co. Ltd

第八章投资分析

第九章 市场机会及未来趋势

The Reusable Foodservice Packaging Market size is estimated at USD 24.96 billion in 2024, and is expected to reach USD 32.27 billion by 2029, growing at a CAGR of 5.27% during the forecast period (2024-2029).

The global reusable packaging market is set for significant growth, fueled by a rising need for durable and sustainable material handling solutions. Returnable packaging stands out for its pivotal role in sustainability, curbing the volume of packaging waste that typically ends up in landfills.

Key Highlights

- A diverse urban landscape drives the country's demand for convenient, on-the-go, lightweight foods. In recent years, ready-to-eat and convenient food has evolved into one of the most diverse segments of the global food service, with rising concern about the environment and the escalation in packaging landfills, reusable food service packaging in hotels, full-service restaurants (FSRs), and quick-service restaurants (QSRs).

- Several government bodies worldwide impose strict guidelines for using reusable packaging across sectors. For instance, the SUP Directive mandates that EU Member States actively reduce single-use plastic waste, setting specific reduction targets at local and national levels. In tandem with restrictions, these states are advocating for reusable food packaging to achieve these goals.

- In France, recent legislation mandates that all on-site meals or snacks be consumed using reusable packaging or crockery.

- Over the past few years, the online food ordering and restaurant delivery sector has grown by 20%. As the online food delivery system gains traction, there is a corresponding surge in demand for sustainable food service packaging. As per the China Internet Network Information Center publication in March 2024, the number of online food delivery users in China rose from 418.83 million in 2020 to a whopping 544.54 million in 2023. This uptick is prompting manufacturers to pivot toward eco-friendly reusable packaging solutions.

- However, transitioning from a single-use to a reuse model for plastic packaging in industrial food applications can introduce unforeseen challenges, particularly in hygiene and sensory perception. Reusing plastic packaging carries the risk of heightening chemical contamination and the presence of microplastic particles in food products. Additionally, it may compromise the packaged goods' hygienic standards and sensory consistency.

- Globally, large companies are shifting from the traditional 'catch, fill, and waste' model to a zero-waste lifestyle. They achieve this by making foodservice packaging reusable, thus extending its lifecycle sustainably. This shift not only cuts down on operational costs tied to packaging but also eliminates the need for continual new packaging purchases.

Key Highlights

Reusable Foodservice Packaging Market Trends

Growing Demand From Quick-service Restaurants (QSR) Aids the Market

- Quick-service restaurants (QSRs) offer low-cost food options, focusing on speed of service. Minimal table service and an emphasis on self-service distinguish this group from traditional restaurants. Food and beverages are paid for before consumption at QSRs. Over the last decade, the regional foodservice market, specifically for these countries, has witnessed the growth of several international QSR chains and home-grown brands offering varied cuisines suiting changing consumer preferences.

- With rising awareness of environmental sustainability, several major QSR chains are increasingly focusing on recyclability, compostability, and reusable packaging. Notable players, including Burger King, McDonald's, and Wendy's, have pledged to adopt reusable packaging.

- For instance, McDonald's in France offers 21 reusable containers for dine-in customers. These include red plastic containers for fries, clear plastic beverage glasses, and white plastic cups designed for chicken nuggets.

- The franchise model will be crucial to the rise of QSR chains, which is expected to fuel market growth across the globe in the upcoming period. According to the data published by the International Franchise Association, in April 2024, after a slight downfall during the COVID-19 pandemic, the number of QSR in the United States rose steadily in the past few years from 183.54 thousand in 2020 to 195.51 thousand in 2023. Notably, as per the estimates, the number of QSRs across the country is expected to further improve during the forecast period.

- Further, increased spending on food, driven by a rising preference for on-the-go eating, has bolstered the demand for QSRs, fueling the need for reusable food service packaging. As per the Office for National Statistics (United Kingdom), consumer spending on restaurants and cafes in the United Kingdom skyrocketed in the post-pandemic period to GBP 132.89 billion (USD 169.50 billion). This bolstered spending is expected to consequently impact the market positively.

- Presently, millennials and Gen Z, in particular, actively seek out brands and places that resonate with their core values. Overall, QSRs can align with consumer demands for transparency and authenticity by actively showcasing their values. This can be achieved through initiatives like fundraisers and promotions, which feature sustainably sourced ingredients and recyclable and reusable packaging.

Asia-Pacific is Expected to Hold a Significant Market Share During the Forecast Period

- Asia-Pacific is home to densely populated and emerging economies such as China and India, and the demand for food services is surging. The market is propelled by a surge in demand for convenience, a pivot toward healthier dietary choices, and consequently, a notable uptick in adopting sustainable packaging is projected to peak during the forecast period. These trends transform the region into a technological innovation and business growth center.

- The region is witnessing a rapid surge in the demand for mobile food service stations. This uptick is primarily driven by escalating urbanization, increasingly busy lifestyles, and a heightened appetite for on-the-go dining.

- For instance, in June 2023, a Hong Kong student-led food service start-up introduced an eco-friendly rental service for reusable bowls. Eleven restaurants with 300 registered users have joined this innovative initiative. Such regional developments would bolster the awareness of reusable product packaging in the foodservice sector.

- The surge in plastic pollution in Asia-Pacific has prompted governments across the region to implement policies that aim to reduce plastic waste and promote sustainable packaging solutions. In 2022, the Government of India introduced a ban on single-use plastic in several sectors, including food service, thereby accelerating the demand for multiple-use packaging products across the country.

- Further, with the growing working population and busy lifestyles, consumer spending on eating outside is also increasing in countries like Japan, China, India, and Indonesia. For instance, according to the Ministry of Internal Affairs and Communications (Japan) and Statistics Bureau of Japan's report published in February 2024, the annual average household expenditure on dining out in Japan increased rapidly from JPY 8.11 thousand (USD 0.051 thousand) in 2021 to JPY 11.11 (USD 0.070 thousand) in just three years ending 2023.

Reusable Foodservice Packaging Industry Overview

The market studied is fragmented, with major vendors accounting for most of the market share. The presence of many players in the market impacts the pricing of services, making it a direct competing factor, especially for small-scale vendors. The vendors in the market studied are expected to focus on providing one-stop-shop services, giving them a competitive advantage. Some of the major players in the market are Berry Global Inc., Ecolab Services, Genpak LLC, and Enpak Enterprise Co. Ltd.

- February 2024: Berry Global launched its Reusable Tableware Range to address the incremental demand for sustainable packaging across the food service industry. This move comes as legislation and consumer demands push the sector towards more eco-friendly packaging solutions. According to the company's Vice President of Food Service division, the new range of reusable tableware aims to cut waste, lessen reliance on new resources, and ensure functionality and durability while meeting legislative standards.

- May 2024: deSter, a developer of serviceware and food packaging, and Eastman, a specialty materials company, collaborated to introduce reusable in-flight drinkware to the airline sector. The packaging utilizes Tritan Renew, a specialty plastic crafted from recycled molecular copolyester. During its development, plastic waste is broken down into its fundamental chemical components, enabling the material to undergo multiple recycling cycles.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of Substitutes

- 4.2.4 Threat of New Entrants

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of Recent Geopolitical Scenario on the Industry

- 4.5 Reusable vs Single-user Safer Solution in Current Scenario

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand In Online Food Delivery Service

- 5.1.2 Incremental Awareness For Environmental Sustainability and Stringent Regulations Against Single-Use Plastic Packaging

- 5.2 Market Restraints

- 5.2.1 Unforeseen Consequences of Reusing Plastic Packaging and Health Related Concerns

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Metal

- 6.1.2 Plastic

- 6.1.3 Glass

- 6.1.4 Other Material Types

- 6.2 By Product Type

- 6.2.1 Corrugated Boxes And Cartons

- 6.2.2 Bottles and Glasses

- 6.2.3 Trays, Plates, Food Containers, and Bowls

- 6.2.4 Cups And Lids

- 6.2.5 Clamshells

- 6.2.6 Other Product Types

- 6.3 By End-user Industry

- 6.3.1 Quick-service Restaurants (QSR)

- 6.3.2 Full-service Restaurants (FSR)

- 6.3.3 Institutional

- 6.3.4 Hospitality

- 6.3.5 Other End-user Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.2.4 Italy

- 6.4.2.5 Spain

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 Australia and New Zealand

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Argentina

- 6.4.4.3 Mexico

- 6.4.5 Middle East and Africa

- 6.4.5.1 Saudi Arabia

- 6.4.5.2 United Arab Emirates

- 6.4.5.3 South Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Berry Global Inc.

- 7.1.2 Ecolab services

- 7.1.3 deSter Corporation

- 7.1.4 Genpak LLC

- 7.1.5 Pactiv Evergreen Inc.

- 7.1.6 Limepack

- 7.1.7 Re:Dish Co.

- 7.1.8 Verive

- 7.1.9 Evergreen Packaging

- 7.1.10 Enpak Enterprise Co. Ltd

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

食品服务包装市场-全球产业规模、份额、趋势、机会及预测(依材料、包装类型、应用、地区及竞争格局划分,2021-2031年)

食品服务包装市场-全球产业规模、份额、趋势、机会及预测(依材料、包装类型、应用、地区及竞争格局划分,2021-2031年) 食品服务包装市场-2026-2031年预测

食品服务包装市场-2026-2031年预测 餐饮包装市场规模、份额及成长分析(依材料、包装类型、应用及地区划分)-2026-2033年产业预测

餐饮包装市场规模、份额及成长分析(依材料、包装类型、应用及地区划分)-2026-2033年产业预测 食品服务包装用生物分解性塑胶市场:全球市场规模、成长及至2034年预测

食品服务包装用生物分解性塑胶市场:全球市场规模、成长及至2034年预测 2025 年至 2033 年线上食品配送包装市场报告(按产品类型(容器、盘子、碗、杯子等)、材料(塑胶、纸和纸板、铝等)和地区)2026 年至 2032 年食品服务包装市场(依包装类型、最终用途、包装形式及地区划分)全球食品服务包装市场:产业分析、规模、份额、成长、趋势与预测(2025-2032 年)

2025 年至 2033 年线上食品配送包装市场报告(按产品类型(容器、盘子、碗、杯子等)、材料(塑胶、纸和纸板、铝等)和地区)2026 年至 2032 年食品服务包装市场(依包装类型、最终用途、包装形式及地区划分)全球食品服务包装市场:产业分析、规模、份额、成长、趋势与预测(2025-2032 年) 线上食品配送包装市场报告:趋势、预测和竞争分析(至 2031 年)

线上食品配送包装市场报告:趋势、预测和竞争分析(至 2031 年) 北美食品服务包装:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)食品服务包装:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

北美食品服务包装:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)食品服务包装:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)