|

市场调查报告书

商品编码

1626294

保护性包装:市场占有率分析、产业趋势、统计和成长预测(2025-2030)Protective Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

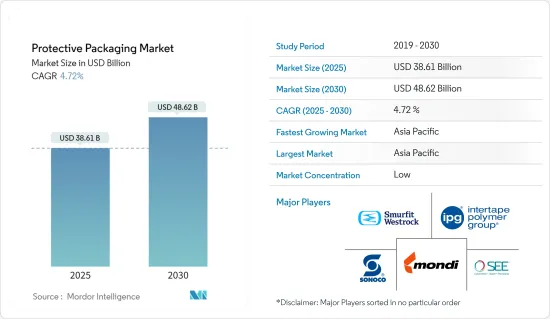

预计2025年保护性包装市场规模为386.1亿美元,预计2030年将达486.2亿美元,预测期内(2025-2030年)复合年增长率为4.72%。

主要亮点

- 物流和物料输送技术的不断发展和创新正在显着发展,新一代的包装产品正在被采用。保护性包装可确保产品在交付时保持与新产品相同的状态。包装不当会严重影响产品的形式和功能。

- 网路购物在消费者中的普及负责产品设计、包装、挑选、履约和运输。因此,产品保护被认为是最重要的问题之一。包装材料的技术发展和电子商务的快速崛起正在主要改变大多数企业选择保护性包装的方式。关键点是性能、先进材料造成的成本问题、包装要求、按需包裹递送系统和永续性。

- 使用软保护包装代替硬包装可显着降低运输成本和重量。据软包装协会(FPA)称,透过製造方法和材料的创新,某些软包装的重量已减轻约50%。

- 软包装还可以节省空间,使得运输大量货物成为可能,同时减少燃料和能源消耗。消费者在决策流程中必须考虑运输成本。与零售应用程式不同,电子商务减少了对单个单位而不是批量单位的运输。

- 对保护性包装不断增长的需求正在吸引企业投资该市场。包装产业併购很常见,成长空间不大。由于包装行业高度依赖终端市场,企业必须寻找併购机会来发展业务并保持竞争力。

- 2023 年 10 月,MacFarlane 以 385 万欧元收购了位于南安普敦的防护包装企业 B&D Group。该公司表示,此次收购是其透过有机和收购成长建立保护性包装业务策略的一部分。 B&D 为英国越来越多的航太、国防和太空产业客户提供服务。 B&D 有大量机会为现有客户提供进一步的包装解决方案,并在 B&D 擅长的领域吸引新客户。

- 然而,食品服务业禁止使用发泡聚苯乙烯(EPS)包装预计将阻碍市场成长。根据新的州法律,纽约居民和企业禁止使用发泡聚苯乙烯 (EPS) 包装。纽约州的禁令禁止销售或分销含有 EPS 泡沫的一次性食品服务容器。

防护包装市场趋势

软保护包装实现稳定成长

- 塑胶软包装是保护性包装的理想选择,因为它能可靠地吸收衝击,提供出色的绝缘包装,并保持清洁度,这在运输食品和药品时极为重要。塑胶也可以回收。此外,其重量轻可让您在运输过程中节省资源。也可用于製作空气枕等超轻包装材料。行业公司正在转向使用可回收材料进行保护性包装。

- 例如,据透露,亚马逊计划在 2023 年 11 月将多项全球创新技术引入印度,生产坚固、耐用且可回收的纸质包装,同时继续努力消除交付中的塑胶包装。

- 近年来,亚马逊一直在探索将产品交付改为纸本交付的方法。履约中心是美国第一个使用可回收纸包装并不再使用塑胶的履行中心。这项转变是透过改造现有的用纸设备、开发坚固且灵活的纸包装、推进定制技术以及用纸填充材取代塑胶气垫来实现的。

- 此外,产业参与者正在使用可回收塑胶为众多产业生产柔性保护包装。聚丙烯和可回收材料等先进包装材料的更多使用可以提供更高的污染和温度屏障,保护包装产品免受损坏。对可回收性的日益关注迫使製造商回收塑胶废弃物。为此,Sealed Air 使用 30% 或 50% 的回收塑胶废弃物开发了新型气泡膜保护包装。

- 此外,不断扩大的电子商务市场将增强对柔性保护包装解决方案的需求。电子商务公司越来越重视永续包装材料,进一步推动了该市场的成长。美国商务部下属的美国人口普查局的资料显示,2024年第二季电子商务将占美国零售总额的16%,高于上一季的15.80%。

亚太地区预计将占据主要市场占有率

- 印度品牌股权基金会(IBEF)的资料显示,消费性电子产业正在推动该地区的主要需求。 2022年,印度家电及消费性电子产业产值达90.9亿美元。预计到2025年将超过211.8亿美元。

- 耐用品通常会使用很多年,因此必须精心包装,以确保它们以原始状态到达消费者手中。这些产品在运输过程中存在处理不当的风险,并且容易受到压力和振动的影响。因此,儘管包装面临挑战,但保护性包装的使用至关重要。

- 印度製造业正在经历重大变革时期。 「印度製造」等倡议加强了印度的本土製造业,并将该国定位为电子和消费性电子产品製造的重要中心。这些行业越来越依赖保护性包装来保护运输过程中的产品,并且对这些解决方案的需求正在迅速增加。这些动态正在推动该地区保护性包装市场的成长。

- 市场的主要趋势之一是增加研发投资,以开发环保和永续的包装材料。供应商正在投资创新技术来开发可回收和再利用的包装材料。

- 例如,2023年6月,陶氏化学与宝洁中国推出用于电商包装的单PE空气胶囊。与传统纸板小包裹箱相比,这项创新减少了材料使用量并减轻了 40% 以上的重量。包装采用来自陶氏的精英 AT PE 树脂,以提高可回收性并取代传统的多材料选择。其设计注重可靠性和易用性,开口是砸道机的,以增加安全性。

防护包装产业概况

保护性包装市场的竞争格局较为分散,主要企业参与者包括 Intertape Polymer Group Inc.、Sonoco Products Company、Smurfit Westrock、Sealed Air Corporation 和 DS Smith PLC。这些供应商正在积极推出新产品、扩大业务、合併和收购公司以增加市场占有率。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

第五章市场动态

- 市场驱动因素

- 对电子商务产品的需求不断增长

- 软保护包装产品的需求

- 市场限制因素

- 关于可降解性的严格规定

第六章 市场细分

- 依产品类型

- 难的

- 纸板保护器

- 纸浆模塑

- 隔热运输货柜

- 其他硬质产品类型

- 柔软的

- 保护邮件

- 气泡膜

- 空气枕/气囊

- 纸填充

- 其他柔性产品类型(铝箔袋/袋、拉伸膜、收缩膜等)

- 形式

- 发泡成型製品

- 就地表格 (FIP)

- 鬆散填充

- 发泡卷材/片材

- 其他泡沫类型(角块等)

- 难的

- 按最终用户产业

- 饮食

- 工业的

- 药品

- 家电

- 美容/家庭护理

- 其他最终用户产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 亚洲

- 中国

- 日本

- 印度

- 澳洲/纽西兰

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 中东/非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 埃及

- 南非

- 北美洲

第七章 竞争格局

- 公司简介

- Intertape Polymer Group Inc.

- Pregis Corporation

- Riverside Paper Co.

- Sealed Air Corporation

- Signode Industrial Group LLC

- Sonoco Products Company

- Smurfit Westrock

- Huhtamaki Group

- DS Smith PLC

- International Paper Company

- Pro-Pac Packaging Limited

- Storopack Hans Reichenecker GmbH

- Mondi Group

第八章投资分析

第九章 市场未来展望

The Protective Packaging Market size is estimated at USD 38.61 billion in 2025, and is expected to reach USD 48.62 billion by 2030, at a CAGR of 4.72% during the forecast period (2025-2030).

Key Highlights

- The ongoing development and innovation in logistics and material handling technology have significantly evolved, and new-generation packaging products have been adopted. Protective packaging ensures that a product remains as intact as new upon delivery. The lack of proper packaging can seriously affect a product's shape and function.

- The popularity of online shopping among consumers is responsible for product design, packaging, picking, fulfillment, and shipping. Therefore, product protection is regarded as one of the most critical issues. The technological developments in packaging material and the exponential rise of e-commerce are primarily altering how most businesses choose protective packaging. The primary points are performance, cost issues brought on by material advancements, packaging requirements, on-demand package delivery systems, and sustainability.

- Transport costs and weight are significantly lower when flexible protective packaging is used instead of rigid packaging. According to the Flexible Packaging Association (FPA), specific flexible packaging has seen a weight reduction of about 50% due to innovations in production methods and materials.

- Also, flexible packaging allows space-saving opportunities, which enables the shipping of large quantities of goods while using less fuel and energy. Consumers must take into account the cost of delivery during the decision-making process. Unlike retail applications, e-commerce scales down shipping into individual units rather than bulk units.

- The growing demand for protective packaging attracts players to invest in the market. M&A is common in the packaging industry, as there is little room for growth. The packaging industry is highly dependent on end markets, so players must look for M&A opportunities to grow their business and remain competitive.

- In October 2023, Macfarlane acquired a Southampton-based protective packaging business, B&D Group, for EUR 3.85 million. The company stated that the acquisition was part of its strategy to build its protective packaging business through organic and acquisition growth. B&D serves customers in the expanding aerospace, defense, and space industries across the United Kingdom and internationally. There are considerable opportunities to deliver further packaging solutions to existing customers and grow new customers in sectors where B&D excels.

- However, a ban on the use of expanded polystyrene foam (EPS) packaging for food service is expected to hinder market growth. New York State residents and businesses are prohibited from using expanded polystyrene foam (EPS) packaging under the new state law. New York's ban will prohibit anyone from selling or distributing disposable food service containers containing EPS foam.

Protective Packaging Market Trends

Flexible Protective Packaging to Execute a Steady Growth Rate

- Plastic-based flexible packaging material is excellent for protective packing because it reliably absorbs shocks, insulates well, and is incredibly clean, which is crucial when sending food and medications. Plastic can also be recycled. Additionally, it is lightweight, saving resources during transportation. It can also be used to create ultralightweight packaging materials such as air pillows. Industry players are focusing on recyclable materials for protective packaging.

- For instance, in November 2023, Amazon disclosed its intention to bring several global innovations into India for manufacturing strong, durable, recyclable paper packaging as Amazon continues its efforts to eliminate plastic packaging from its deliveries.

- In recent years, Amazon has sought ways to transition its product deliveries to paper. The fulfillment center in Euclid, Ohio, became the first in the United States to adopt curbside-recyclable paper packaging, moving away from plastic. This shift was achieved by retrofitting existing paper-use equipment, developing robust and flexible paper packaging, advancing made-to-fit technology, and replacing plastic air cushions with paper fillers.

- Additionally, players are using recyclable plastic to produce flexible protective packaging across numerous industries. Advanced packaging materials, such as polypropylene and increased use of recyclable material, can provide a high barrier against contamination and temperatures, protecting the packaged product from damage. The growing recyclability concerns are forcing manufacturers to recycle plastic waste. In line with this, Sealed Air has developed a range of new bubble wrap protective packaging that uses 30% or 50% recycled plastic waste.

- Also, the expanding e-commerce market is poised to bolster the demand for flexible protective packaging solutions. E-commerce companies increasingly prioritize sustainable packaging materials, further fueling this market's growth. Data from the US Census Bureau, part of the US Department of Commerce, reveals that in the second quarter of 2024, e-commerce accounted for 16% of total retail sales in the United States, marking an increase from the prior quarter's 15.80%.

Asia-Pacific is Expected to Occupy Significant Market Share

- The consumer electronics segment is driving significant demand in the region as per data from the India Brand Equity Foundation (IBEF). The Indian appliances and consumer electronics industry was valued at USD 9.09 billion in 2022. Projections indicate a robust growth trajectory, expected to exceed USD 21.18 billion by 2025.

- Consumer durables, typically used for years, require meticulous packaging to ensure they reach consumers in pristine condition. These items are at risk of improper handling during transport and are vulnerable to stress and vibration. Consequently, while packaging poses challenges, the use of protective packaging becomes paramount.

- India's manufacturing industry is undergoing a significant transformation. Initiatives like 'Make in India' bolstered indigenous production, positioning India as a key hub for electronics and home appliance manufacturing. As these industries increasingly rely on protective packaging to safeguard their products during transit, the demand for such solutions is surging. Collectively, these dynamics are fueling the growth of the protective packaging market in the region.

- One significant trend in the market is the increased investment in research and development to develop environmentally friendly and sustainable packaging materials. Vendors are investing in innovative technologies to develop packaging materials that can be recycled and reused.

- For instance, in June 2023, Dow and Procter & Gamble China introduced a mono-PE air capsule for e-commerce packaging. This innovation reduces material usage and achieves a weight reduction exceeding 40% compared to conventional corrugated parcel boxes. The packaging utilizes ELITE AT PE resins sourced from Dow, enhancing recyclability and replacing traditional multi-material options. Emphasizing reliability and user-friendliness, the design features a tamper-free opening to enhance security.

Protective Packaging Industry Overview

The protective packaging market features a fragmented competitive landscape with a diverse array of vendors such as Intertape Polymer Group Inc., Sonoco Products Company, Smurfit Westrock, Sealed Air Corporation, and DS Smith PLC are key players. These vendors actively pursue new product launches, expansions, mergers, and acquisitions to bolster their market share.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand for E-commerce-based Products

- 5.1.2 Demand for Flexible Protective Packaging Products

- 5.2 Market Restraints

- 5.2.1 Stringent Regulations Related to Degradability

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Rigid

- 6.1.1.1 Corrugated Paperboard Protectors

- 6.1.1.2 Molded Pulp

- 6.1.1.3 Insulated Shipping Containers

- 6.1.1.4 Other Rigid Product Types

- 6.1.2 Flexible

- 6.1.2.1 Protective Mailers

- 6.1.2.2 Bubble Wraps

- 6.1.2.3 Air Pillows/Air Bags

- 6.1.2.4 Paper Fill

- 6.1.2.5 Other Flexible Product Types (Foil Pouches/Bags, Stretch and Shrink Films, etc.)

- 6.1.3 Foam

- 6.1.3.1 Molded Foam

- 6.1.3.2 Foam in Place (FIP)

- 6.1.3.3 Loose Fill

- 6.1.3.4 Foam Rolls/Sheets

- 6.1.3.5 Other Foam Types (Corner Blocks, etc.)

- 6.1.1 Rigid

- 6.2 By End-user Industry

- 6.2.1 Food and Beverage

- 6.2.2 Industrial

- 6.2.3 Pharmaceuticals

- 6.2.4 Consumer Electronics

- 6.2.5 Beauty and Home Care

- 6.2.6 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Italy

- 6.3.2.5 Spain

- 6.3.3 Asia

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.5.1 Brazil

- 6.3.5.2 Argentina

- 6.3.5.3 Mexico

- 6.3.6 Middle East and Africa

- 6.3.6.1 Saudi Arabia

- 6.3.6.2 United Arab Emirates

- 6.3.6.3 Egypt

- 6.3.6.4 South Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Intertape Polymer Group Inc.

- 7.1.2 Pregis Corporation

- 7.1.3 Riverside Paper Co.

- 7.1.4 Sealed Air Corporation

- 7.1.5 Signode Industrial Group LLC

- 7.1.6 Sonoco Products Company

- 7.1.7 Smurfit Westrock

- 7.1.8 Huhtamaki Group

- 7.1.9 DS Smith PLC

- 7.1.10 International Paper Company

- 7.1.11 Pro-Pac Packaging Limited

- 7.1.12 Storopack Hans Reichenecker GmbH

- 7.1.13 Mondi Group

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET

全球包装花生市场:预测(至 2032 年)-按产品、材料、类型、分销管道和地区进行分析

全球包装花生市场:预测(至 2032 年)-按产品、材料、类型、分销管道和地区进行分析 全球纸边保护器市场

全球纸边保护器市场 全球泡棉保护包装市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测保护性包装市场规模、份额和趋势分析报告:按类型、材料、功能、最终用途、地区和细分市场预测,2025 年至 2033 年

全球泡棉保护包装市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测保护性包装市场规模、份额和趋势分析报告:按类型、材料、功能、最终用途、地区和细分市场预测,2025 年至 2033 年 全球瓦楞纸边缘保护器市场:绩效及预测(2020-2031年)柔性保护包装市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

全球瓦楞纸边缘保护器市场:绩效及预测(2020-2031年)柔性保护包装市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 保护性包装市场规模、份额及成长分析(按类型、材料、功能、最终用途和地区)-2025-2032 年产业预测

保护性包装市场规模、份额及成长分析(按类型、材料、功能、最终用途和地区)-2025-2032 年产业预测 北美保护性包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)

北美保护性包装:市场占有率分析、行业趋势和成长预测(2025-2030 年) 2025 年保护性包装全球市场报告保护性包装市场:未来预测(2025-2030)

2025 年保护性包装全球市场报告保护性包装市场:未来预测(2025-2030)